Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Nigeria’s car finance market represents a critical segment of the country’s automotive ecosystem, enabling vehicle ownership through structured lending products provided by banks, financial institutions, and specialized auto finance companies. A recent historical assessment indicates that the Nigeria car finance market is valued at approximately USD ~ billion, based on vehicle loan portfolio data published by the Central Bank of Nigeria and automotive financing statistics compiled by the National Bureau of Statistics. Market growth is driven by rising vehicle demand, expanding middle-income populations, and increasing availability of structured auto lending products offered by financial institutions.

Lagos, Abuja, and Port Harcourt dominate the Nigeria car finance market due to strong automobile demand, higher household income levels, and concentration of financial institutions offering vehicle financing services. Lagos leads the market because of its large urban population, corporate workforce, and extensive vehicle dealership networks. Abuja benefits from government employment and stable income demographics supporting vehicle ownership, while Port Harcourt’s oil and gas industry workforce drives demand for financed personal and commercial vehicles.

Market Segmentation

By Vehicle Type

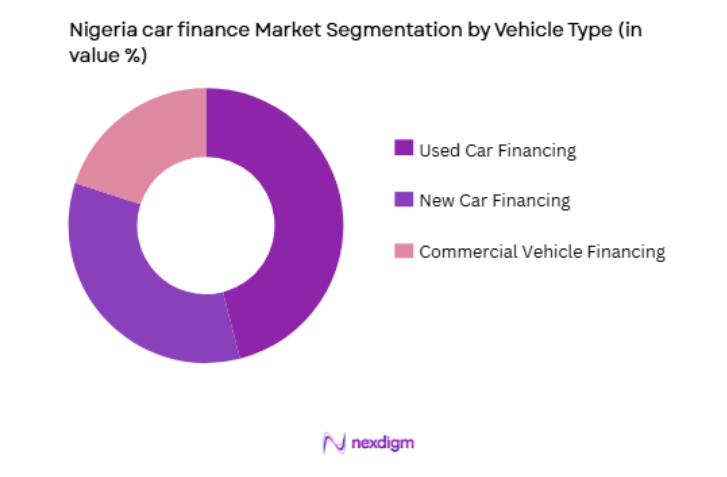

Nigeria car finance Market Outlook to 2035 market is segmented by product type into new car financing, used car financing, and commercial vehicle financing. Recently, used car financing has a dominant market share due to factors such as affordability considerations, strong supply of imported used vehicles, and higher consumer demand for lower purchase price vehicles. Nigeria’s automotive market relies heavily on imported used vehicles, making financing solutions for pre-owned cars particularly relevant for consumers seeking vehicle ownership within limited budgets. Financial institutions increasingly provide structured loan products specifically designed for used car purchases with flexible repayment schedules. Additionally, ride-hailing drivers, small businesses, and logistics operators frequently finance used vehicles to minimize upfront investment costs while still obtaining reliable transportation assets. As vehicle affordability remains a critical factor for many consumers across Nigeria’s urban markets, used car financing continues to represent the dominant segment within the country’s expanding automotive finance ecosystem.

By Financing Provider

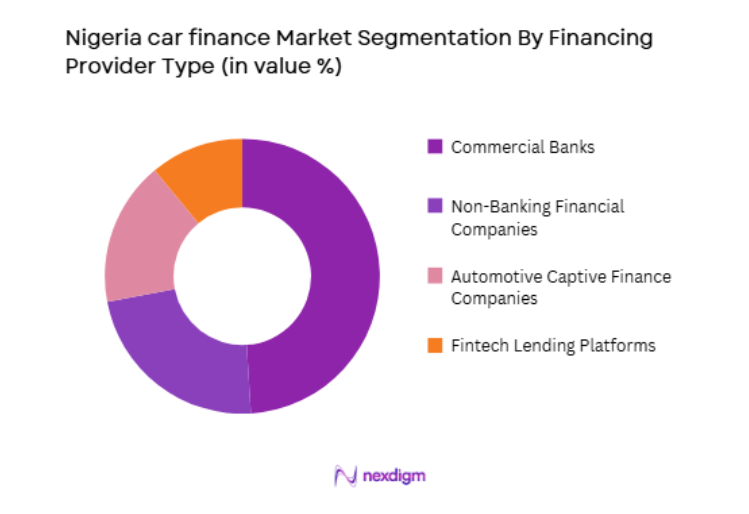

Nigeria car finance Market is segmented by Financing Provider into commercial banks, non-banking financial companies, automotive captive finance companies, and fintech lending platforms. Recently, commercial banks have a dominant market share due to factors such as stronger capital availability, established lending frameworks, and widespread branch networks capable of serving customers across the country. Major Nigerian banks offer structured vehicle loan programs that allow individuals and corporate clients to finance automobile purchases with defined repayment schedules. Banks also collaborate with automobile dealerships to provide point-of-sale financing solutions for vehicle buyers. Additionally, corporate fleet operators and government agencies often rely on bank financing to procure vehicles through institutional lending programs. The established reputation and regulatory oversight associated with commercial banks further strengthens consumer confidence in bank-based vehicle financing products, ensuring their continued dominance in Nigeria’s car finance ecosystem.

Competitive Landscape

The Nigeria car finance market is moderately consolidated with participation from commercial banks, leasing companies, and specialized automotive finance providers. Major Nigerian financial institutions dominate the market by offering structured vehicle loan products supported by strong capital resources and nationwide branch networks. Automotive finance subsidiaries and fintech lenders are also expanding their presence through digital lending platforms and partnerships with automobile dealerships to simplify vehicle financing for consumers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Loan Tenure |

| First Bank of Nigeria | 1894 | Nigeria | ~ | ~ | ~ | ~ | ~ |

| Access Bank | 1989 | Nigeria | ~ | ~ | ~ | ~ | ~ |

| Stanbic IBTC Bank | 1989 | Nigeria | ~ | ~ | ~ | ~ | ~ |

| United Bank for Africa | 1949 | Nigeria | ~ | ~ | ~ | ~ | ~ |

| Zenith Bank | 1990 | Nigeria | ~ | ~ | ~ | ~ | ~ |

Nigeria car finance Market Analysis

Growth Drivers

Expansion of Consumer Credit Access and Retail Banking Penetration

Nigeria’s expanding retail banking sector and increasing accessibility of consumer credit products are significantly driving growth within the country’s car finance market as financial institutions develop new lending solutions designed to support automobile purchases for a growing population of urban consumers seeking personal mobility. Banks and financial service providers are introducing flexible vehicle financing programs that allow customers to spread the cost of car purchases over extended repayment periods, making vehicle ownership more accessible for middle-income households. Rising employment levels in urban centers and increasing disposable income among salaried professionals further contribute to the demand for auto financing services. Financial institutions also partner with automobile dealerships to offer point-of-sale vehicle financing that simplifies the purchasing process for consumers. Digital banking platforms enable lenders to process loan applications more efficiently while improving accessibility to credit products for customers who may not previously have had access to traditional bank financing. As Nigeria’s banking infrastructure continues to expand and financial inclusion initiatives encourage more individuals to participate in formal banking systems, demand for car financing solutions is expected to increase significantly across both private and commercial vehicle segments.

Growth of Ride-Hailing Platforms and Commercial Mobility Services

The rapid expansion of ride-hailing platforms and app-based transportation services across Nigeria’s major cities has created significant demand for vehicle financing solutions that enable drivers to acquire vehicles used for commercial transportation services. Platforms operating within the ride-hailing ecosystem rely heavily on drivers who must purchase or lease vehicles capable of meeting platform operational standards. Many drivers lack the financial resources required to purchase vehicles outright, making car financing programs an essential mechanism enabling participation in the ride-hailing economy. Financial institutions and mobility platforms increasingly collaborate to provide specialized financing packages designed specifically for ride-hailing drivers. These financing models often incorporate flexible repayment structures that align with driver income patterns generated through platform operations. Additionally, logistics and delivery services supporting e-commerce growth across Nigeria also rely heavily on financed vehicles for commercial operations. As the gig economy expands and digital mobility platforms attract more participants seeking income opportunities, the demand for vehicle financing products supporting commercial transportation services is expected to continue expanding across the Nigerian car finance market.

Market Challenges

High Interest Rates and Credit Risk Concerns in Vehicle Financing

One of the primary challenges affecting the Nigeria car finance market is the relatively high interest rate environment combined with credit risk concerns faced by lenders providing automobile loans to consumers and small business operators. Financial institutions must evaluate borrower creditworthiness carefully due to economic volatility and income uncertainty affecting many consumers. Higher perceived credit risk leads lenders to apply stricter lending criteria and higher interest rates in order to offset potential loan default risks. These financing costs can discourage potential borrowers who may find vehicle loans less affordable compared with purchasing vehicles through alternative methods such as informal financing or outright cash purchases. Additionally, fluctuations in macroeconomic conditions and currency exchange rates affecting vehicle import costs can increase the overall price of automobiles, further influencing loan affordability for consumers. Lenders must also account for vehicle depreciation risks when structuring loan agreements. Addressing these credit risk challenges requires improved credit assessment tools, stronger financial inclusion initiatives, and development of alternative financing models capable of supporting a broader range of borrowers across Nigeria’s evolving automotive market.

Limited Domestic Automotive Manufacturing and Dependence on Imported Vehicles

Nigeria’s automotive market remains heavily dependent on imported vehicles, which creates structural challenges for car financing providers due to fluctuating import costs, supply chain disruptions, and currency exchange rate volatility affecting vehicle pricing. The majority of vehicles purchased in Nigeria are imported either as new vehicles or used automobiles, meaning financing institutions must account for potential fluctuations in vehicle value associated with currency movements and international trade dynamics. Import duties and regulatory changes affecting vehicle imports can also influence automobile pricing and market demand, creating uncertainty for lenders planning long-term vehicle financing programs. Limited domestic automotive manufacturing capacity further constrains the ability of the local market to stabilize vehicle prices or ensure consistent vehicle supply. Without a strong domestic automotive production ecosystem, the cost structure of vehicle purchases remains closely linked to international markets and foreign exchange conditions. These structural dependencies introduce additional complexity for financial institutions seeking to develop sustainable car financing solutions within Nigeria’s automotive ecosystem.

Opportunities

Expansion of Digital Lending Platforms and Fintech-Based Vehicle Financing Solutions

The rapid growth of financial technology innovation across Nigeria presents significant opportunities for expanding car financing accessibility through digital lending platforms designed to streamline loan applications, credit assessment, and approval processes for vehicle buyers. Fintech companies are leveraging mobile banking technologies and digital identity verification tools to simplify credit evaluation and reduce loan processing times for consumers seeking vehicle financing solutions. Digital platforms allow borrowers to compare financing options, submit loan applications online, and receive approval decisions more quickly than traditional bank lending channels. Such technological innovation improves accessibility for customers located outside major urban banking centers and expands the reach of vehicle financing services across a broader population. Fintech-driven lending models can also incorporate alternative credit scoring methodologies using digital transaction data, enabling lenders to evaluate borrowers who may not have extensive traditional credit histories. As smartphone adoption and digital banking penetration continue expanding across Nigeria, fintech-based vehicle financing platforms are expected to play an increasingly important role in supporting growth within the country’s car finance market.

Development of Automotive Leasing and Subscription-Based Vehicle Ownership Models

Emerging vehicle leasing and subscription-based mobility models present a significant opportunity for transforming the Nigeria car finance market by offering consumers flexible alternatives to traditional vehicle ownership financing structures. Leasing programs allow customers to access vehicles for defined periods while paying monthly usage fees rather than committing to long-term purchase loans. Subscription-based vehicle services further expand this concept by offering bundled packages that include insurance, maintenance, and vehicle replacement options. Such mobility solutions can be particularly attractive to urban professionals and commercial drivers who prefer flexibility rather than permanent vehicle ownership. Automotive leasing companies and mobility service providers partnering with financial institutions can create innovative financing ecosystems that combine vehicle access with structured payment solutions. These models reduce the financial risk associated with vehicle ownership while providing consumers with greater mobility flexibility. As Nigeria’s urban mobility landscape continues evolving and digital mobility platforms expand, leasing and subscription-based financing models are expected to create new growth opportunities within the car finance market.

Future Outlook

Nigeria’s car finance market is expected to experience steady expansion over the next five years as vehicle ownership demand increases and financial institutions continue expanding consumer lending products. Digital banking technologies and fintech innovation will improve access to vehicle financing services for a wider population. Government policies supporting automotive industry development and financial inclusion will further strengthen market growth. Increasing adoption of ride-hailing services and commercial mobility platforms will also continue to stimulate demand for vehicle financing solutions.

Major Players

- First Bank of Nigeria

- Access Bank

- Stanbic IBTC Bank

- United Bank for Africa

- Zenith Bank

- Guaranty Trust Bank

- Fidelity Bank Nigeria

- Ecobank Nigeria

- Union Bank of Nigeria

- Wema Bank

- Standard Chartered Nigeria

- Toyota Financial Services

- Hyundai Capital

- Kia Motors Finance

- ALAT by Wema Bank

Key Target Audience

- Automotive Dealership Networks

- Vehicle Leasing Companies

- Commercial Fleet Operators

- Ride-Hailing Platform Operators

- Digital Lending Platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive Importers

Research Methodology

Step 1: Identification of Key Variables

Key market variables such as vehicle ownership trends, consumer credit availability, automotive import statistics, and banking sector lending activity are identified to understand structural drivers influencing the Nigeria car finance market.

Step 2: Market Analysis and Construction

Data collected from financial institution reports, automotive industry publications, and national economic statistics is analyzed to construct market segmentation and identify demand patterns influencing vehicle financing adoption.

Step 3: Hypothesis Validation and Expert Consultation

Financial industry experts, banking professionals, automotive dealers, and mobility sector analysts are consulted to validate assumptions regarding lending behavior, consumer demand, and financing trends shaping the Nigeria car finance market.

Step 4: Research Synthesis and Final Output

Validated insights are synthesized into structured research outputs covering competitive landscape, segmentation, growth drivers, and long-term opportunities influencing the Nigeria car finance market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising urban vehicle ownership supported by expanding middle income population

Growth of digital lending platforms improving access to vehicle financing

Expansion of ride hailing and mobility services increasing financed vehicle purchases - Market Challenges

High interest rates and credit risk associated with consumer lending

Limited credit history and financial inclusion among large population segments

Currency volatility affecting vehicle import costs and financing affordability - Market Opportunities

Development of digital auto financing platforms with faster loan approvals

Partnerships between automobile dealers and financial institutions

Expansion of financing products for used vehicles and commercial fleets - Trends

Adoption of digital loan origination and automated credit scoring systems

Growing role of fintech companies in vehicle financing services - Government Regulations

Central Bank of Nigeria lending guidelines affecting consumer credit

Financial regulations governing banking and non banking lending institutions

Policies supporting financial inclusion and digital financial services - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

New Vehicle Financing

Used Vehicle Financing

Lease Financing

Hire Purchase Financing

Balloon Payment Financing - By Platform Type (In Value%)

Bank Based Auto Loans

Non Banking Financial Company Auto Loans

Digital Lending Platforms

Dealer Based Financing Platforms

Peer to Peer Vehicle Financing Platforms - By Fitment Type (In Value%)

Direct Bank Financing

Dealer Integrated Financing

Online Marketplace Financing

Third Party Financial Brokerage - By End User Segment (In Value%)

Individual Vehicle Buyers

Corporate Fleet Buyers

Ride Hailing Drivers

- Market Share Analysis

- Cross Comparison Parameters (Interest Rate Structure, Loan Tenure Options, Down Payment Requirement, Credit Approval Time, Digital Loan Processing Capability, Credit Score Requirements, Loan to Value Ratio, Early Repayment Penalties)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Access Bank

Guaranty Trust Bank

Zenith Bank

First Bank of Nigeria

United Bank for Africa

Fidelity Bank Nigeria

Stanbic IBTC Bank

FCMB Group

Wema Bank

Union Bank Nigeria

Toyota Financial Services

Autochek Africa

Cars45 Finance

Moove Africa

Carbon Finance

- Individual buyers increasingly relying on financing options to purchase vehicles

- Corporate fleets adopting structured financing for vehicle procurement

- Ride hailing drivers using auto loans to enter mobility service platforms

- Small businesses financing vehicles for logistics and service operations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now