Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia’s last-mile delivery market forms a critical component of the country’s logistics and e-commerce ecosystem, with the sector valued at approximately USD ~ billion based on a recent historical assessment derived from logistics industry trade statistics and transportation service revenue data published by the Malaysian Communications and Multimedia Commission and regional logistics associations. Market expansion is primarily driven by strong e-commerce penetration, rapid urban consumer demand for fast parcel delivery, increasing digital retail platforms, and the development of integrated courier networks supporting nationwide distribution systems.

Major logistics activity is concentrated in Kuala Lumpur, Selangor, Penang, and Johor due to their large urban consumer populations, dense retail infrastructure, and strong connectivity with airport cargo terminals and distribution hubs. Kuala Lumpur functions as the primary parcel distribution center supported by advanced courier sorting facilities and e-commerce fulfillment warehouses, while Johor and Penang serve as regional logistics gateways facilitating cross-border trade flows and high parcel delivery volumes across Malaysia’s urban logistics corridors.

Market Segmentation

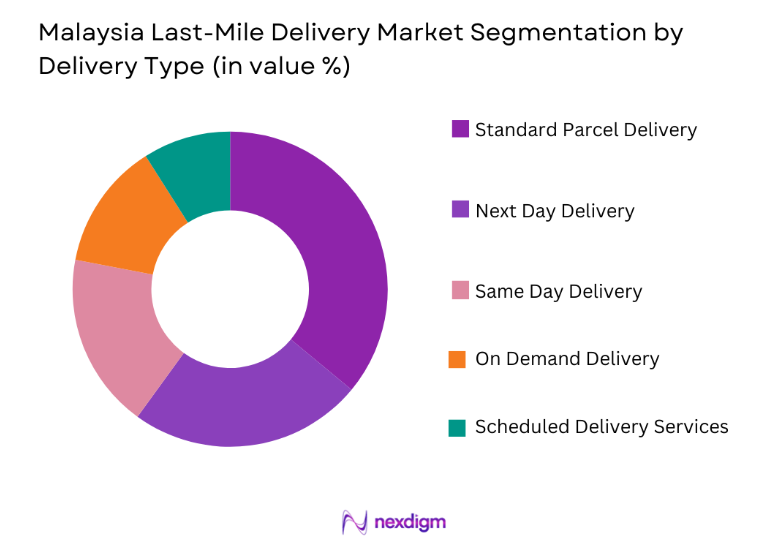

By Delivery Type

Malaysia Last-Mile Delivery market is segmented by Delivery Type into standard parcel delivery, same day delivery, next day delivery, on demand delivery, and scheduled delivery services. Recently, standard parcel delivery has a dominant market share due to factors such as high e-commerce order volumes, cost efficiency for retailers, and the widespread availability of courier distribution networks across Malaysia’s urban logistics infrastructure. Online retailers and marketplace platforms typically rely on standard delivery services for nationwide order fulfillment because the service balances affordability with delivery speed. Courier providers operate large scale sorting centers and regional delivery hubs that enable efficient parcel consolidation before dispatch to urban distribution routes. The growth of small online businesses and social commerce platforms has also increased reliance on cost effective standard parcel delivery systems across the national logistics network.

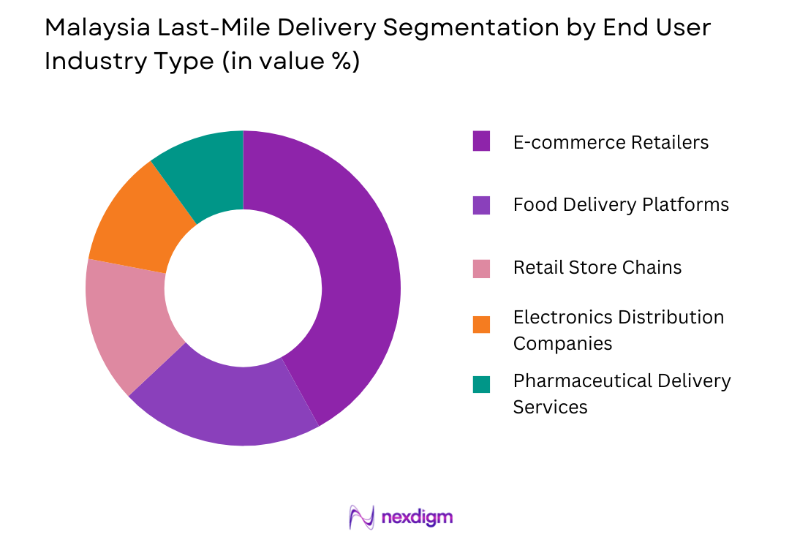

By End User Industry

Malaysia Last-Mile Delivery market is segmented by End User Industry into e-commerce retailers, food delivery platforms, retail store chains, pharmaceutical delivery services, and electronics distribution companies. Recently, e-commerce retailers have a dominant market share due to factors such as increasing digital shopping adoption, widespread smartphone usage, and the expansion of online marketplace platforms across Malaysia’s consumer economy. Major online retailers and marketplace platforms rely heavily on courier logistics providers to manage parcel deliveries across densely populated cities and suburban areas. The growth of direct-to-consumer retail brands and independent online merchants further increases parcel shipment volumes. Courier companies therefore invest in automated sorting hubs and digital parcel tracking systems to manage growing order fulfillment demand from Malaysia’s rapidly expanding e-commerce sector.

Competitive Landscape

The Malaysia last-mile delivery market is characterized by a competitive ecosystem involving international courier providers, domestic logistics companies, and digital delivery platforms competing to expand parcel distribution networks across urban centers. Large courier companies dominate nationwide parcel delivery services due to their established logistics infrastructure and advanced digital tracking platforms. Domestic logistics firms focus on regional delivery networks and specialized e-commerce fulfillment operations. Increasing parcel volumes generated by online retail platforms continue to encourage investment in automated sorting facilities, digital logistics systems, and integrated delivery management technologies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet Size |

| DHL eCommerce | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Pos Malaysia | 1800s | Malaysia | ~ | ~ | ~ | ~ | ~ |

| J&T Express | 2015 | Indonesia | ~ | ~ | ~ | ~ | ~ |

| Ninja Van | 2014 | Singapore | ~ | ~ | ~ | ~ | ~ |

| FedEx Logistics | 1971 | United States | ~ | ~ | ~ | ~ | ~ |

Malaysia Last-Mile Delivery Market Analysis

Growth Drivers

Rapid Expansion of E-commerce Platforms and Digital Retail Marketplaces

Malaysia’s rapidly expanding e-commerce ecosystem significantly drives demand for last-mile delivery services because online retailers require efficient parcel distribution systems capable of reaching consumers across multiple cities and suburban regions. Digital marketplaces such as Lazada Shopee and other regional online retail platforms generate high parcel volumes that must be delivered directly to residential addresses within short delivery timeframes. Consumers increasingly rely on online shopping platforms for purchasing clothing electronics groceries and household products which increases daily parcel shipment volumes handled by courier logistics companies. Last-mile delivery providers therefore invest heavily in automated sorting facilities digital tracking platforms and route optimization software to manage rising delivery demand across urban logistics networks. The expansion of direct to consumer retail brands further increases parcel delivery requirements because businesses rely on courier networks rather than physical retail stores to reach customers. Social commerce platforms and mobile shopping applications also contribute to growing parcel delivery volumes across Malaysia’s digital consumer economy. Courier companies continuously expand delivery fleets and regional distribution hubs to improve delivery efficiency across densely populated cities. These structural changes in Malaysia’s retail environment strongly accelerate the growth of the last-mile delivery market.

Urban Population Density and Rapid Growth of On Demand Delivery Services

Malaysia’s urban population density and growing consumer preference for rapid delivery services significantly accelerate the development of last-mile delivery logistics networks across major metropolitan areas. Cities such as Kuala Lumpur and Penang generate large volumes of parcel deliveries due to concentrated residential communities and active digital commerce participation. Consumers increasingly expect same day or next day parcel deliveries which encourages logistics providers to expand urban micro fulfillment centers located close to consumer markets. Food delivery platforms grocery delivery services and instant retail logistics providers rely heavily on last-mile delivery networks to deliver products within short time windows. Logistics companies therefore deploy route optimization technologies digital delivery management platforms and real time parcel tracking systems to improve operational efficiency. Increasing smartphone penetration and digital payment adoption further strengthen consumer engagement with app based delivery platforms. Courier companies continuously recruit delivery riders and drivers to meet increasing delivery demand across urban logistics corridors. These developments collectively strengthen last-mile logistics infrastructure supporting Malaysia’s fast evolving consumer delivery ecosystem.

Market Challenges

Traffic Congestion and Urban Logistics Infrastructure Constraints

Urban traffic congestion and limited road infrastructure in major Malaysian cities create operational challenges for last-mile delivery companies attempting to maintain efficient parcel distribution networks. High vehicle density in metropolitan areas often slows courier vehicles and delivery motorcycles during peak traffic hours which reduces delivery efficiency and increases delivery time variability. Logistics providers must carefully design delivery routes to minimize delays caused by congestion around commercial districts and residential neighborhoods. Limited parking space for delivery vehicles in densely populated urban areas also complicates parcel distribution operations particularly in high rise residential zones and shopping districts. Delivery companies sometimes require additional manpower to manage deliveries in areas where vehicles cannot easily access residential buildings. These infrastructure limitations increase operational costs because courier companies must allocate additional resources and time to complete deliveries. Rapid growth in parcel delivery volumes further intensifies congestion around distribution centers and commercial delivery zones. Addressing these challenges requires improved urban logistics planning and collaboration between logistics providers and municipal authorities.

Rising Operational Costs and Workforce Management Challenges

The Malaysia last-mile delivery market faces increasing operational cost pressures related to labor wages fuel prices vehicle maintenance and technology investments required to manage complex parcel distribution networks. Courier companies must maintain large fleets of delivery vehicles motorcycles and vans capable of serving multiple delivery routes across urban and suburban regions. Recruiting and retaining delivery drivers and riders also presents challenges because logistics companies compete for labor within a growing gig economy workforce. Rising fuel prices increase transportation costs which directly affect courier service profitability particularly for companies operating high frequency urban delivery routes. Investment in digital logistics systems automated sorting facilities and parcel tracking technologies further increases capital expenditure requirements for logistics providers. Smaller courier companies often struggle to maintain competitive delivery pricing while absorbing operational cost increases. These financial pressures may lead to industry consolidation as larger logistics providers acquire smaller regional delivery operators to expand operational efficiency and maintain service quality.

Opportunities

Expansion of Micro Fulfillment Centers and Smart Logistics Infrastructure

The development of micro fulfillment centers located close to urban residential areas presents a major opportunity for improving last-mile delivery efficiency across Malaysia’s logistics ecosystem. Micro fulfillment centers enable logistics companies to store high demand products closer to consumers allowing faster order processing and shorter delivery routes. E-commerce retailers increasingly collaborate with logistics providers to establish urban distribution hubs that reduce parcel delivery distances and improve service speed. Advanced warehouse automation technologies such as robotic sorting systems and artificial intelligence driven inventory management platforms also improve order fulfillment efficiency. The integration of real time logistics data platforms allows delivery companies to monitor parcel flows and optimize delivery scheduling across urban networks. Investment in smart logistics infrastructure can significantly improve delivery efficiency while reducing operational costs. As Malaysia’s digital commerce sector continues expanding the development of advanced urban logistics facilities will become increasingly important for supporting rapid parcel distribution systems.

Growth of Cross Border E-commerce and Regional Logistics Integration

Malaysia’s strategic geographic location within Southeast Asia creates strong opportunities for last-mile delivery companies to support cross border e-commerce trade flows between neighboring countries. Regional digital marketplaces increasingly enable Malaysian consumers to purchase products from international sellers located across Asia and global markets. Cross border e-commerce transactions require integrated logistics networks capable of handling customs clearance international transportation and domestic parcel delivery operations. Logistics companies are therefore investing in cross border parcel distribution centers located near airports and seaports to manage international shipments entering the country. Courier providers also collaborate with international logistics partners to streamline cross border parcel tracking and delivery coordination systems. As regional trade agreements and digital commerce platforms expand international retail transactions the demand for integrated cross border delivery services will increase significantly. Last-mile delivery companies capable of integrating international logistics operations with domestic parcel distribution networks will benefit from growing cross border e-commerce activity.

Future Outlook

Malaysia’s last-mile delivery market is expected to expand steadily as digital commerce adoption continues to rise and logistics infrastructure evolves to support faster parcel distribution. Investment in automated sorting hubs smart delivery technologies and urban fulfillment centers will significantly improve delivery efficiency. Government policies supporting digital economy development and logistics infrastructure modernization will also strengthen market growth. Increasing consumer demand for rapid delivery services and cross border e-commerce integration will continue shaping the long term expansion of Malaysia’s last-mile logistics ecosystem.

Major Players

- DHL eCommerce

- Pos Malaysia

- J&T Express

- Ninja Van

- FedEx Logistics

- UPS

- Aramex

- SF Express

- GD Express Malaysia

- City-Link Express

- Lalamove

- GrabExpress

- Flash Express

- Kerry Express

- Skynet Worldwide Express

Key Target Audience

- E-commerce retail platforms

- Logistics and courier service companies

- Retail and consumer goods companies

- Food delivery platform operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Transportation infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key variables including parcel delivery volumes e-commerce shipment demand courier network capacity logistics infrastructure development and consumer delivery preferences were identified using logistics industry databases government trade statistics and courier service reports.

Step 2: Market Analysis and Construction

The market structure was constructed through analysis of courier service revenues parcel shipment volumes urban delivery network capacity and the operational scale of major logistics companies operating across Malaysia.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions and preliminary findings were validated through interviews with logistics managers courier network operators e-commerce fulfillment specialists and transportation infrastructure experts operating in Malaysia’s logistics sector.

Step 4: Research Synthesis and Final Output

Validated market data logistics infrastructure insights and operational trends were integrated to develop the final market assessment including segmentation competitive landscape and strategic growth outlook for the Malaysia last-mile delivery market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E Commerce and Online Retail Platforms

Increasing Urban Consumer Demand for Fast Delivery Services

Growth of Digital Payment Systems and Mobile Commerce - Market Challenges

Urban Traffic Congestion Affecting Delivery Efficiency

High Operational Costs in Urban Delivery Networks

Delivery Workforce Management and Labor Shortages - Market Opportunities

Expansion of Same Day and Instant Delivery Services

Adoption of Smart Delivery Technologies and Route Optimization

Growth of Cross Border E Commerce Deliveries - Trends

Adoption of Electric Vehicles for Urban Delivery Fleets

Integration of AI Based Route Optimization and Delivery Tracking - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Standard Parcel Delivery Services

Same Day Delivery Services

Express Delivery Services

Scheduled Delivery Services

On Demand Delivery Services - By Platform Type (In Value%)

E Commerce Delivery Platforms

Retail Distribution Delivery Platforms

Food Delivery Platforms

Courier and Express Logistics Platforms - By Fitment Type (In Value%)

In House Logistics Operations

Third Party Logistics Providers

Crowdsourced Delivery Networks

Hybrid Logistics Delivery Models - By End User Segment (In Value%)

E Commerce Retailers

Food and Grocery Delivery Platforms

Pharmaceutical and Healthcare Product Distributors

- Market Share Analysis

- Cross Comparison Parameters (Delivery Network Coverage, Fleet Size, Delivery Speed Capability, Technology Platform Integration, Last Mile Delivery Cost Efficiency, Warehouse and Fulfillment Infrastructure, Strategic E Commerce Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Pos Malaysia

DHL eCommerce Malaysia

Ninja Van Malaysia

J&T Express Malaysia

City Link Express

GD Express Malaysia

Aramex Malaysia

FedEx Malaysia

UPS Malaysia

Lalamove Malaysia

GrabExpress

Teleport Logistics

Kerry Express Malaysia

Flash Express Malaysia

Skynet Worldwide Express Malaysia

- E Commerce Platforms Increasing Dependence on Fast Urban Delivery Networks

- Retail Chains Expanding Omni Channel Distribution Strategies

- Food Delivery Platforms Driving High Frequency Parcel Movement

- Healthcare Product Distribution Requiring Reliable Same Day Delivery

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now