Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Malaysia digital health market has seen rapid growth, driven by the increasing demand for advanced healthcare technologies and digital solutions. As of a recent historical assessment, the market size is projected to reach USD ~ billion, with healthcare providers embracing digital platforms, telemedicine, and wearable devices to enhance patient care, operational efficiency, and cost-effectiveness. The government’s focus on improving healthcare infrastructure and expanding digital health services also plays a significant role in this market’s growth, as public and private sectors invest in integrating digital health technologies across Malaysia.

Key cities such as Kuala Lumpur, Penang, and Johor Bahru are dominant players in the market, with large healthcare providers and medical centers adopting digital solutions. Malaysia’s strategic position in Southeast Asia and its robust healthcare sector make it an attractive hub for digital health investments. The country’s healthcare modernization efforts, along with government incentives and policies, particularly in urban regions, contribute to its market dominance. These cities lead the way in healthcare innovation, particularly in telemedicine, diagnostic technologies, and health information systems, establishing Malaysia as a regional leader in digital health.

Market Segmentation

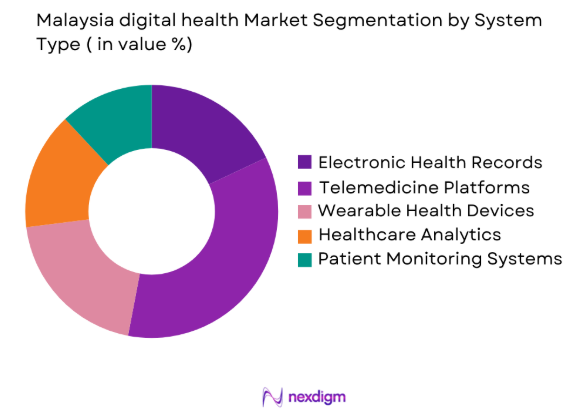

By System Type

The Malaysia digital health market is segmented by system type into electronic health records, telemedicine platforms, wearable health devices, healthcare analytics software, and patient monitoring systems. Recently, telemedicine platforms have a dominant market share due to the increased adoption of virtual consultations and healthcare services, especially amidst the COVID-19 pandemic. Factors such as government support for telehealth policies, advancements in broadband connectivity, and the growing acceptance of online consultations among healthcare providers and patients have significantly contributed to the growth of telemedicine platforms in Malaysia.

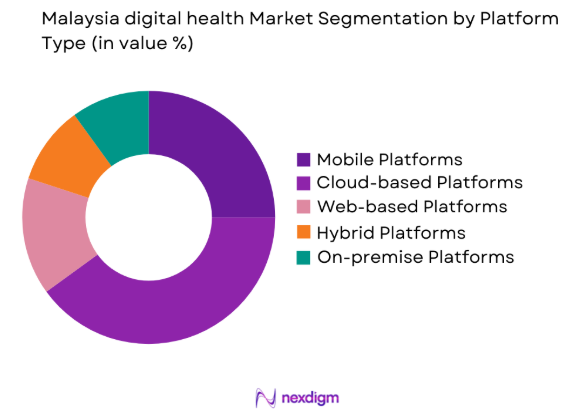

By Platform Type

The Malaysia digital health market is also segmented by platform type into mobile platforms, cloud-based platforms, web-based platforms, hybrid platforms, and on-premise platforms. Cloud-based platforms dominate the market due to their scalability, flexibility, and cost-effectiveness. With the increasing adoption of cloud technology by healthcare providers to store and manage patient data securely, cloud-based platforms offer significant advantages in terms of accessibility and integration across various healthcare systems, contributing to their strong market position.

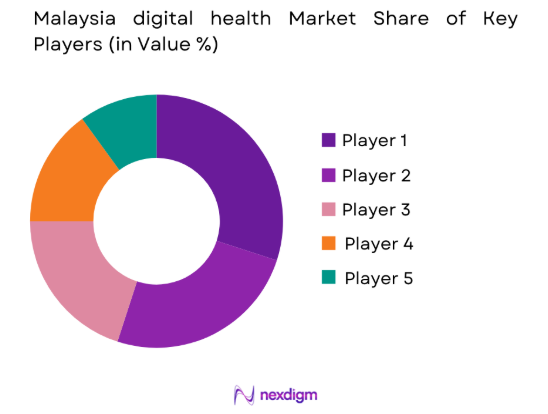

Competitive Landscape

The competitive landscape of the Malaysia digital health market is characterized by the presence of several global and local players competing to offer advanced healthcare solutions. Consolidation in the market is being driven by mergers, acquisitions, and partnerships between healthcare providers, technology companies, and government bodies. Major players are increasingly focusing on expanding their product offerings to cater to the growing demand for digital health services across the region.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| Cerner Corporation | 1979 | USA | ~ | ~ | ~ | ~ | ~ |

| GE Healthcare | 1892 | USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Ireland | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| IBM Watson Health | 2015 | USA | ~ | ~ | ~ | ~ | ~ |

Malaysia digital health Market Analysis

Growth Drivers

Government Initiatives in Digital Health

The Malaysian government’s strong support for digital health initiatives has been a major growth driver for the market. Through policies and funding, the government has aimed to improve the country’s healthcare infrastructure by encouraging the adoption of digital health solutions like telemedicine, electronic health records, and patient monitoring systems. These initiatives are driven by the need to modernize healthcare services, improve patient access, and enhance operational efficiencies in the healthcare sector. The government’s focus on promoting digital health technologies, such as through the National eHealth Initiative, has fostered collaborations between public and private sectors, accelerating the implementation of digital health systems across the nation.

Technological Advancements in Health Tech

A key growth driver in the Malaysia digital health market is the rapid advancement of health technologies, including artificial intelligence (AI), machine learning, and big data analytics. The integration of these technologies enables personalized patient care, predictive analytics, and enhanced healthcare resource management. AI-driven platforms are being increasingly adopted for diagnostic purposes, while machine learning and predictive analytics help healthcare providers make more accurate, timely decisions. As healthcare providers across Malaysia continue to integrate these technologies into their operations, the demand for advanced health tech products is expected to grow. This trend is expected to accelerate the expansion of the digital health market, providing better healthcare outcomes and improved efficiency.

Market Challenges

Data Privacy and Security Concerns

Data privacy and security pose significant challenges in the Malaysia digital health market as the volume of electronic health records and patient data grows. The rising frequency of cyberattacks and data breaches in the healthcare sector raises concerns about the confidentiality and security of sensitive patient information. Malaysia’s healthcare system is addressing these issues by enhancing cybersecurity measures and adhering to data protection regulations like the Personal Data Protection Act (PDPA). However, the persistent threat of cyberattacks, coupled with the constantly evolving nature of digital threats, continues to present major challenges for the market. Ensuring robust security and maintaining patient trust are critical for the successful expansion of digital health services in Malaysia.

High Implementation Costs

The high cost of implementing digital health systems remains a significant challenge in the Malaysian market. Hospitals and healthcare providers must invest heavily in advanced technologies such as electronic health records, telemedicine platforms, and patient monitoring systems, which come with substantial upfront costs. Small and medium-sized healthcare providers, in particular, face difficulties in managing these expenses, hindering the widespread adoption of digital health technologies across the sector. While the government offers financial incentives to support digital health integration, the additional costs associated with staff training, system maintenance, and upgrading infrastructure further burden healthcare providers. As a result, despite the potential benefits of digital health systems, these financial barriers limit their implementation and hinder broader adoption, especially among smaller healthcare entities.

Opportunities

Expansion of Telemedicine Services

The growth of telemedicine services offers substantial opportunities for the Malaysia digital health market. Telemedicine platforms allow healthcare providers to deliver consultations, diagnoses, and treatments remotely, improving access to healthcare, especially in rural areas. The COVID-19 pandemic accelerated telemedicine adoption, and as demand for remote healthcare continues to grow, this segment presents significant potential. Additionally, advancements in digital health technologies, such as video conferencing tools and AI-powered diagnostics, are expanding telemedicine’s capabilities and improving patient outcomes. These developments, along with growing consumer acceptance and government support, make telemedicine a key driver of the digital health market in Malaysia, offering innovative solutions for healthcare delivery.

Integration of Wearable Devices for Preventive Healthcare

The integration of wearable devices into digital health is driving significant market growth. Devices like fitness trackers, smartwatches, and health monitors enable real-time tracking of health metrics such as heart rate, sleep patterns, and physical activity. The rising consumer awareness of preventive healthcare, combined with the growing popularity of fitness and wellness, has fueled the demand for these devices. Wearables empower individuals to take control of their health while providing healthcare providers with valuable data for patient management. This combination of consumer interest and healthcare utility is opening up new opportunities for the digital health market, particularly in areas like chronic disease management and overall wellness monitoring.

Future Outlook

Over the next five years, the Malaysia digital health market is expected to continue its robust growth, driven by technological advancements, government support, and the growing adoption of digital healthcare solutions. The expansion of telemedicine services, the integration of AI and machine learning into healthcare, and the increasing use of wearable health devices will further propel the market forward. As the healthcare sector continues to modernize, the demand for digital health solutions will increase, creating new opportunities for companies to innovate and expand their offerings. Regulatory support and funding initiatives from the government will also play a crucial role in fostering the growth of the digital health market in Malaysia.

Major Players

- Cerner Corporation

- GE Healthcare

- Medtronic

- Philips Healthcare

- IBM Watson Health

- Siemens Healthineers

- Optum

- Johnson & Johnson

- Health Catalyst

- Allscripts Healthcare Solutions

- Oracle Corporation

- InterSystems Corporation

- McKesson Corporation

- Meditech

- SAS Institute

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Hospitals and medicalcenters

- Pharmaceutical companies

- Healthcare technology developers

- Insurance and healthcare financing companies

- Private healthcare investors

Research Methodology

Step 1: Identification of Key Variables

Identifying key variables involves gathering data on the digital health market, understanding its dynamics, and recognizing influential factors such as technological advancements, regulatory frameworks, and market trends.

Step 2: Market Analysis and Construction

This step involves analyzing data and constructing a comprehensive model of the digital health market, including market size, growth drivers, and challenges, based on primary and secondary research.

Step 3: Hypothesis Validation and Expert Consultation

The market hypotheses are validated through expert consultations and feedback from stakeholders, ensuring the model is accurate and applicable to current market conditions.

Step 4: Research Synthesis and Final Output

This final step involves synthesizing the research findings into a report that clearly outlines the market’s current status, growth prospects, and actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Government Support for Digital Healthcare Initiatives

Technological Advancements in AI and Machine Learning for Healthcare

Surge in Adoption of Telemedicine Due to COVID-19 Impact - Market Challenges

High Initial Investment Costs in Digital Health Systems

Privacy and Data Security Concerns

Lack of Standardization Across Digital Health Platforms - Market Opportunities

Growth of AI and IoT in Remote Patient Monitoring

Integration of Blockchain for Secure Health Data Management

Expansion of Wearable Health Devices for Preventive Care - Trends

Rise in Adoption of Mobile Health Applications

Technological Convergence with Wearable Devices

Increased Focus on Preventive Healthcare via Digital Platforms - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electronic Health Records

Telemedicine Platforms

Wearable Health Devices

Healthcare Analytics Software

Patient Monitoring Systems - By Platform Type (In Value%)

Mobile Platforms

Cloud-based Platforms

Web-based Platforms

Hybrid Platforms

On-premise Platforms - By Fitment Type (In Value%)

Personalized Solutions

Integrated Solutions

Cloud-based Solutions

AI-enabled Solutions

IoT-enabled Solutions - By End User Segment (In Value%)

Hospitals

Private Clinics

Healthcare Providers

Home Care

Pharmaceutical Companies - By Procurement Channel (In Value%)

Direct Procurement

Healthcare Tenders

Online Procurement Platforms

Private Sector Procurement

Distributors and Resellers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Integration, Market Penetration, Consumer Adoption Rates, Cost Efficiency, Regulatory Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Cerner Corporation

GE Healthcare

Allscripts Healthcare Solutions

Medtronic

Philips Healthcare

Siemens Healthineers

IBM Watson Health

Optum

Johnson & Johnson

Hewlett Packard Enterprise

Samsung Electronics

Mindray Medical

Zebra Medical Vision

Mobius Health

Apple Inc.

- Growth of Digital Health Adoption Among Hospitals

- Private Sector Push for Healthcare Digitization

- Role of Home Care in Expanding Digital Health Reach

- Rising Demand for Patient Monitoring Solutions in Clinics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now