Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA wealth management market manages financial assets exceeding USD ~ billion in investable wealth, driven by rising high-net-worth populations, expanding capital markets participation, and diversification mandates under national economic transformation programs. Growth is supported by increasing domestic asset management firms, wider access to global investment vehicles through licensed intermediaries, and structural reforms enabling private capital deployment across equities, fixed income, real estate, and alternative investment products.

Within the Kingdom, Riyadh and Jeddah dominate wealth management activity due to concentration of financial institutions, sovereign entities, and affluent family conglomerates requiring structured advisory and portfolio services. Riyadh hosts regulatory authorities, capital market institutions, and investment headquarters, strengthening advisory ecosystems and product innovation. Jeddah remains a historic commercial hub with entrenched merchant wealth and family offices seeking succession planning and Sharia-compliant structuring, while Eastern Province wealth centers benefit from energy-linked corporate and executive wealth accumulation.

Market Segmentation

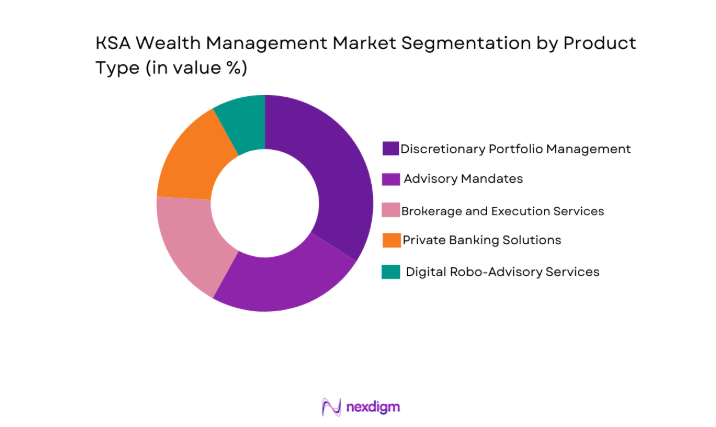

By Product Type

KSA Wealth Management market is segmented by product type into discretionary portfolio management, advisory mandates, brokerage and execution services, private banking solutions, and digital robo-advisory services. Recently, discretionary portfolio management has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

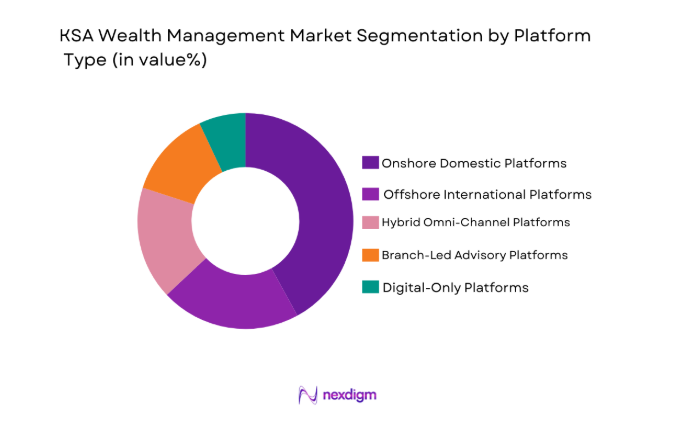

By Platform Type

KSA Wealth Management market is segmented by platform type into onshore domestic platforms, offshore international platforms, digital-only platforms, branch-led advisory platforms, and hybrid omni-channel platforms. Recently, onshore domestic platforms have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

Competitive Landscape

The KSA wealth management market shows moderate consolidation with domestic bank-owned asset managers controlling large client assets, while international private banks operate through joint ventures or licensed subsidiaries targeting ultra-high-net-worth clients. Leading firms differentiate through Sharia structuring, discretionary mandates, and access to global alternatives. Competitive intensity is increasing as digital investment platforms expand into affluent segments and domestic capital market reforms broaden investment product availability.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Client Segment Focus |

| SNB Capital | 2008 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Al Rajhi Capital | 2008 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Riyad Capital | 2008 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Jadwa Investment | 2006 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| HSBC Saudi Arabia | 2005 | Riyadh | ~ | ~ | ~ | ~ | ~ |

KSA wealth management Market Analysis

Growth Drivers

Rising High-Net-Worth and Ultra-High-Net-Worth Population Expansion

The sustained increase in affluent individuals within the Kingdom is fundamentally enlarging the addressable base for professional wealth management services and transforming the structure of financial intermediation. Wealth creation has accelerated through capital market participation, family-owned conglomerate expansion, privatization transactions, and entrepreneurial activity linked to economic diversification initiatives, resulting in substantial pools of investable financial assets requiring preservation and growth strategies. The concentration of private wealth in large family businesses and holding groups has intensified demand for institutionalized portfolio governance, asset allocation frameworks, and intergenerational transfer planning, encouraging migration from informal investment practices toward structured advisory mandates. Additionally, the emergence of first-generation millionaires from technology, healthcare, and services sectors has expanded the affluent segment beyond traditional merchant families, increasing the diversity of client needs and investment horizons. These clients increasingly seek global diversification across equities, fixed income, private markets, and real assets to mitigate domestic concentration risk, thereby raising reliance on licensed wealth managers with international access. Domestic capital market reforms, including broader listings and sukuk issuance, have also created more investable instruments, further attracting affluent investors into professionally managed portfolios. Wealth preservation considerations are intensifying as business cycles and oil-linked economic volatility highlight the importance of risk-adjusted asset allocation and liquidity planning, strengthening demand for discretionary management. The expansion of family office structures and succession planning requirements is reinforcing long-term advisory relationships and multi-asset portfolio oversight mandates. Moreover, increased financial literacy and exposure to global investment practices among Saudi investors are reducing barriers to outsourced portfolio management, accelerating industry penetration. Consequently, the structural growth of affluent populations is establishing a durable and expanding demand foundation for the Kingdom’s wealth management sector.

Capital Market Development and Financial Sector Diversification Programs

The ongoing transformation of the Kingdom’s financial ecosystem is significantly enhancing the scale and sophistication of wealth management activities by expanding investable opportunities and institutional infrastructure. Regulatory modernization and market liberalization have broadened the range of domestic securities, funds, and structured products available to investors, enabling more diversified and professionally managed portfolios. The growth of the national stock exchange, debt markets, and asset management industry has improved liquidity and price discovery, encouraging affluent individuals and institutions to allocate larger portions of wealth to financial assets rather than traditional holdings. Concurrently, financial sector development initiatives are attracting global asset managers and private banks to establish local operations, bringing advanced portfolio construction methodologies, risk analytics, and alternative investment access into the domestic market. Public investment programs and sovereign wealth participation in strategic sectors are catalyzing private investment ecosystems, generating new wealth pools and co-investment opportunities for private investors. The expansion of licensed intermediaries and digital brokerage platforms is also lowering entry barriers for affluent investors to participate in diversified portfolios, supporting migration toward managed investment solutions. Furthermore, regulatory encouragement of asset management localization is fostering domestic expertise, increasing competition, and improving service quality across advisory and discretionary offerings. As domestic financial markets deepen and integrate with global capital flows, the need for professional asset allocation, compliance oversight, and risk management capabilities intensifies, reinforcing the structural relevance of wealth managers. This systemic financial sector evolution is therefore a central driver of sustained growth in the Kingdom’s wealth management industry.

Market Challenges

Limited Local Advisory Talent and Portfolio Management Expertise

The wealth management industry within the Kingdom faces structural constraints due to the limited availability of experienced local advisors capable of delivering sophisticated portfolio construction, risk management, and multi-asset allocation services. Historically, investment management expertise has been concentrated within international financial centers, resulting in reliance on expatriate professionals or offshore advisory support for complex mandates. This dependency increases operational costs, restricts scalability, and creates continuity risks in client relationships, particularly in a market where trust and long-term engagement are central to wealth management success. Domestic education and professional training pipelines for wealth advisory, asset allocation, and private banking remain underdeveloped relative to the rapidly expanding affluent client base, producing a mismatch between demand for advanced advisory capabilities and available talent supply. Cultural preferences for relationship-driven banking and family-centric financial decision-making further require advisors with localized understanding of Sharia structuring, succession planning norms, and family governance practices, skills that are scarce among international professionals. Additionally, the growing complexity of investment products, including alternatives and structured instruments, demands specialized analytical competencies that remain limited in the domestic workforce. Firms therefore face challenges in building scalable advisory teams capable of serving mass affluent, high-net-worth, and ultra-high-net-worth segments simultaneously. Competition for experienced advisors among banks, asset managers, and family offices intensifies talent shortages and raises compensation costs, compressing profitability. Without sustained investment in local capability development and certification frameworks, advisory quality disparities may persist across the market. Consequently, talent constraints remain a fundamental barrier to industry expansion and service depth in the Kingdom’s wealth management sector.

Client Preference for Relationship-Led Banking over Discretionary Mandates

The evolution of wealth management adoption in the Kingdom is moderated by entrenched client behaviors that prioritize direct control over investment decisions and relationship-based banking interactions rather than delegated portfolio authority. Many affluent investors historically managed wealth through personal networks, family offices, or self-directed trading, resulting in limited familiarity with discretionary mandates and formal asset allocation frameworks. Trust dynamics in financial decision-making remain strongly linked to personal banker relationships, reducing willingness to transfer full portfolio management authority to institutional managers despite potential performance and diversification benefits. This behavioral pattern constrains the growth of fee-based discretionary services, which are typically more scalable and profitable for wealth managers compared to transaction-driven advisory models. Clients also often prefer concentrated holdings in familiar domestic assets or business sectors, limiting diversification opportunities and reducing demand for comprehensive portfolio management solutions. The perception of higher costs associated with professional wealth management services further discourages adoption among emerging affluent segments, particularly where historical investment returns were achieved through direct business ownership. Additionally, generational transitions within family wealth structures can create decision fragmentation, delaying migration toward institutionalized wealth management frameworks. Wealth managers must therefore invest heavily in education, trust-building, and customized engagement models to encourage discretionary adoption, increasing acquisition and servicing costs. These behavioral and cultural factors collectively slow the maturation of the Kingdom’s wealth management market toward globally prevalent advisory structures.

Opportunities

Expansion of Family Office Structuring and Intergenerational Wealth Transfer Advisory

The increasing scale and complexity of private wealth within the Kingdom is creating substantial demand for institutionalized family office structures and specialized advisory services addressing governance, succession, and long-term asset preservation. Large family-owned conglomerates and merchant groups are transitioning from founder-led control to multi-generational ownership models, necessitating formalized investment committees, asset allocation policies, and estate planning mechanisms. Wealth managers capable of delivering integrated family office solutions, including fiduciary oversight, consolidated reporting, and strategic asset allocation across global markets, can capture significant advisory mandates. The need to preserve capital across generations while balancing income requirements and risk tolerance is driving adoption of diversified multi-asset portfolios and alternative investments managed through professional advisors. Additionally, regulatory clarity around trusts, foundations, and family investment vehicles is enabling more sophisticated wealth structuring within the domestic jurisdiction, reducing reliance on offshore arrangements. Families are also increasingly seeking philanthropic advisory, governance frameworks, and education programs for next-generation members, expanding the scope of wealth management services beyond investment portfolios. Domestic financial institutions are positioned to develop dedicated family office divisions integrating tax structuring, Sharia compliance, and succession planning expertise. The scale of intergenerational wealth transfer anticipated within the Kingdom over coming decades further amplifies this opportunity. As family wealth institutionalization accelerates, comprehensive advisory platforms integrating governance, investment, and legacy planning will represent a major growth frontier in the Kingdom’s wealth management sector.

Digital Wealth Platforms Targeting Emerging Affluent Segments

Rapid digital adoption and expanding middle-to-affluent wealth brackets in the Kingdom are enabling scalable wealth management models delivered through technology-driven platforms. A growing cohort of professionals, entrepreneurs, and corporate executives is accumulating investable assets below traditional private banking thresholds yet demonstrating strong demand for diversified investment access and portfolio guidance. Digital wealth platforms integrating robo-advisory algorithms, model portfolios, and hybrid human advisory interfaces allow institutions to profitably serve this segment at scale while maintaining personalization and regulatory compliance. Mobile-first engagement models align with consumer preferences for accessible financial services and real-time portfolio monitoring, enhancing adoption among younger investors. The integration of Sharia-compliant portfolios, thematic investment strategies, and global exchange-traded products within digital interfaces broadens product accessibility beyond conventional banking channels. Additionally, digital onboarding and automated suitability assessment reduce acquisition costs and accelerate account activation compared to branch-centric advisory models. As domestic capital market participation expands, digital platforms provide an efficient distribution channel for funds, sukuk, and alternative investment vehicles to emerging affluent clients. The scalability of digital advisory also enables institutions to build long-term client relationships that may transition into high-net-worth segments over time. Consequently, technology-enabled wealth platforms represent a significant structural opportunity for expanding market penetration and revenue diversification in the Kingdom’s wealth management industry.

Future Outlook

The KSA wealth management market is expected to expand steadily as financial sector reforms, capital market depth, and private wealth accumulation continue to strengthen the domestic investment ecosystem. Increasing adoption of discretionary mandates, digital advisory platforms, and alternative investments will reshape service models and product structures. Regulatory support for asset management localization and fintech innovation will broaden access to diversified portfolios. Demand from family offices and emerging affluent segments will sustain long-term industry growth and competitive evolution.

Major Players

- SNB Capital

- Al Rajhi Capital

- Riyad Capital

- HSBC Saudi Arabia

- Saudi Fransi Capital

- Jadwa Investment

- Derayah Financial

- Alinma Investment

- Albilad Capital

- Morgan Stanley Saudi Arabia

- Goldman Sachs Saudi Arabia

- UBS Saudi Arabia

- Credit Suisse Saudi Arabia

- NCB Capital

- SABB Invest

Key Target Audience

- Private banks

- Asset management companies

- Family offices

- Investment and venture capitalist firms

- Sovereign wealth entities

- Pension and institutional funds

- Government and regulatory bodies

- High-net-worth investor groups

Research Methodology

Step 1: Identification of Key Variables

Market variables including investable wealth pools, client segments, product penetration, and advisory models were defined using regulatory disclosures and financial sector datasets. Structural drivers such as capital market depth, digital adoption, and wealth distribution were mapped to establish analytical scope.

Step 2: Market Analysis and Construction

Quantitative assessment integrated financial institution reports, asset management statistics, and wealth distribution studies to construct market sizing and segmentation. Platform, product, and client segment structures were modeled to reflect domestic advisory and investment patterns.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through expert consultations with wealth managers, private bankers, and financial analysts operating within the Kingdom’s investment ecosystem. Assumptions on client behavior, product adoption, and advisory structures were refined through practitioner insights.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into a structured market framework covering size, segmentation, competition, and outlook. Outputs were cross-checked for consistency with regulatory and institutional data to ensure analytical reliability.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising domestic millionaire and billionaire population expanding addressable wealth base

National transformation programs increasing private capital formation and investment activity

Growing investor appetite for diversified global and alternative assets

Digital banking adoption enabling scalable wealth advisory delivery models

Expansion of capital markets instruments and investment vehicles in the Kingdom - Market Challenges

Concentration of wealth within limited client segments constraining scale economics

Regulatory and compliance complexity for cross-border and offshore investments

Shortage of experienced local wealth advisors and portfolio specialists

Client preference for relationship-led banking over discretionary mandates

Market volatility influencing risk appetite and portfolio allocation stability - Market Opportunities

Expansion of family office advisory and succession planning services

Growth of Sharia-compliant alternative and private market investments

Digital wealth platforms targeting emerging affluent investors - Trends

Shift toward discretionary and model portfolio mandates

Integration of ESG and impact investing preferences in portfolios

Increasing allocation to private equity and venture capital funds

Adoption of hybrid human-digital advisory engagement models

Localization of global asset management partnerships - Government Regulations & Defense Policy

Strengthening of capital market regulations and investor protection frameworks

Policies encouraging domestic asset management industry development

Regulatory support for fintech and digital investment platforms - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory Mandates

Brokerage and Execution Services

Private Banking Solutions

Digital Robo-Advisory Services - By Platform Type (In Value%)

Onshore Domestic Platforms

Offshore International Platforms

Digital-Only Platforms

Branch-Led Advisory Platforms

Hybrid Omni-Channel Platforms - By Fitment Type (In Value%)

Mass Affluent Portfolios

High Net Worth Portfolios

Ultra High Net Worth Portfolios

Family Office Structures

Institutional Mandates - By EndUser Segment (In Value%)

Mass Affluent Individuals

High Net Worth Individuals

Ultra High Net Worth Individuals

Family Offices

Institutional Investors

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Client Segment Focus, Advisory Model, Product Breadth, Sharia Capability, Digital Platform Maturity, Global Access, Alternative Investment Capability, Relationship Coverage, Fee Structure)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

SNB Capital

Al Rajhi Capital

Riyad Capital

HSBC Saudi Arabia

Saudi Fransi Capital

Jadwa Investment

Derayah Financial

Alinma Investment

Albilad Capital

Morgan Stanley Saudi Arabia

Goldman Sachs Saudi Arabia

UBS Saudi Arabia

Credit Suisse Saudi Arabia

NCB Capital

SABB Invest

- High Net Worth and Ultra High Net Worth segments dominate assets under management concentration

- Family offices demand bespoke advisory, governance, and succession structuring services

- Mass affluent segment adoption rising through digital and bank-led platforms

- Institutional investors increasing allocation to domestic and regional assets

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now