Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Malaysia online insurance market generated approximately USD ~ billion in digitally originated gross written premiums based on disclosures from Bank Negara Malaysia and insurer annual reports, reflecting sustained migration of policy purchase and servicing to online channels across motor, health, and life segments. Expansion is driven by widespread mobile connectivity exceeding ~million subscriptions reported by the Malaysian Communications and Multimedia Commission, alongside insurer investment in instant underwriting engines, digital claims automation, and aggregator comparison platforms enabling fully remote policy lifecycle management.

Within Malaysia, Kuala Lumpur and Selangor dominate online insurance activity due to concentration of insurers, fintech intermediaries, high-income urban professionals, and advanced broadband infrastructure that supports mobile financial services adoption. Penang and Johor Bahru also demonstrate strong digital insurance uptake driven by export-oriented industries and cross-border employment patterns requiring flexible coverage. National leadership is reinforced by Malaysia’s position as a Southeast Asian Islamic finance hub, supporting digital takaful innovation and regional distribution partnerships through multilingual online platforms.

Market Segmentation

By Product Type

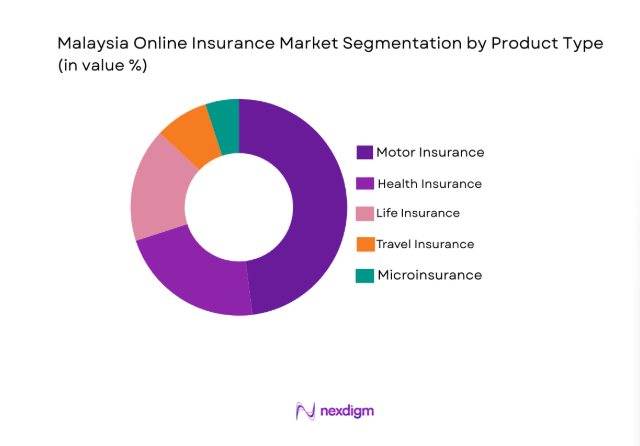

Malaysia online insurance market is segmented by product type into motor insurance, health insurance, life insurance, travel insurance, and microinsurance. Recently, motor insurance has a dominant market share due to factors such as mandatory vehicle coverage requirements, high vehicle ownership density, established insurer brand presence in motor policies, and seamless digital renewal integration with national road transport databases enabling instant policy issuance and verification.

By Platform Type

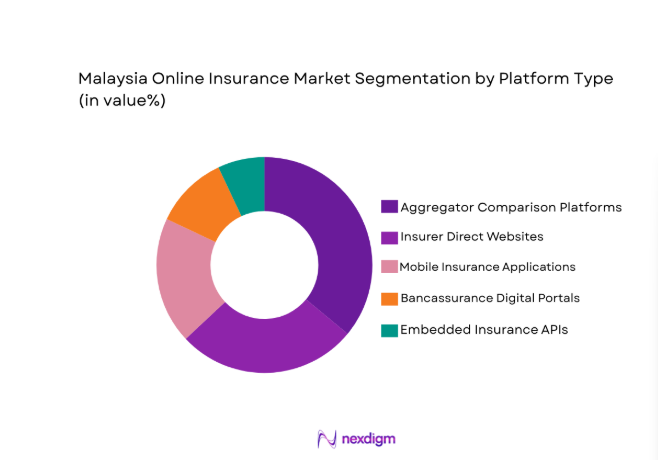

Malaysia online insurance market is segmented by platform type into insurer direct websites, mobile insurance applications, aggregator comparison platforms, bancassurance digital portals, and embedded insurance APIs. Recently, aggregator comparison platforms have a dominant market share due to factors such as transparent price comparison across insurers, simplified purchase journeys, strong fintech marketing reach, and consumer preference for multi-brand evaluation before selecting policies through centralized digital marketplaces.

Competitive Landscape

Malaysia online insurance market exhibits moderate consolidation led by large composite insurers and takaful operators that possess strong capital bases, multi-product portfolios, and nationwide distribution partnerships, while digital aggregators and insurtech platforms influence pricing transparency and customer acquisition dynamics. Major insurers maintain competitive advantage through brand trust, bancassurance alliances, and integrated digital servicing ecosystems, whereas newer platforms compete on user experience, comparison capabilities, and embedded insurance partnerships across ecommerce and fintech channels.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Digital Distribution Strength |

| AIA Malaysia | 1948 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Allianz Malaysia | 2001 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Prudential Assurance Malaysia | 1924 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Etiqa Insurance & Takaful | 2007 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Zurich Malaysia | 2006 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

Malaysia Online Insurance Market Analysis

Growth Drivers

Mobile-First Financial Behavior and High Digital Connectivity

Malaysia online insurance market expansion is strongly supported by widespread smartphone adoption, affordable mobile data access, and consumer familiarity with app-based financial transactions that collectively reduce barriers to purchasing and servicing insurance digitally across diverse demographic groups. Consumers routinely manage banking, payments, and investments through mobile interfaces, creating behavioral readiness to adopt fully digital insurance journeys without dependence on agents or branches, especially among urban salaried populations and digitally engaged youth cohorts. Insurers have aligned distribution strategies with this behavior by prioritizing mobile-optimized policy quotation, underwriting, and claims processes designed for rapid completion on handheld devices, improving conversion rates and customer satisfaction while reducing acquisition costs. Aggregator platforms and superapps have amplified mobile insurance penetration by embedding policy comparison and purchase functions within frequently used financial ecosystems, allowing users to evaluate coverage during routine digital financial interactions rather than dedicated insurance search processes. Continuous improvements in mobile network coverage across semi-urban regions have extended digital insurance accessibility beyond major cities, enabling first-time policyholders in emerging markets to access standardized protection products through smartphones without physical documentation requirements. Government digital identity initiatives and electronic verification frameworks further streamline onboarding by allowing insurers to authenticate customer information remotely, eliminating traditional paperwork and in-person verification constraints that previously limited online policy adoption. The integration of mobile notifications, digital policy storage, and automated renewal reminders enhances retention and lifetime value by maintaining persistent digital engagement between insurers and customers throughout policy cycles. Younger consumers demonstrate strong preference for self-service digital insurance management, reinforcing insurer investment in intuitive mobile interfaces, AI-assisted customer support, and real-time claims tracking that collectively normalize online insurance as a primary purchase channel. Increasing trust in digital financial services due to secure payment gateways and regulatory oversight has reduced perceived risk associated with online policy transactions, supporting broader demographic acceptance of digital insurance platforms. As mobile ecosystems continue to evolve toward integrated financial superapps, online insurance participation is expected to deepen structurally across Malaysia’s consumer base.

Regulatory Enablement and Digital Insurance Framework Development

Malaysia online insurance market growth is significantly reinforced by progressive regulatory initiatives from Bank Negara Malaysia that encourage electronic policy issuance, digital onboarding, and remote servicing while maintaining consumer protection and solvency oversight across insurers and takaful operators. Regulatory approval of electronic know-your-customer procedures allows insurers to complete identity verification through digital channels using national identification databases and biometric validation tools, removing historical compliance barriers that constrained fully online policy acquisition. Licensing frameworks for digital insurers and insurtech intermediaries foster competitive innovation by enabling new entrants to operate online-only models while adhering to prudential standards, thereby expanding consumer choice and accelerating digital product experimentation. Clear guidance on digital document validity and electronic signatures ensures legal enforceability of online policies, claims submissions, and endorsements, providing both insurers and customers confidence in remote transactions without physical documentation. Supervisory encouragement of financial inclusion initiatives has motivated insurers to develop simplified digital microinsurance and takaful offerings accessible through mobile channels, supporting underserved populations while expanding the online insurance customer base. Regulatory sandboxes facilitate testing of novel distribution models such as embedded insurance within ecommerce and fintech platforms, enabling insurers to refine digital propositions under controlled oversight before commercial rollout. Data protection and cybersecurity regulations strengthen trust in digital insurance ecosystems by mandating secure storage and transmission of customer information, addressing privacy concerns that previously discouraged online policy engagement. Standardization of digital reporting and disclosure requirements promotes transparency in online insurance marketing and pricing, allowing consumers to compare products confidently across platforms and reducing mis-selling risk. Collaboration between regulators and industry associations on digital literacy campaigns has improved consumer awareness of online insurance processes and rights, accelerating adoption across diverse socioeconomic segments. As regulatory frameworks continue to evolve toward fully digital insurance supervision, Malaysia online insurance market participation is positioned to expand sustainably across both conventional and takaful segments.

Market Challenges

Consumer Trust Deficit in Fully Digital Claims Settlement

Malaysia online insurance market development faces constraints from persistent consumer skepticism regarding fairness, transparency, and reliability of digital claims processes, particularly in segments such as health and motor where claim outcomes materially affect financial security and perceived insurer credibility. Many policyholders remain accustomed to agent-assisted claims guidance and express concern that fully automated digital submission and assessment may reduce personal advocacy during disputes or complex coverage interpretation scenarios. Instances of delayed digital claim processing or perceived algorithmic rejection have amplified apprehension about insurer accountability in online channels, encouraging some consumers to maintain offline policy relationships despite digital purchase convenience. Limited visibility into internal claims evaluation criteria and status progression within digital platforms reduces perceived transparency, making customers uncertain about documentation sufficiency or decision rationale compared with traditional face-to-face interactions. Variability in digital claims user experience across insurers and aggregators creates inconsistent expectations, with some platforms lacking intuitive guidance or real-time communication features necessary to reassure customers during high-stress claim events. Complex claims such as hospitalization or accident liability often require multiple document uploads and verifications, and difficulties navigating these requirements through mobile interfaces can discourage continued digital engagement or lead to incomplete submissions. Older demographic segments demonstrate lower digital confidence and fear procedural errors when submitting claims online, reinforcing reliance on agents and slowing full lifecycle digital migration. Perceived cybersecurity risks and data privacy concerns further undermine trust, particularly when sensitive medical or financial information must be transmitted electronically through insurer systems. Social media amplification of negative digital claims experiences can disproportionately influence public perception, creating reputational challenges for insurers seeking to promote online channels. Without consistent improvement in digital claims transparency, communication, and human support integration, trust barriers may continue to moderate Malaysia online insurance adoption across certain consumer segments.

Intense Price Competition and Margin Compression in Digital Channels

Malaysia online insurance market participants encounter significant profitability pressure arising from transparent price comparison across aggregators and direct platforms, which commoditizes standardized products such as motor and travel insurance and limits insurer ability to differentiate on non-price attributes. Consumers using digital marketplaces can evaluate multiple insurer quotations instantly, encouraging selection of lowest premium options and reducing brand loyalty traditionally cultivated through agent relationships and bundled offerings. Aggregators emphasize price ranking algorithms and promotional discounts to attract traffic, compelling insurers to match or undercut competitor pricing to maintain visibility and conversion rates within digital listings. Reduced distribution costs associated with online sales are partially offset by higher marketing expenditure on digital advertising, search optimization, and platform commissions required to compete for customer acquisition in crowded online environments. Standardized policy features mandated by regulation in segments like motor insurance further constrain product differentiation, intensifying price-based competition and narrowing underwriting margins across insurers. New insurtech entrants often adopt aggressive pricing strategies supported by venture funding or lean cost structures, disrupting incumbent pricing discipline and forcing established insurers to respond competitively in digital channels. Customer switching costs decline in online ecosystems where renewal reminders and comparison tools enable easy insurer changes annually, limiting long-term profitability and increasing retention challenges. Promotional campaigns and cashback incentives common in digital distribution erode premium revenue while conditioning consumers to expect discounts, complicating efforts to restore sustainable pricing levels. Continuous downward pressure on premiums may reduce insurer capacity to invest in advanced digital innovation or service improvements if margin erosion persists. Sustained price competition without parallel value differentiation therefore represents a structural challenge for Malaysia online insurance market profitability and strategic positioning.

Opportunities

Expansion of Digital Health and Microinsurance for Underserved Populations

Malaysia online insurance market holds significant growth potential through development of simplified digital health and microinsurance products targeting low-income households, gig workers, and informal sector participants who historically lacked access to affordable protection due to distribution and underwriting constraints. Mobile-based enrollment and premium payment flexibility enable insurers to reach populations outside traditional agent networks, supporting financial inclusion objectives while expanding policyholder volume through scalable digital platforms. Micro-duration coverage aligned with gig employment patterns allows workers to purchase protection only during active earning periods, enhancing affordability and relevance compared with annual policies. Integration of digital health insurance with telemedicine services and wellness applications creates bundled value propositions that encourage adoption among younger demographics comfortable with mobile healthcare access. Government support for inclusive insurance initiatives and takaful models provides regulatory alignment and social legitimacy for low-cost digital offerings addressing protection gaps across rural and semi-urban communities. Partnerships with telecommunications providers and fintech wallets facilitate premium collection through prepaid or micro-payment mechanisms suited to irregular income streams, reducing payment friction and lapse rates. Data analytics from digital platforms enables insurers to design risk-appropriate pricing and targeted product features based on behavioral and demographic insights derived from underserved segments. Awareness campaigns delivered through social media and community digital channels can educate populations previously unfamiliar with insurance concepts, improving understanding and trust in digital protection solutions. Scalable digital distribution allows insurers to achieve viable economics despite low individual premium values by aggregating large customer bases efficiently. Expansion of inclusive digital insurance therefore represents a major structural opportunity for Malaysia online insurance market growth and societal resilience.

Embedded Insurance Integration Across Ecommerce and Digital Ecosystems

Malaysia online insurance market can expand substantially through embedding protection products within ecommerce transactions, digital banking platforms, travel booking systems, and mobility applications, enabling contextual policy purchase at the point of need rather than separate insurance search journeys. Consumers purchasing electronics, travel tickets, or ride-hailing services can be offered relevant micro-coverage seamlessly during checkout, increasing conversion rates by aligning insurance with immediate purchase context and perceived risk exposure. Ecommerce platforms benefit from added revenue streams and customer value enhancement, while insurers gain scalable distribution without high marketing acquisition costs associated with standalone digital advertising. Real-time API connectivity between insurers and partner platforms enables automated underwriting and policy issuance based on transaction data, eliminating manual input and reducing friction for customers. Embedded insurance models also support dynamic pricing reflecting product value or trip duration, improving affordability and relevance compared with static annual policies. Financial superapps integrating payments, banking, and lifestyle services provide recurring engagement channels through which insurers can offer renewal prompts, upgrades, or complementary coverage aligned with user activity patterns. Cross-border ecommerce growth in Southeast Asia presents additional embedded distribution opportunities for travel and logistics-related insurance products linked to international transactions. Regulatory sandboxes in Malaysia encourage experimentation with such distribution innovations under supervised conditions, accelerating market readiness and consumer acceptance. Partnerships between insurers and digital ecosystem leaders can strengthen brand visibility and trust through association with widely used platforms. As digital commerce penetration deepens, embedded insurance integration is positioned to become a major structural growth pathway for Malaysia online insurance market expansion.

Future Outlook

Malaysia online insurance market is expected to expand steadily over the next five years supported by continued mobile financial adoption, deeper integration of insurance within digital ecosystems, and regulatory encouragement of electronic onboarding and claims processes. Insurers are likely to invest further in AI underwriting, automated claims assessment, and personalized digital engagement to improve efficiency and customer experience. Growth in embedded insurance, micro-coverage, and digital health products will broaden participation across new demographic segments. Strengthening cybersecurity and consumer protection frameworks will reinforce trust and sustain long-term digital channel migration.

Major Players

- AIA Malaysia

- Allianz Malaysia

- Prudential Assurance Malaysia

- Etiqa Insurance & Takaful

- Zurich Malaysia

- Great Eastern Life Malaysia

- Tokio Marine Life Malaysia

- Generali Insurance Malaysia

- Manulife Insurance Malaysia

- Sun Life Malaysia

- Tune Protect Group

- FWD Takaful

- RHB Insurance

- AmGeneral Insurance

- PolicyStreet

Key Target Audience

- Insurance companies

- Takaful operators

- Digital insurance platforms

- Banking and bancassurance institutions

- E-commerce and fintech platforms

- Investment and venture capitalist firms

- Government and regulatory bodies

- Technology providers

Research Methodology

Step 1: Identification of Key Variables

Key variables include digital premium volumes, online policy issuance rates, platform adoption, regulatory frameworks, and consumer behavior patterns across Malaysia online insurance distribution channels. These variables are derived from insurer disclosures, regulatory statistics, and digital finance adoption indicators to define market structure and segmentation parameters.

Step 2: Market Analysis and Construction

Market size and segmentation are constructed using insurer annual reports, Bank Negara Malaysia data, and digital distribution metrics to estimate online premium contribution across product and platform categories. Competitive positioning and ecosystem dynamics are mapped through company disclosures and platform penetration analysis.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings on growth drivers, challenges, and opportunities are validated through review of regulatory publications, industry associations, and insurer strategy reports to ensure alignment with observed digital insurance adoption trends in Malaysia. Assumptions are cross-checked against market behavior indicators.

Step 4: Research Synthesis and Final Output

Validated data and insights are synthesized into structured market analysis covering size, segmentation, competition, and outlook to produce a coherent assessment of Malaysia online insurance market dynamics. Final outputs integrate quantitative indicators with qualitative industry interpretation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

High Smartphone and Internet Penetration Enabling Mobile Policy Purchase

Regulatory Support for Electronic Policy Issuance and eKYC

Expansion of Aggregator and Embedded Insurance Distribution - Market Challenges

Low Consumer Trust in Fully Digital Claims Processes

Price Competition Compressing Digital Policy Margins

Limited Awareness of Non-Motor Online Insurance Products - Market Opportunities

Expansion of Health and Microinsurance via Mobile Channels

Partnerships with Ecommerce and Fintech Platforms

AI-Based Personalized Digital Insurance Offerings - Trends

Shift Toward App-Based Policy Lifecycle Management

Integration of Insurance in Digital Banking Superapps

Usage-Based and On-Demand Coverage Models

Automation of Claims Through Digital Verification

Growth of Embedded Insurance in Online Transactions - Government Regulations & Defense Policy

Bank Negara Malaysia Digital Insurance Frameworks

Electronic Know Your Customer Compliance Standards

Consumer Data Protection and Cybersecurity Regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Life Insurance Digital Platforms

Health Insurance Digital Platforms

Motor Insurance Digital Platforms

Travel Insurance Digital Platforms

Microinsurance Digital Platforms - By Platform Type (In Value%)

Insurer Direct Websites

Mobile Insurance Applications

Aggregator Comparison Platforms

Embedded Insurance APIs

Bancassurance Digital Portals - By Fitment Type (In Value%)

Standalone Online Policies

Bundled Financial Products

Embedded Retail Checkout Cover

Subscription-Based Protection

On-Demand Usage-Based Cover - By End User Segment (In Value%)

Urban Salaried Individuals

SME Owners and Entrepreneurs

Gig Economy Workers

Expatriate Residents

Students and Young Professionals

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product Breadth, Digital UX Capability, Pricing Competitiveness, Distribution Partnerships, Claims Automation Level)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

AIA Malaysia

Great Eastern Takaful Malaysia

Prudential Assurance Malaysia

Etiqa Insurance and Takaful

Allianz Malaysia

Zurich Malaysia

Tokio Marine Life Insurance Malaysia

Generali Insurance Malaysia

Manulife Insurance Berhad

Sun Life Malaysia

Tune Protect Group

FWD Takaful

RHB Insurance

AmGeneral Insurance

PolicyStreet

- Young Urban Consumers Driving Mobile-First Policy Adoption

- SMEs Increasingly Purchasing Digital Health and Liability Cover

- Gig Workers Seeking Flexible Microinsurance Products

- Expatriates Preferring Online Multilingual Insurance Platforms

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now