Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA warehousing market has expanded rapidly alongside growth in logistics infrastructure, retail supply chains, and e commerce distribution networks. Based on a recent historical assessment, the market generated approximately USD ~ billion in warehousing service revenues according to logistics industry data compiled from Saudi logistics sector reports and trade infrastructure statistics. Demand is driven by large scale industrial development, rising imports of consumer goods, and growing regional distribution activity. Expansion of logistics parks, bonded warehouses, and temperature controlled storage facilities is strengthening supply chain capacity across the kingdom.

Riyadh, Jeddah, and Dammam remain the most prominent warehousing hubs due to concentration of industrial activity, large consumer markets, and proximity to major ports and airports. Riyadh hosts extensive logistics zones supporting domestic distribution networks and e-commerce fulfillment operations. Jeddah benefits from port driven trade activity connected to the Red Sea shipping corridor, while Dammam supports logistics operations linked to oil, petrochemicals, and industrial exports. Government backed logistics initiatives and industrial city developments further reinforce these cities as central warehousing and distribution centers.

Market Segmentation

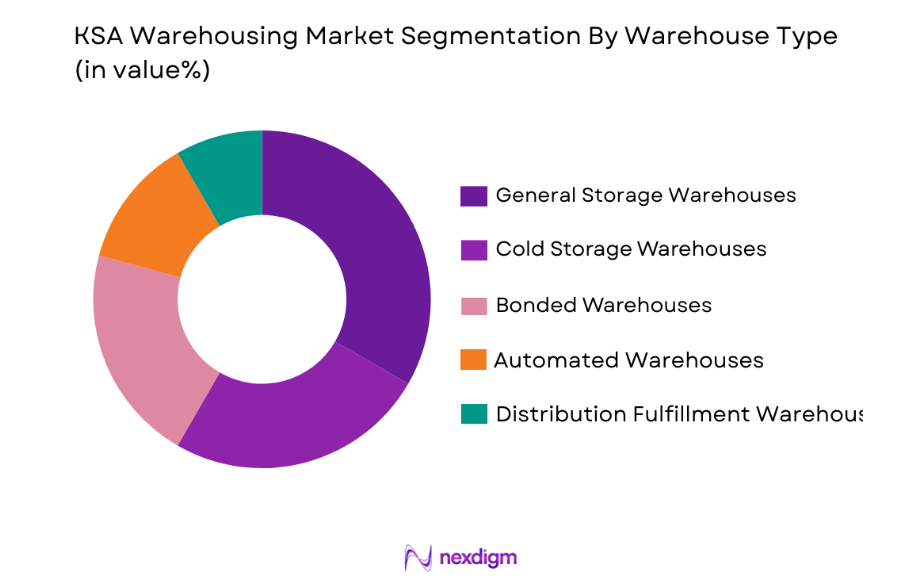

By Warehouse Type

KSA Warehousing market is segmented by warehouse type into general storage warehouses, cold storage warehouses, bonded warehouses, automated warehouses, and distribution fulfillment warehouses. Recently, distribution fulfillment warehouses have a dominant market share due to rapid growth in e commerce logistics and retail distribution across Saudi Arabia. Large retailers and online marketplaces rely heavily on fulfillment centers to manage inventory storage, packaging, and order dispatch operations efficiently. Government investments in logistics parks and industrial zones have increased the availability of large distribution warehouses near major transport corridors. Retail companies and third party logistics providers increasingly prefer centralized fulfillment hubs to reduce transportation time and improve delivery speed. The rise of omnichannel retail and same day delivery services has also increased the demand for technologically advanced warehouses capable of handling large volumes of orders. Automation technologies such as warehouse management systems, robotic picking solutions, and digital inventory tracking further support operational efficiency within fulfillment warehouses. As retail supply chains become more sophisticated, distribution fulfillment warehouses continue to play a central role in the KSA warehousing ecosystem.

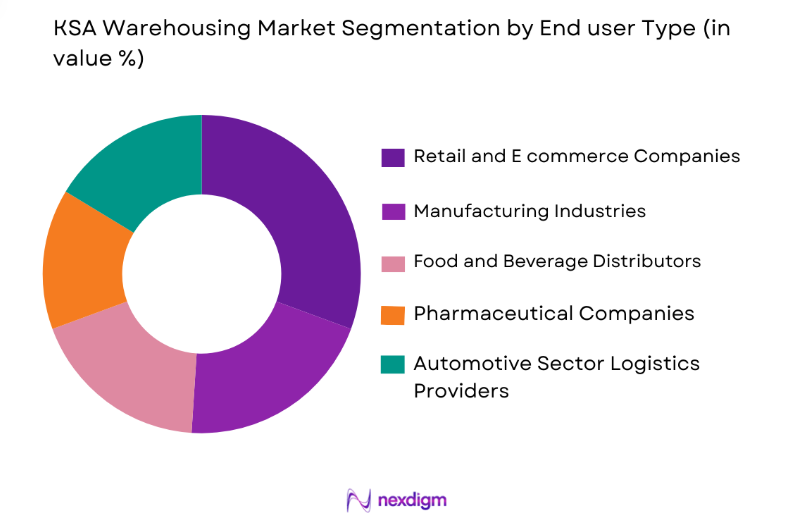

By End User Industry

KSA Warehousing market is segmented by end user industry into retail and e commerce companies, manufacturing industries, food and beverage distributors, pharmaceutical companies, and automotive sector logistics providers. Recently, retail and e commerce companies have a dominant market share due to the rapid expansion of online shopping platforms and organized retail networks in Saudi Arabia. Major online marketplaces and retail chains require extensive warehouse infrastructure to support large scale product storage, inventory management, and last mile distribution operations. The increasing number of digital consumers has accelerated demand for regional distribution centers capable of handling high volumes of parcels. Retail supply chains depend heavily on warehousing networks located near major population centers to reduce delivery times and improve logistics efficiency. Additionally, multinational retail brands entering the Saudi market have expanded their storage and fulfillment operations to support growing demand for consumer goods. Warehousing operators continue to build new logistics facilities tailored for e commerce inventory management, which further strengthens the dominance of the retail and e commerce segment in the overall market.

Competitive Landscape

The KSA warehousing market is moderately consolidated with a mix of international logistics providers and regional warehouse operators competing to expand logistics infrastructure across the kingdom. Global logistics companies have established large distribution networks supported by advanced warehouse automation technologies, while regional players focus on industrial zone developments and local supply chain services. Increasing investments in logistics parks and industrial cities are encouraging new partnerships between warehouse developers, logistics providers, and retail companies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity Focus |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Agility Logistics | 1979 | Kuwait | ~ | ~ | ~ | ~ | ~ |

| Aramex Logistics | 1982 | UAE | ~ | ~ | ~ | ~ | ~ |

| Bahri Logistics | 1978 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Almajdouie Logistics | 1965 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

KSA Warehousing Market Analysis

Growth Drivers

Expansion of E Commerce and Retail Fulfillment Infrastructure in Saudi Arabia

The rapid growth of e commerce platforms across Saudi Arabia has become one of the most important factors accelerating demand for warehousing infrastructure. Online marketplaces and retail companies require large fulfillment centers capable of handling inventory storage, packaging operations, and order dispatch activities to support fast delivery services. Consumers increasingly prefer digital shopping platforms which has significantly increased parcel volumes moving through distribution networks. Warehouses located near major cities enable retailers to shorten delivery times and improve supply chain responsiveness. Advanced warehouse management technologies including automated sorting systems and digital inventory monitoring tools allow companies to process large volumes of orders efficiently. Retail companies also rely on regional distribution centers to manage product availability across multiple cities. Logistics providers are expanding large scale fulfillment facilities designed specifically for online retail operations. Investment in warehouse automation continues to improve operational efficiency within logistics networks. As online commerce expands further, demand for sophisticated warehousing facilities will continue rising across Saudi Arabia.

Government Investment in National Logistics Infrastructure under Vision Development Programs

Saudi Arabia has invested heavily in logistics infrastructure development as part of national economic diversification initiatives. Large scale logistics zones, industrial cities, and integrated transport corridors are being developed to transform the country into a regional trade hub connecting Asia, Europe, and Africa. These projects include expansion of logistics parks, freight terminals, and warehousing clusters designed to support large scale cargo distribution networks. Infrastructure development programs also focus on improving connectivity between ports, airports, highways, and industrial centers. Improved transport connectivity enables faster cargo movement and increases efficiency within supply chains. Government backed initiatives encourage private sector participation in warehouse development and logistics services. Industrial zones across Riyadh, Jeddah, and Dammam have witnessed rapid growth in storage facilities and distribution hubs. Logistics companies are investing in modern warehouses equipped with automation technologies and digital management systems. As infrastructure development progresses, warehousing capacity continues expanding to support the kingdom’s growing trade and logistics ecosystem.

Market Challenges

High Capital Investment Requirements for Modern Warehousing Infrastructure

Developing large scale warehousing infrastructure requires significant financial investment in land acquisition, construction, automation technology, and operational systems. Advanced warehouses equipped with automated storage systems, robotics, and digital inventory platforms demand high upfront capital expenditure. Logistics companies must allocate substantial resources to develop facilities capable of handling large cargo volumes efficiently. In addition to construction costs, operational expenses such as energy consumption, maintenance of automated equipment, and skilled labor requirements also increase financial burdens. Smaller logistics providers often face challenges in accessing sufficient capital to build modern warehouses. Financing limitations can slow expansion of warehouse capacity in certain regions. Land costs near major cities and logistics corridors also contribute to rising development expenses. Investors typically require long term commitments from logistics operators before funding warehouse construction projects. As supply chains become increasingly technology driven, companies must continuously upgrade infrastructure which further increases investment requirements. These financial barriers remain a key challenge affecting growth within the KSA warehousing market.

Limited Availability of Skilled Workforce for Advanced Logistics Operations

Operating modern warehouse facilities increasingly requires skilled professionals capable of managing automated systems, digital inventory tools, and advanced logistics technologies. However, the availability of trained logistics professionals within the region remains relatively limited compared to the rapid pace of warehouse expansion. Many advanced warehouse systems rely on specialized knowledge in robotics operations, data analytics, and warehouse management software. Companies must invest heavily in employee training programs to ensure operational efficiency. Recruitment of skilled logistics engineers and technology specialists can be difficult in certain regions. Workforce shortages may reduce operational productivity and slow implementation of automation technologies. Logistics companies often rely on international expertise to manage complex warehouse systems which can increase operational costs. Training programs and skill development initiatives are gradually improving workforce capabilities but demand continues to exceed supply. As the warehousing sector becomes more technologically advanced, the need for specialized logistics professionals will remain a major operational challenge.

Opportunities

Expansion of Temperature Controlled Warehousing for Food and Pharmaceutical Supply Chains

Demand for temperature controlled storage facilities has increased significantly due to growth in food imports, pharmaceutical distribution, and healthcare supply chains. Cold chain warehousing infrastructure is essential for maintaining product quality and safety during storage and transportation. Saudi Arabia imports large volumes of perishable food products requiring refrigerated storage facilities before distribution to retail markets. Pharmaceutical supply chains also rely heavily on controlled temperature environments to preserve sensitive medical products. Logistics companies are investing in specialized warehouses equipped with advanced refrigeration systems and monitoring technologies. Growth in healthcare services and pharmaceutical manufacturing further increases demand for cold storage facilities. Modern cold chain warehouses integrate digital monitoring systems that track temperature conditions in real time. Expansion of refrigerated transport networks complements cold storage infrastructure across the supply chain. Government initiatives encouraging food security and pharmaceutical production also strengthen demand for specialized warehousing facilities. These factors create strong opportunities for logistics companies investing in cold chain storage capacity.

Development of Smart Warehousing and Automation Technologies

The adoption of automation technologies within warehouse facilities is creating significant opportunities for logistics providers seeking to improve efficiency and productivity. Smart warehouses utilize robotics systems, automated storage solutions, and digital inventory management tools to optimize operations. Automation reduces manual labor requirements while improving accuracy and speed in order processing. Logistics companies increasingly deploy artificial intelligence powered warehouse management systems capable of predicting inventory demand and optimizing storage utilization. Automated sorting systems allow warehouses to handle larger volumes of parcels efficiently. Robotics technologies enable faster picking and packaging operations within fulfillment centers. Digital monitoring systems provide real time visibility into warehouse operations and supply chain performance. Smart warehouse infrastructure also improves safety and reduces operational errors. As logistics networks become more complex, automation technologies offer major advantages in operational scalability. Companies investing in smart warehouse systems will gain competitive advantages within the evolving KSA logistics market.

Future Outlook

The KSA warehousing market is expected to experience steady expansion as logistics infrastructure continues to develop across major economic zones. Growth in e commerce, manufacturing, and retail distribution will increase demand for large scale storage facilities and distribution centers. Technological adoption including automation and digital warehouse management systems will improve operational efficiency across logistics networks. Government initiatives aimed at strengthening Saudi Arabia’s position as a global logistics hub will further support infrastructure development and investment in modern warehouse facilities.

Major Players

- DHL Supply Chain

- Agility Logistics

- Aramex Logistics

- Bahri Logistics

- AlmajdouieLogistics

- Kuehne + Nagel

- DB Schenker

- DSV Logistics

- CEVA Logistics

- Gulf Warehousing Company

- NaqelExpress

- SAL Logistics Services

- Al Futtaim Logistics

- Hellmann Worldwide Logistics

- Wared Logistics

Key Target Audience

- Logistics and supply chain companies

- E commerce companies

- Retail distribution companies

- Manufacturing companies

- Food and beverage distributors

- Pharmaceutical companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying critical variables affecting the KSA warehousing market such as logistics infrastructure, warehouse capacity, supply chain demand, trade flows, and industrial development trends.

Step 2: Market Analysis and Construction

Researchers analyze available industry reports, logistics databases, trade statistics, and infrastructure development data to construct a structured market framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, logistics professionals, and supply chain specialists are consulted to validate assumptions and verify market insights.

Step 4: Research Synthesis and Final Output

All data and insights are consolidated into a comprehensive market report outlining current market conditions, industry dynamics, competitive landscape, and future outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E commerce Fulfillment Infrastructure in Saudi Arabia

Government Logistics Hub Development under Vision 2030

Growth of Retail and FMCG Distribution Networks - Market Challenges

High Capital Investment Required for Automated Warehousing Facilities

Land Availability Constraints in Urban Logistics Zones

Operational Cost Pressures from Energy and Labor Requirements - Market Opportunities

Development of Smart Warehousing with Automation and Robotics

Expansion of Cold Chain Warehousing for Food and Pharmaceutical Supply Chains

Growth of Regional Distribution Centers Serving GCC Trade - Trends

Integration of Warehouse Automation and Digital Inventory Systems

Expansion of Logistics Parks near Major Ports and Industrial Cities

Rising Adoption of Temperature Controlled Warehousing Facilities - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tie,r 2020-2025

- By System Type (In Value%)

General Storage Warehouses

Temperature Controlled Warehouses

Automated Storage and Retrieval Warehouses

Bonded Warehouses

Distribution and Fulfillment Warehouses - By Platform Type (In Value%)

Standalone Industrial Warehouses

Logistics Park Warehouses

Free Zone Warehouses

Port Based Warehouses

Airport Cargo Warehouses - By Fitment Type (In Value%)

Built to Suit Warehousing Facilities

Multi Client Shared Warehouses

Leased Standard Warehousing Units

Automated Smart Warehousing Facilities

Cold Storage Integrated Warehouses - By EndUser Segment (In Value%)

E commerce and Retail Companies

Manufacturing and Industrial Firms

Food and Beverage Distributors

- Market Share Analysis

- CrossComparison Parameters (Warehouse Capacity, Automation Level, Storage Technology, Geographic Coverage, Client Industry Focus)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Agility Logistics

Bahri Logistics

Almajdouie Logistics

Kuehne + Nagel

DHL Supply Chain

Aramex Logistics

Gulf Warehousing Company

Al Bayan Holding

Al Futtaim Logistics

DB Schenker

DSV Solutions

Ceva Logistics

Naqel Express

SAL Logistics Services

Wared Logistics

- Retail and E commerce Companies Expanding Fulfillment Networks

- Manufacturers Increasing Regional Distribution Warehousing

- Pharmaceutical Firms Requiring Temperature Controlled Storage Infrastructure

- Food Importers Utilizing Cold Chain Warehousing for Perishable Goods

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now