Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia’s edge computing market reached approximately USD ~ million based on a recent historical assessment, supported by expanding 5G rollout, hyperscale data center investments, and industrial digitalization programs. Government initiatives under the MyDIGITAL blueprint and National Fourth Industrial Revolution Policy are accelerating deployment of localized processing infrastructure across manufacturing, logistics, and smart city applications, while telecom operators and cloud providers expand distributed compute nodes to support latency-sensitive enterprise workloads and connected device ecosystems nationwide.

Kuala Lumpur and Johor dominate Malaysia’s edge computing landscape due to concentration of hyperscale data centers, submarine cable landings, and proximity to Singapore’s regional cloud hub ecosystem. Penang’s advanced electronics manufacturing cluster drives industrial edge adoption across semiconductor fabrication and automation environments, while Cyberjaya’s established ICT infrastructure and government digital corridors sustain enterprise and public-sector deployments. Cross-border digital connectivity investments and industrial corridor development further reinforce these regions as focal points for distributed computing infrastructure expansion.

Market Segmentation

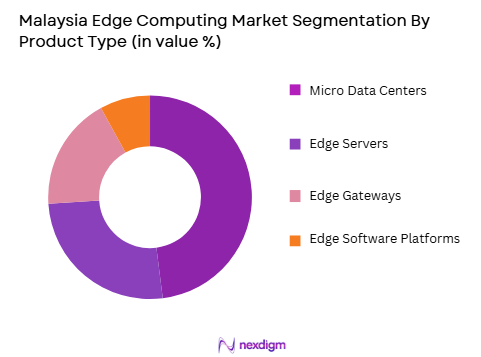

By Product Type

Malaysia Edge Computing market is segmented by product type into edge servers, edge gateways, micro data centers, and edge software platforms. Recently, micro data centers have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Their dominance stems from rapid enterprise demand for localized, modular compute capacity that can be deployed in telecom exchanges, factories, and logistics hubs without large-scale construction, aligning with Malaysia’s distributed industrial geography and telecom-led edge rollout models.

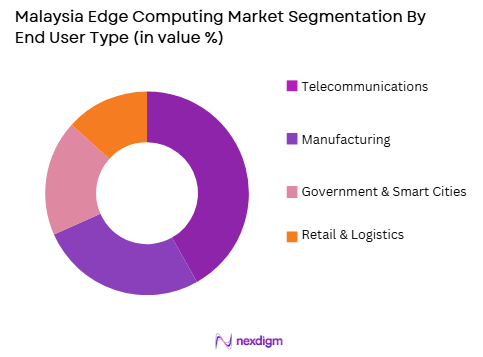

By End User

Malaysia Edge Computing market is segmented by end user into telecommunications, manufacturing, government & smart cities, and retail & logistics. Recently, telecommunications has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Telecom operators lead deployment because national 5G networks and mobile edge computing nodes require distributed compute at base stations and aggregation sites, positioning telecoms as primary investors and infrastructure hosts for enterprise and consumer edge services across Malaysia’s digital economy initiatives.

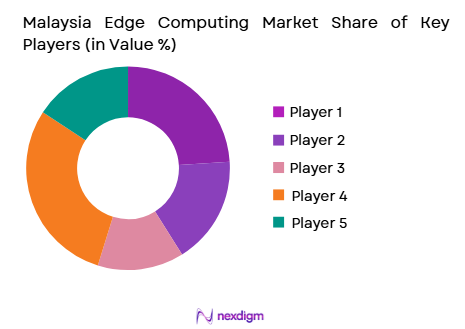

Competitive Landscape

Malaysia’s edge computing market shows moderate consolidation with global cloud providers, telecom operators, and infrastructure vendors shaping deployment models and technology standards. Partnerships between telecom carriers and hyperscalers define service ecosystems, while regional data center specialists expand modular edge facilities near industrial zones and connectivity hubs.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Malaysia Edge Deployment Model |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | USA | ~ | ~ | ~ | ~ | ~ |

| Schneider Electric | 1836 | France | ~ | ~ | ~ | ~ | ~ |

| Nokia | 1865 | Finland | ~ | ~ | ~ | ~ | ~ |

| Huawei | 1987 | China | ~ | ~ | ~ | ~ | ~ |

Malaysia Edge Computing Market Analysis

Growth Drivers

5G Network Expansion and Telecom Edge Infrastructure Investment

Malaysia’s nationwide 5G rollout is fundamentally reshaping the edge computing market by requiring distributed processing capacity at radio access and aggregation layers, prompting telecom operators to deploy mobile edge computing nodes across urban and industrial zones. The national single-wholesale 5G network structure has accelerated standardized infrastructure deployment, enabling faster integration of edge servers and micro data centers at telecom facilities. Enterprises adopting private 5G networks in manufacturing and logistics environments require localized compute to process machine vision, automation control, and real-time analytics workloads. Telecom-hyperscaler collaborations are expanding edge cloud availability zones within Malaysia, supporting latency-critical applications such as autonomous robotics, immersive media, and smart mobility platforms. Increasing mobile data traffic and video streaming demand also necessitate content caching and processing at the network edge, further driving telecom investment. Government digital infrastructure programs and spectrum policy frameworks support continuous expansion of edge-ready network architecture nationwide. As operators monetize 5G enterprise services, edge computing becomes integral to revenue diversification strategies through managed services and industrial connectivity solutions. This convergence of telecom modernization and enterprise digitalization ensures sustained demand for edge infrastructure deployment across Malaysia’s connectivity ecosystem.

Industrial Automation and Smart Manufacturing Digitalization

Malaysia’s advanced manufacturing base, particularly in electronics, semiconductor assembly, and precision engineering, is driving adoption of edge computing to enable Industry 4.0 operations requiring real-time processing and low-latency control. Manufacturing facilities increasingly deploy machine vision inspection, predictive maintenance analytics, and autonomous material handling systems that rely on localized compute nodes for deterministic performance. Penang’s semiconductor and electronics clusters and Johor’s industrial corridors host multinational factories integrating edge servers and micro data centers within production environments. Industrial IoT sensor networks generate high-volume data streams that cannot be economically transmitted to centralized clouds, reinforcing demand for on-premise edge processing. Government initiatives promoting smart factories and digital industrial transformation further accelerate enterprise investment in edge infrastructure. Edge computing also supports digital twin modeling, robotics coordination, and quality assurance analytics in manufacturing plants. Local system integrators and automation vendors are incorporating edge platforms into industrial solutions, expanding market penetration. As Malaysia strengthens its position in global electronics supply chains, manufacturers prioritize operational resilience and productivity gains enabled by distributed computing architectures, making industrial digitalization a central growth engine for the national edge computing market.

Market Challenges

High Capital Intensity and Infrastructure Integration Complexity

Edge computing deployments in Malaysia face significant financial and technical barriers due to the capital-intensive nature of distributed infrastructure requiring servers, power systems, cooling, connectivity, and secure facilities across multiple sites. Enterprises and telecom operators must invest in numerous small-scale nodes rather than centralized data centers, increasing total cost of ownership and operational complexity. Integrating edge platforms with existing IT, OT, and network environments requires specialized engineering capabilities that remain limited in local talent pools. Interoperability challenges between vendor hardware, telecom networks, and cloud platforms can delay deployment and increase integration risk. Industrial facilities often lack standardized environments for edge installation, necessitating site retrofitting and environmental controls. Cybersecurity risks expand with distributed nodes, requiring additional investment in monitoring and protection systems. Energy reliability and cooling constraints in certain industrial or remote locations further complicate infrastructure planning. These combined cost and integration factors slow adoption among smaller enterprises and create dependence on large telecom or multinational vendors to deploy and operate edge infrastructure across Malaysia.

Fragmented Enterprise Readiness and Limited Edge Application Ecosystem

Despite infrastructure expansion, many Malaysian enterprises remain in early digitalization stages, limiting immediate demand for advanced edge computing solutions that require mature data, automation, and analytics capabilities. Small and mid-sized firms often lack technical expertise and business cases to justify localized computing investments, slowing market diffusion beyond large manufacturing and telecom sectors. Industry-specific edge applications tailored to Malaysian use cases remain underdeveloped compared with mature markets, constraining perceived value among potential adopters. Skills shortages in distributed computing architecture, AI integration, and industrial IoT engineering hinder enterprise implementation capacity. Awareness gaps regarding latency-driven benefits and operational gains reduce executive prioritization of edge initiatives. Ecosystem fragmentation between telecom providers, cloud vendors, system integrators, and application developers complicates solution packaging and deployment. Regulatory uncertainty around data localization and cross-border processing in distributed architectures also affects enterprise planning. This combination of readiness gaps and ecosystem immaturity presents a structural adoption barrier in Malaysia’s evolving edge computing landscape.

Opportunities

Cross-Border Edge Interconnectivity with Singapore Digital Hub Ecosystem

Malaysia’s geographic proximity and fiber connectivity to Singapore position it uniquely to develop cross-border edge computing infrastructure serving regional enterprises requiring cost-efficient distributed processing outside Singapore’s constrained data center market. Johor’s expanding data center corridors and submarine cable landings enable deployment of edge nodes linked to hyperscale cloud regions in Singapore while operating under Malaysia’s cost and land advantages. Enterprises operating across ASEAN markets increasingly require hybrid architectures combining centralized cloud and localized processing across borders, creating demand for interoperable edge platforms. Telecom carriers and data center developers are investing in interconnection facilities that extend Singapore’s cloud availability zones into Malaysia through edge nodes. This cross-border digital architecture supports latency-sensitive financial services, gaming, and media distribution workloads serving Southeast Asia users. Government digital economy strategies emphasizing regional connectivity and data infrastructure reinforce this opportunity. As regional data traffic and digital services expand, Malaysia can capture investment by positioning itself as a distributed edge extension of the Singapore hub, strengthening national edge computing market growth.

Smart City and Public Infrastructure Digitalization Programs

Malaysia’s national and municipal digital transformation initiatives in transportation, urban services, utilities, and public safety create substantial opportunities for edge computing deployment within smart city infrastructure. Real-time traffic management, surveillance analytics, environmental monitoring, and connected public services require localized data processing at city nodes to ensure latency, reliability, and data governance compliance. Government agencies and municipal authorities are integrating IoT sensors and digital platforms across urban environments, generating continuous demand for edge servers and micro data centers. Smart mobility initiatives such as intelligent transport systems and autonomous public transit pilots depend on distributed compute architecture. Public-sector digital corridors such as Cyberjaya and planned smart industrial parks incorporate edge-ready infrastructure design. Telecom providers and technology vendors are partnering with municipalities to deploy urban edge nodes integrated with 5G networks. As Malaysia urbanizes and digital public services expand, government-led smart infrastructure programs will drive sustained adoption of edge computing platforms across cities and public utilities nationwide.

Future Outlook

Malaysia’s edge computing market is expected to expand steadily over the next five years as nationwide 5G coverage, smart manufacturing investments, and hyperscale data center growth accelerate distributed infrastructure deployment. Telecom-cloud partnerships will extend edge availability zones into industrial and urban nodes, while government digital economy programs stimulate public-sector and enterprise adoption. Increasing cross-border connectivity with regional digital hubs and maturation of industrial IoT ecosystems will further strengthen demand for localized computing architectures.

Major Players

- Dell Technologies

- Hewlett Packard Enterprise

- Schneider Electric

- Nokia

- Huawei

- Cisco Systems

- IBM

- Microsoft

- Google Cloud

- Telekom Malaysia

- Maxis

- CelcomDigi

- EdgeConneX

- Equinix

- SkyeChip

Key Target Audience

- Telecom network operators

- Manufacturing conglomerates

- Cloud service providers

- Data center developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Smart city authorities

- Industrial automation companies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including edge infrastructure deployments, telecom 5G rollout, industrial automation adoption, and data center expansion were identified through secondary research and policy analysis. Supply-side metrics such as vendor presence and deployment models were mapped alongside demand-side indicators across telecom, manufacturing, and public sectors to define market boundaries.

Step 2: Market Analysis and Construction

Market size was constructed using triangulation of infrastructure deployment data, vendor revenues attributable to Malaysia, telecom edge investments, and enterprise adoption indicators. Segmentation by product type and end user was developed through mapping of deployment patterns across industries and infrastructure layers to estimate relative market distribution.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary estimates and structural assumptions were validated through consultations with telecom infrastructure specialists, industrial automation integrators, and regional data center experts. Feedback on deployment trends, cost structures, and adoption barriers refined segmentation shares and competitive positioning analysis.

Step 4: Research Synthesis and Final Output

Validated datasets and expert insights were synthesized into a coherent market model integrating infrastructure, industry demand, and policy drivers. Findings were structured into standardized market report sections, ensuring internal consistency across sizing, segmentation, competitive landscape, and forward outlook for Malaysia’s edge computing ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for low-latency applications

Expansion of 5G infrastructure

Increase in IoT deployments across industries - Market Challenges

High initial deployment costs

Integration complexity with legacy systems

Data security and privacy concerns - Market Opportunities

Adoption of AI-driven edge analytics

Expansion in smart manufacturing initiatives

Growth in healthcare edge computing solutions - Trends

Convergence of edge and cloud architectures

Deployment of containerized edge computing solutions

Increase in decentralized data processing models - Government regulations

Data localization mandates

Telecommunications compliance standards

Cybersecurity certification requirements - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge AI Servers

Edge Storage Solutions

Edge Networking Equipment

IoT Gateway Devices

Micro Data Centers - By Platform Type (In Value%)

On-premise Edge Platforms

Cloud-integrated Edge Platforms

Hybrid Edge Platforms

Telecom-integrated Edge Platforms

Enterprise Edge Platforms - By Fitment Type (In Value%)

Standalone Systems

Modular Systems

Scalable Rack Systems

Containerized Systems

Integrated Systems - By EndUser Segment (In Value%)

Telecommunications Providers

Manufacturing & Industrial Automation

Healthcare & Medical Facilities

Retail & E-commerce Chains

Government & Public Sector - By Procurement Channel (In Value%)

Direct Vendor Sales

System Integrators

Cloud Service Providers

Technology Distributors

Government Tenders

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Procurement Channel, Deployment Model, Regional Adoption, Security Compliance, System Complexity, Technology Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Huawei Technologies Malaysia

Dell Technologies Malaysia

Hewlett Packard Enterprise Malaysia

Cisco Systems Malaysia

IBM Malaysia

Nokia Networks Malaysia

Lenovo Malaysia

Schneider Electric Malaysia

Microsoft Azure Edge Malaysia

Amazon Web Services Malaysia

Fujitsu Malaysia

Hitachi Vantara Malaysia

EdgeConneX Malaysia

Vertiv Malaysia

Supermicro Malaysia

- Telecom providers require robust low-latency platforms to support 5G services

- Manufacturers leverage edge analytics for predictive maintenance and operational efficiency

- Healthcare facilities deploy edge solutions for real-time patient monitoring and data processing

- Retail chains integrate edge platforms for personalized customer experiences and inventory management

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now