Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Malaysia Used Harvester Market Outlook to 2035 market current size stands at around USD ~ million, reflecting steady circulation of refurbished and preowned harvesters across smallholder and plantation farming systems. Market activity is supported by active dealer resale, independent refurbishers, and farm-to-farm transactions, with service networks enabling lifecycle extension. Financing access through rural cooperatives and equipment leasing underpins replacement cycles, while parts availability and reconditioning standards shape transactional confidence and sustained equipment utilization across cropping seasons.

Demand concentration is strongest across rice-growing clusters in Kedah and Perlis, alongside plantation corridors in Johor and Sabah where mechanized harvesting is operationally entrenched. Logistics connectivity to ports and inland depots supports inflows of refurbished units, while localized service workshops anchor uptime. Regional policy emphasis on farm mechanization and labor substitution strengthens ecosystem maturity, and dealer networks aligned with after-sales coverage influence buyer confidence and geographic penetration patterns.

Market Segmentation

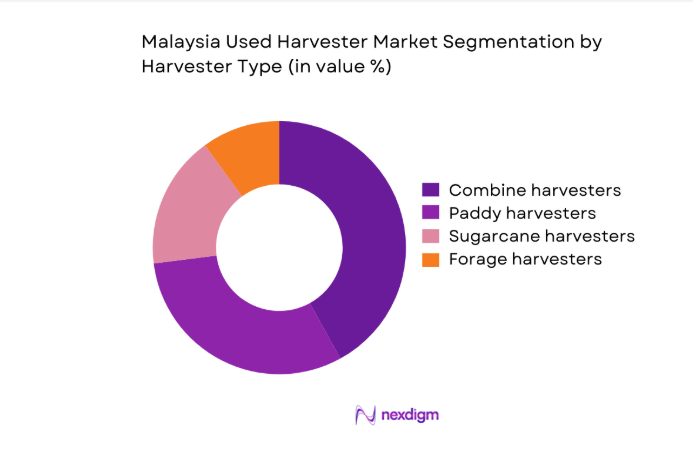

By Harvester Type

Combine and paddy harvesters dominate transaction activity due to suitability for fragmented landholdings and multi-crop adaptability. Compact configurations fit narrow field access and short harvesting windows, encouraging reuse cycles. Sugarcane and forage units show selective uptake within plantation clusters where terrain and crop density justify specialized machinery. Dealer refurbishment programs prioritize high-turnover models with reliable parts ecosystems, reinforcing liquidity in common formats. The installed fleet composition also reflects historic import patterns from neighboring mechanized markets, shaping resale velocity. Operator familiarity with specific platforms lowers switching barriers, consolidating demand around widely serviced types.

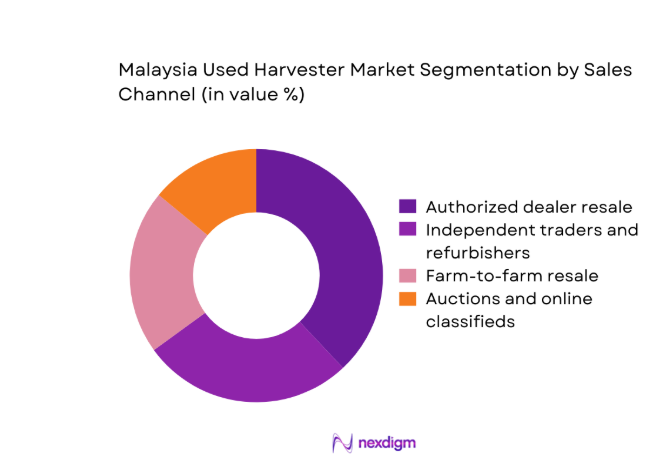

By Sales Channel

Authorized dealer resale leads due to certification, warranty options, and bundled service contracts that reduce operational risk for buyers. Independent traders and refurbishers provide price-accessible alternatives, serving smallholders seeking lower entry barriers. Farm-to-farm resale remains active in rural clusters, supported by trust-based networks and local repair capability. Auctions and online classifieds are gaining traction as discovery channels, improving price transparency and expanding geographic reach. Channel dominance reflects buyer risk tolerance, financing access, and proximity to service depots. Digital discovery increasingly complements physical inspection, accelerating deal flow while retaining offline completion norms.

Competitive Landscape

The competitive landscape is characterized by a mix of OEM-affiliated dealers, regional equipment distributors, and specialized refurbishers that differentiate through service coverage, refurbishment depth, and financing facilitation. Competitive positioning is shaped by parts availability, turnaround times for reconditioning, and localized service reach across agricultural clusters.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Kubota Malaysia | 1978 | Shah Alam | ~ | ~ | ~ | ~ | ~ | ~ |

| Yanmar Malaysia | 1912 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ | ~ |

| ISEKI Malaysia | 1926 | Selangor | ~ | ~ | ~ | ~ | ~ | ~ |

| AGCO Malaysia | 1990 | Selangor | ~ | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial Malaysia | 2013 | Selangor | ~ | ~ | ~ | ~ | ~ | ~ |

Malaysia Used Harvester Market Analysis

Growth Drivers

Mechanization push in paddy cultivation

Public programs expanded mechanized harvesting coverage across rice clusters, increasing equipment utilization cycles. In 2024, agricultural mechanization grants supported 12 regional deployment programs, with 3 national agencies coordinating field-level adoption. Labor constraints intensified during peak harvest windows, where farm operators reported 4 to 6 week compression of harvesting schedules. Irrigation modernization in 2023 covered 9 major granary zones, improving machine operability. Training centers certified 1,200 operators in 2025, raising confidence in pre-owned equipment handling. Rural credit disbursement channels processed 18,000 equipment-related applications in 2024, reinforcing reuse markets. Import inspection throughput at two ports cleared 7,400 refurbished units in 2025, sustaining circulation.

Rising cost of new harvesters

Capital intensity for new agricultural machinery constrained smallholder acquisition, redirecting demand toward refurbished units. In 2024, commercial bank equipment loans carried 2 tightening cycles aligned with policy rate adjustments. Dealer financing approvals in 2025 recorded 9 additional documentation requirements for new machinery compared with used units. Exchange rate volatility during 2023 increased landed costs for imported new equipment across 4 procurement windows. Warehouse inventory turnover for new harvesters slowed to 68 days in 2024, while refurbished units averaged 31 days. Repair workshops expanded capacity by 22 bays nationwide in 2025 to support lifecycle extension. Training curricula for maintenance technicians added 6 modules focused on legacy platforms during 2024.

Challenges

Inconsistent quality and grading of used machines

Quality dispersion across refurbished units undermines buyer confidence and complicates valuation. In 2024, 5 inspection protocols were applied unevenly across independent refurbishers, creating variability in condition disclosure. Certification audits covered 42 workshops in 2025, identifying 11 recurring nonconformance issues in drivetrain and hydraulic systems. Spare parts traceability checks flagged 3 supply chains with documentation gaps during 2023. Warranty claim resolution times averaged 21 days in 2024, compared with 9 days at certified dealers. Field breakdown reports logged 1,260 incidents in 2025 across mixed-condition units. Operator retraining programs addressed 8 common misuse patterns observed during post-sale assessments.

Limited availability of genuine spare parts for older models

Parts constraints elevate downtime and maintenance risk for legacy platforms prevalent in secondary markets. In 2023, 14 discontinued model lines required substitute components sourced through parallel channels. Customs clearance delays affected 2 primary inbound routes in 2024, extending lead times by 17 days for critical assemblies. Dealer inventories prioritized 6 high-rotation parts families, leaving low-volume components understocked. Workshop cannibalization practices increased by 4 documented cases per month in 2025 to sustain operability. Technical bulletins issued in 2024 covered 9 retrofit pathways for obsolete electronics. Training programs certified 380 technicians in 2025 to fabricate interim fittings for hydraulic and belt systems.

Opportunities

Development of certified pre-owned programs by OEM dealers

Formal certification can standardize quality, elevate trust, and improve asset liquidity. In 2024, dealer networks piloted 3 certification frameworks aligned with manufacturer service manuals. Audit coverage expanded to 26 outlets in 2025, integrating 12-point inspection checklists for powertrain, hydraulics, and control systems. Warranty adoption rates increased across 2 consecutive quarters in 2025 as service contracts bundled maintenance visits. Technician accreditation programs certified 540 personnel in 2024 to execute refurbishment protocols. Digital service records adoption reached 8 platforms integrated with dealer ERP systems in 2025. Logistics hubs consolidated 5 regional reconditioning centers in 2024 to reduce turnaround times for certified inventory circulation.

Digital marketplaces for used agricultural machinery

Online discovery channels can expand reach, improve price transparency, and shorten transaction cycles. In 2024, 6 domestic platforms enabled listing verification with machine serial tracking. Mobile app adoption recorded 480,000 active users across rural districts in 2025. Listing-to-inspection conversion averaged 3 days during 2024 due to geotagged inventory mapping. Digital escrow pilots processed 1,900 transactions in 2025, reducing counterparty risk. Telematics retrofits enabled remote diagnostics for 2,700 units in 2024, supporting condition disclosure. Government e-procurement standards updated in 2025 introduced 4 compliance criteria for machinery listings, enhancing trust in online marketplaces and accelerating cross-regional deal flow.

Future Outlook

The market outlook reflects continued policy emphasis on mechanization, growing formalization of refurbishment standards, and deeper penetration of digital discovery channels. Regional service ecosystems are expected to mature as certification frameworks expand and technician training scales. Cross-border sourcing will remain active, while financing innovation and warranty-backed resale models strengthen buyer confidence across cycles through 2035.

Major Players

- Kubota Malaysia

- Yanmar Malaysia

- ISEKI Malaysia

- AGCO Malaysia

- CNH Industrial Malaysia

- Sime Darby Industrial

- UMW Equipment

- Niplo Malaysia

- Shin-Norin Machinery Malaysia

- TC Machinery Trading

- Fujimoto Agricultural Machinery

- Kumpulan Selangor Agro

- Tractors Malaysia

- Boon Siew Machinery

- Sabah Agro Machinery

Key Target Audience

- Contract harvesting service providers

- Rice and plantation farm operators

- Authorized agricultural machinery dealers

- Independent refurbishers and service workshops

- Rural cooperatives and farmer associations

- Equipment leasing and financing institutions

- Investments and venture capital firms

- Government and regulatory bodies with agency names including the Ministry of Agriculture and Food Security Malaysia and the Department of Agriculture Malaysia

Research Methodology

Step 1: Identification of Key Variables

Core variables include harvester type mix, refurbishment depth, service network coverage, parts availability, financing access, and channel performance across regions. Data points are aligned to operational indicators and lifecycle utilization patterns. Policy instruments influencing mechanization adoption are mapped to regional clusters.

Step 2: Market Analysis and Construction

Supply chains are structured across import, refurbishment, resale, and after-sales nodes. Channel flows are constructed using dealer throughput and workshop capacity indicators. Regional ecosystems are profiled by service density and logistics connectivity.

Step 3: Hypothesis Validation and Expert Consultation

Operational hypotheses are validated through structured interviews with dealers, refurbishers, operators, and service technicians. Workshop audits and field observations triangulate refurbishment quality assumptions. Policy interpretation is aligned with implementing agencies.

Step 4: Research Synthesis and Final Output

Findings are synthesized into demand drivers, constraints, and opportunity pathways. Cross-validation ensures consistency across regional clusters and channel dynamics. Insights are structured to support strategic planning and operational execution.

- Executive Summary

- Research Methodology (Market Definitions and grading of used harvesters, Dealer and refurbisher interviews across Malaysia, Field surveys of paddy and plantation operators, Transaction price scraping from auction and classifieds, Import-export and reconditioning flow tracking, Spare parts and service network mapping)

- Definition and Scope

- Market evolution

- Usage patterns across paddy and plantation crops

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Mechanization push in paddy cultivation

Rising cost of new harvesters

Expansion of contract harvesting services

Availability of reconditioned imports from Japan and Thailand

Financing support from agro-cooperatives and rural banks

Labor shortages during peak harvest seasons - Challenges

Inconsistent quality and grading of used machines

Limited availability of genuine spare parts for older models

High refurbishment and reconditioning costs

Fragmented dealer and reseller network

Regulatory scrutiny on used machinery imports

Low residual value perception among smallholders - Opportunities

Development of certified pre-owned programs by OEM dealers

Digital marketplaces for used agricultural machinery

Local refurbishment hubs near rice bowls

Leasing and pay-per-use models for smallholders

Integration of telematics retrofits for older harvesters

Cross-border sourcing partnerships with regional suppliers - Trends

Growing preference for Japanese-origin used harvesters

Shift toward dealer-backed warranties on refurbished units

Rising demand for compact harvesters for small plots

Increased online discovery and price transparency

Bundling of maintenance contracts with used equipment sales

Adoption of financing and trade-in schemes - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Harvester Type (in Value %)

Combine harvesters

Paddy harvesters

Sugarcane harvesters

Forage harvesters - By Crop Application (in Value %)

Rice and paddy

Oil palm plantations

Sugarcane estates

Mixed crop farming - By Power Capacity (in Value %)

Below 100 HP

100–200 HP

Above 200 HP - By Condition Grade (in Value %)

Refurbished and certified

Operational used

As-is for parts - By Sales Channel (in Value %)

Authorized dealer resale

Independent traders and refurbishers

Farm-to-farm resale

Auctions and online classifieds - By Region (in Value %)

Peninsular Malaysia

Sabah

Sarawak

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (brand reputation, refurbishment capability, pricing competitiveness, parts availability, warranty coverage, geographic reach, financing options, after-sales service footprint)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Kubota Malaysia

Yanmar Malaysia

ISEKI Malaysia

AGCO Malaysia

CNH Industrial Malaysia

Sime Darby Industrial

UMW Equipment

Niplo Malaysia

Shin-Norin Machinery Malaysia

TC Machinery Trading

Fujimoto Agricultural Machinery

Kumpulan Selangor Agro

Tractors Malaysia

Boon Siew Machinery

Sabah Agro Machinery

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now