Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia freight aggregator market reached approximately USD ~ billion based on a recent historical assessment, driven by rapid digitalization of logistics procurement and expansion of e-commerce fulfillment demand across urban corridors. Platform-enabled truck booking, load consolidation, and multimodal routing solutions are increasingly adopted by SMEs and large shippers seeking cost optimization and real-time visibility. Government logistics digitization initiatives and cross-border ASEAN trade growth further accelerate platform penetration, supporting scalable freight aggregation models across domestic and regional supply chains.

Kuala Lumpur and Selangor dominate the Malaysia freight aggregator market due to dense industrial clusters, distribution hubs, and advanced digital infrastructure enabling rapid logistics platform adoption. Penang and Johor also show strong activity driven by manufacturing exports and proximity to international ports and Singapore trade corridors. These regions benefit from established trucking fleets, warehouse ecosystems, and technology-ready shippers, creating favorable conditions for aggregator platforms to scale network density and offer reliable multimodal freight matching services across Malaysia’s logistics backbone.

Market Segmentation

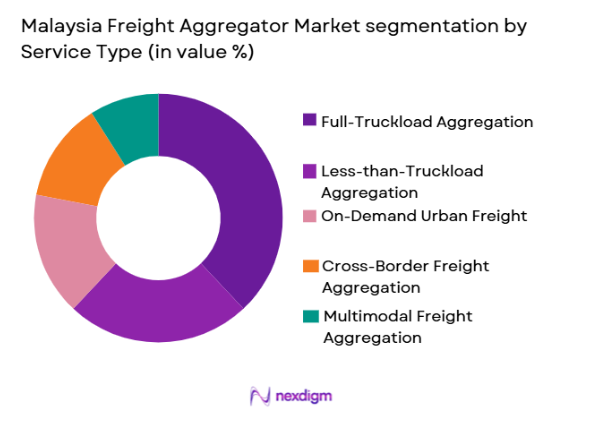

By Service Type

Malaysia freight aggregator market is segmented by Service type into Full-Truckload Aggregation, Less-than-Truckload Aggregation, On-Demand Urban Freight, Cross-Border Freight Aggregation, and Multimodal Freight Aggregation. Recently, Full-Truckload Aggregation has a dominant market share due to factors such as high industrial shipment volumes, consistent manufacturing freight demand, established trucking networks, and platform optimization efficiencies. Large shippers prefer full-truckload aggregation for predictable capacity, route optimization, and cost transparency, while aggregators achieve higher utilization rates and margins compared to fragmented partial loads.

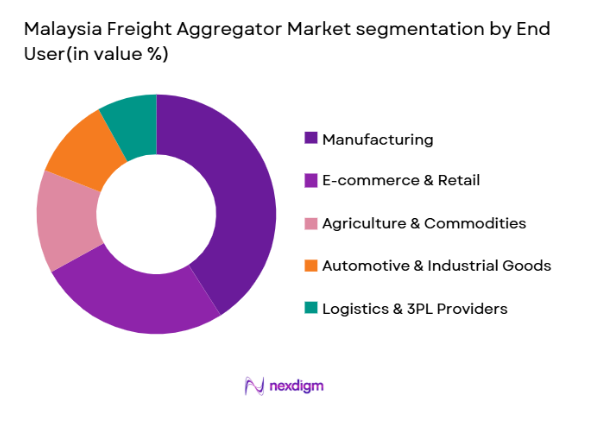

By End-User

Malaysia freight aggregator market is segmented by End-User into Manufacturing, E-commerce & Retail, Agriculture & Commodities, Automotive & Industrial Goods, and Logistics & 3PL Providers. Recently, Manufacturing has a dominant market share due to factors such as continuous outbound freight flows, export-oriented production hubs, predictable shipment volumes, and integration of digital logistics procurement systems. Manufacturers leverage aggregators to secure reliable trucking capacity and optimize freight costs across factory-to-port and inter-plant distribution networks.

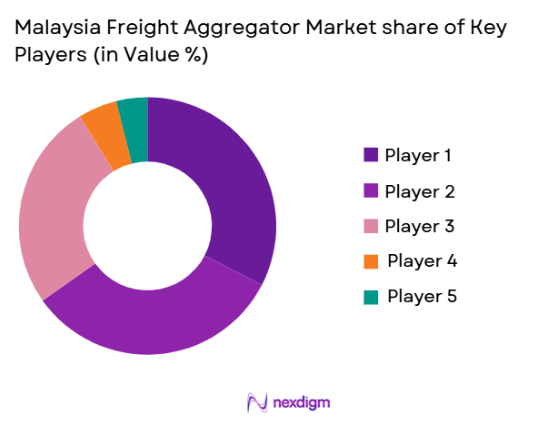

Competitive Landscape

Malaysia freight aggregator market shows moderate consolidation with regional digital logistics platforms expanding through partnerships and carrier onboarding strategies. Leading players differentiate through real-time tracking, pricing algorithms, and cross-border capabilities, while local specialists focus on SME accessibility and domestic trucking networks. Strategic integration with warehousing, fulfillment, and e-commerce ecosystems strengthens platform stickiness and network scale advantages.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Carrier Network Scale |

| Lalamove | 2013 | Hong Kong | ~ | ~ | ~ | ~ | ~ |

| Ninja Van | 2014 | Singapore | ~ | ~ | ~ | ~ | ~ |

| TheLorry | 2014 | Malaysia | ~ | ~ | ~ | ~ | ~ |

| GoGoX | 2013 | Hong Kong | ~ | ~ | ~ | ~ | ~ |

| Deliveree | 2015 | Thailand | ~ | ~ | ~ | ~ | ~ |

Malaysia Freight Aggregator Market Analysis

Growth Drivers

E-commerce Fulfillment Expansion Driving On-Demand Freight Aggregation:

Rapid growth of digital commerce logistics in Malaysia is significantly increasing demand for flexible freight capacity and platform-based truck procurement across urban and regional distribution corridors. Online retail fulfillment models require frequent shipments between warehouses, sorting centers, and last-mile hubs, which aligns strongly with aggregator-enabled trucking marketplaces offering real-time booking and pricing transparency. Logistics platforms reduce idle capacity by matching fragmented loads with available carriers, improving utilization rates and reducing freight costs for e-commerce sellers and marketplaces. The proliferation of same-day and next-day delivery expectations further intensifies demand for responsive freight aggregation solutions capable of dynamic routing and rapid dispatch. Aggregators also enable small online sellers to access enterprise-grade logistics networks without owning fleets, accelerating platform adoption among SMEs. Integration with warehouse management and order management systems strengthens operational efficiency and shipment visibility across fulfillment chains. Regional cross-border e-commerce flows between Malaysia, Singapore, and Thailand additionally create recurring trucking demand across trade corridors. Aggregator platforms therefore become critical infrastructure for scalable e-commerce logistics orchestration across Malaysia’s digital economy.

Logistics Digitalization and SME Adoption of Platform-Based Transport Procurement:

Malaysia logistics sector is undergoing structural digital transformation as shippers transition from manual freight sourcing toward automated platform-based procurement and real-time shipment visibility solutions. Small and medium enterprises, which represent a large share of Malaysia’s shipper base, increasingly rely on aggregators to access competitive trucking rates, verified carriers, and predictable service quality without complex contracts. Digital freight marketplaces reduce transaction friction by enabling instant quotations, route optimization, and electronic documentation, replacing traditional broker-driven freight booking processes. Government initiatives supporting logistics modernization and supply chain digitization further encourage technology adoption across manufacturing, agriculture, and distribution sectors. Aggregators also generate operational data that improves demand forecasting and capacity planning for both shippers and carriers. The ability to compare rates and transit times across multiple carriers enhances procurement transparency and cost control for businesses. As SMEs expand domestic and export operations, scalable digital logistics access becomes essential for competitiveness. This structural shift toward platform-enabled freight procurement sustains long-term growth of Malaysia freight aggregator market.

Market Challenges

Fragmented Trucking Ecosystem Limiting Network Density and Reliability:

Malaysia road freight sector remains highly fragmented with a large proportion of small independent carriers operating limited fleets and varying service standards, creating challenges for aggregator platforms seeking consistent capacity and reliability. Many traditional trucking operators lack digital systems or telematics integration, restricting real-time tracking and automated dispatch capabilities required by freight marketplaces. Aggregators must invest heavily in onboarding, training, and technology enablement of carriers to ensure standardized service levels across networks. Geographic dispersion of fleets across rural and urban regions also reduces route density, affecting platform matching efficiency and utilization optimization. Shippers may experience inconsistent service quality due to variable carrier professionalism and operational maturity. Trust barriers between carriers and digital platforms further slow adoption, particularly among older operators resistant to pricing transparency. Limited standardized documentation and compliance processes complicate cross-border aggregation operations. These structural inefficiencies constrain scalability and operational reliability of freight aggregation networks across Malaysia.

Price Competition and Margin Pressure in Digital Freight Marketplaces:

Malaysia freight aggregator market experiences intense price competition as multiple platforms compete to attract shippers and carriers, often resulting in aggressive discounting and low commission structures. Freight services are highly price-sensitive, with shippers prioritizing cost savings over platform differentiation, limiting ability of aggregators to command premium pricing. Carrier oversupply in certain corridors also compresses freight rates and platform margins. New entrants leveraging venture funding frequently subsidize prices to gain market share, further intensifying competitive pressure. Limited switching costs allow shippers to move between platforms based on short-term pricing advantages. Aggregators must balance carrier incentives with shipper discounts, reducing profitability. Investments in technology, marketing, and carrier onboarding raise operating costs while revenue per shipment remains constrained. As platforms scale, sustaining profitability without raising transaction fees becomes challenging. Persistent margin pressure therefore restricts long-term financial sustainability for some market participants.

Opportunities

Cross-Border ASEAN Freight Corridor Aggregation Expansion:

Malaysia strategic location within Southeast Asian trade routes creates strong opportunity for aggregators to expand cross-border freight orchestration across Singapore, Thailand, and Indonesia corridors. Regional manufacturing supply chains and e-commerce distribution networks increasingly require seamless trucking connectivity between ports, industrial zones, and fulfillment hubs across borders. Aggregator platforms capable of integrating customs documentation, compliance workflows, and cross-border carrier networks can deliver significant efficiency gains for exporters and distributors. Harmonization of ASEAN logistics policies and trade facilitation initiatives further supports digital freight integration across countries. Shippers benefit from unified booking, tracking, and pricing visibility across international routes, reducing reliance on multiple brokers. Cross-border aggregation also increases shipment frequency and network density, improving platform utilization economics. Partnerships with regional logistics operators and customs brokers enable scalable service expansion. As ASEAN intra-regional trade volumes rise, digital aggregation of cross-border freight becomes a major growth avenue for Malaysia platforms.

Integration of Value-Added Logistics Services Within Aggregator Platforms:

Freight aggregators in Malaysia can expand beyond transport matching into integrated logistics ecosystems combining warehousing, fulfillment, insurance, financing, and supply chain analytics services. Shippers increasingly prefer unified logistics solutions that reduce vendor complexity and provide end-to-end visibility from origin to delivery. Aggregator platforms possess transaction data enabling credit scoring and embedded financing offerings for carriers and SMEs. Insurance products covering cargo and transit risks can be seamlessly integrated within booking workflows, enhancing customer trust. Warehousing partnerships enable multimodal and distribution services linked directly to freight procurement. Data analytics modules can optimize routing, demand forecasting, and cost benchmarking for enterprise shippers. These value-added capabilities increase platform stickiness and revenue diversification beyond transport commissions. As logistics outsourcing trends grow among Malaysian businesses, integrated digital logistics ecosystems represent a significant monetization and differentiation opportunity for freight aggregators.

Future Outlook

Malaysia freight aggregator market is expected to expand steadily as logistics digitalization accelerates across manufacturing, retail, and cross-border trade sectors. Adoption of AI-driven route optimization, real-time visibility platforms, and integrated logistics ecosystems will enhance efficiency and scalability. Government logistics modernization policies and ASEAN trade connectivity initiatives will support platform expansion. Rising SME participation in digital freight procurement and e-commerce logistics growth will sustain demand for aggregator-enabled transport networks across Malaysia.

Major Players

- Lalamove

- Ninja Van

- TheLorry

- GoGoX

- Deliveree

- Pickupp

- EasyParcel

- Janio

- Teleport

- J&T Cargo

- Kerry Logistics Network

- CJ Century Logistics

- Tiong Nam Logistics

- FMX

- Zeek Logistics

Key Target Audience

- Logistics and transportation companies

- E-commerce fulfillment operators

- Manufacturing exporters

- Freight forwarding companies

- Supply chain technology providers

- Automotive distribution firms

- Agriculture commodity traders

- Retail distribution networks

Research Methodology

Step 1: Identification of Key Variables

Comprehensive identification of Malaysia freight aggregator market variables including platform adoption rates, freight demand patterns, carrier availability, pricing structures, and logistics digitalization indicators across industries and regions.

Step 2: Market Analysis and Construction

Aggregation of shipment volumes, platform transaction data, logistics sector indicators, and technology adoption metrics to construct market size and segmentation models for Malaysia freight aggregator ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Validation of market assumptions through interviews with logistics operators, platform providers, shippers, and industry specialists to confirm demand drivers, pricing dynamics, and operational trends.

Step 4: Research Synthesis and Final Output

Integration of quantitative and qualitative insights into structured market analysis covering segmentation, competitive landscape, growth drivers, challenges, opportunities, and future outlook for Malaysia freight aggregator market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid ecommerce expansion increasing fragmented freight demand

Digitalization push across Malaysia logistics and SME sectors

Government initiatives promoting logistics technology adoption

Cross-border ASEAN trade growth requiring aggregation efficiency

Rising need for cost optimization in transport procurement - Market Challenges

Fragmented trucking ecosystem with low digital penetration

Price competition reducing aggregator margins

Data integration challenges with legacy shipper systems

Regulatory complexity in cross-border freight aggregation

Trust deficit among traditional carriers toward platforms - Market Opportunities

Expansion into cross-border ASEAN freight aggregation corridors

Integration with warehouse and fulfillment marketplaces

AI-driven dynamic pricing and capacity pooling services - Trends

Shift toward asset-light digital freight brokerage models

Adoption of real-time tracking and visibility platforms

Growth of multimodal aggregation combining road sea air

Platform consolidation through logistics tech partnerships

Embedded finance and freight insurance within platforms - Government Regulations & Defense Policy

Malaysia National Transport Policy digital logistics initiatives

Cross-border trade facilitation under ASEAN frameworks

Data governance and digital commerce regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital Freight Matching Platforms

Load Consolidation Aggregators

On-demand Truck Booking Platforms

Multimodal Freight Aggregators

Cross-border Freight Aggregators - By Platform Type (In Value%)

Web-based Freight Platforms

Mobile Application Platforms

API-integrated Logistics Platforms

Cloud-native Aggregation Platforms

AI-enabled Freight Platforms - By Fitment Type (In Value%)

Standalone Aggregator Platforms

Integrated TMS-linked Platforms

Marketplace-integrated Platforms

ERP-integrated Aggregation Systems

White-label Aggregator Solutions - By EndUser Segment (In Value%)

SME Shippers

Large Manufacturing Enterprises

Ecommerce Retailers

Freight Forwarders and 3PLs

Agriculture and Commodity Traders - By Procurement Channel (In Value%)

Direct Platform Subscription

Enterprise Contracts

Logistics Service Bundling

Marketplace Onboarding

Channel Partner Resellers - By Material / Technology (in Value %)

AI-based Route Optimization Engines

Real-time Telematics Integration

Cloud Computing Infrastructure

Blockchain-enabled Freight Contracts

Predictive Pricing Algorithms - By System Type (In Value%)

Digital Freight Matching Platforms

Load Consolidation Aggregators

On-demand Truck Booking Platforms

Multimodal Freight Aggregators

Cross-border Freight Aggregators - By Platform Type (In Value%)

Web-based Freight Platforms

Mobile Application Platforms

API-integrated Logistics Platforms

Cloud-native Aggregation Platforms

AI-enabled Freight Platforms - By Fitment Type (In Value%)

Standalone Aggregator Platforms

Integrated TMS-linked Platforms

Marketplace-integrated Platforms

ERP-integrated Aggregation Systems

White-label Aggregator Solutions - By EndUser Segment (In Value%)

SME Shippers

Large Manufacturing Enterprises

Ecommerce Retailers

Freight Forwarders and 3PLs

Agriculture and Commodity Traders - By Procurement Channel (In Value%)

Direct Platform Subscription

Enterprise Contracts

Logistics Service Bundling

Marketplace Onboarding

Channel Partner Resellers - By Material / Technology (in Value %)

AI-based Route Optimization Engines

Real-time Telematics Integration

Cloud Computing Infrastructure

Blockchain-enabled Freight Contracts

Predictive Pricing Algorithms

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Platform Capability, Carrier Network Size, Pricing Model Flexibility, Real-time Visibility Features, Multimodal Coverage, Cross-border Capability, Integration Ecosystem, SME Accessibility, AI Optimization Level, Value-added Services)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Lalamove

Ninja Van

EasyParcel

TheLorry

GoGoX

Deliveree

Janio

Pickupp

Teleport

J&T Cargo

Kerry Logistics Network

CJ Century Logistics

Tiong Nam Logistics

FMX

Zeek Logistics

- SMEs increasingly rely on aggregators for cost-efficient spot freight access

- Ecommerce players demand scalable on-demand transport capacity

- Manufacturers seek integrated freight visibility and optimization tools

- 3PLs use aggregators to expand carrier networks without asset investment

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now