Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia’s AI servers and GPU hardware market reached approximately USD ~ million based on a recent historical assessment, driven by hyperscale data center expansion, enterprise AI adoption, and cloud infrastructure investments across the country. Rapid deployment of accelerated computing clusters by telecom operators, cloud providers, and colocation facilities supports AI training and inference workloads in financial services, manufacturing analytics, and digital platforms, while government digital economy programs and semiconductor ecosystem growth reinforce demand for high-performance compute infrastructure nationwide.

Johor and Kuala Lumpur dominate Malaysia’s AI servers and GPU hardware landscape due to concentration of hyperscale and colocation data centers supporting regional cloud and AI workloads. Johor’s proximity to Singapore’s constrained data center market attracts large-scale AI infrastructure deployment, while Kuala Lumpur hosts enterprise, telecom, and financial sector compute clusters. Penang’s semiconductor manufacturing ecosystem and electronics design capabilities further drive localized AI hardware integration and testing activity, reinforcing these regions as Malaysia’s primary AI compute infrastructure hubs.

Market Segmentation

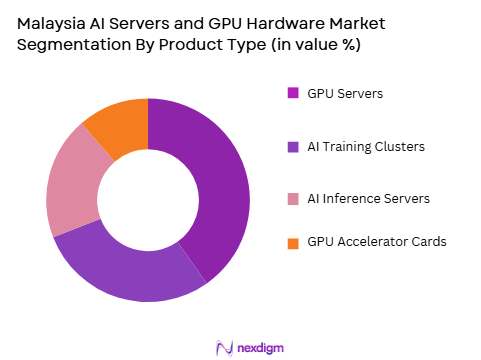

By Product Type

Malaysia AI Servers and GPU Hardware market is segmented by product type into GPU servers, AI training clusters, AI inference servers, and GPU accelerator cards. Recently, GPU servers have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Hyperscale cloud providers and enterprise data centers in Malaysia deploy integrated GPU server platforms as foundational AI infrastructure because they offer scalable, rack-level acceleration suitable for both training and inference workloads, simplifying procurement and deployment compared with discrete accelerator integration across distributed facilities.

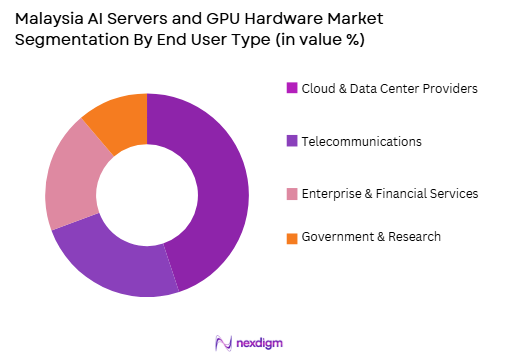

By End User

Malaysia AI Servers and GPU Hardware market is segmented by end user into cloud & data center providers, telecommunications, enterprise & financial services, and government & research. Recently, cloud & data center providers have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Hyperscale and colocation operators in Malaysia invest heavily in GPU-accelerated infrastructure to serve regional AI workloads and sovereign cloud requirements, positioning them as primary purchasers of AI servers and GPU hardware across national and cross-border digital service ecosystems.

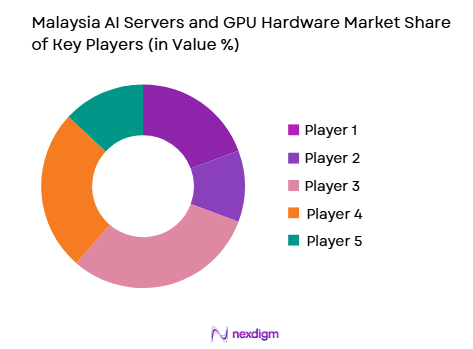

Competitive Landscape

Malaysia’s AI servers and GPU hardware market is dominated by global accelerated computing vendors and cloud infrastructure providers, with strong consolidation around GPU architecture leaders and server OEM ecosystems. Partnerships between hyperscale cloud operators, telecom carriers, and hardware manufacturers define procurement and deployment patterns, while regional data center expansion reinforces demand concentration among a limited group of multinational technology firms.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI GPU Architecture |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| AMD | 1969 | USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | USA | ~ | ~ | ~ | ~ | ~ |

Malaysia AI Servers and GPU Hardware Market Analysis

Growth Drivers

Hyperscale and Colocation Data Center Expansion for AI Workloads

Malaysia’s rapid emergence as a regional data center hub is significantly accelerating demand for AI servers and GPU hardware because hyperscale cloud providers and colocation operators are deploying accelerated compute clusters to support artificial intelligence training and inference workloads across Southeast Asia. Johor’s large-scale data center campuses and Kuala Lumpur’s enterprise colocation facilities host GPU-dense server racks designed for cloud AI services, generative AI platforms, and analytics workloads. Regional demand for sovereign cloud and localized AI processing encourages multinational cloud providers to establish compute availability zones within Malaysia. AI model training requires high-performance GPU clusters with advanced interconnects and cooling systems, driving procurement of specialized AI servers at scale. Data center operators increasingly market GPU-as-a-service offerings, creating recurring demand for accelerator hardware refresh cycles. Government support for digital infrastructure investment and cross-border connectivity strengthens Malaysia’s attractiveness for AI compute deployment. Power and land availability advantages compared with neighboring markets further encourage hyperscale GPU cluster construction. As enterprises shift AI workloads from centralized global regions to regional nodes, Malaysia’s data center expansion directly translates into sustained growth in national AI server and GPU hardware demand.

Enterprise Artificial Intelligence Adoption Across Finance, Manufacturing, and Digital Platforms

Malaysian enterprises across financial services, manufacturing, healthcare, and digital commerce sectors are adopting artificial intelligence for analytics, automation, and decision intelligence, driving procurement of on-premise and private-cloud GPU-accelerated infrastructure. Banks deploy AI servers for fraud detection, risk modeling, and customer analytics requiring localized high-performance computing. Manufacturing firms use GPU systems for machine vision, predictive maintenance, and process optimization within smart factory environments. E-commerce and digital platforms require GPU inference servers to support recommendation engines, search optimization, and real-time personalization workloads. National AI and digital economy strategies encourage enterprises to invest in domestic compute capacity rather than relying exclusively on overseas cloud regions. Data governance and latency considerations further promote local AI hardware deployment. System integrators and enterprise IT vendors in Malaysia are expanding AI infrastructure solution offerings incorporating GPU servers and accelerators. Growing availability of AI software frameworks compatible with GPU architectures lowers adoption barriers for enterprises. As AI becomes embedded across Malaysian industries, enterprise compute modernization becomes a structural growth driver for the national AI servers and GPU hardware market.

Market Challenges

High Cost and Power Density Constraints of GPU-Accelerated Infrastructure

AI servers and GPU hardware deployments in Malaysia face substantial financial and operational challenges due to the extremely high capital cost and power density requirements of modern GPU-accelerated systems used for AI training and inference. Advanced GPUs and AI servers require significant upfront investment, limiting adoption primarily to hyperscale cloud providers and large enterprises. GPU clusters generate high heat loads, necessitating advanced cooling technologies such as liquid cooling that increase infrastructure complexity and cost. Data centers in Malaysia must secure sufficient power capacity and grid stability to support dense AI compute racks, which can strain local energy infrastructure. Power efficiency and sustainability requirements further complicate deployment planning. Hardware supply constraints and long procurement lead times for advanced GPUs can delay infrastructure projects. Skilled engineers capable of deploying and maintaining high-performance AI clusters remain scarce locally. These cost, energy, and expertise barriers restrict broader market participation and slow diffusion of AI hardware across smaller Malaysian enterprises and institutions.

Dependence on Imported GPU Supply Chains and Limited Domestic Semiconductor Capability

Malaysia’s AI servers and GPU hardware market relies heavily on imported accelerator chips and server systems from global vendors because domestic semiconductor manufacturing focuses primarily on assembly, testing, and packaging rather than advanced GPU fabrication. This structural dependence exposes the market to global supply disruptions, export controls, and pricing volatility affecting availability of cutting-edge AI hardware. Geopolitical technology restrictions and allocation policies by GPU manufacturers can influence hardware access for regional markets. Local value creation in AI hardware remains limited to integration and deployment rather than core chip design or fabrication. Enterprises and data center operators must align procurement with international vendor ecosystems, reducing domestic technological autonomy. Although Malaysia has a strong electronics manufacturing base, it lacks indigenous GPU architecture development capability. This reliance on external supply chains constrains national competitiveness in AI compute infrastructure. The absence of local high-performance chip manufacturing presents a long-term structural challenge for Malaysia’s AI hardware ecosystem.

Opportunities

Regional AI Compute Hub Positioning Leveraging Johor–Singapore Digital Corridor

Malaysia has a strategic opportunity to position itself as Southeast Asia’s primary regional AI compute hub by leveraging Johor’s proximity to Singapore’s constrained data center and AI infrastructure market. Singapore’s power and land limitations are pushing hyperscale AI deployments into nearby Malaysian territories where capacity expansion is feasible. Johor’s large data center developments can host GPU-dense clusters serving regional cloud and enterprise AI workloads while maintaining low latency connectivity to Singapore and ASEAN markets. Cross-border digital infrastructure integration allows Malaysia to capture AI hardware investment and GPU cluster deployment driven by regional demand. Cloud providers seeking cost-efficient AI compute capacity increasingly view Malaysia as a complementary extension of Singapore’s digital ecosystem. Government incentives for digital infrastructure and technology investment can further attract AI hardware deployment. As Southeast Asian AI adoption accelerates, Malaysia’s geographic and infrastructure advantages enable it to become a central node for regional accelerated computing infrastructure, creating significant growth potential for the national AI servers and GPU hardware market.

National AI Strategy and Public-Sector Compute Infrastructure Development

Malaysia’s national artificial intelligence and digital economy policies create opportunities for large-scale public-sector investment in domestic AI compute infrastructure, including GPU clusters for research, government analytics, and sovereign cloud platforms. Government agencies and research institutions require high-performance AI servers to support national data analytics, healthcare AI, climate modeling, and smart city applications. Public cloud and sovereign data initiatives encourage domestic hosting of sensitive AI workloads, stimulating procurement of GPU hardware within national borders. Collaboration between government, academia, and industry can establish national AI compute centers and shared infrastructure platforms. Public-sector funding can catalyze local ecosystem development in AI software, integration, and services around GPU infrastructure. Expansion of digital public services and AI-enabled governance systems will require scalable compute capacity. By investing in national AI infrastructure programs, Malaysia can accelerate domestic adoption and reduce dependence on foreign cloud regions. This policy-driven infrastructure development represents a major opportunity for sustained expansion of Malaysia’s AI servers and GPU hardware market.

Future Outlook

Malaysia’s AI servers and GPU hardware market is expected to grow strongly over the next five years as hyperscale data center expansion, enterprise AI adoption, and regional cloud demand accelerate deployment of accelerated compute clusters. National AI and digital economy initiatives will stimulate domestic infrastructure investment, while Johor’s emergence as a regional AI compute corridor linked to Singapore will attract multinational GPU deployments. Continued semiconductor ecosystem growth and enterprise digitalization will further reinforce demand for high-performance AI hardware across Malaysia.

Major Players

- NVIDIA

- AMD

- Intel

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Supermicro

- Inspur

- Cisco Systems

- IBM

- Huawei

- Google Cloud

- Microsoft

- Amazon Web Services

- SkyeChip

Key Target Audience

- Hyperscale cloud providers

- Colocation data center operators

- Telecommunications companies

- Financial institutions

- Manufacturing conglomerates

- Investments and venture capitalist firms

- Government and regulatory bodies

- AI platform developers

Research Methodology

Step 1: Identification of Key Variables

AI infrastructure deployments, GPU procurement volumes, data center expansion, and enterprise AI adoption indicators were identified through secondary research and industry analysis. Supply-side variables such as vendor shipments and server configurations were mapped alongside demand-side indicators across cloud, telecom, enterprise, and government sectors to define market scope.

Step 2: Market Analysis and Construction

Market size was constructed by triangulating AI server shipments, GPU accelerator deployments, and Malaysia-specific infrastructure investment data attributed to hyperscale, telecom, and enterprise buyers. Segmentation shares were derived from deployment patterns across product architectures and end-user verticals to ensure internal consistency.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary estimates and structural assumptions were validated through consultations with data center architects, AI infrastructure specialists, and regional cloud ecosystem experts. Feedback on deployment scale, procurement trends, and technology adoption refined segmentation distribution and competitive positioning analysis.

Step 4: Research Synthesis and Final Output

Validated quantitative datasets and qualitative insights were synthesized into a structured market model linking infrastructure deployment, industry demand, and policy drivers. Results were integrated into standardized report sections covering sizing, segmentation, competitive landscape, and outlook for Malaysia’s AI servers and GPU hardware ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of hyperscale and regional cloud data centers in Malaysia

Government led AI and digital economy infrastructure investments

Rising enterprise adoption of AI workloads across industries - Market Challenges

High capital intensity and energy requirements of GPU infrastructure

Dependence on imported advanced semiconductor hardware

Limited domestic expertise in AI infrastructure deployment and integration - Market Opportunities

Development of sovereign AI cloud and national compute initiatives

Localization of AI data center infrastructure supply chains

Growth of AI adoption across manufacturing and smart city programs - Trends

Shift toward liquid cooled and energy efficient GPU servers

Deployment of edge AI compute across telecom networks

Integration of AI accelerators with high speed networking fabrics - Government regulations

Malaysia National AI Roadmap and digital infrastructure policies

Data sovereignty and cross border data governance frameworks

Energy efficiency and green data center standards - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Training GPU Servers

AI Inference GPU Servers

High Performance Computing GPU Clusters

Edge AI GPU Servers

AI Optimized Storage and Accelerated Servers - By Platform Type (In Value%)

Cloud Data Center Platforms

Enterprise On Premise Data Centers

Telecom Edge Infrastructure

Government and Sovereign AI Infrastructure

Research and Academic Supercomputing Platforms - By Fitment Type (In Value%)

Rack Scale Integrated Systems

Blade GPU Server Systems

Modular GPU Expansion Systems

Preconfigured AI Appliance Systems

Hyperconverged GPU Infrastructure - By End User Segment (In Value%)

Cloud Service Providers

Telecommunications Operators

Government and Public Sector Agencies

Financial Services and Enterprises

Universities and Research Institutions - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrator and VAR Procurement

Government Tender Procurement

Cloud Marketplace Procurement

Distributor and Channel Partner Procurement

- Market Share Analysis

- Cross Comparison Parameters (System Performance, Energy Efficiency, Cooling Technology, Scalability, Deployment Model, GPU Architecture Support, Networking Bandwidth, Storage Throughput, Management Software Stack, AI Framework Compatibility, Service and Support Capability, Total Cost of Ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Dell Technologies

Hewlett Packard Enterprise

Lenovo Group

Supermicro

Fujitsu

Inspur Information

Cisco Systems

Quanta Computer

Foxconn Industrial Internet

Wiwynn

Advantech

GIGABYTE Technology

ASUS

NEC Corporation

Hitachi

- Cloud providers scaling GPU clusters to serve regional AI workloads

- Telecom operators deploying edge AI compute for 5G services

- Government agencies building sovereign AI infrastructure

- Enterprises adopting AI servers for analytics and automation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now