Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Malaysia car finance market is driven by increasing consumer demand for personal vehicles, with an estimated market size of USD ~ billion based on a recent historical assessment. The growth is primarily fueled by factors such as rising disposable incomes, evolving financing options, and the introduction of innovative lending platforms. Additionally, favorable government policies, coupled with expanding financial institutions, have contributed to a favorable environment for car financing in the region.

The dominant regions contributing to the growth of this market are Kuala Lumpur, Penang, and Johor, where higher income levels, improved infrastructure, and urbanization have led to an increased demand for vehicle ownership. These areas benefit from a robust financial ecosystem, with numerous banks and financial institutions offering tailored financing products to meet consumer needs. The presence of major automotive manufacturers also contributes to the strong demand for car financing in these regions.

Market Segmentation

By Product Type

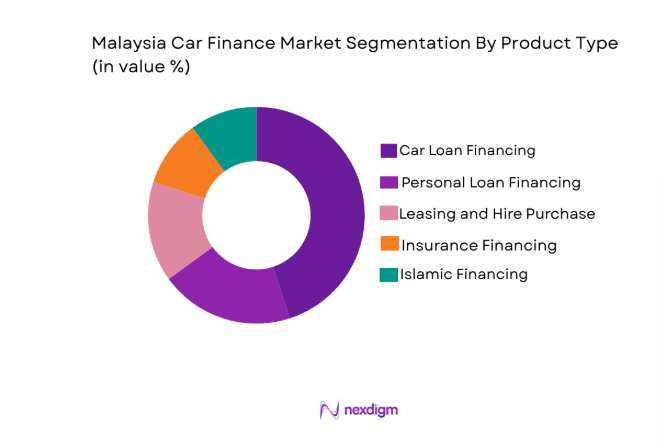

The Malaysia car finance market is segmented by product type into car loan financing, personal loan financing, leasing and hire purchase, insurance financing, and Islamic financing. Recently, car loan financing has a dominant market share due to consumer preference for flexible and affordable options. Car loan financing offers low-interest rates and long-tenure options, which align with the increasing trend of affordable monthly payments and vehicle ownership among consumers. The simplicity of traditional car loan products and the ease of access to financing from various institutions have cemented its position as the most popular form of vehicle financing in Malaysia.

By Platform Type

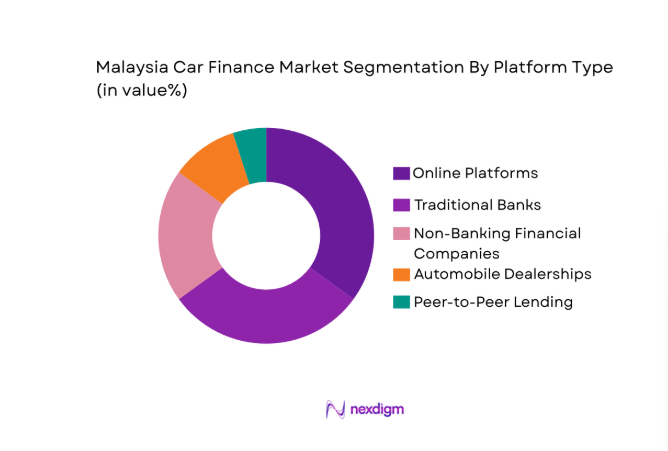

The market is segmented by platform type into online platforms, traditional banks, non-banking financial companies (NBFCs), automobile dealerships, and peer-to-peer lending. Online platforms have recently captured a dominant market share due to the growing adoption of digital financial services. These platforms provide customers with easy access to various financing options, allowing them to compare interest rates, loan terms, and fees from multiple lenders. This has made the process of securing car financing more convenient and accessible to a wider demographic, contributing to the rise of online platforms as the preferred choice for consumers seeking car loans in Malaysia.

Competitive Landscape

The competitive landscape of the Malaysia car finance market is characterized by significant consolidation, with key players including both traditional financial institutions and emerging fintech platforms. The increasing influence of online platforms has created a shift in how car loans are offered, allowing customers to access financing more quickly and with greater ease. Major players continue to focus on improving their digital infrastructure and expanding product offerings to capture a larger share of the market.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Maybank | 1960 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| CIMB Bank | 1956 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Public Bank | 1966 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| RHB Bank | 1997 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| OCBC Bank | 1932 | Singapore | ~ | ~ | ~ | ~ | ~ |

Malaysia Car Finance Market Analysis

Growth Drivers

Increasing Consumer Demand for Vehicles

The increasing consumer demand for vehicles is a major driver in the Malaysia car finance market. As the country’s economic conditions improve, rising disposable incomes have enabled more individuals to purchase personal vehicles. Furthermore, Malaysia’s strategic location and the expanding automotive industry have made cars a symbol of status and convenience for the growing middle class. The growth of car financing options has further accelerated this trend, as consumers are now able to afford monthly installment plans for vehicles that were once out of reach. The availability of various financing options such as car loans, personal loans, and hire purchase plans has played a crucial role in catering to the demand. Additionally, government incentives and tax breaks offered to vehicle buyers have made financing more affordable. This combination of factors has led to increased market demand, and the market is expected to continue growing as more consumers opt for financing options that provide flexibility and affordability in their car purchases.

Evolving Financing Solutions and Digitalization

Another key growth driver is the increasing digitalization of financing solutions in Malaysia. Traditional banking systems are undergoing a significant transformation, with financial institutions investing in innovative digital platforms to streamline the car loan process. Online lending platforms have surged in popularity due to their convenience, allowing consumers to apply for car financing from the comfort of their homes. The development of advanced technologies such as artificial intelligence (AI) has also enabled financial institutions to improve their credit scoring systems and risk management, ensuring better loan terms and lower interest rates. As these digital platforms expand their reach, they provide more options to customers, which further drives demand for car loans. The ease of application, quicker approval processes, and enhanced customer experience have contributed to the rapid growth of digital platforms in the market. Additionally, the widespread use of smartphones and mobile banking applications has made car financing more accessible, thus propelling the growth of the market.

Market Challenges

Rising Interest Rates and Financial Risks

One of the major challenges in the Malaysia car finance market is the rising interest rates, which have made car loans more expensive for consumers. As interest rates increase, monthly payments on loans also rise, placing additional financial pressure on individuals. Consumers may struggle to afford higher installment amounts, especially if their incomes are not increasing at the same pace as their loan obligations. This can lead to a rise in defaults and increase the risk for financial institutions. Additionally, higher interest rates can make it difficult for lenders to offer competitive loan products, reducing their ability to attract new customers. The financial risks associated with lending become higher as a result, which can dampen the growth of the car finance market. For financial institutions, managing these risks requires a careful balance of loan offerings, interest rates, and customer creditworthiness. In some cases, stricter lending policies may be enforced, which could limit the number of individuals eligible for financing, further challenging market expansion.

Consumer Credit Risk and Defaults

Another significant challenge faced by the Malaysia car finance market is the increasing rate of consumer credit defaults. While financial institutions offer attractive financing options, the risk of non-payment due to poor credit management remains a concern. The availability of unsecured personal loans and other credit facilities has led to higher levels of consumer debt, and many individuals struggle to meet their repayment obligations. Defaults on car loans can lead to significant losses for lenders, especially when vehicles are repossessed but do not recover the full value of the loan. In some cases, borrowers may face financial difficulties, making it harder for them to repay their loans, particularly in uncertain economic conditions. For financial institutions, managing this challenge requires sophisticated credit risk assessment tools, as well as strategies to mitigate the impact of defaults. Tightening of credit requirements and offering more personalized loan products may help reduce the risk of defaults but may also limit market reach. Therefore, managing consumer credit risk is critical to maintaining stability and sustainable growth in the market.

Opportunities

Growth of Electric Vehicle Financing

With the increasing global focus on sustainability and environmental responsibility, the demand for electric vehicles (EVs) in Malaysia is expected to rise. This trend presents a significant opportunity for car finance providers to expand their product offerings to include financing solutions for EVs. As more consumers shift towards electric vehicles, financial institutions can offer specialized financing products that cater to the unique requirements of EV ownership, such as longer loan tenures or subsidized interest rates for environmentally-friendly vehicles. Government incentives, tax rebates, and subsidies further support the growth of the electric vehicle market, encouraging consumers to make the switch to greener transportation options. Financial institutions can also capitalize on this trend by partnering with automotive manufacturers and electric vehicle dealers to offer competitive financing options for EV buyers. By tapping into the growing demand for electric vehicles, car finance providers can not only contribute to a sustainable future but also tap into a new market segment with potential for significant growth.

Expansion of Digital Car Financing Platforms

The rapid growth of digital platforms presents a significant opportunity for car finance providers to expand their customer base and streamline their offerings. Consumers are increasingly turning to digital channels for their financing needs due to the convenience, accessibility, and ease of use they offer. Online platforms that provide quick loan approvals, competitive interest rates, and flexible repayment terms have become highly popular, especially among younger, tech-savvy consumers. As more financial institutions invest in digital technologies and mobile applications, the opportunities for expanding market reach and improving customer satisfaction grow. By enhancing the user experience through seamless digital interfaces, providing personalized loan options, and leveraging data analytics for better decision-making, car finance providers can position themselves as leaders in the digital space. This digital transformation is set to reshape the car finance market in Malaysia, offering new avenues for growth and consumer engagement.

Future Outlook

The future outlook for the Malaysia car finance market is positive, with expected growth driven by technological advancements, changing consumer preferences, and regulatory support. Digital platforms are expected to play an increasingly important role, providing consumers with more convenient and tailored financing solutions. The continued push towards electric vehicle adoption, supported by government incentives, will further boost demand for specialized car financing products. As the market evolves, increased competition will drive innovation, and financial institutions will focus on providing flexible, customer-centric financing options to meet the growing demands of the modern consumer.

Major Players

- Maybank

- CIMB Bank

- Public Bank

- Hong Leong Bank

- RHB Bank

- OCBC Bank

- UOB

- Standard Chartered

- Alliance Bank

- Bank Rakyat

- Affin Bank

- Bank Muamalat

- EON Bank

- Bumi Armada

- AmBank

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Banks and financial institutions

- Automotive manufacturers

- Car dealerships

- Leasing companies

- Insurance companies

- Peer-to-peer lending platforms

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the key variables that affect the market dynamics, such as consumer behavior, financing options, economic factors, and technological trends.

Step 2: Market Analysis and Construction

In this phase, the market is analyzed to understand the different segments, competitive landscape, and growth drivers using both qualitative and quantitative research methods.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations and industry validation are conducted to test the initial hypotheses regarding market trends, growth factors, and consumer preferences, ensuring the accuracy of the analysis.

Step 4: Research Synthesis and Final Output

The findings from various research methods are synthesized to produce a comprehensive market report, providing actionable insights for decision-makers and stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Demand for Personal Vehicles

Expansion of Fintech Platforms

Government Subsidies and Tax Breaks

Growth in Middle-Class Population

Rising Vehicle Affordability - Market Challenges

Rising Interest Rates

Regulatory Compliance and Barriers

Credit Risk Management Issues

Low Financial Literacy in Rural Areas

High Default Rates on Loans - Market Opportunities

Growth of Online Car Financing Platforms

Adoption of Islamic Financing Products

Increased Demand for Electric Vehicle Financing - Trends

Shift Towards Digital and Online Financing

Rise of Subscription-based Vehicle Financing

Growth in Shared Mobility and Car Rentals

Integration of AI in Risk Assessment

Adoption of Eco-friendly Vehicle Financing Models - Government Regulations & Defense Policy

Government Incentives for Green Vehicles

Regulations on Auto Loan Transparency

Consumer Protection Laws in Auto Financing - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Car Loan Financing

Personal Loan Financing

Leasing and Hire Purchase

Insurance Financing

Islamic Financing - By Platform Type (In Value%)

Online Platforms

Traditional Banks

Non-Banking Financial Companies (NBFCs)

Automobile Dealerships

Peer-to-Peer Lending - By Fitment Type (In Value%)

New Car Financing

Used Car Financing

Refinancing Solutions

Lease Buyouts

Fleet Financing - By End User Segment (In Value%)

Individual Consumers

Corporate Fleet Managers

Automobile Dealerships

Leasing Companies

Banks & Financial Institutions

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (System Type, Platform Type, End User Segment, Procurement Channel, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Maybank

CIMB Bank

Public Bank

Hong Leong Bank

RHB Bank

Ambank

OCBC Bank

Affin Bank

Bank Muamalat

UOB

Standard Chartered Bank

Alliance Bank

Bank Rakyat

Bumi Armada

EON Bank

- High Demand from Urban Consumers

- Corporate Financing for Fleet Expansion

- Increasing Preference for Flexible Financing Options

- Adoption of Green and Sustainable Financing by Consumers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now