Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia home finance market recorded approximately USD ~ billion in outstanding residential mortgage financing based on Bank Negara Malaysia banking system housing loan statistics and financial stability disclosures. The market is driven by sustained urban housing demand, supportive banking liquidity, and strong Islamic mortgage penetration across households. Government housing schemes and developer-linked financing structures continue expanding borrower accessibility. Stable property transaction volumes across primary and secondary markets further reinforce financing growth across commercial banks and Islamic financial institutions.

Within Malaysia, Kuala Lumpur and Selangor dominate home finance activity due to high property transaction density, concentration of banking headquarters, and large urban population bases requiring mortgage financing. Penang and Johor also demonstrate strong financing demand supported by industrial employment centers and cross-border property investment flows. These regions attract developers launching high-value residential projects aligned with urban migration trends. Mature banking infrastructure and digital mortgage origination capabilities in these urban corridors sustain their dominance in national home financing activity.

Market Segmentation

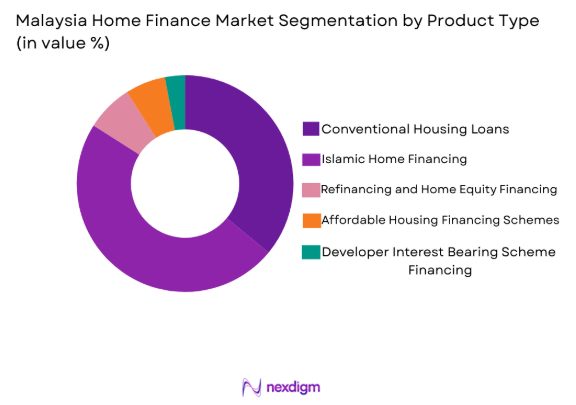

By Product Type

Malaysia home finance market is segmented by product type into conventional housing loans, Islamic home financing, refinancing and home equity financing, affordable housing financing schemes, and developer interest bearing scheme financing. Recently, Islamic home financing has a dominant market share due to factors such as strong Sharia compliance preference among majority Muslim borrowers, extensive Islamic bank participation, and regulatory support for Islamic mortgage structures. Competitive profit rates, flexible Musharakah Mutanaqisah contracts, and nationwide Islamic banking infrastructure further strengthen adoption.

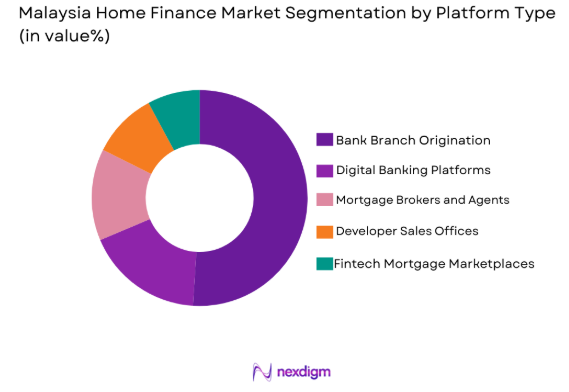

By Platform Type

Malaysia home finance market is segmented by platform type into bank branch origination, digital banking platforms, mortgage brokers and agents, developer sales offices, and fintech mortgage marketplaces. Recently, bank branch origination has a dominant market share due to factors such as borrower preference for advisory-based mortgage structuring, documentation verification requirements, and relationship banking practices in large-ticket housing loans. Major banks maintain extensive nationwide branch networks enabling credit assessment and property valuation coordination. High-value transactions and regulatory compliance processes continue reinforcing branch-led origination dominance.

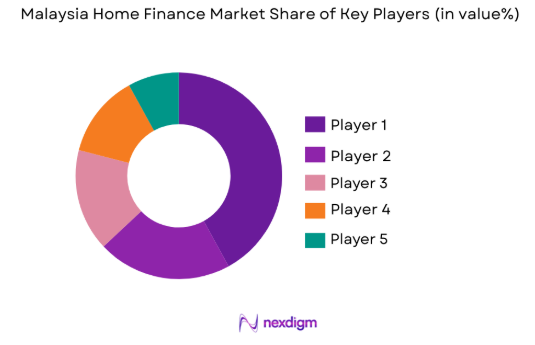

Competitive Landscape

Malaysia home finance market exhibits moderate consolidation dominated by large domestic banks and Islamic financial institutions holding substantial mortgage portfolios and nationwide distribution networks. Leading banks leverage scale advantages in funding cost, Sharia-compliant product depth, and digital origination platforms to sustain competitive positioning. Foreign banks maintain niche presence in premium urban segments, while government-linked institutions support affordable housing financing expansion.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Islamic Finance Capability |

| Malayan Banking Berhad | 1960 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| CIMB Group Holdings Berhad | 1924 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Public Bank Berhad | 1966 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| RHB Bank Berhad | 1913 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Bank Islam Malaysia Berhad | 1983 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

Malaysia Home Finance Market Analysis

Growth Drivers

Household Debt Saturation Limiting Borrower Eligibility Expansion

Household debt saturation limiting borrower eligibility expansion constrains Malaysia home finance market growth by reducing the pool of financially qualified borrowers able to meet banking sector debt-service ratio requirements and prudential lending standards. Malaysia exhibits relatively high household debt levels compared with regional peers due to long-standing consumer credit penetration across mortgages, auto loans, and personal financing facilities embedded in household balance sheets. Banks maintain conservative loan-to-income and debt-service thresholds to preserve asset quality and financial stability, restricting incremental mortgage approvals among leveraged households. Rising living costs in urban centers compress disposable income, reducing affordability margins for mortgage repayment commitments across middle-income borrowers. Younger households entering the housing market often carry education or consumer debt obligations that weaken credit profiles during mortgage assessment. Property price escalation in major cities increases required loan quantum, intensifying debt burden relative to income levels and triggering regulatory affordability constraints. Lenders face portfolio risk concentration concerns in housing finance segments when borrower leverage ratios increase, prompting tighter underwriting filters. Islamic mortgage structures also require similar affordability assessments, preventing alternative financing pathways for highly leveraged borrowers. Financial regulators emphasize macroprudential safeguards in mortgage lending to avoid systemic risk buildup, sustaining structural limitations on borrower expansion despite housing demand.

Property Price Escalation in Urban Centers Outpacing Income Growth

Property price escalation in urban centers outpacing income growth challenges Malaysia home finance market sustainability by widening affordability gaps between residential property values and household earning capacity across metropolitan regions. Land scarcity and development cost inflation in Kuala Lumpur, Selangor, and Penang have driven sustained residential price increases across primary and secondary markets. Wage growth across middle-income households has not matched housing price appreciation, increasing reliance on higher loan-to-value financing structures and longer mortgage tenures. Borrowers increasingly allocate larger income shares toward mortgage servicing, reducing financial flexibility and increasing credit risk sensitivity to interest rate movements. Developers focus on higher-margin urban projects targeting upper-income segments, limiting supply of affordable housing aligned with median income levels. Affordable housing initiatives partially offset supply imbalance but remain constrained relative to urban demand scale. Banks face elevated collateral valuation risks when property prices outpace underlying income fundamentals, affecting lending prudence. Rising down payment requirements in high-value urban properties further exclude first-time buyers from mortgage eligibility. Persistent affordability pressure suppresses transaction volumes in mid-market housing segments, directly moderating mortgage origination growth potential across urban Malaysia.

Expansion of Affordable Housing Financing Ecosystems through Public–Private Partnerships

Expansion of affordable housing financing ecosystems through public–private partnerships presents significant opportunity for Malaysia home finance market by broadening borrower inclusion across lower- and middle-income households traditionally underserved by commercial mortgage products. Government-led housing programs such as PR1MA and Rumah Selangorku create structured pipelines of price-controlled residential units requiring specialized financing models aligned with beneficiary income profiles. Banks and Islamic financial institutions collaborate with developers and housing agencies to design tailored mortgage products featuring subsidized profit rates, extended tenures, and flexible down payment structures improving affordability thresholds. Credit guarantee mechanisms and risk-sharing frameworks under public programs reduce lender exposure, enabling expansion of financing access to households with moderate credit capacity. Integration of housing allocation platforms with participating bank mortgage systems streamlines borrower identification and approval processes. Affordable housing pipelines stabilize mortgage demand across economic cycles by anchoring financing activity in policy-driven housing supply rather than purely market-priced developments. Islamic finance compatibility with social housing objectives further accelerates adoption among eligible populations. Digital application channels dedicated to government housing schemes enhance accessibility across semi-urban and lower-income segments. Scaling such ecosystems across states can structurally expand Malaysia’s mortgage penetration while supporting national homeownership objectives.

Digital End-to-End Mortgage Origination and Property Transaction Integration

Digital end-to-end mortgage origination and property transaction integration creates substantial opportunity for Malaysia home finance market by reducing processing time, operational cost, and borrower friction across housing loan acquisition journeys. Banks are increasingly deploying automated credit scoring, e-KYC verification, and digital documentation workflows enabling remote mortgage applications without branch dependency. Integration between property listing platforms, valuation databases, and bank underwriting systems allows real-time financing pre-approval linked to property selection, accelerating purchase decisions. Younger digital-native borrowers demonstrate strong preference for online mortgage comparison and application channels, expanding addressable market reach. Fintech mortgage marketplaces aggregate lender offers improving transparency and competition, stimulating borrower engagement. Digital processing reduces turnaround time from application to disbursement, enhancing customer experience and conversion rates. Cost efficiencies enable lenders to target smaller-ticket and affordable housing segments previously constrained by manual processing economics. Government digital identity and land registry modernization further enable seamless electronic mortgage registration and collateral verification. Fully digital mortgage ecosystems can expand Malaysia’s housing finance penetration while strengthening operational scalability for banks and Islamic financial institutions.

Future Outlook

Malaysia home finance market is expected to sustain stable expansion driven by urban housing demand, Islamic mortgage innovation, and digital lending transformation across banking institutions. Government affordable housing programs and regulatory support for Sharia-compliant financing will continue broadening borrower inclusion. Metropolitan property development pipelines and infrastructure projects will reinforce mortgage origination volumes. Advancing digital mortgage ecosystems and integrated property platforms will enhance accessibility, efficiency, and competitive differentiation across lenders.

Major Players

- Malayan Banking Berhad

- CIMB Group Holdings Berhad

- Public Bank Berhad

- RHB Bank Berhad

- Hong Leong Bank Berhad

- AmBank Group

- Bank Islam Malaysia Berhad

- Bank Rakyat

- Alliance Bank Malaysia Berhad

- AffinBank Berhad

- HSBC Bank Malaysia Berhad

- OCBC Bank Malaysia Berhad

- Standard Chartered Bank Malaysia Berhad

- UOB Malaysia

- MBSB Bank Berhad

Key Target Audience

- Commercial banks

- Islamic financial institutions

- Mortgage lenders

- Real estate developers

- Housing finance agencies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Property investment firms

Research Methodology

Step 1: Identification of Key Variables

Malaysia home finance market variables including mortgage portfolios, housing supply, borrower demographics, and regulatory frameworks were identified through banking statistics, housing authority data, and financial disclosures. Demand drivers and risk factors were mapped across lending institutions and housing segments.

Step 2: Market Analysis and Construction

Residential mortgage financing volumes, lender portfolios, and housing transaction ecosystems were analyzed across regions and institutions. Market segmentation and competitive structure were constructed using financial reports, central bank statistics, and property market databases.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with banking professionals, housing finance specialists, and property market experts. Regulatory interpretations and lending practices were cross-verified against policy frameworks and institutional disclosures.

Step 4: Research Synthesis and Final Output

All validated data and insights were synthesized into structured market analysis covering size, segmentation, competition, and outlook. Outputs were standardized to ensure consistency with financial market research and housing finance reporting conventions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Urbanization and rising household formation increasing housing demand

Government affordable housing initiatives expanding financing access

Growth of Islamic finance strengthening Sharia compliant mortgages

Digital mortgage platforms improving loan accessibility and approval speed

Stable banking sector liquidity supporting long tenor housing loans - Market Challenges

Rising property prices reducing affordability for middle income households

High household debt levels constraining borrower eligibility

Interest rate volatility affecting mortgage repayment capacity

Lengthy property approval and land regulation processes

Limited financing access for informal income borrowers - Market Opportunities

Expansion of affordable housing financing programs and subsidies

Digital mortgage ecosystems integrating property search and financing

Green home financing and energy efficient housing incentives - Trends

Shift toward Islamic home financing structures among borrowers

End to end digital mortgage origination and approval journeys

Integration of property marketplaces with bank financing offers

Flexible repayment and refinancing options gaining popularity

Increased focus on affordable housing loan products - Government Regulations & Defense Policy

Bank Negara Malaysia housing loan eligibility and lending guidelines

National Affordable Housing Policy and PR1MA schemes

Stamp duty exemptions and home ownership campaigns

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Conventional Housing Loans

Islamic Home Financing

Refinancing and Home Equity Financing

Affordable Housing Financing Schemes

Developer Interest Bearing Scheme Financing - By Platform Type (In Value%)

Bank Branch Origination

Digital Banking Platforms

Mortgage Brokers and Agents

Developer Sales Offices

Fintech Mortgage Marketplaces - By Fitment Type (In Value%)

Owner Occupied Residential Financing

Investment Property Financing

Subsale Property Financing

New Launch Property Financing

Rural and Landed Property Financing - By EndUser Segment (In Value%)

First Time Homebuyers

Upgraders and Existing Homeowners

Property Investors

Affordable Housing Beneficiaries

Non Resident Malaysian Buyers - By Procurement Channel (In Value%)

Direct Bank Lending

Government Housing Programs

Developer Linked Financing

Islamic Financial Institutions

Non Bank Mortgage Providers - By Material / Technology (in Value %)

Sharia Compliant Financing Structures

Automated Credit Scoring Systems

Digital Mortgage Processing Platforms

Property Valuation Analytics Tools

E KYC and Digital Documentation Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Loan Type Portfolio, Islamic Finance Capability, Digital Origination, Interest Rate Competitiveness, Government Scheme Participation)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Malayan Banking Berhad

CIMB Group Holdings Berhad

Public Bank Berhad

RHB Bank Berhad

Hong Leong Bank Berhad

AmBank Group

Bank Islam Malaysia Berhad

Bank Rakyat

Alliance Bank Malaysia Berhad

Affin Bank Berhad

HSBC Bank Malaysia Berhad

OCBC Bank Malaysia Berhad

Standard Chartered Bank Malaysia Berhad

UOB Malaysia

MBSB Bank Berhad

- First time buyers driving demand for affordable and subsidized mortgages

- Urban middle income households seeking upgrading and refinancing loans

- Investors focusing on rental yield properties in major cities

- Government supported buyers accessing social housing finance

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now