Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Malaysia Green Hydrogen market is valued at approximately USD ~ million based on a recent historical assessment, driven by the country’s commitment to reducing carbon emissions and transitioning to renewable energy. Malaysia’s government has set ambitious goals for clean energy adoption, and green hydrogen is seen as a crucial component in decarbonizing sectors like transportation, industry, and energy. The decline in production costs, coupled with the increase in hydrogen infrastructure, is contributing to the growing demand for green hydrogen.

Key regions such as Kuala Lumpur, Penang, and Johor Bahru are central to the growth of the green hydrogen market. Kuala Lumpur, as the economic and political capital, plays a crucial role in driving policies and investments in renewable energy. Penang, with its strong industrial base, is becoming a hub for green hydrogen adoption in manufacturing processes, while Johor Bahru, with its proximity to Singapore, offers significant potential for large-scale hydrogen projects. These cities are key to Malaysia’s green hydrogen development and market expansion.

Market Segmentation

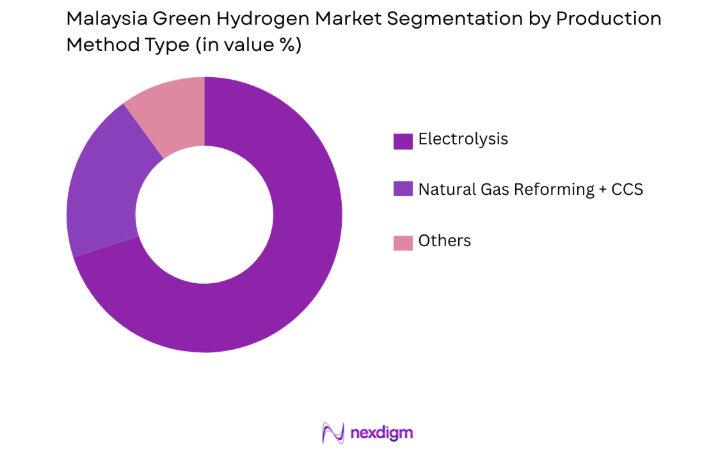

By Production Method

The Malaysia Green Hydrogen market is segmented by production method into electrolysis, natural gas reforming with carbon capture and storage (CCS), and others. Recently, electrolysis has dominated the market share due to its alignment with the country’s clean energy goals. Electrolysis, using renewable energy to split water into hydrogen and oxygen, offers a sustainable and environmentally friendly method of producing hydrogen. With Malaysia’s focus on expanding renewable energy sources like solar and wind, electrolysis is expected to remain the dominant method as it supports the country’s objective of reducing its carbon footprint. The growing availability of renewable energy and advancements in electrolyzer technology continue to drive the market’s preference for electrolysis in green hydrogen production.

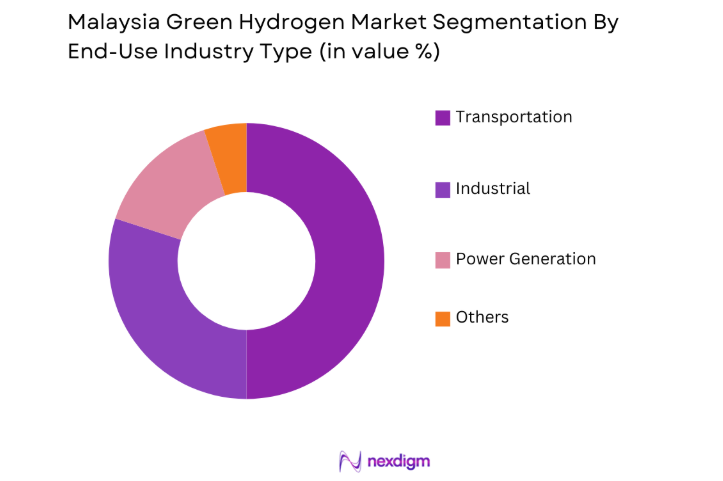

By End-Use Industry

The Malaysia Green Hydrogen market is also segmented by end-use industry into transportation, industrial, power generation, and others. Recently, the transportation sector has led the market share due to the increasing demand for clean energy solutions in the automotive industry. The adoption of green hydrogen fuel cell vehicles (FCVs) is gaining momentum, driven by government incentives and the automotive industry’s commitment to sustainability. Malaysia’s plans to integrate hydrogen into public transportation systems and the rise in hydrogen-powered vehicles are key drivers in this sector. The focus on reducing emissions in the transportation sector is expected to make green hydrogen an attractive alternative fuel for Malaysia’s future mobility landscape.

Competitive Landscape

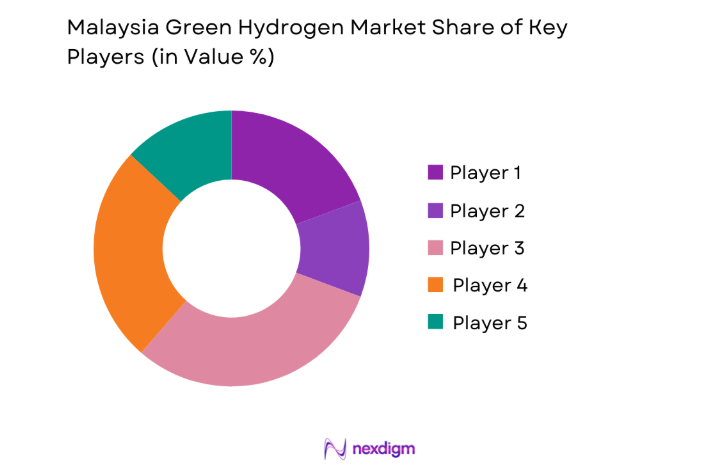

The competitive landscape of the Malaysia Green Hydrogen market is characterized by both international and local players working to develop hydrogen production, storage, and distribution technologies. International players like Air Products and Siemens Energy lead the market with their established global presence and advanced hydrogen technologies. Local companies, such as Petronas and Malakoff Corporation, are increasingly investing in green hydrogen projects as part of their transition towards renewable energy. As the green hydrogen market expands in Malaysia, collaborations between local players and international firms will be vital for accelerating technology adoption and scaling up hydrogen production.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Market-Specific Focus |

| Air Products | 1940 | Allentown, USA | ~ | ~ | ~ | ~ | ~ |

| Siemens Energy | 2020 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| Petronas | 1974 | Kuala Lumpur, Malaysia | ~ | ~ | ~ | ~ | ~ |

| Malakoff Corporation | 1975 | Kuala Lumpur, Malaysia | ~ | ~ | ~ | ~ | ~ |

| Siemens Gamesa | 1976 | Zamudio, Spain | ~ | ~ | ~ | ~ | ~ |

Malaysia Green Hydrogen Market Analysis

Growth Drivers

Government Policy and Renewable Energy Targets

The Malaysia Green Hydrogen market is primarily driven by government policies supporting clean energy and renewable hydrogen initiatives. Malaysia’s commitment to achieving net-zero carbon emissions by 2050 has led to the creation of policies that favor the development and adoption of green hydrogen technologies. Key initiatives, including subsidies for hydrogen production, incentives for companies investing in hydrogen infrastructure, and regulations favoring clean energy adoption, are expected to drive long-term growth in the market. Malaysia’s Renewable Energy Transition Plan, which includes a roadmap for hydrogen adoption, provides a clear regulatory framework, making green hydrogen a priority area for the government. As the nation invests in sustainable energy solutions, green hydrogen will play a critical role in decarbonizing sectors such as transportation and industrial manufacturing, further driving demand.

Technological Advancements in Hydrogen Production

The rapid advancements in hydrogen production technologies, particularly electrolysis, are a major growth driver for the Malaysia Green Hydrogen market. Innovations in electrolyzer technology have made green hydrogen production more cost-effective and scalable. As the cost of renewable energy generation decreases, hydrogen production via electrolysis becomes increasingly viable. Furthermore, improvements in hydrogen storage and transportation technologies are overcoming logistical barriers, making green hydrogen a more feasible solution for industries across Malaysia. The continued technological development in hydrogen-related infrastructure, such as fuel cell systems and hydrogen refueling stations, will further facilitate the growth of green hydrogen applications in transportation and industry.

Market Challenges

High Production Costs and Infrastructure Development

One of the key challenges facing the Malaysia Green Hydrogen market is the high production costs associated with hydrogen generation, particularly via electrolysis. The equipment required for electrolysis, such as electrolyzers and renewable energy systems, represents a significant upfront investment, which can deter potential investors and slow the widespread adoption of green hydrogen. Furthermore, the infrastructure required to store, transport, and distribute hydrogen remains underdeveloped in Malaysia, adding additional costs. The lack of sufficient hydrogen refueling stations and transportation infrastructure limits the ability of hydrogen-powered vehicles to operate on a large scale, restricting the growth of the market. To overcome these challenges, the government will need to continue supporting the development of hydrogen infrastructure and incentivize investments in production technologies.

Lack of Market Awareness and Skilled Workforce

Another challenge facing the Malaysia Green Hydrogen market is the lack of awareness and understanding of hydrogen technology among both industry players and consumers. Many industries are still in the early stages of exploring green hydrogen solutions, and there is limited knowledge regarding the potential benefits and cost savings. Additionally, the green hydrogen sector requires a specialized workforce with expertise in hydrogen production, storage, and distribution technologies. The shortage of skilled labor in these areas could limit the growth of the industry, as companies may struggle to find qualified workers to implement and maintain green hydrogen technologies. Addressing this issue will require investment in education and training programs to build a skilled workforce capable of supporting the green hydrogen sector.

Opportunities

Expansion of Hydrogen-Fueled Transportation

The growing demand for clean and sustainable transportation presents a significant opportunity for the Malaysia Green Hydrogen market. Hydrogen fuel cell vehicles (FCVs) are gaining attention as a potential solution to reduce emissions in the transportation sector, particularly in heavy-duty and long-range applications where battery-electric vehicles face limitations. Malaysia’s government has identified hydrogen as a key component of its clean energy transition, and policies are in place to support the development of hydrogen-powered transportation. As Malaysia seeks to reduce its reliance on fossil fuels and meet global environmental standards, hydrogen fuel cell vehicles could become a key part of the national fleet, driving the demand for green hydrogen in the transportation sector.

Hydrogen as a Clean Energy Solution for Industry

The adoption of green hydrogen in industrial processes offers significant opportunities for decarbonizing sectors such as manufacturing, chemicals, and steel production. Industries in Malaysia, which are major contributors to carbon emissions, can benefit from switching to hydrogen as a clean energy source. For example, green hydrogen can replace natural gas in industrial heating and act as a feedstock in chemical production, reducing overall emissions. The growing global emphasis on sustainability and the demand for low-carbon products will encourage industries to adopt green hydrogen technologies. As Malaysia continues to pursue its decarbonization targets, hydrogen offers an opportunity for industries to transition to cleaner processes while maintaining productivity.

Future Outlook

The Malaysia Green Hydrogen market is expected to grow significantly over the next five years, driven by the country’s renewable energy ambitions and the continued development of hydrogen production technologies. Government policies supporting green hydrogen production, along with technological advancements in electrolysis and hydrogen storage, will play a crucial role in expanding the market. The increasing demand for clean energy solutions in transportation and industrial applications will further boost the adoption of green hydrogen, positioning Malaysia as a key player in the regional hydrogen economy.

Major Players

- Siemens Gamesa

- Vestas

- Air Products

- Petronas

- Siemens Energy

- Malakoff Corporation

- Hydrogenics

- Linde

- Shell

- BP Alternative Energy

- Enel Green Power

- Mitsubishi Heavy Industries

- First Solar

- SunPower

- Acciona Energy

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hydrogen fuel cell vehicle manufacturers

- Industrial energy consumers

- Renewable energy solution providers

- Energy storage companies

- Hydrogen infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Identify the key drivers, barriers, and trends that impact the Malaysia Green Hydrogen market, including government policies, technological advancements, and market demand.

Step 2: Market Analysis and Construction

Analyze market data, trends, and forecasts to construct a model that reflects the current and projected state of the green hydrogen market in Malaysia.

Step 3: Hypothesis Validation and Expert Consultation

Consult with industry experts, stakeholders, and policymakers to validate assumptions and ensure the accuracy of research findings.

Step 4: Research Synthesis and Final Output

Synthesize the research into a comprehensive report that includes actionable insights, strategic recommendations, and market forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government policies and subsidies

Technological advancements in hydrogen production

Increasing demand for clean energy solutions - Market Challenges

High capital expenditure for hydrogen infrastructure

Limited hydrogen distribution networks

Technological barriers to scalability - Market Opportunities

Expansion of hydrogen infrastructure

Partnerships with international energy firms

Growth in industrial demand for hydrogen - Trends

Development of hydrogen refueling stations

Advancements in hydrogen fuel cell vehicles - Government Regulations

National hydrogen strategies and targets

Carbon emission reduction policies

Hydrogen safety and certification standards - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electrolyzers

Fuel Cells

Storage Solutions

Hydrogen Production Systems

Distribution Systems - By Platform Type (In Value%)

Onshore Platforms

Offshore Platforms

Hybrid Platforms

Mobile Platforms - By Fitment Type (In Value%)

On-site Hydrogen Production

Centralized Hydrogen Production

Decentralized Hydrogen Production

Modular Hydrogen Solutions - By End User Segment (In Value%)

Industrial Applications

Transportation

Residential

- Market Share Analysis

- Cross Comparison Parameters (Technology, Cost of Production, Market Penetration, Regulatory Support, Government Incentives, Storage Capacity, Distribution Infrastructure)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Air Products and Chemicals, Inc.

Nel ASA

ITM Power

Siemens Energy

Linde Group

Shell

McPhy Energy

Plug Power

Ballard Power Systems

Ceres Power

Hydrogenics Corporation

Toyota Industries Corporation

BASF SE

Siemens Gamesa

Envision Energy

- Increasing demand for hydrogen in industrial applications

- Government initiatives for hydrogen-powered transportation

- Residential sector adoption of hydrogen energy solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now