Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia’s cold chain logistics sector operates as a critical component of the country’s food distribution and pharmaceutical supply infrastructure, with the market valued at approximately USD ~ billion based on a recent historical assessment derived from industry trade statistics and logistics sector reports published by the Malaysian Investment Development Authority and regional logistics associations. Market growth is primarily supported by increasing imports of temperature sensitive food products, pharmaceutical distribution expansion, rising organized retail networks, and continuous investment in refrigerated transport and warehouse infrastructure.

Major logistics activity is concentrated in Kuala Lumpur, Selangor, Penang, and Johor due to the presence of major ports, pharmaceutical manufacturing zones, and food distribution hubs connected to international trade corridors. Port Klang and Tanjung Pelepas function as key logistics gateways handling temperature controlled cargo flows, while Kuala Lumpur serves as a pharmaceutical distribution center supported by advanced warehouse facilities and airport cargo terminals that facilitate efficient storage and transportation of perishable products.

Market Segmentation

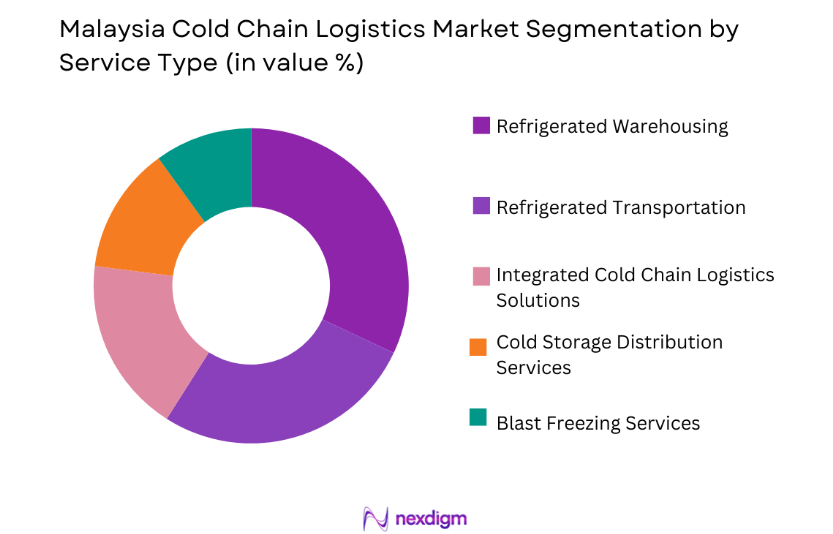

By Service Type

Malaysia Cold Chain Logistics market is segmented by service type into refrigerated transportation, refrigerated warehousing, blast freezing services, cold storage distribution services, and integrated cold chain logistics solutions. Recently, refrigerated warehousing has a dominant market share due to factors such as increasing pharmaceutical storage requirements, expansion of frozen food imports, and the development of large distribution centers supporting supermarket and food processing supply chains. Large scale temperature controlled warehouses located near seaports and urban consumption centers support long term storage of perishable goods while maintaining strict regulatory compliance for pharmaceutical and food safety standards across national logistics networks.

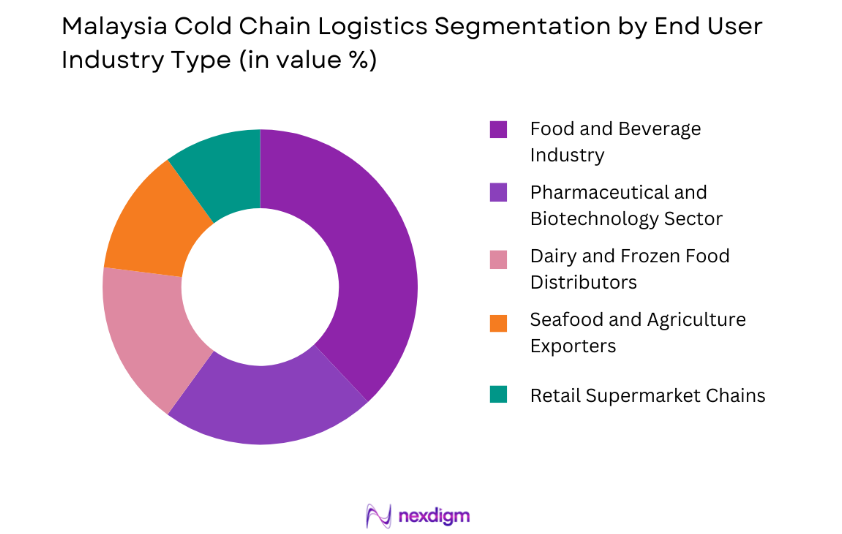

By End User Industry

Malaysia Cold Chain Logistics market is segmented by end user industry into food and beverage industry, pharmaceutical and biotechnology sector, seafood and agriculture exporters, dairy and frozen food distributors, and retail supermarket chains. Recently, the food and beverage industry has a dominant market share due to factors such as increasing frozen food consumption, rising imported seafood volumes, expanding supermarket retail chains, and growing demand for temperature controlled storage across processed food distribution networks serving urban consumer markets across Malaysia.

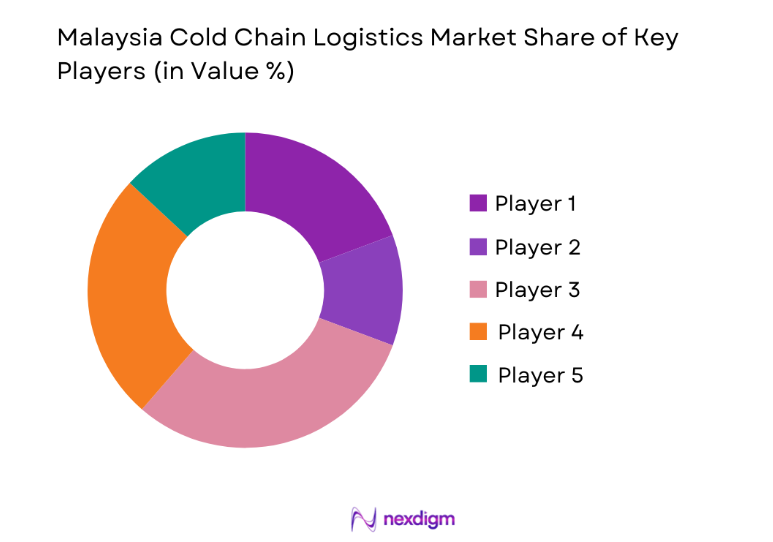

Competitive Landscape

The Malaysia cold chain logistics market is moderately consolidated with a mix of multinational logistics providers and domestic cold storage operators competing across warehousing, transportation, and integrated distribution services. Large logistics firms dominate pharmaceutical and export oriented cold storage operations due to their advanced infrastructure and regulatory compliance capabilities. Local logistics operators focus primarily on domestic food distribution networks and regional warehouse services. Increasing demand for pharmaceutical logistics and temperature controlled food distribution continues to encourage partnerships between global logistics companies and domestic infrastructure providers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Refrigerated Warehouse Capacity |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Lineage Logistics | 2008 | United States | ~ | ~ | ~ | ~ | ~ |

| Tasco Logistics | 2007 | Malaysia | ~ | ~ | ~ | ~ | ~ |

Malaysia Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Temperature Controlled Pharmaceutical Distribution Networks

Malaysia’s pharmaceutical distribution network increasingly relies on specialized cold chain logistics systems to maintain strict temperature integrity across vaccine storage biologics transportation insulin distribution and specialty medicine handling within national healthcare supply chains. Hospitals pharmaceutical manufacturers and healthcare distributors require reliable refrigerated transportation and controlled storage environments to prevent product degradation and ensure regulatory compliance across medical supply chains. The expansion of pharmaceutical manufacturing clusters and clinical distribution facilities further increases demand for certified cold chain logistics infrastructure. Government supported healthcare modernization programs have also increased the movement of temperature sensitive medicines between urban hospitals and regional medical centers. Pharmaceutical wholesalers increasingly depend on advanced cold warehouses and refrigerated trucking fleets to support national drug distribution networks. The growth of biologic medicines and advanced therapeutics has strengthened demand for ultra low temperature storage facilities across pharmaceutical logistics operations. These factors collectively strengthen the demand for reliable cold chain logistics infrastructure throughout Malaysia’s pharmaceutical supply ecosystem.

Rapid Expansion of Organized Food Retail and Frozen Food Imports

Malaysia’s growing urban population and evolving consumer food consumption patterns are driving strong demand for refrigerated logistics services supporting frozen food imports seafood distribution and processed food retail supply chains. Large supermarket chains hypermarkets and modern grocery platforms increasingly require temperature controlled storage infrastructure to manage perishable food inventories across multiple cities. The import of frozen meat dairy products seafood and processed food products from international suppliers requires specialized refrigerated cargo handling facilities at seaports and airports. Logistics operators are therefore investing heavily in refrigerated warehouse development near major consumption centers. The expansion of food processing industries and quick service restaurant chains also contributes to increasing demand for reliable cold storage distribution systems. Urban food distribution networks rely on refrigerated transport fleets to deliver perishable food products from central warehouses to retail stores while maintaining strict food safety standards. These structural changes in food supply systems continue to accelerate the growth of Malaysia’s cold chain logistics market.

Market Challenges

High Infrastructure Investment and Operational Cost Requirements

Developing and operating cold chain logistics infrastructure requires substantial capital investment in refrigerated warehouses temperature controlled transport fleets advanced monitoring technologies and energy intensive refrigeration systems across logistics facilities. Logistics operators must invest in high capacity cold storage warehouses equipped with insulation systems refrigeration compressors temperature monitoring sensors and backup power infrastructure to ensure uninterrupted cold storage operations. Energy consumption for refrigeration systems significantly increases operating costs for cold storage facilities especially in tropical climates where temperature control requires continuous energy usage. Smaller logistics providers often struggle to compete with large multinational operators due to limited financial resources required for cold storage infrastructure expansion. Maintenance of refrigeration systems and compliance with food safety and pharmaceutical regulatory standards further increase operational expenses. These cost pressures create barriers for new market entrants and limit the expansion of cold chain infrastructure in smaller regional logistics markets. The financial intensity of cold storage investments therefore remains a significant challenge affecting market development.

Fragmented Logistics Networks and Supply Chain Coordination Limitations

Malaysia’s cold chain logistics ecosystem faces operational challenges due to fragmented supply chain networks involving multiple transportation providers warehouse operators food distributors and pharmaceutical wholesalers across different regions. Inefficient coordination between logistics stakeholders often results in delays temperature fluctuations and product spoilage risks within perishable supply chains. Rural distribution networks remain particularly vulnerable due to limited availability of advanced refrigerated transportation infrastructure connecting remote agricultural production areas with urban consumption centers. Small logistics companies operating refrigerated trucks often lack digital tracking systems that monitor temperature integrity across transportation routes. Supply chain visibility limitations can therefore reduce operational efficiency and increase product losses within perishable food distribution networks. Integration between warehouse management systems transport management systems and supplier logistics platforms remains inconsistent across many logistics operators. Addressing these coordination challenges requires greater adoption of digital logistics technologies and integrated supply chain platforms to ensure reliable cold chain performance across the national distribution network.

Opportunities

Expansion of Pharmaceutical Biologics and Vaccine Logistics Infrastructure

The rapid growth of biologic medicines advanced vaccines and specialty pharmaceutical therapies across Asia presents significant opportunities for cold chain logistics providers operating in Malaysia. Biologic drugs require strict temperature controlled storage environments including ultra low temperature logistics systems capable of preserving product stability during transportation and storage. Pharmaceutical companies increasingly require certified logistics partners capable of maintaining validated temperature conditions throughout the supply chain. Malaysia’s strategic location within Southeast Asia positions the country as a regional pharmaceutical distribution hub for international drug manufacturers. Investment in pharmaceutical logistics facilities including validated cold storage warehouses and GDP compliant transportation networks is therefore expanding rapidly. Healthcare authorities are also strengthening regulatory frameworks governing pharmaceutical logistics to ensure safe distribution of temperature sensitive medicines. Logistics providers capable of developing pharmaceutical grade cold chain infrastructure can benefit from long term supply agreements with pharmaceutical manufacturers healthcare distributors and government health programs.

Growth of Export Oriented Seafood and Agricultural Cold Chain Networks

Malaysia’s seafood aquaculture and agricultural export industries require reliable cold chain logistics systems to maintain product freshness during international transportation to key export markets across Asia Europe and the Middle East. Exporters of seafood tropical fruits poultry and processed food products depend heavily on refrigerated storage and transportation systems connecting production areas with seaports and airport cargo terminals. The development of modern cold storage facilities near fishing ports and agricultural processing zones is therefore expanding rapidly. Export oriented cold chain logistics services also require advanced packaging temperature monitoring and cargo handling technologies that ensure product quality during international shipment. Increasing demand for premium seafood and tropical agricultural products from international markets creates strong incentives for investment in export focused refrigerated logistics infrastructure. Cold chain providers capable of supporting integrated export logistics services will benefit from expanding agricultural trade volumes across Malaysia’s international food export industry.

Future Outlook

Malaysia’s cold chain logistics market is expected to experience sustained growth as food distribution systems modernize and pharmaceutical supply chains expand across Southeast Asia. Increasing investment in refrigerated warehouses automated logistics technologies and digital monitoring platforms will strengthen cold chain reliability. Government initiatives supporting food safety standards and pharmaceutical distribution compliance will further encourage infrastructure development. Rising international food trade and healthcare logistics demand are likely to accelerate long term market expansion.

Major Players

- DHL Supply Chain

- DB Schenker

- Kuehne + Nagel

- Lineage Logistics

- Tasco Logistics

- Agility Logistics

- CEVA Logistics

- DSV

- FedEx Logistics

- Yusen Logistics

- Nichirei Logistics Group

- Swire Cold Storage

- Americold Logistics

- Sinotrans Cold Chain Logistics

- JD Cold Chain Logistics

Key Target Audience

- Cold chain logistics companies

- Food and beverage manufacturing companies

- Pharmaceutical and biotechnology companies

- Retail supermarket chains

- Investments and venture capitalist firms

- Government and regulatory bodies

- International food export companies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including refrigerated warehouse capacity food import volumes pharmaceutical distribution infrastructure and logistics investment trends were identified through government trade databases logistics industry reports and supply chain infrastructure studies.

Step 2: Market Analysis and Construction

Market structure was constructed using logistics infrastructure capacity analysis temperature controlled warehouse statistics transportation fleet data and trade flow analysis across Malaysia’s food and pharmaceutical supply chains.

Step 3: Hypothesis Validation and Expert Consultation

Industry insights were validated through consultations with logistics operators supply chain managers cold storage infrastructure developers and pharmaceutical distribution specialists active in Malaysia’s logistics sector.

Step 4: Research Synthesis and Final Output

All validated quantitative data industry insights infrastructure capacity trends and regulatory information were synthesized to produce the final market analysis including segmentation competitive landscape and future growth outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Perishable Food Import and Export Trade

Growth of Pharmaceutical and Vaccine Distribution Networks

Increasing Demand for Temperature Controlled E Commerce Food Delivery - Market Challenges

High Capital Investment for Refrigerated Infrastructure Development

Energy Consumption and Operational Cost Pressures

Limited Cold Chain Infrastructure in Secondary Logistics Corridors - Market Opportunities

Expansion of Pharmaceutical and Biotech Supply Chain Logistics

Growth of Halal Food Export Cold Chain Infrastructure

Development of Smart Cold Chain Monitoring Technologies - Trends

Adoption of IoT Enabled Temperature Monitoring Systems

Integration of Automated Cold Storage Warehousing Technologies - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Warehousing Systems

Temperature Controlled Transportation Systems

Cold Storage Distribution Centers

Pharmaceutical Cold Chain Systems

Integrated Cold Chain Monitoring Systems - By Platform Type (In Value%)

Road Refrigerated Transport

Air Cargo Cold Chain Logistics

Sea Freight Refrigerated Container Logistics

Rail Temperature Controlled Logistics - By Fitment Type (In Value%)

Standalone Cold Storage Facilities

Integrated Logistics Hub Facilities

Mobile Refrigeration Units

Modular Cold Storage Infrastructure - By End User Segment (In Value%)

Food and Beverage Distribution Companies

Pharmaceutical and Biotechnology Companies

Retail and Supermarket Chains

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Technology Integration, Geographic Coverage, Service Portfolio, Temperature Control Range, Logistics Network Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain Malaysia

DB Schenker Malaysia

Kuehne + Nagel Malaysia

CEVA Logistics Malaysia

DSV Malaysia

Yusen Logistics Malaysia

Tiong Nam Logistics Holdings

Cold Chain Network Malaysia

Agility Logistics Malaysia

CJ Century Logistics Holdings

FM Global Logistics

Swift Haulage Berhad

Bolloré Logistics Malaysia

GDEX Cold Chain Solutions

Tasco Berhad

- Growing Demand from Pharmaceutical Manufacturers for Vaccine Storage Logistics

- Supermarket Chains Expanding Temperature Controlled Distribution Networks

- Food Export Companies Increasing Use of Refrigerated Container Logistics

- Online Grocery Platforms Requiring Rapid Cold Chain Delivery Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now