Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Nigeria AI Infrastructure market reached approximately USD ~ million based on a recent historical assessment, supported by expanding hyperscale data center investments and accelerated enterprise AI adoption across telecom, banking, and government digitalization programs. Public and private infrastructure spending, including national data center capacity expansion and cloud region deployments, continues to drive demand for AI compute servers, accelerators, and networking systems. Industry estimates from Nigerian Communications Commission and data center operators indicate strong capital inflows into AI-ready infrastructure across major metropolitan hubs.

Lagos dominates the Nigeria AI Infrastructure market due to concentration of commercial data centers, submarine cable landing stations, and headquarters of telecom operators and cloud providers. Abuja follows with government sovereign cloud and national data initiatives, while Ogun State and Rivers State attract edge and industrial AI deployments linked to manufacturing and energy sectors. These locations benefit from fiber connectivity corridors, reliable power clusters, and proximity to enterprise customers, enabling large-scale AI infrastructure installation and colocation expansion.

Market Segmentation

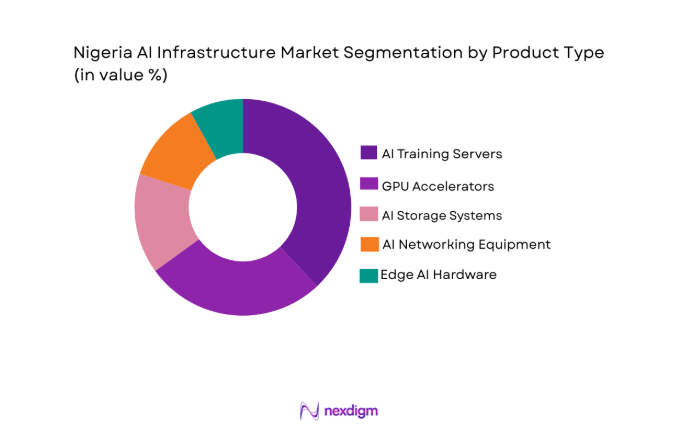

By Product Type

Nigeria AI Infrastructure market is segmented by product type into AI compute servers, GPU accelerators, AI storage systems, AI networking equipment, and edge AI hardware. Recently, AI compute servers has a dominant market share due to factors such as enterprise AI workload consolidation, hyperscale deployment patterns, vendor ecosystem maturity, and compatibility with data center infrastructure. Nigerian telecom operators, banks, and government cloud programs prioritize scalable server platforms capable of supporting AI training and inference workloads in centralized facilities. Availability of OEM partnerships and integrator support further strengthens adoption, while demand for high-density rack deployments favors compute-centric infrastructure procurement strategies across national data center expansions.

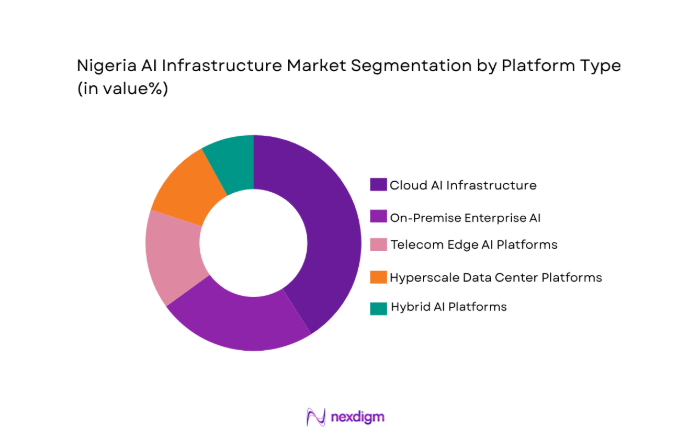

By Platform Type

Nigeria AI Infrastructure market is segmented by platform type into cloud AI infrastructure, on-premise enterprise AI, telecom edge AI platforms, hyperscale data center platforms, and hybrid AI platforms. Recently, cloud AI infrastructure has a dominant market share due to factors such as enterprise migration to cloud environments, hyperscale region entry, service scalability, and managed AI platform availability. Nigerian enterprises prefer cloud-based AI infrastructure to avoid capital expenditure and overcome power and cooling constraints associated with on-premise deployments. Telecom and fintech sectors particularly leverage cloud AI services for analytics, fraud detection, and digital service optimization, reinforcing platform dominance.

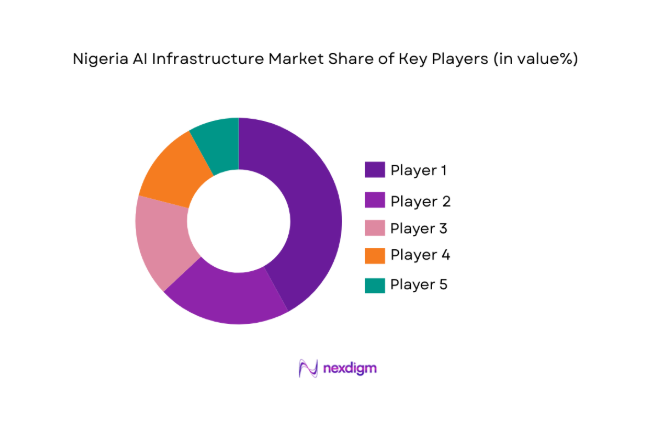

Competitive Landscape

Nigeria AI Infrastructure market shows moderate consolidation with a mix of global hyperscale cloud providers, telecom-owned data center operators, and regional infrastructure vendors shaping deployment standards and pricing dynamics. International technology firms supply core AI hardware and cloud platforms, while local operators dominate colocation and sovereign infrastructure projects. Strategic partnerships between telecom companies and global cloud providers accelerate hyperscale expansion and edge deployment coverage across urban corridors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Data Center Capacity |

| MTN Nigeria | 2001 | Lagos | ~ | ~ | ~ | ~ | ~ |

| MainOne | 2010 | Lagos | ~ | ~ | ~ | ~ | ~ |

| Rack Centre | 2012 | Lagos | ~ | ~ | ~ | ~ | ~ |

| Huawei Technologies | 1987 | Shenzhen | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond | ~ | ~ | ~ | ~ | ~ |

Nigeria AI Infrastructure Market Analysis

Growth Drivers

National Digital Economy and AI Adoption Programs

Nigeria’s national digital economy agenda has accelerated demand for AI infrastructure by prioritizing cloud computing, data sovereignty, and artificial intelligence deployment across public and private sectors, creating structural momentum for large-scale infrastructure investments. Government digital identity, fintech expansion, and e-governance platforms require high-performance compute environments capable of handling large datasets and analytics workloads, driving procurement of AI servers and accelerators. Telecom operators and banks align with national strategies by deploying AI-enabled customer analytics, fraud detection, and network optimization systems, further expanding infrastructure requirements. Hyperscale cloud providers entering the Nigerian market respond to policy incentives encouraging local data hosting and digital service localization, resulting in new data center construction and AI-ready capacity installations. Public sector cloud initiatives and sovereign data platforms increase centralized AI compute demand, encouraging public-private partnerships and colocation growth. Enterprise digital transformation across finance, retail, energy, and logistics sectors generates sustained AI workload growth, requiring scalable compute clusters and high-performance storage infrastructure. Domestic startup ecosystems focused on fintech and AI analytics create incremental demand for GPU-accelerated cloud platforms and AI services infrastructure. Infrastructure investors view Nigeria as a regional digital hub due to population scale and connectivity growth, directing capital into AI-capable data centers and edge networks. Expansion of submarine cable capacity and fiber backbones enhances data flow volumes, strengthening economic justification for AI infrastructure deployment nationwide.

Hyperscale Data Center and Cloud Region Expansion

Hyperscale cloud and colocation expansion within Nigeria significantly increases AI infrastructure demand by enabling localized high-performance computing environments for enterprises and government agencies requiring low-latency AI processing. Lagos has emerged as a hyperscale cluster due to submarine cable landings and enterprise concentration, attracting investments from global cloud providers and data center developers building AI-ready facilities with high rack densities. Cloud service providers deploy GPU-enabled compute clusters to support analytics, machine learning, and AI application hosting for Nigerian enterprises transitioning from on-premise systems. Telecom companies partner with cloud vendors to deliver edge AI capabilities integrated with 5G and broadband networks, extending infrastructure deployment beyond central data centers. Colocation providers expand capacity to host AI workloads from fintech, media, and digital services firms requiring scalable compute without capital investment. Modular data center construction techniques enable faster AI infrastructure rollout across emerging commercial hubs. Increased regional cloud adoption across West Africa positions Nigeria as a hosting location for cross-border AI services, further driving infrastructure capacity requirements. Enterprise migration to hybrid cloud models necessitates interconnected AI compute environments linking on-premise and cloud platforms, increasing networking and accelerator deployments. Availability of hyperscale AI infrastructure locally reduces latency and compliance risks, encouraging domestic AI application development and reinforcing infrastructure growth.

Market Challenges

Power Reliability Constraints for High Density AI Infrastructure

Nigeria’s inconsistent power supply presents a structural challenge for AI infrastructure deployment because high-density compute clusters require uninterrupted electricity and advanced cooling systems to operate reliably. Data center operators must invest heavily in backup generation, energy storage, and redundant power architecture to maintain uptime for AI workloads, significantly increasing capital and operating costs. AI servers and GPU clusters consume substantially more energy than conventional IT systems, intensifying exposure to grid instability and fuel price volatility affecting diesel-based backup generation. Cooling requirements for dense AI racks further elevate energy consumption and infrastructure complexity, requiring specialized thermal management systems and resilient facility design. Enterprises considering on-premise AI deployments often avoid investment due to uncertainty around power reliability, shifting demand toward cloud providers but constraining broader infrastructure diversification. Power constraints also limit geographic expansion of AI facilities beyond major urban energy clusters, slowing nationwide infrastructure distribution. Data center developers must negotiate independent power arrangements or captive generation projects, extending project timelines and financing requirements. Renewable energy integration remains limited in high-density computing facilities, restricting sustainable AI infrastructure growth. Overall energy reliability challenges elevate cost per compute unit and hinder rapid scaling of AI infrastructure across Nigeria.

Limited Domestic Hardware Manufacturing and Skilled Workforce

Nigeria lacks a domestic ecosystem for advanced AI hardware manufacturing and specialized infrastructure engineering, resulting in heavy dependence on imported servers, accelerators, networking equipment, and technical expertise. Import reliance increases costs through tariffs, logistics expenses, and foreign exchange exposure, making AI infrastructure procurement financially challenging for local enterprises and operators. Maintenance and lifecycle management of complex AI systems require skilled engineers in high-performance computing, cooling design, and accelerator optimization, yet talent availability remains limited within the national workforce. Infrastructure deployment projects often rely on foreign vendors and integrators, raising operational costs and reducing technology localization benefits. Training programs for AI infrastructure engineering are still emerging, creating a gap between infrastructure expansion and technical capability development. Limited domestic semiconductor or hardware assembly capability prevents local cost optimization and supply chain resilience. Small and medium enterprises face barriers adopting AI infrastructure due to lack of technical expertise to manage advanced compute environments. Talent shortages also affect regulatory and policy capacity to oversee complex AI infrastructure ecosystems. Dependence on external vendors slows technology transfer and reduces domestic value capture from AI infrastructure investments.

Opportunities

Localized Edge AI Infrastructure for Telecom and Smart Cities

Expansion of edge AI infrastructure across Nigerian urban and industrial corridors presents a major opportunity because telecom networks and smart city systems require distributed compute capabilities close to data sources. Telecom operators deploying 5G and fiber broadband infrastructure can integrate edge AI nodes within network facilities to support real-time analytics, traffic optimization, and intelligent service delivery across cities. Smart surveillance, transportation management, and utility monitoring applications demand localized AI processing to reduce latency and bandwidth consumption, encouraging deployment of compact edge compute clusters. Industrial zones in Lagos, Ogun, and Rivers states offer environments for edge AI supporting manufacturing automation and energy monitoring. Edge deployments reduce dependency on centralized data centers, enabling scalable AI adoption across diverse sectors. Telecom infrastructure ownership provides a ready platform for AI hardware installation at base stations and aggregation sites. Government smart city initiatives stimulate procurement of distributed AI systems integrated with urban infrastructure. Enterprises benefit from localized processing for IoT analytics and operational intelligence applications. Edge AI infrastructure growth broadens market participation beyond hyperscale data centers, diversifying revenue streams for infrastructure providers.

Sovereign Cloud and National Data Infrastructure Development

Nigeria’s push toward sovereign cloud and national data infrastructure offers significant opportunity for domestic AI infrastructure expansion as government and regulated sectors prioritize local data hosting and processing capabilities. National digital identity, financial regulation, and public service platforms require secure domestic AI compute environments compliant with data localization requirements. Government investments in national data centers create anchor demand for AI servers, storage, and networking infrastructure integrated with sovereign cloud platforms. Local cloud providers and telecom operators can partner with government agencies to deliver AI-enabled services hosted within national boundaries. Sovereign infrastructure reduces reliance on foreign cloud hosting and strengthens data governance frameworks. Public sector procurement stimulates domestic infrastructure ecosystem development including colocation, cloud services, and integrator networks. National data infrastructure supports AI innovation ecosystems by providing compute access to startups and research initiatives. Regulated industries such as banking and healthcare prefer sovereign AI platforms for compliance and security assurance. Sovereign cloud initiatives position Nigeria as a regional AI hosting hub for West African markets, expanding infrastructure demand.

Future Outlook

Nigeria AI Infrastructure market is expected to expand steadily over the next five years driven by hyperscale data center construction, sovereign cloud programs, and enterprise AI adoption across telecom and finance sectors. Increasing submarine cable capacity and fiber backbones will enable larger AI workloads and distributed edge deployments. Government digital economy initiatives and data localization policies will stimulate domestic AI infrastructure investment. Cooling innovation and modular data center designs are likely to improve deployment efficiency and scalability nationwide.

Major Players

- MTN Nigeria

- MainOne

- Rack Centre

- Equinix

- Huawei Technologies

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- NVIDIA

- Microsoft

- Amazon Web Services

- Google Cloud

- Zinox Technologies

- Layer3

- Galaxy Backbone

Key Target Audience

- Telecom operators

- Cloud service providers

- Data center operators

- Financial institutions

- Government and regulatory bodies

- Technology investors

- Venture capital firms

- Enterprise IT infrastructure buyers

Research Methodology

Step 1: Identification of Key Variables

Key variables including AI compute capacity, data center investments, cloud adoption levels, and sectoral demand drivers were identified through industry databases, regulatory publications, and infrastructure investment disclosures. Supply-side and demand-side indicators were mapped to Nigeria’s digital economy context to establish analytical boundaries.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using infrastructure capacity data, company financial disclosures, procurement trends, and AI workload adoption patterns across telecom, finance, and government sectors. Cross-validation was conducted using operator announcements and technology vendor shipment indicators.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultation with data center engineers, telecom infrastructure planners, and cloud deployment specialists to confirm adoption drivers, deployment models, and technical constraints influencing Nigeria AI infrastructure demand dynamics.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into structured market estimates, segmentation frameworks, and strategic analysis ensuring consistency with infrastructure investment flows, technology adoption patterns, and national digitalization policies shaping Nigeria AI infrastructure evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid telecom network expansion and 5G readiness initiatives

National digital economy and AI adoption strategies

Growth of cloud services and hyperscale data centers

Rising enterprise demand for data analytics and automation

Government smart infrastructure and e governance programs - Market Challenges

Unreliable power supply affecting data center operations

Limited domestic semiconductor and hardware ecosystem

High capital cost of advanced AI infrastructure imports

Connectivity bottlenecks outside major urban hubs

Shortage of skilled AI infrastructure engineers - Market Opportunities

Localized edge AI deployments for telecom and smart cities

AI infrastructure for fintech and digital banking growth

Public private partnerships in national data centers - Trends

Shift toward GPU dense and accelerator based computing

Adoption of modular and containerized AI data centers

Integration of AI workloads into telecom edge networks

Increased use of liquid cooling in high density racks

Hybrid cloud AI infrastructure adoption by enterprises - Government Regulations & Defense Policy

National AI strategy and digital economy policy frameworks

Data localization and sovereign cloud initiatives

Cybersecurity and critical infrastructure protection laws - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Compute Servers

GPU Accelerated Data Center Infrastructure

AI Storage Systems

AI Networking and Interconnect Solutions

Edge AI Processing Systems - By Platform Type (In Value%)

Cloud AI Infrastructure

On Premise Enterprise AI Infrastructure

Telecom Network Edge AI Platforms

Hyperscale Data Center Platforms

Hybrid AI Infrastructure Platforms - By Fitment Type (In Value%)

New AI Data Center Deployments

Retrofit AI Upgrades in Existing Data Centers

Edge Node Installations

Embedded AI Infrastructure in Telecom Sites

Modular Containerized AI Infrastructure - By End User Segment (In Value%)

Telecommunications Providers

Financial Services Institutions

Government and Smart City Programs

Energy and Utilities Operators

Healthcare and Research Institutions - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrator Contracts

Cloud Service Provider Partnerships

Government Tenders and Public Projects

Value Added Reseller Networks - By Material / Technology (in Value %)

Advanced GPUs and AI Accelerators

High Performance CPUs

Silicon Photonics Interconnects

NVMe and High Speed Flash Storage

Liquid Cooling and Thermal Management Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Compute Performance, Energy Efficiency, Scalability, Deployment Model Flexibility, Cooling Technology, Interconnect Bandwidth, Local Support Capability, Security Compliance, Total Cost of Ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

MTN Nigeria

MainOne

Rack Centre

Equinix

Huawei Technologies

Dell Technologies

Hewlett Packard Enterprise

Lenovo

NVIDIA

Microsoft Azure

Amazon Web Services

Google Cloud

Zinox Technologies

Layer3

Galaxy Backbone

- Telecom operators deploying edge AI for network optimization and services

- Banks investing in AI infrastructure for fraud detection and analytics

- Government agencies building sovereign data and AI platforms

- Enterprises adopting AI compute for automation and decision intelligence

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now