Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Saudi Arabian warehousing aggregator market is valued at approximately USD ~ billion, driven by the growth in logistics, e-commerce, and the manufacturing sectors. The demand for warehousing services has surged due to the rapid expansion of these industries, as businesses increasingly rely on third-party logistics providers for efficient supply chain management. This growth is further supported by government initiatives to modernize the infrastructure, particularly within the logistics and transportation sectors, under its Vision 2030 goals.

The dominant cities in Saudi Arabia driving the warehousing aggregator market are Riyadh, Jeddah, and Dammam. Riyadh’s central location and strong transportation infrastructure, including its proximity to key highways and rail systems, make it a strategic hub for logistics and warehousing. Jeddah, with its major port, is a key player in the maritime logistics sector, while Dammam’s growing industrial base contributes to the demand for large-scale warehousing. These cities play a critical role in shaping the market due to their strategic positions within the country’s logistics ecosystem.

Market Segmentation

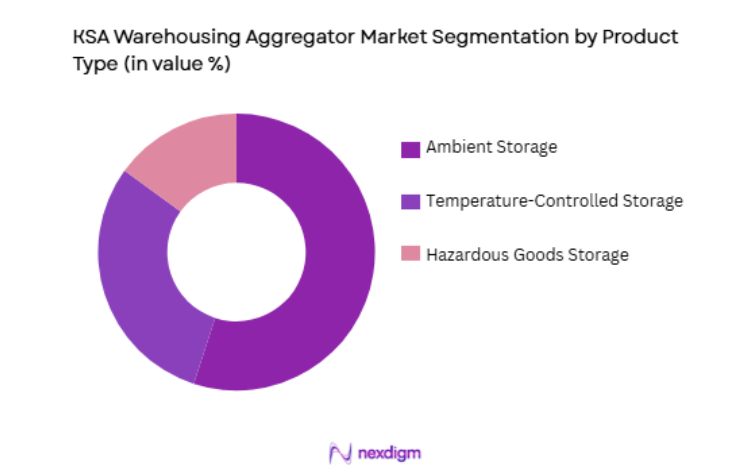

By Product Type

The Saudi warehousing aggregator market is segmented by product type into ambient storage, temperature-controlled storage, and hazardous goods storage. Recently, ambient storage has emerged as the dominant sub-segment due to the rising demand for retail and e-commerce goods, which typically do not require temperature regulation. The availability of large, cost-effective warehouses, particularly in Riyadh and Jeddah, has further contributed to the growing dominance of ambient storage. The rise in cross-border e-commerce and the shift to online shopping have made ambient storage facilities more popular, as they can accommodate a wide range of products, such as consumer electronics and apparel, that don’t necessitate specific temperature control.

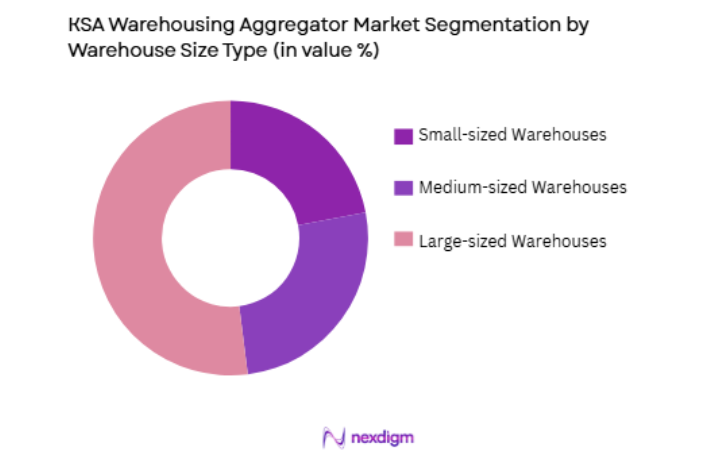

By Warehouse Size

The Saudi warehousing aggregator market is segmented by warehouse size into small, medium, and large-sized warehouses. Recently, large-sized warehouses have dominated the market due to the increasing demand for large-scale storage to accommodate rising product volumes, especially in the fast-growing e-commerce and retail sectors. These large warehouses are primarily located in logistics hubs such as Riyadh and Jeddah, which benefit from proximity to transportation networks and key industries. The trend of multi-story and high-capacity facilities enables businesses to store significant amounts of inventory, thus driving the preference for large-sized warehouses in the region.

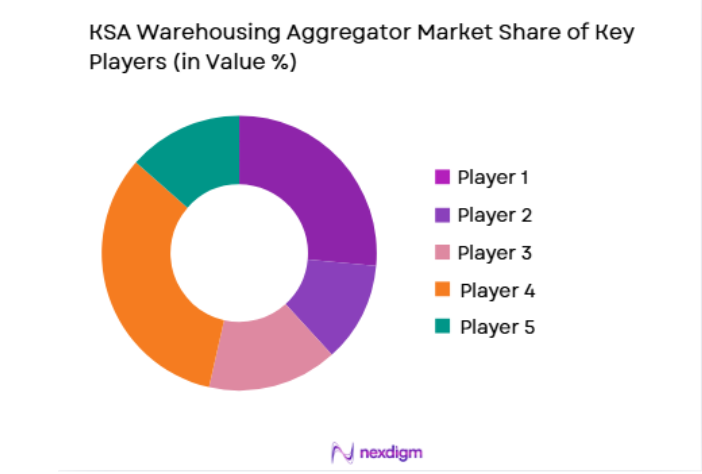

Competitive Landscape

The competitive landscape of the Saudi warehousing aggregator market is marked by consolidation, with both regional and global players competing for market share. Major players focus on expanding their service offerings by integrating advanced technology such as automation, AI-driven inventory management, and IoT for enhanced warehouse efficiency. These players are also forming strategic alliances to expand their footprint and enhance service offerings. The market is witnessing a rise in tech-driven warehousing solutions, offering significant potential for businesses to optimize supply chains.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Logistics Integration Strategy |

| Saudi Logistics Group | 1995 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Aramex Logistics | 1982 | Dubai | ~ | ~ | ~ | ~ | ~ |

| National Shipping Co. | 1983 | Jeddah | ~ | ~ | ~ | ~ | ~ |

| Bahri Logistics | 1978 | Dammam | ~ | ~ | ~ | ~ | ~ |

| Almarai Logistics | 1977 | Riyadh | ~ | ~ | ~ | ~ | ~ |

KSA Warehousing Aggregator Market Analysis

Growth Drivers

Expansion of E-commerce in Saudi Arabia

The e-commerce sector in Saudi Arabia has witnessed exponential growth in recent years, and it continues to be a key growth driver for the warehousing aggregator market. With the rise of online shopping platforms, businesses are increasingly looking for efficient warehousing solutions that can accommodate the growing volume of products being sold online. The growth of e-commerce platforms such as Noon and Souq has significantly increased the demand for storage facilities, particularly in urban centers like Riyadh and Jeddah. Moreover, government initiatives to support digital transformation, such as the “E-commerce Strategy,” are expected to further boost the demand for efficient warehousing services. As online retailers seek faster delivery times, they are increasingly investing in local warehousing solutions that allow for quicker stock turnover and inventory management. This shift has led to an increased demand for large warehouses with advanced technological features, including automated inventory management systems, to ensure optimal storage and distribution capabilities.

Government Infrastructure Investments

The Saudi government has been actively investing in its logistics and transportation infrastructure under Vision 2030, which includes expanding the warehousing and distribution sector. These investments include developing new logistics hubs, expanding existing ports, and enhancing transport networks that connect key cities like Riyadh, Jeddah, and Dammam. The government’s emphasis on improving infrastructure is a crucial driver for the warehousing aggregator market, as it enables smoother supply chain operations and fosters growth in sectors such as retail, manufacturing, and pharmaceuticals. Additionally, the government’s push for modernization, which includes introducing smart logistics and enhancing last-mile delivery capabilities, is also contributing to the rapid growth of the warehousing aggregator market. These infrastructure improvements are driving demand for both large and small warehousing solutions, which can accommodate the evolving needs of businesses across the country.

Market Challenges

High Operational Costs in Warehousing

The Saudi warehousing aggregator market faces significant challenges related to high operational costs, particularly in terms of real estate and labor. The increasing cost of land in major logistics hubs like Riyadh and Jeddah puts pressure on businesses to secure affordable warehouse spaces. Furthermore, the cost of maintaining a warehouse, including utilities, labor, and technology, is rising. With an increasing demand for larger and more advanced facilities, the associated costs are becoming a major challenge for businesses seeking to stay competitive while keeping operating expenses under control. To remain profitable, warehousing aggregators must focus on cost-efficiency, optimizing warehouse management, and utilizing automation to reduce manual labor costs. However, balancing these operational costs while still providing high-quality services is an ongoing challenge in the market.

Technological Integration and System Compatibility

While the introduction of advanced technologies such as AI, IoT, and robotics is transforming the warehousing industry, the integration of these technologies into existing systems remains a challenge. Many warehousing operators in Saudi Arabia face difficulties in adopting and integrating these technologies into their operations due to the complexity of supply chain systems and the high cost of implementation. In addition, the compatibility of various systems—such as inventory management software, robotics, and automation systems—remains a significant hurdle. This challenge is compounded by the varying technological readiness levels of businesses, especially among smaller operators who may lack the financial resources to invest in the latest technologies. Successful adoption of these technologies is critical to maintaining competitive advantage, but the cost and complexity of integration are significant barriers to widespread adoption.

Opportunities

Investment in Smart Warehousing Solutions

One of the key opportunities in the Saudi warehousing aggregator market is the investment in smart warehousing solutions. The growing need for automation and real-time inventory management presents an opportunity for businesses to implement AI-driven solutions, robotics, and IoT technologies. By utilizing these advanced solutions, warehousing aggregators can optimize space utilization, reduce labor costs, and improve order accuracy and delivery speeds. Additionally, the increasing adoption of blockchain for supply chain transparency offers a further opportunity for aggregators to enhance the trust and efficiency of their operations. As more businesses seek integrated, tech-driven logistics solutions, the demand for smart warehouses that provide real-time monitoring, automated picking systems, and predictive maintenance is expected to increase. This presents a significant growth opportunity for companies operating in the Saudi warehousing aggregator market.

Sustainability and Green Warehousing

With increasing environmental awareness, there is a growing opportunity for warehousing aggregators to adopt sustainable practices in their operations. Implementing green warehousing solutions, such as energy-efficient systems, renewable energy sources, and waste reduction strategies, offers both environmental and economic benefits. The Saudi government’s commitment to sustainability, including its Vision 2030 objectives, aligns with this trend, encouraging businesses to adopt eco-friendly practices. The rise in demand for green logistics solutions presents a promising opportunity for warehousing aggregators to differentiate themselves in the market. By investing in sustainable technologies, such as solar-powered warehouses and energy-efficient refrigeration systems, companies can attract environmentally conscious clients and reduce operational costs over time.

Future Outlook

The future outlook for the Saudi warehousing aggregator market is highly positive, with continued growth expected over the next few years. Technological advancements, including automation, AI, and robotics, will drive the market toward more efficient and scalable solutions. Government investments in infrastructure development, such as new ports, roads, and logistics parks, will further facilitate the growth of warehousing services in the region. As e-commerce and industrial sectors continue to expand, the demand for modern and integrated warehousing solutions will remain strong. Warehousing aggregators that invest in smart technologies and sustainability will be well-positioned to capture market share.

Major Players

- Saudi Logistics Group

- Aramex Logistics

- National Shipping Co.

- Bahri Logistics

- Almarai Logistics

- Agility Logistics

- Kuehne + Nagel

- DB Schenker

- XPO Logistics

- CEVA Logistics

- DHL Supply Chain

- Aramex International

- FedEx Logistics

- UPS Supply Chain Solutions

- Maersk Logistics

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Large-scale e-commerce companies

- Logistics service providers

- Retailers and wholesalers

- Manufacturing companies

- Real estate developers focusing on logistics parks

- Freight forwarding companies

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the key market drivers, including technological advancements, demand for warehousing, and government infrastructure investments.

Step 2: Market Analysis and Construction

In this step, the overall market is analyzed, focusing on segments, growth trends, and the competitive landscape, followed by the construction of the market model.

Step 3: Hypothesis Validation and Expert Consultation

Insights from industry experts are used to validate market assumptions and adjust forecasts based on the latest industry trends and expert opinions.

Step 4: Research Synthesis and Final Output

The final market report is generated by synthesizing the collected data, ensuring that it provides a comprehensive and accurate market overview.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E-commerce

Increased Government Investment in Logistics Infrastructure

Rising Demand for Automated Solutions - Market Challenges

High Initial Investment Costs

Technological Integration Issues

Lack of Skilled Workforce - Market Opportunities

Demand for Real-time Inventory Management Solutions

Growth in Warehouse Automation Technologies

Expansion of Logistics Infrastructure in New Regions - Trends

Use of AI and Robotics in Warehousing

Integration of Real-time Data and Analytics

Adoption of Green Technologies for Sustainability - Government regulations

Warehouse Safety Regulations

Environmental and Sustainability Regulations

Regulations on Data Protection and Privacy - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Inventory Management Systems

Order Fulfillment Systems

Warehouse Management Systems

Automated Storage & Retrieval Systems

Warehouse Control Systems - By Platform Type (In Value%)

Cloud-based Platforms

On-premise Platforms

Hybrid Platforms

Mobile Platforms

Integrated Platforms - By Fitment Type (In Value%)

Standalone Solutions

Modular Solutions

Cloud-based Solutions

Hybrid Solutions

Custom Solutions - By EndUser Segment (In Value%)

E-commerce Retailers

Third-party Logistics Providers

Manufacturers

Automotive Industry

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Technology Integration, Service Level, Operational Efficiency, Scalability, Regional Reach)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Al-Rajhi Logistics

Saudi Post

LogiPoint

Aramex

Al-Futtaim Logistics

DHL Supply Chain

Agility Logistics

Kuehne + Nagel

Siemens Logistics

Manhattan Associates

Dematic

Swisslog

JDA Software

Honeywell Intelligrated

XPO Logistics

- E-commerce Companies Seeking Efficient Fulfillment Solutions

- Logistics Providers Pursuing Cost-effective Automation

- Manufacturers Adopting Warehouse Management Systems

- Food & Beverage Industry Focused on Perishable Goods Handling

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now