Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Malaysia Semiconductor Manufacturing market generated approximately USD ~ billion in manufacturing output value supported by the country’s extensive semiconductor assembly, testing, and wafer fabrication ecosystem according to data published by the Malaysia Investment Development Authority and national electronics industry statistics. The market is driven by strong global demand for integrated circuits used in consumer electronics, automotive electronics, telecommunications equipment, industrial automation systems, and data center processors produced within Malaysia’s advanced electronics manufacturing clusters.

Malaysia’s semiconductor manufacturing ecosystem is concentrated primarily in Penang, Kulim, and Selangor where multinational semiconductor firms operate fabrication plants, advanced packaging facilities, and semiconductor testing centers supported by strong electronics supply chains and export infrastructure. Penang functions as a major semiconductor manufacturing hub due to decades of electronics industry development and skilled engineering workforce availability, while Kulim High Tech Park hosts advanced wafer fabrication operations and Selangor supports semiconductor component manufacturing and global electronics logistics networks.

Market Segmentation

By Product Type

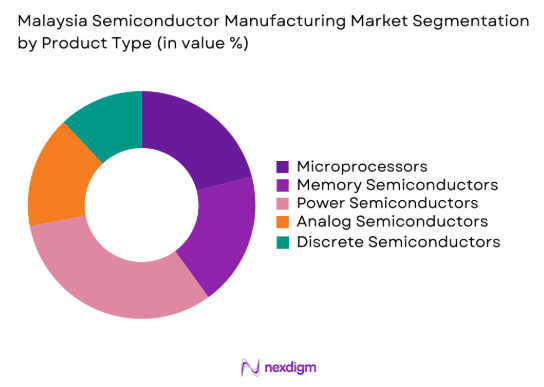

Malaysia Semiconductor Manufacturing market is segmented by product type into microprocessors, memory semiconductors, power semiconductors, analog semiconductors, and discrete semiconductors. Recently, power semiconductors have a dominant market share due to increasing demand for electric vehicles, renewable energy power management systems, industrial motor drives, and high efficiency power conversion technologies widely produced in Malaysian semiconductor facilities. Power semiconductor manufacturing benefits from large investment by global chip manufacturers expanding production capacity for automotive electronics and industrial automation applications. Malaysian semiconductor plants produce significant volumes of insulated gate bipolar transistors, power management integrated circuits, and silicon carbide devices supporting global electrification technologies.

By Manufacturing Stage

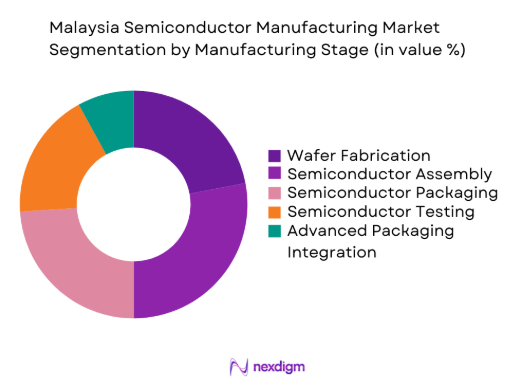

Malaysia Semiconductor Manufacturing market is segmented by manufacturing stage into wafer fabrication, semiconductor assembly, semiconductor packaging, semiconductor testing, and advanced packaging integration. Recently, semiconductor assembly has a dominant market share due to Malaysia’s strong specialization in outsourced semiconductor assembly and test services supported by global semiconductor companies operating advanced packaging facilities across Penang and Kulim. Assembly operations require precision semiconductor processing equipment, automated inspection technologies, and skilled technicians enabling Malaysian facilities to process high volumes of semiconductor chips for global electronics supply chains. Continuous investment in advanced packaging technologies including system in package and wafer level packaging further strengthens Malaysia’s role within the international semiconductor manufacturing ecosystem.

Competitive Landscape

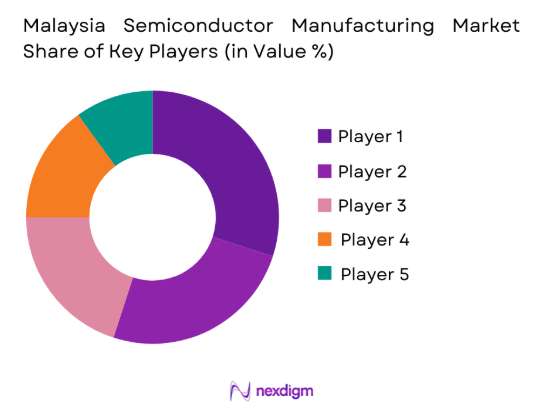

The Malaysia Semiconductor Manufacturing market demonstrates a moderately consolidated competitive structure where large multinational semiconductor companies operate major fabrication and advanced packaging facilities while regional semiconductor manufacturers contribute to specialized chip assembly and testing operations. Global semiconductor leaders maintain strong technological capabilities in wafer fabrication and chip design while Malaysian facilities focus heavily on advanced packaging, power semiconductor manufacturing, and outsourced semiconductor assembly and test services supporting global electronics supply chains.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fabrication Capacity |

| Intel Corporation | 1968 | United States | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies | 1999 | Germany | ~ | ~ | ~ | ~ | ~ |

| ASE Technology Holding | 1984 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Amkor Technology | 1968 | United States | ~ | ~ | ~ | ~ | ~ |

| Unisem Group | 1989 | Malaysia | ~ | ~ | ~ | ~ | ~ |

Malaysia Semiconductor Manufacturing Market Analysis

Growth Drivers

Expansion of Global Electronics Manufacturing Supply Chains into Southeast Asia

Malaysia has emerged as a major semiconductor manufacturing hub in Southeast Asia supported by strong electronics production infrastructure, stable industrial policies, and extensive global trade connectivity enabling semiconductor exports. Global electronics companies increasingly diversify semiconductor manufacturing across Southeast Asia to reduce supply chain dependency on single production locations and improve resilience against geopolitical disruptions. Malaysia benefits from decades of semiconductor manufacturing experience and well developed electronics supply chains including printed circuit board production, semiconductor packaging, precision engineering, and industrial automation equipment manufacturing. Multinational companies including Intel, Infineon, and ASE Technology operate large semiconductor facilities in the country. These investments strengthen Malaysia’s integrated semiconductor ecosystem and support expansion of advanced semiconductor manufacturing operations.

Growing Demand for Power Semiconductors and Automotive Electronics Chips

The rapid electrification of vehicles and expansion of renewable energy technologies significantly increase demand for advanced power semiconductors produced within Malaysia’s semiconductor industry. Electric vehicles require specialized semiconductor devices including insulated gate bipolar transistors, silicon carbide modules, and power management integrated circuits used in energy conversion and electric drive systems. Automotive electronics also integrate semiconductor chips supporting driver assistance systems, battery management, infotainment, and safety technologies. Renewable energy systems such as solar power and energy storage infrastructure depend on efficient power semiconductor modules for electricity conversion. Industrial automation equipment including robotics and factory control systems further drives demand. Semiconductor companies therefore expand fabrication technologies to support efficient power semiconductor production.

Market Challenges

Extremely High Capital Investment Requirements for Semiconductor Fabrication Facilities

Semiconductor manufacturing is among the most capital intensive industries because advanced wafer fabrication facilities require sophisticated equipment, ultra clean production environments, and continuous technology upgrades to remain competitive. Establishing a modern semiconductor fabrication plant requires multi billion dollar investments in photolithography systems, deposition equipment, etching tools, wafer inspection machines, and process control technologies essential for integrated circuit production. Malaysian semiconductor companies often depend on multinational technology firms to finance large fabrication investments due to these high infrastructure costs. Continuous reinvestment in advanced technology nodes and manufacturing equipment is also necessary. Rising electricity consumption, equipment maintenance expenses, and demand for skilled engineers further increase operational costs within Malaysia’s semiconductor manufacturing industry.

Global Semiconductor Supply Chain Vulnerabilities and Materials Dependency

Semiconductor manufacturing depends on complex global supply chains involving specialized materials, precision manufacturing equipment, and advanced chemical processing technologies sourced from international suppliers. Malaysian semiconductor facilities rely heavily on imported equipment including photolithography machines, wafer processing tools, and semiconductor metrology systems produced mainly in technologically advanced countries. Disruptions such as geopolitical trade restrictions, export control regulations, or equipment shortages can directly affect semiconductor production operations. Fabrication processes also require high purity chemicals, silicon wafers, specialty gases, and advanced photoresist materials. Many of these inputs originate from limited global suppliers, creating supply risks. Malaysian semiconductor companies therefore diversify suppliers and develop strategic partnerships to maintain stable manufacturing operations and reduce supply chain vulnerabilities.

Opportunities

Expansion of Advanced Semiconductor Packaging and Chip Integration Technologies

Advanced semiconductor packaging technologies represent one of the fastest growing segments within the semiconductor manufacturing ecosystem, and Malaysia is well positioned to benefit from increasing demand for advanced chip packaging solutions. Modern electronic devices require complex semiconductor architectures where multiple integrated circuits are combined into compact modules through technologies such as system in package, wafer level packaging, and three dimensional chip stacking. Malaysia hosts numerous outsourced semiconductor assembly and test providers capable of processing large volumes of semiconductor devices through advanced packaging operations. Semiconductor companies continue investing in packaging technologies integrating high performance computing chips, memory modules, and power management devices into compact semiconductor packages used across smartphones, automotive electronics, artificial intelligence processors, and telecommunications infrastructure.

Foreign Direct Investment and Semiconductor Manufacturing Expansion Programs

International semiconductor companies increasingly invest in Malaysia to strengthen supply chain resilience and diversify global chip production. Malaysia offers stable industrial policies, well developed electronics manufacturing infrastructure, and a strategic location within Asia that supports global semiconductor trade. Government agencies promote semiconductor expansion through investment incentives, tax benefits, and high technology industrial parks attracting multinational manufacturers. New fabrication plants, packaging facilities, and semiconductor research centers continue expanding across the country. Companies benefit from skilled engineering talent, reliable electronics supply chains, and strong export logistics networks. Rising demand for semiconductors used in artificial intelligence, electric vehicles, telecommunications infrastructure, and industrial automation further supports continued semiconductor manufacturing investment in Malaysia.

Future Outlook

The Malaysia Semiconductor Manufacturing market is expected to expand steadily over the coming years as global semiconductor demand continues rising across automotive electronics, artificial intelligence computing systems, telecommunications infrastructure, and renewable energy technologies. Semiconductor companies are likely to invest further in advanced packaging facilities, power semiconductor manufacturing technologies, and automated semiconductor production systems. Continued government investment incentives and strategic semiconductor industry development programs will further strengthen Malaysia’s role within the global semiconductor supply chain.

Major Players

- Intel Corporation

- Infineon Technologies

- ASE Technology Holding

- Amkor Technology

- UnisemGroup

- InariAmertronBerhad

- Carsem Semiconductor

- Micron Technology

- SilTerraMalaysia

- Globetronics Technology

- Texas Instruments

- STMicroelectronics

- Renesas Electronics

- JHM Consolidation Berhad

- OsramOptoSemiconductors

Key Target Audience

- Semiconductor Manufacturing Companies

- Electronics Manufacturing Companies

- Automotive Electronics Manufacturers

- Industrial Automation Equipment Manufacturers

- Telecommunications Infrastructure Companies

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Semiconductor Equipment Manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key semiconductor manufacturing variables including wafer fabrication capacity, semiconductor packaging technologies, chip demand across electronics sectors, global semiconductor supply chains, and industrial policy frameworks are identified to define the analytical boundaries of the Malaysia Semiconductor Manufacturing market.

Step 2: Market Analysis and Construction

Comprehensive analysis integrates manufacturing output statistics, semiconductor industry production data, government industrial investment records, electronics manufacturing exports, and semiconductor equipment procurement trends to construct a structured view of Malaysia’s semiconductor manufacturing ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including semiconductor engineers, electronics manufacturing specialists, semiconductor equipment suppliers, and industrial policy analysts validate research assumptions through consultations ensuring accurate interpretation of semiconductor manufacturing market developments.

Step 4: Research Synthesis and Final Output

All quantitative industry data, qualitative insights, semiconductor production trends, and expert inputs are synthesized into a structured research framework generating an integrated market intelligence report describing Malaysia’s semiconductor manufacturing landscape.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Global Electronics Manufacturing Supply Chains

Government Incentives Supporting Semiconductor Investment

Growing Demand for Automotive and Industrial Semiconductors - Market Challenges

High Capital Requirements for Semiconductor Fabrication Facilities

Supply Chain Disruptions in Semiconductor Equipment and Materials

Shortage of Skilled Semiconductor Engineering Talent - Market Opportunities

Expansion of Advanced Packaging and Chip Testing Facilities

Foreign Direct Investment in Semiconductor Manufacturing Infrastructure

Growth of Power Semiconductor Manufacturing for Electric Vehicles - Trends

Adoption of Advanced Packaging Technologies

Integration of Automation and Smart Manufacturing Systems

Increasing Localization of Semiconductor Supply Chains - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price ,2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Equipment

Assembly and Packaging Systems

Semiconductor Testing Equipment

Photolithography Systems

Process Control and Metrology Equipment - By Platform Type (In Value%)

Integrated Circuit Manufacturing Platforms

Memory Semiconductor Manufacturing Platforms

Power Semiconductor Manufacturing Platforms

Analog Semiconductor Manufacturing Platforms

Discrete Semiconductor Manufacturing Platforms - By Fitment Type (In Value%)

Front-End Manufacturing Systems

Back-End Assembly Systems

Integrated Manufacturing Lines

Modular Semiconductor Processing Systems

Automated Semiconductor Production Systems - By End User Segment (In Value%)

Integrated Device Manufacturers

Foundry Service Providers

Outsourced Semiconductor Assembly and Test Providers

Electronics Manufacturing Service Companies

Automotive Semiconductor Suppliers - By Procurement Channel (In Value%)

Direct Procurement from Equipment Manufacturers

Strategic Supplier Partnerships

Government Supported Technology Procurement Programs

Industrial Equipment Distributors

Technology Integration Contractors

- Market Share Analysis

- Cross Comparison Parameters (Manufacturing Technology Node, Production Capacity, Advanced Packaging Technology Capability, Wafer Fabrication Capability, Semiconductor Process Technology, Regional Manufacturing Presence, End Market Application Focus, R&D Investment Intensity, Supply Chain Integration Capability, Strategic Industry Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intel Corporation

Infineon Technologies

STMicroelectronics

Texas Instruments

Renesas Electronics

ASE Technology Holding

Amkor Technology

Unisem Group

Inari Amertron Berhad

Carsem Semiconductor

Micron Technology

SilTerra Malaysia

Silterra Manufacturing

Globetronics Technology

JHM Consolidation Berhad

- Integrated Device Manufacturers Expanding Regional Production Capacity

- Foundry Companies Strengthening Global Contract Manufacturing Networks

- OSAT Providers Increasing Advanced Packaging Capabilities

- Electronics Manufacturers Securing Local Semiconductor Supply Chains

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now