Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Malaysia diagnostic labs market is currently valued at approximately USD ~ billion, driven by growing healthcare awareness, technological advancements, and the rising prevalence of chronic diseases. The market has seen robust growth with increasing demand for diagnostic services fueled by government health initiatives and the expansion of healthcare infrastructure. The high demand for quality healthcare services, coupled with advancements in diagnostic technology, particularly in molecular diagnostics and imaging, has contributed significantly to the market’s growth. This trend is supported by both public and private investments in the healthcare sector.

The market is largely concentrated in urban areas such as Kuala Lumpur, Penang, and Johor Bahru, where the healthcare infrastructure is more developed and accessible. These cities serve as hubs for diagnostic laboratories due to the higher population density, greater disposable income, and the availability of skilled healthcare professionals. Kuala Lumpur, in particular, is at the forefront, hosting major diagnostic facilities and benefiting from both local and international healthcare investments. The dominance of these cities is attributed to their central role in healthcare delivery, coupled with ongoing infrastructure improvements and government support for urban healthcare development.

Market Segmentation

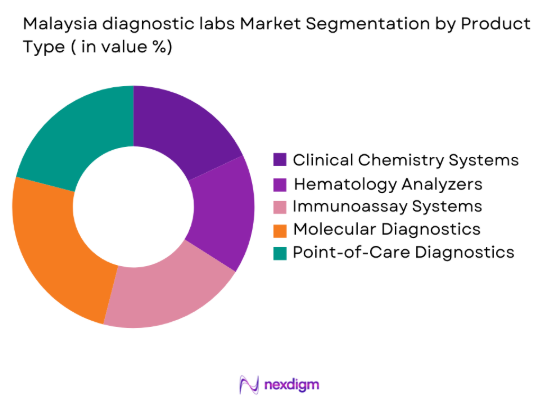

By Product Type

The Malaysia diagnostic labs market is segmented by product type into clinical chemistry systems, hematology analyzers, immunoassay systems, molecular diagnostics, and point-of-care diagnostics. Recently, molecular diagnostics has seen the highest market share due to factors such as advancements in genetic testing, the growing demand for precision medicine, and the increasing adoption of innovative technologies in healthcare. The rise in chronic disease prevalence, such as cancer and genetic disorders, has further increased the demand for molecular diagnostic tools.

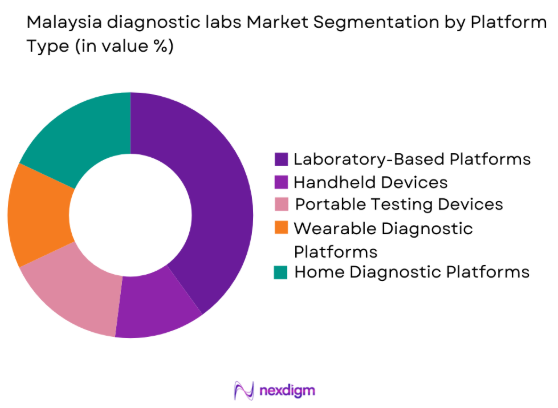

By Platform Type

The market is segmented by platform type into laboratory-based platforms, handheld devices, portable testing devices, wearable diagnostic platforms, and home diagnostic platforms. Laboratory-based platforms dominate the market due to the high volume of diagnostic tests conducted in centralized labs across Malaysia. These platforms are preferred for their accuracy, efficiency, and ability to handle large-scale testing, making them the go-to choice for healthcare facilities seeking reliable diagnostic results. The increasing number of hospitals and diagnostic centers has further propelled the adoption of these platforms.

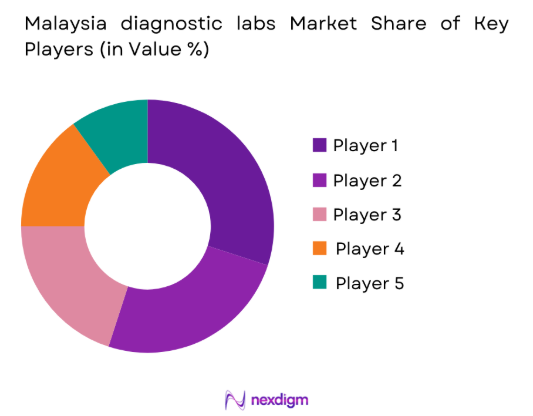

Competitive Landscape

The Malaysia diagnostic labs market is competitive, with major players continually expanding their technological capabilities and geographic reach. The market has seen significant consolidation, as larger players acquire smaller diagnostic companies to enhance their service offerings and expand their market presence. Leading players dominate the landscape by leveraging their advanced technologies, extensive distribution networks, and robust brand recognition. These companies focus on product innovation, customer satisfaction, and compliance with strict regulatory standards to maintain their competitive edge. The market is characterized by continuous technological advancements, particularly in molecular diagnostics and point-of-care solutions, which are expected to drive future growth.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | USA | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| GE Healthcare | 1892 | USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Ireland | ~ | ~ | ~ | ~ | ~ |

Malaysia diagnostic labs Market Analysis

Growth Drivers

Technological Advancements in Diagnostic Tools

The continuous advancement in diagnostic technologies, especially in molecular diagnostics and imaging, is a key growth driver for the Malaysia diagnostic labs market. These innovations improve the speed, accuracy, and efficiency of diagnostic tests, enabling healthcare providers to offer better services. Additionally, advancements in point-of-care diagnostic solutions have made it possible for diagnostic tests to be conducted outside traditional laboratory settings, improving accessibility and reducing waiting times for patients. These technologies also aid in early detection, which is critical in the treatment of diseases such as cancer and diabetes. As healthcare providers adopt these advanced tools, the demand for sophisticated diagnostic systems will continue to grow, propelling market growth.

Expansion of Healthcare Infrastructure

The expansion of healthcare infrastructure in Malaysia is a key growth driver for the diagnostic labs market. With growing investments from both public and private sectors, diagnostic labs are expanding rapidly across urban and rural regions. Government initiatives aimed at improving healthcare access and quality are promoting the establishment of new diagnostic centers, boosting market growth. As more healthcare facilities are developed, there is a corresponding rise in demand for diagnostic services, driven by increased access to advanced healthcare systems. This growing network of diagnostic labs is helping to meet the rising healthcare needs of a larger and more diverse patient population across the country.

Market Challenges

Regulatory Compliance and Standardization

A major challenge for the Malaysia diagnostic labs market is the complex and constantly changing regulatory landscape. Diagnostic labs must comply with stringent regulations and certifications to ensure the accuracy, safety, and reliability of their services. Navigating these requirements can be both time-consuming and costly, especially for smaller centers that lack the resources to meet all regulatory demands. In addition, regulatory barriers such as inconsistent standards and lengthy approval processes for new diagnostic products further slow market growth. These challenges limit the ability of diagnostic labs to quickly adopt or introduce innovative solutions, hindering their competitiveness and growth in the rapidly evolving healthcare sector.

High Operational Costs for Diagnostic Labs

Operating diagnostic labs requires substantial financial investment, including the purchase of expensive diagnostic equipment, ongoing maintenance costs, and the need for skilled personnel. For smaller diagnostic centers, these operational expenses pose a significant barrier to entry and hinder growth, limiting their capacity to scale services or adopt advanced technologies. Larger market players, with greater financial resources, can absorb these costs, giving them a competitive advantage. In contrast, smaller labs face financial constraints, which restrict their ability to compete effectively. This challenge makes it difficult for them to meet the increasing demand for high-quality diagnostic services, ultimately limiting their market expansion opportunities.

Opportunities

Growing Demand for Home-Based Diagnostics

The growing trend of home-based diagnostics presents a key opportunity for the Malaysia diagnostic labs market. Driven by advancements in telemedicine, wearable health technologies, and consumer preferences for convenience, there is a rising demand for diagnostic services that can be performed from home. This shift reflects a desire for more accessible, cost-effective healthcare solutions and is supported by the increasing focus on preventive healthcare. As more consumers seek at-home testing options, diagnostic labs can leverage this trend by offering remote testing services. By doing so, they can expand their market reach, attract a broader customer base, and strengthen their position in the evolving healthcare landscape.

Government Support for Healthcare Development

The Malaysian government’s ongoing investment in healthcare infrastructure and digital health initiatives presents a significant opportunity for the diagnostic labs market. Efforts to improve healthcare access and quality include expanding healthcare facilities, particularly diagnostic labs. Furthermore, government incentives to adopt advanced healthcare technologies and digital health solutions will encourage diagnostic labs to upgrade their equipment and services. This support will stimulate market growth, driving the adoption of innovative diagnostic tools and creating new opportunities for service providers to meet the increasing demand for high-quality healthcare solutions. These initiatives will be crucial in shaping the future of the diagnostic labs market in Malaysia.

Future Outlook

The Malaysia diagnostic labs market is expected to continue its upward trajectory in the next five years, driven by advancements in diagnostic technologies, increased healthcare spending, and government support for healthcare infrastructure. The market will see significant growth in the adoption of molecular diagnostics, wearable health devices, and point-of-care testing solutions. The shift toward home-based diagnostics and remote healthcare services will further expand market opportunities. Additionally, the increasing prevalence of chronic diseases, combined with the expansion of healthcare facilities, will ensure sustained demand for diagnostic services.

Major Players

- Siemens Healthineers

- Abbott Laboratories

- Roche Diagnostics

- GE Healthcare

- Medtronic

- Philips Healthcare

- ThermoFisher Scientific

- Bio-Rad Laboratories

- Mindray

- Sysmex Corporation

- BD Diagnostics

- Horiba Medical

- PerkinElmer

- Beckman Coulter

- Abbott Point of Care

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare service providers

- Hospitals and diagnosticcenters

- Medical technology developers

- Pharmaceutical companies

- Diagnostic equipment manufacturers

- Insurance companies

Research Methodology

Step 1: Identification of Key Variables

Identify key variables and trends influencing the market, including technological advancements, regulatory factors, and demand-side drivers.

Step 2: Market Analysis and Construction

Analyze market size, trends, and segmentation, focusing on product types, platforms, and market dynamics that affect growth.

Step 3: Hypothesis Validation and Expert Consultation

Validate the hypotheses formed during analysis through expert consultations and secondary research from industry leaders and market reports.

Step 4: Research Synthesis and Final Output

Synthesize findings from all research phases into a comprehensive report, ensuring accurate and actionable insights for decision-makers.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased healthcare spending

Technological advancements in diagnostic equipment

Growing prevalence of chronic diseases - Market Challenges

High cost of diagnostic equipment

Regulatory hurdles in equipment approval

Limited access to advanced diagnostic technologies in rural areas - Market Opportunities

Expansion of diagnostic labs in underserved regions

Increase in telemedicine and remote diagnostics

Rise in public-private partnerships for healthcare advancements - Trends

Adoption of AI and machine learning in diagnostics

Growing preference for non-invasive diagnostic techniques

Emerging market for personalized medicine - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Systems

Hematology Analyzers

Immunoassay Systems

Molecular Diagnostics

Point-of-Care Diagnostics - By Platform Type (In Value%)

Laboratory-Based Platforms

Handheld Devices

Portable Testing Devices

Wearable Diagnostic Platforms

Home Diagnostic Platforms - By Fitment Type (In Value%)

In-House Diagnostic Labs

Outsourced Diagnostic Labs

Molle Diagnostic Units

Clinic-Based Diagnostic Units

Home-Based Diagnostic Kits - By End User Segment (In Value%)

Hospitals

Diagnostic Laboratories

Clinics

Home Healthcare Providers

Research Institutes - By Procurement Channel (In Value%)

Direct Procurement

Online Platforms

Third-Party Distributors

Government Tenders

Private Sector Procurement

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Diagnostic Technology, Market Reach, Product Innovation, Distribution Network, Customer Demographics)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Abbott Laboratories

Siemens Healthineers

Thermo Fisher Scientific

Roche Diagnostics

GE Healthcare

Medtronic

Philips Healthcare

Danaher Corporation

BD Diagnostics

PerkinElmer

Bio-Rad Laboratories

Sysmex Corporation

Abbott Point of Care

Mindray

Horiba Medical

- Increased demand for diagnostics in hospitals

- Expansion of diagnostic services in clinics

- Rising focus on preventive healthcare

- Growth of home-based diagnostic testing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now