Download PDF

Download PDF Download PDF

Download PDF- Investment and venture capitalist firms

- Private banks and wealth management institutions

- Asset management companies

- Family offices

- Government and regulatory bodies

- High-net-worth investors

- Financial advisory firms

- Islamic finance institutions

Market Overview

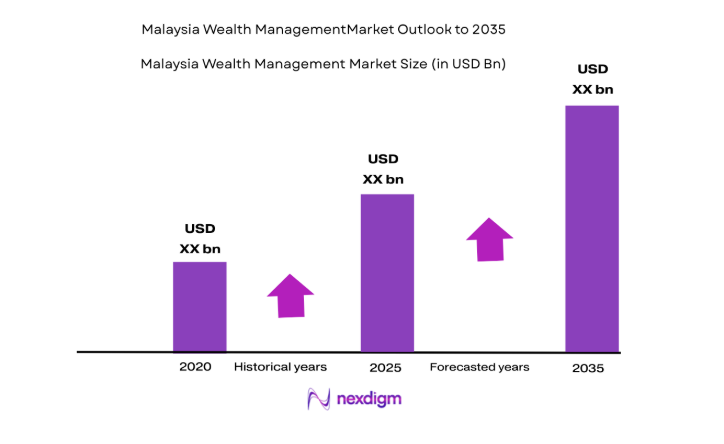

Malaysia wealth management market assets under management reached approximately USD ~ billion across private banking, advisory, and discretionary mandates based on Bank Negara Malaysia and Securities Commission Malaysia disclosures. Growth is driven by expanding high-net-worth population, rising capital market participation, and increasing allocation to managed portfolios. Private banks and investment institutions expanded structured investment and trust services, while digital wealth platforms widened access among affluent investors, strengthening professionally managed financial asset penetration nationwide.

Within Malaysia, Kuala Lumpur dominates wealth management activity due to concentration of financial institutions, private banks, and high-income professionals linked to corporate headquarters and capital markets. Labuan functions as an offshore structuring hub attracting regional wealth through international financial center frameworks and tax-efficient vehicles. Penang and Johor Bahru contribute through entrepreneurial wealth and cross-border business ownership, while Singapore linkages reinforce Malaysia’s position in Southeast Asian cross-border wealth flows.

Market Segmentation

By Product Type

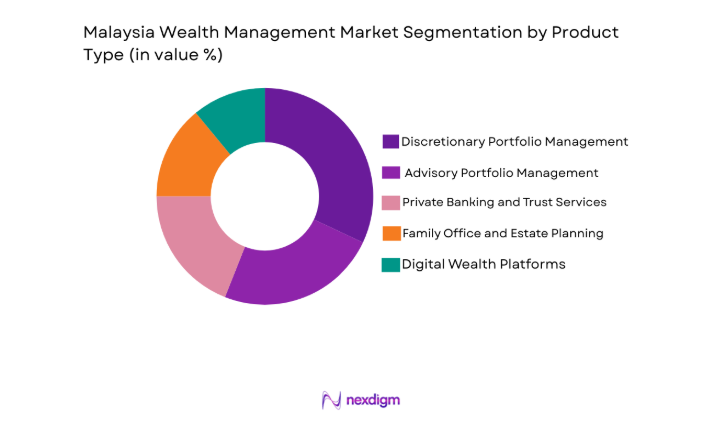

Malaysia Wealth Management market is segmented by product type into discretionary portfolio management, advisory portfolio management, private banking and trust services, family office and estate planning, and digital wealth platforms. Recently, discretionary portfolio management has a dominant market share due to rising demand for professional asset allocation among high-net-worth clients seeking diversified global exposure and risk-managed returns. Private banks and investment firms increasingly promote discretionary mandates as wealth complexity grows, enabling structured multi-asset portfolios and active management aligned with client objectives. Regulatory suitability frameworks encourage formal advisory structures, while clients prefer delegated decision-making amid volatile markets and expanding alternative investments. Institutionalization of family wealth and liquidity events from business exits further accelerate transition toward discretionary mandates across Malaysia’s affluent and high-net-worth segments.

By Platform Type

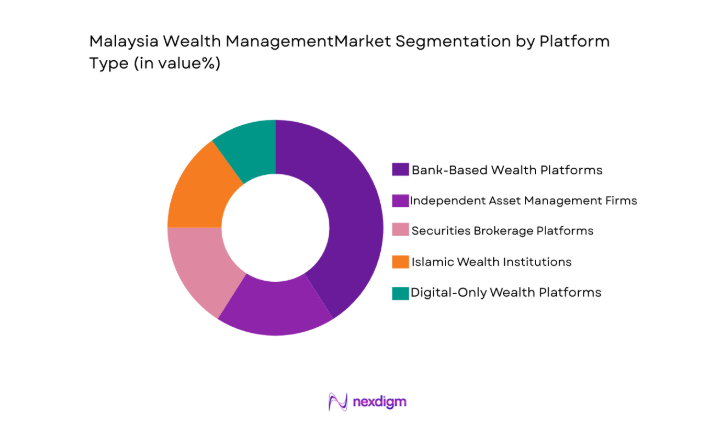

Malaysia Wealth Management market is segmented by platform type into bank-based wealth platforms, independent asset management firms, securities brokerage platforms, Islamic wealth institutions, and digital-only wealth platforms. Recently, bank-based wealth platforms have a dominant market share due to entrenched client relationships, nationwide branch networks, and integrated banking-investment offerings enabling seamless wealth services. Major Malaysian banks leverage large deposit client bases to cross-sell investment and portfolio services, supported by relationship managers and research capabilities. Clients trust established banking institutions for custody and advisory, while regulatory oversight and capital strength reinforce confidence. Cross-border capabilities through regional banking networks further consolidate bank-led wealth platform dominance.

Competitive Landscape

The market is moderately consolidated with leading domestic banks and global private banks controlling high-net-worth client assets, supported by strong distribution networks and advisory capabilities. International institutions compete in ultra-high-net-worth and cross-border structuring segments, while independent asset managers and digital platforms expand within affluent investors. Islamic wealth institutions maintain strong niche positioning through Sharia-compliant investment expertise, reinforcing competitive differentiation across client segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Client Segment Focus |

| Maybank Private Wealth | 1960 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| CIMB Private Banking | 1974 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| Public Bank Private Banking | 1966 | Kuala Lumpur | ~ | ~ | ~ | ~ | ~ |

| HSBC Global Private Banking Malaysia | 1865 | London | ~ | ~ | ~ | ~ | ~ |

| UOB Private Bank Malaysia | 1935 | Singapore | ~ | ~ | ~ | ~ | ~ |

Malaysia Wealth Management Market Analysis

Growth Drivers

Rising High-Net-Worth Population and Financial Asset Formalization

Malaysia wealth management market expansion is strongly driven by sustained growth in high-net-worth individuals generated through entrepreneurship, corporate ownership, and capital market participation that collectively increase demand for professional asset management and advisory services across domestic financial institutions. As Malaysian businesses expand regionally and liquidity events from corporate transactions rise, wealth holders accumulate investable financial assets requiring structured portfolio allocation, risk management, and succession planning frameworks beyond traditional savings or property holdings. Private banks and wealth institutions capture this demand by offering discretionary mandates, trust structures, and diversified multi-asset portfolios aligned with global markets and alternative investments. The transition from informal asset holding toward managed financial portfolios accelerates as second-generation wealth inheritors seek institutional governance, reporting transparency, and long-term preservation strategies integrated with family wealth objectives. Malaysia’s mature banking infrastructure and regulatory frameworks enable scalable wealth services delivery through relationship managers and digital advisory tools that extend reach beyond ultra-wealthy segments into emerging affluent investors. Capital market development including equities, bonds, and unit trusts provides domestic investment channels that complement international diversification through global funds and structured products offered by wealth providers. Tax-efficient structures and estate planning vehicles increase adoption of professional wealth management solutions as families formalize intergenerational transfer strategies and asset protection frameworks. Rising financial literacy and exposure to global investment opportunities further encourage clients to allocate assets into managed portfolios rather than self-directed holdings. Institutional credibility of major Malaysian banks and international private banks reinforces client trust in professional wealth services, sustaining inflows into discretionary and advisory mandates nationwide.

Digitalization of Wealth Platforms and Hybrid Advisory Adoption

Malaysia wealth management market growth is increasingly supported by digital transformation across banking and investment platforms that enable scalable, efficient, and accessible wealth services delivery to broader affluent and high-net-worth client segments. Financial institutions deploy digital onboarding, portfolio analytics, and remote advisory systems that streamline client acquisition and enhance engagement while reducing operational friction in account opening and investment execution processes. Hybrid advisory models combining relationship managers with digital portfolio monitoring tools allow clients to access professional investment management with greater transparency, convenience, and responsiveness aligned with modern financial behavior. Digital wealth platforms also lower minimum investment thresholds, expanding managed portfolio adoption among emerging affluent professionals whose investable assets are rising with income growth and capital market participation. Integration of data analytics and risk profiling algorithms supports personalized asset allocation and suitability assessment, strengthening advisory quality and regulatory compliance across Malaysian wealth providers. Clients increasingly demand real-time portfolio visibility, performance reporting, and digital communication channels, prompting institutions to modernize wealth interfaces and mobile investment platforms. Cross-border connectivity through digital banking networks enables Malaysian investors to access global markets and products seamlessly, reinforcing portfolio diversification and international wealth integration. Digitalization further enhances operational scalability for banks and asset managers, allowing them to serve larger client bases without proportional expansion of physical infrastructure or advisory staff. Competitive pressure from fintech and robo-advisory entrants accelerates innovation among incumbent banks, ensuring continuous technology investment and service modernization across Malaysia’s wealth management ecosystem.

Market Challenges

Limited Domestic Alternative Investment Depth and Concentrated Asset Allocation

Malaysia wealth management market faces structural constraints from relatively limited domestic alternative investment opportunities and concentrated asset allocation patterns that restrict portfolio diversification within locally accessible investment vehicles. High-net-worth clients traditionally allocate substantial wealth toward real estate, family businesses, and bank deposits, creating portfolio concentration that reduces demand for diversified managed portfolios compared with more mature wealth markets. Domestic capital markets, while developed in equities and bonds, offer narrower private equity, venture capital, hedge fund, and real asset exposure, limiting local discretionary mandates’ ability to deliver global diversification without offshore structures. Wealth managers must rely on international funds and cross-border investment products to meet diversification objectives, increasing regulatory complexity, custody considerations, and currency risk exposure for Malaysian investors. Limited scale of domestic alternative managers also reduces institutional investment depth and track record visibility, constraining allocation confidence among conservative wealth holders. Family-owned conglomerate wealth structures often retain assets within operating businesses, delaying transition into professionally managed financial portfolios and reducing addressable wealth management penetration. Illiquidity preferences and intergenerational business continuity priorities further anchor wealth in corporate holdings rather than diversified portfolios. Financial advisory adoption remains uneven across wealth tiers due to cultural preference for tangible assets and self-directed investment decisions. Expanding domestic alternative investment ecosystem remains critical for sustained discretionary portfolio growth and competitive parity with regional wealth centers.

Talent Shortage in Advanced Advisory and Family Office Structuring Expertise

Malaysia wealth management sector encounters capability constraints arising from limited availability of highly specialized professionals in discretionary portfolio management, cross-border tax structuring, and family office governance design required for sophisticated high-net-worth advisory services. As wealth complexity increases among Malaysian ultra-high-net-worth families with regional business interests and global asset exposure, demand for integrated advisory covering estate planning, philanthropy structuring, investment strategy, and intergenerational governance exceeds current domestic talent capacity. Private banks and asset managers compete for experienced relationship managers and investment advisors capable of delivering institutional-grade portfolio construction and alternative investment access, creating recruitment pressure and rising compensation costs. Family office formation trends further intensify demand for expertise in trust law, fiduciary oversight, and succession frameworks that combine financial, legal, and governance competencies. Malaysia’s advisory workforce pipeline remains smaller than global wealth hubs, requiring institutions to rely on expatriate expertise or regional centers for complex structuring services. Limited domestic training infrastructure and certification pathways in advanced wealth advisory slow professional development and skill scaling across the industry. Talent scarcity constrains service depth, innovation, and client coverage expansion, particularly in ultra-high-net-worth segments requiring bespoke solutions. Competition from Singapore and Hong Kong wealth hubs attracts experienced Malaysian advisors abroad, intensifying domestic shortages. Sustained capability development remains essential for Malaysia to advance from relationship-based private banking toward comprehensive wealth management leadership.

Opportunities

Expansion of Malaysia as Regional Islamic Wealth Management Hub

Malaysia wealth management market holds significant expansion potential through positioning as a leading global Islamic wealth management center attracting Sharia-compliant assets from Southeast Asia, the Middle East, and Muslim high-net-worth populations seeking ethical investment frameworks aligned with religious principles. Malaysia’s established Islamic finance ecosystem including Sukuk markets, Sharia-compliant funds, and regulatory expertise provides structural advantage for scaling Islamic discretionary portfolios and cross-border wealth structuring solutions. Wealth institutions can leverage domestic Sharia scholarship, product innovation, and certification credibility to design diversified multi-asset portfolios compliant with Islamic investment guidelines while delivering competitive financial returns. Regional Muslim investors seeking professionally managed halal portfolios increasingly consider Malaysia as an alternative to conventional wealth hubs lacking deep Islamic finance infrastructure. Integration of Islamic wealth platforms with global investment markets expands product breadth and geographic diversification while maintaining Sharia compliance across asset classes. Labuan international financial center supports offshore Islamic wealth structures including trusts and foundations suitable for cross-border Muslim families and institutional investors. Rising global interest in ethical and ESG-aligned investments further converges with Islamic wealth principles, widening investor appeal beyond religious segments. Malaysia’s geopolitical stability, regulatory clarity, and financial sector maturity reinforce its credibility as an Islamic wealth domicile. Strategic development of Islamic family office services and international marketing can significantly elevate Malaysia’s wealth management inflows and industry scale.

Growth of Family Office Structures Among Malaysian Entrepreneurial Wealth

Malaysia wealth management market presents strong opportunity through accelerating formation of family offices among first- and second-generation entrepreneurial wealth holders seeking institutionalized governance, investment oversight, and intergenerational succession planning frameworks tailored to complex family asset structures. As Malaysian business founders monetize stakes through listings, mergers, or generational transition, liquidity conversion from operating businesses into financial assets increases demand for centralized wealth administration and strategic asset allocation services. Family offices enable integrated management of investments, philanthropy, estate structures, and governance policies that preserve family control while professionalizing financial stewardship across generations. Wealth institutions and advisory firms can capture this trend by offering outsourced family office services, trust structuring, consolidated reporting, and discretionary investment management aligned with family mandates. Malaysia’s regulatory and legal environment supports trust and foundation frameworks suitable for domestic and cross-border family wealth, particularly through Labuan structures. Growing awareness of succession risks and governance challenges among business families accelerates adoption of structured family office models. Institutionalization of family wealth enhances demand for alternative investments, global diversification, and professional advisory capabilities across Malaysian wealth providers. Development of domestic expertise and service infrastructure around family offices can significantly expand Malaysia’s wealth management depth and sophistication.

Future Outlook

Malaysia wealth management market is expected to expand steadily as rising financial wealth, digital advisory adoption, and regional asset flows reinforce demand for professional portfolio management. Islamic wealth positioning, family office growth, and cross-border diversification will strengthen Malaysia’s role within Southeast Asian wealth networks. Technology integration and regulatory support for trust and offshore structures will further enhance service scalability and investor confidence.

Major Players

- Maybank Private Wealth

- CIMB Private Banking

- Public Bank Private Banking

- RHB Private Banking

- Hong Leong Bank Private Banking

- OCBC Premier Private Client Malaysia

- UOB Private Bank Malaysia

- HSBC Global Private Banking Malaysia

- Standard Chartered Private Bank Malaysia

- BNP Paribas Wealth Management Malaysia

- Julius Baer Malaysia

- Kenanga Private Wealth

- Affin Hwang Investment Bank Wealth Management

- AmInvestment Bank Private Wealth

- Labuan IBFC Wealth Firms

Key Target Audience

Research Methodology

Step 1: Identification of Key Variables

Key wealth indicators including high-net-worth population, assets under management, portfolio allocation patterns, and advisory adoption were mapped across Malaysia’s banking and investment ecosystem. Regulatory frameworks and institutional capabilities were assessed to determine structural drivers shaping wealth management demand.

Step 2: Market Analysis and Construction

Primary financial disclosures from banks and regulators were synthesized with industry databases to estimate market size, segmentation, and competitive structure. Cross-border asset flows and Islamic finance positioning were integrated to construct Malaysia-specific wealth dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation of financial sector experts, investment professionals, and regulatory publications to confirm structural trends, segmentation relevance, and competitive positioning accuracy within Malaysia’s wealth ecosystem.

Step 4: Research Synthesis and Final Output

Validated insights were consolidated into market framework covering size, segmentation, competitive landscape, and outlook to produce a structured analytical view of Malaysia wealth management evolution and opportunity pathways.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising private wealth accumulation from diversified corporate ownership and capital market participation among Malaysian entrepreneurs and professionals

Expansion of Islamic wealth management attracting domestic and regional Sharia-compliant capital into structured investment products

Digital wealth platforms enabling scalable advisory reach to affluent and emerging wealth segments beyond traditional private banking hubs

Cross-border asset diversification demand among Malaysian high-net-worth clients seeking global portfolio exposure

Regulatory support for family offices and trust structures strengthening formal wealth preservation adoption - Market Challenges

Concentration of wealth within family-owned conglomerates limiting penetration of external discretionary wealth mandates

Regulatory complexity across onshore and offshore jurisdictions increasing compliance costs for wealth providers

Limited domestic alternative investment depth constraining portfolio diversification within Malaysia-based assets

Talent shortages in advanced portfolio advisory and family office structuring capabilities

Client preference for relationship-based banking reducing transition to fee-based advisory models - Market Opportunities

Development of Malaysia as a regional Islamic wealth management hub attracting Southeast Asian and Middle Eastern assets

Growth of family office structures among second-generation wealth holders seeking governance and succession planning

Expansion of digital hybrid advisory models targeting affluent mass investors transitioning toward professional wealth services - Trends

Increasing allocation to global equities and private markets among Malaysian high-net-worth portfolios

Integration of Sharia screening across mainstream wealth platforms and advisory mandates

Adoption of discretionary mandates replacing transactional brokerage relationships

Rise of digital onboarding and remote advisory across private banking clients

Growth of ESG-aligned portfolios within Malaysian wealth mandates - Government Regulations & Defense Policy

Strengthening of Labuan International Business and Financial Centre frameworks for offshore wealth structuring

Securities Commission Malaysia guidelines on digital investment management and robo-advisory licensing

Bank Negara Malaysia policies on wealth management suitability, risk profiling, and investor protection - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory Portfolio Management

Private Banking and Trust Services

Family Office and Estate Planning Solutions

Digital Wealth and Robo-Advisory Platforms - By Platform Type (In Value%)

Bank-Based Wealth Platforms

Independent Asset Management Firms

Securities Brokerage Wealth Platforms

Islamic Wealth Management Institutions

Digital-Only Wealth Platforms - By Fitment Type (In Value%)

Onshore Wealth Structures

Offshore Wealth Structures

Hybrid Onshore-Offshore Structures

Sharia-Compliant Wealth Structures

Trust and Foundation-Based Structures - By End User Segment (In Value%)

Ultra-High-Net-Worth Individuals

High-Net-Worth Individuals

Affluent Mass Segment

Family Offices and Business Owners

Institutional Private Clients

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Client Segment Focus, Sharia Capability, Digital Platform Sophistication, Cross-Border Structuring, Advisory Depth, Family Office Services, Product Breadth, Relationship Coverage, Regulatory Jurisdiction Reach)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Maybank Private Wealth

CIMB Private Banking

Public Bank Private Banking

RHB Private Banking

Hong Leong Bank Private Banking

OCBC Premier Private Client Malaysia

UOB Private Bank Malaysia

HSBC Global Private Banking Malaysia

Standard Chartered Private Bank Malaysia

BNP Paribas Wealth Management Malaysia

Julius Baer Malaysia

Kenanga Private Wealth

Affin Hwang Investment Bank Wealth Management

AmInvestment Bank Private Wealth

Labuan IBFC Wealth Management Firms

- Ultra-high-net-worth Malaysian families increasingly formalize governance through family offices and trust vehicles to manage intergenerational wealth transition

- High-net-worth entrepreneurs diversify from domestic real estate and corporate holdings into managed global portfolios via private banks

- Affluent professionals adopt digital hybrid wealth platforms as investable surplus rises with income growth and capital market participation

- Business-owning clients integrate corporate liquidity events into structured discretionary mandates and estate planning frameworks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Malaysia Wealth Management market manages approximately USD ~ billion in assets under management across private banking and advisory mandates. This reflects consolidated disclosures from Bank Negara Malaysia and Securities Commission Malaysia financial sector statistics.

Malaysia Wealth Management market is led by domestic banks such as Maybank and CIMB alongside global private banks including HSBC and UOB. These institutions collectively manage the majority of high-net-worth financial assets within Malaysia.

Malaysia Wealth Management market growth is supported by rising high-net-worth population and increasing allocation to managed portfolios. Digital advisory platforms and Islamic wealth solutions also expand participation across affluent investors.

Malaysia Wealth Management market is dominated by discretionary portfolio management with about 32% share of managed assets. Bank-based wealth platforms lead distribution with approximately 41% platform share nationwide.

Malaysia Wealth Management market acts as Southeast Asian Islamic wealth hub supported by Labuan international financial center. Cross-border Muslim wealth and regional investors use Malaysia for Sharia-compliant portfolio structuring.

Malaysia Wealth Management market digital platforms expand access to advisory services among affluent investors. Hybrid wealth models and online portfolio tools increase managed asset adoption across Malaysia’s financial sector.

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now