Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia cloud infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by sustained hyperscale data center investments, enterprise cloud migration, and expansion of digital services platforms. Demand growth is reinforced by government cloud-first procurement policies, rising AI and analytics workloads, and increasing colocation and managed cloud adoption by enterprises. Major telecom operators and global hyperscalers continue to deploy large-scale compute and storage capacity, supporting domestic and regional digital economy expansion.

Kuala Lumpur and Johor dominate Malaysia cloud infrastructure market due to concentration of hyperscale data center campuses, international submarine cable landings, and proximity to Singapore’s digital hub. Johor benefits from cross-border cloud and colocation spillover driven by land and power availability, while Kuala Lumpur leads in enterprise demand, financial services infrastructure, and government cloud deployments. Malaysia also serves regional ASEAN workloads due to strategic connectivity and stable regulatory frameworks enabling multinational cloud operations.

Market Segmentation

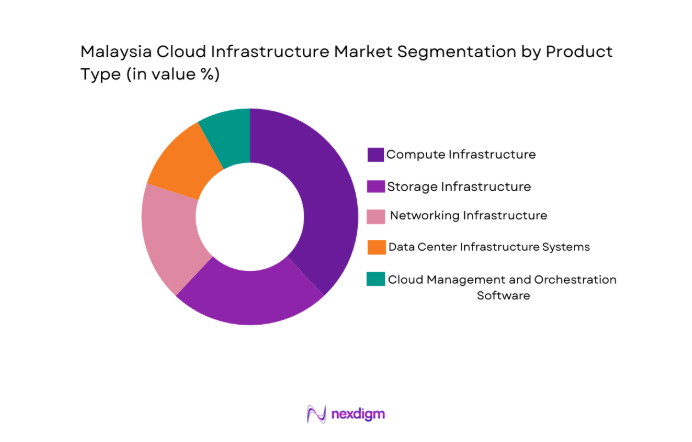

By Product Type

Malaysia cloud infrastructure market is segmented by product type into compute infrastructure, storage infrastructure, networking infrastructure, data center infrastructure systems, and cloud management and orchestration software. Recently, compute infrastructure has a dominant market share due to factors such as hyperscale server deployments, AI and analytics workloads, and enterprise migration of applications to virtualized environments. Expansion of cloud regions and high-performance computing clusters further increases demand for scalable processing capacity across Malaysia’s digital economy ecosystem.

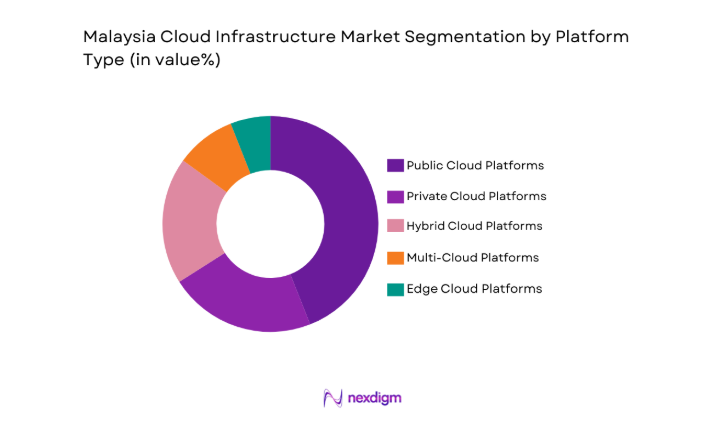

By Platform Type

Malaysia cloud infrastructure market is segmented by platform type into public cloud platforms, private cloud platforms, hybrid cloud platforms, multi-cloud platforms, and edge cloud platforms. Recently, public cloud platforms has a dominant market share due to factors such as strong hyperscaler presence, consumption-based pricing models, and broad service availability for enterprises and digital platforms. Rapid adoption by SMEs and large enterprises migrating from on-premise IT environments reinforces public cloud platform leadership in Malaysia.

Competitive Landscape

Malaysia cloud infrastructure market shows moderate consolidation, with global hyperscalers and domestic telecom-led cloud providers controlling core infrastructure capacity while colocation operators and managed service firms compete in enterprise and hybrid deployments. Strategic alliances between telecom operators and hyperscalers strengthen distribution reach and regulatory compliance positioning. Continuous data center expansion and sovereign cloud initiatives reinforce competitive intensity among leading providers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Data Center Footprint Malaysia |

| Telekom Malaysia | 1984 | Kuala Lumpur, Malaysia | ~ | ~ | ~ | ~ | ~ |

| Maxis Berhad | 1995 | Kuala Lumpur, Malaysia | ~ | ||||

| Amazon Web Services | 2006 | Seattle, USA | |||||

| Microsoft Azure | 2010 | Redmond, USA | |||||

| Google Cloud | 2008 | Mountain View, USA |

Malaysia Cloud Infrastructure Market Analysis

Growth Drivers

Hyperscale Data Center and Cloud Region Expansion in Malaysia

Malaysia’s emergence as a regional hyperscale data center destination is driving substantial growth in cloud infrastructure capacity, as global cloud providers and colocation firms invest heavily in new campuses, power infrastructure, and fiber connectivity across Kuala Lumpur and Johor corridors. These investments increase available compute, storage, and networking capacity while improving service latency for domestic and ASEAN workloads, enabling enterprises to migrate critical applications from on-premise IT environments to scalable cloud platforms. Hyperscale expansion also stimulates supporting ecosystems including renewable power procurement, submarine cable landings, and carrier-neutral interconnection hubs, strengthening Malaysia’s attractiveness as a regional digital infrastructure node. Government incentives for data center development and foreign direct investment policies further accelerate hyperscaler entry and expansion decisions. The clustering of cloud regions, availability zones, and interconnection facilities enhances reliability and redundancy capabilities required by financial services, digital platforms, and government agencies. As capacity expands, cloud providers introduce advanced services including AI accelerators, high-performance computing, and managed analytics platforms, encouraging higher-value cloud adoption by enterprises. Hyperscale presence also drives price competition and service innovation among providers, improving affordability and functionality of cloud infrastructure. Enterprises respond by accelerating digital transformation programs and migrating mission-critical workloads, which increases overall infrastructure utilization. These structural dynamics collectively position Malaysia as a key regional cloud infrastructure hub, reinforcing sustained market growth momentum.

Enterprise Digital Transformation and Cloud Migration Across Malaysian Industries

Accelerating enterprise digital transformation across banking, telecommunications, manufacturing, and government sectors is generating sustained demand for scalable cloud infrastructure platforms capable of supporting data-intensive applications, digital customer channels, and automation initiatives. Malaysian enterprises increasingly adopt cloud-native architectures to modernize legacy systems, improve operational agility, and enable advanced analytics and artificial intelligence deployment across core business processes. Financial institutions migrate transaction processing and digital banking platforms to secure hybrid cloud environments to enhance resilience and regulatory compliance. Telecommunications operators virtualize network functions and deploy 5G core systems on cloud platforms, driving large-scale compute and storage consumption. Manufacturing firms implement industrial IoT and smart factory systems requiring edge-to-cloud integration, further expanding infrastructure demand. Government agencies transition public services to cloud-based platforms to improve citizen service delivery and data integration across departments. Cloud adoption also supports rapid scaling of ecommerce and digital platforms responding to evolving consumer behavior in Malaysia’s digital economy. Enterprises prioritize consumption-based infrastructure models to optimize IT costs and reduce capital expenditure requirements. The shift toward multi-cloud strategies increases total infrastructure utilization across providers. These widespread digital transformation initiatives across sectors constitute a structural demand driver sustaining long-term growth of Malaysia cloud infrastructure market.

Market Challenges

High Energy Demand and Sustainability Constraints in Malaysian Data Center Expansion

Rapid expansion of hyperscale and colocation data centers in Malaysia significantly increases electricity consumption, placing pressure on national power infrastructure and sustainability commitments while raising operational costs for cloud providers. Data centers require continuous high-density power supply and advanced cooling systems, creating large energy loads concentrated in specific regions such as Johor and Kuala Lumpur technology corridors. Utilities must expand grid capacity and transmission infrastructure to support these developments, which involves regulatory approvals, long investment cycles, and environmental considerations. Rising electricity tariffs and carbon emission targets affect the long-term economics of cloud infrastructure deployment and pricing competitiveness. Cloud operators face increasing requirements to procure renewable energy or implement energy-efficient technologies to meet sustainability expectations from enterprises and regulators. Land availability and environmental approvals for large-scale campuses also constrain expansion speed in high-demand zones. Water consumption for cooling systems introduces additional environmental management challenges in certain locations. Energy reliability and redundancy requirements necessitate backup generation systems, further increasing infrastructure costs. These combined sustainability and energy constraints complicate long-term scaling of Malaysia cloud infrastructure capacity and may influence investment allocation decisions by hyperscalers and colocation providers.

Regulatory Complexity and Data Sovereignty Requirements Affecting Cloud Adoption

Malaysia cloud infrastructure market faces regulatory challenges related to data sovereignty, cybersecurity compliance, and sector-specific regulations that influence enterprise cloud deployment decisions and provider operations. Financial services, government, and telecommunications sectors require strict data residency and security controls, often mandating local hosting and certified infrastructure environments. Compliance with personal data protection regulations and cross-border data transfer restrictions introduces operational complexity for multinational cloud providers. Certification requirements and regulatory audits increase deployment timelines and operational costs for cloud infrastructure facilities. Enterprises in regulated industries must implement hybrid or sovereign cloud architectures to satisfy legal requirements, limiting full public cloud migration potential. Government procurement frameworks and localization policies also shape provider market access and partnership models. Rapid evolution of cybersecurity standards and data protection frameworks requires continuous infrastructure upgrades and compliance monitoring. Uncertainty in future regulatory interpretations can delay enterprise cloud migration projects and investment commitments. Providers must invest heavily in compliance capabilities and localized operations to maintain market presence. These regulatory and sovereignty constraints create structural barriers affecting adoption pace and infrastructure utilization across Malaysia cloud infrastructure market.

Opportunities

Malaysia as ASEAN Regional Cloud and Data Center Hub Serving Cross-Border Digital Demand

Malaysia possesses geographic, economic, and infrastructure advantages enabling it to evolve into a major regional cloud infrastructure hub serving ASEAN digital markets, particularly as Singapore faces land and power constraints limiting further hyperscale expansion. Availability of industrial land, comparatively lower energy costs, and strong connectivity via submarine cable systems position Malaysia as an attractive alternative location for large-scale cloud regions and colocation campuses. Cross-border digital traffic and cloud spillover demand from Singapore and neighboring economies drive investment in Johor and southern Malaysia corridors. Regional enterprises and global digital platforms increasingly deploy workloads in Malaysia to achieve latency optimization and cost efficiency across Southeast Asia. Government promotion of digital economy zones and data center investment incentives further strengthens regional positioning. Hyperscale clusters attract ecosystem investments including fiber networks, interconnection exchanges, and cloud service integrators. Regional cloud deployment demand encourages advanced infrastructure offerings such as AI compute clusters and high-performance data platforms. Malaysia’s political stability and regulatory clarity support long-term infrastructure investment decisions by global providers. As regional digitalization accelerates, Malaysia can capture growing share of ASEAN cloud infrastructure capacity, creating substantial expansion opportunity for the domestic market.

Sovereign Cloud and Government Digital Infrastructure Modernization Initiatives

Malaysia’s public sector digital transformation agenda and national data sovereignty priorities create significant opportunity for development of sovereign cloud infrastructure platforms hosted within national jurisdiction and compliant with government security frameworks. Government agencies increasingly require localized cloud environments supporting sensitive data processing, national digital identity systems, and integrated public service platforms. Domestic telecom and technology providers partner with global hyperscalers to deliver sovereign cloud architectures combining international technology with local hosting and governance. Public sector cloud adoption programs drive infrastructure demand across ministries, healthcare systems, and smart city initiatives. National cybersecurity strategies encourage deployment of secure domestic cloud environments, increasing investment in certified data centers and secure cloud platforms. Government procurement frameworks provide long-term infrastructure contracts supporting provider investment stability. Sovereign cloud initiatives also stimulate domestic ecosystem development including cloud engineering, cybersecurity, and data analytics capabilities. Localization requirements favor domestic operators and joint ventures in infrastructure deployment. These modernization and sovereignty initiatives represent a sustained structural opportunity driving expansion of Malaysia cloud infrastructure market over the long term.

Future Outlook

Malaysia cloud infrastructure market is expected to expand steadily over the next five years driven by hyperscale data center investments, enterprise digital transformation, and regional cloud demand spillover from ASEAN markets. Continued government digital economy programs and sovereign cloud initiatives will accelerate public sector adoption. Technological advances in AI infrastructure, edge computing, and high-density data centers will shape capacity expansion. Increasing sustainability requirements and renewable energy integration will influence infrastructure design and investment patterns.

Major Players

- Telekom Malaysia

- TM One

- Axiata Digital Services

- Maxis Berhad

- TIME dot Com Berhad

- YTL Communications

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Alibaba Cloud

- Tencent Cloud

- Oracle Cloud

- Equinix

- NTT Global Data Centers

- Bridge Data Centres Malaysia

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hyperscale cloud providers

- Telecommunications operators

- Data center developers

- Enterprise IT and digital transformation leaders

- Financial institutions

- Digital platform companies

Research Methodology

Step 1: Identification of Key Variables

Key demand and supply variables including hyperscale investments, enterprise cloud adoption, data center capacity, and sector digitalization trends were identified through secondary research and industry databases. Regulatory frameworks, energy constraints, and regional connectivity factors influencing Malaysia cloud infrastructure market were mapped.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using triangulation of data center capacity data, cloud revenue benchmarks, enterprise IT spending patterns, and hyperscaler investment announcements specific to Malaysia. Segmentation shares were derived from sector adoption and infrastructure allocation trends.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through expert inputs from cloud infrastructure providers, telecom operators, and regional data center specialists. Assumptions on growth drivers, regulatory impact, and regional positioning were refined based on industry consensus and deployment evidence.

Step 4: Research Synthesis and Final Output

Validated data and qualitative insights were synthesized into a structured Malaysia cloud infrastructure market framework including segmentation, competitive landscape, and forward outlook. Final outputs were reviewed for internal consistency and alignment with infrastructure investment trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid digitalization of enterprises and public services

Expansion of hyperscale data center investments

Government cloud-first and digital economy initiatives

Rising demand for AI and data analytics infrastructure

Growth of ecommerce and digital platforms requiring scalable compute - Market Challenges

High capital and energy requirements for data centers

Latency and connectivity constraints in secondary regions

Data sovereignty and regulatory compliance complexity

Shortage of specialized cloud engineering talent

Cybersecurity and data protection risks - Market Opportunities

Development of regional hyperscale campuses in Malaysia

Growth in sovereign and government cloud platforms

Expansion of edge cloud for 5G and IoT ecosystems - Trends

Shift toward multi-cloud and hybrid architectures

Adoption of AI accelerated cloud infrastructure

Integration of telecom networks with cloud platforms

Rise of sustainable and green data centers

Growth of containerized and cloud-native workloads - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Multi-Cloud Infrastructure

Edge Cloud Infrastructure - By Platform Type (In Value%)

Compute Infrastructure

Storage Infrastructure

Networking Infrastructure

Virtualization Platforms

Container and Kubernetes Platforms - By Fitment Type (In Value%)

Greenfield Cloud Deployments

Brownfield Data Center Modernization

Colocation Integrated Cloud

On-Premise Cloud Stack

Managed Cloud Hosting - By End User Segment (In Value%)

Banking and Financial Services

Telecommunications and Digital Services

Government and Public Sector

Ecommerce and Digital Platforms

Manufacturing and Industrial Enterprises - By Procurement Channel (In Value%)

Direct Hyperscaler Contracts

Telecom Operator Bundled Cloud

System Integrator Procurement

Managed Service Provider Contracts

Government Framework Agreements - By Material / Technology (in Value %)

x86 Server Infrastructure

ARM-Based Cloud Servers

Software Defined Networking

Hyperconverged Infrastructure

AI Optimized GPU Infrastructure

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Service Portfolio Breadth, Data Center Footprint, Network Integration Capability, Security and Compliance Certifications, Pricing Model Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Telekom Malaysia

TM One

Axiata Digital Services

Maxis Berhad

TIME dotCom Berhad

YTL Communications

Amazon Web Services

Microsoft Azure

Google Cloud

Alibaba Cloud

Tencent Cloud

Oracle Cloud

Equinix

NTT Global Data Centers

Bridge Data Centres Malaysia

- Banks and financial institutions scaling secure hybrid cloud platforms

- Telecom operators integrating network and edge cloud capabilities

- Government agencies migrating services to sovereign cloud

- Digital enterprises expanding hyperscale compute and storage usage

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now