Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Nigeria’s cloud infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by accelerated enterprise digitalization, expansion of hyperscale and carrier-neutral data centers, and rising demand for localized secure hosting environments. Investments from global cloud providers and telecom operators expanded capacity across compute, storage, and networking layers, while fintech and digital services growth increased workload migration to cloud platforms. Regulatory emphasis on data sovereignty and cybersecurity further strengthened enterprise and government adoption of domestic cloud infrastructure.

Lagos dominates the market due to concentration of submarine cable landing stations, major carrier-neutral data centers, and headquarters of telecom operators, financial institutions, and digital firms that generate high cloud demand. Abuja follows with strong government cloud and sovereign infrastructure deployments supported by national ICT policies and public sector digitization programs. Port Harcourt and Kano are emerging nodes as regional enterprises adopt hybrid cloud services and telecom operators extend edge and metro data center presence to improve latency and service resilience nationwide.

Market Segmentation

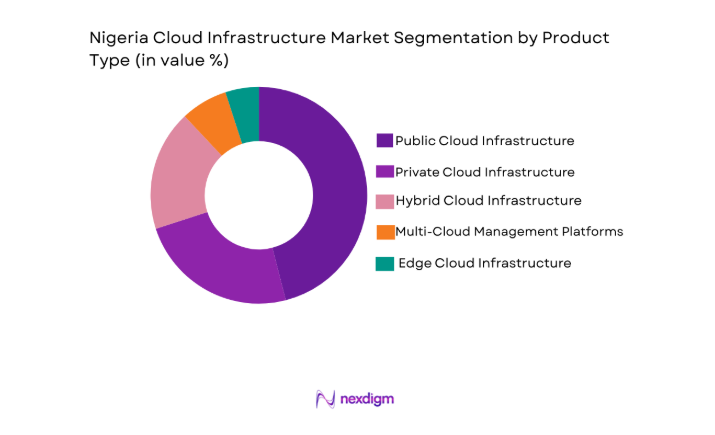

By Product Type

Nigeria Cloud Infrastructure market is segmented by product type into Public Cloud Infrastructure, Private Cloud Infrastructure, Hybrid Cloud Infrastructure, Multi Cloud Management Systems, and Edge Cloud Infrastructure. Recently, Public Cloud Infrastructure has a dominant market share due to factors such as scalable on-demand capacity, strong presence of hyperscale providers, mature data center ecosystems in Lagos, and enterprise preference for cost-efficient outsourced infrastructure. Telecom integration and managed services partnerships also accelerate public cloud adoption across banking, fintech, and digital service sectors nationwide.

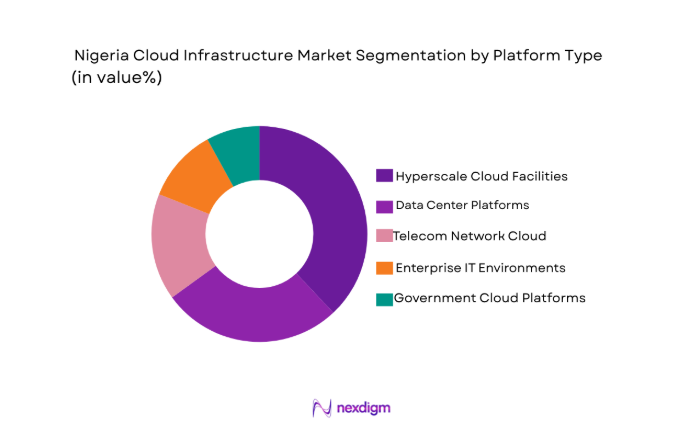

By Platform Type

Nigeria Cloud Infrastructure market is segmented by platform type into Data Center Platforms, Telecom Network Cloud, Enterprise IT Environments, Government Cloud Platforms, and Hyperscale Cloud Facilities. Recently, Hyperscale Cloud Facilities has a dominant market share due to factors such as large-scale capacity deployment by global providers, concentration of carrier-neutral colocation hubs, high enterprise workload density, and strong connectivity to submarine cable systems. Hyperscale environments enable scalable compute clusters, AI-ready infrastructure, and multi-tenant hosting supporting nationwide cloud service delivery.

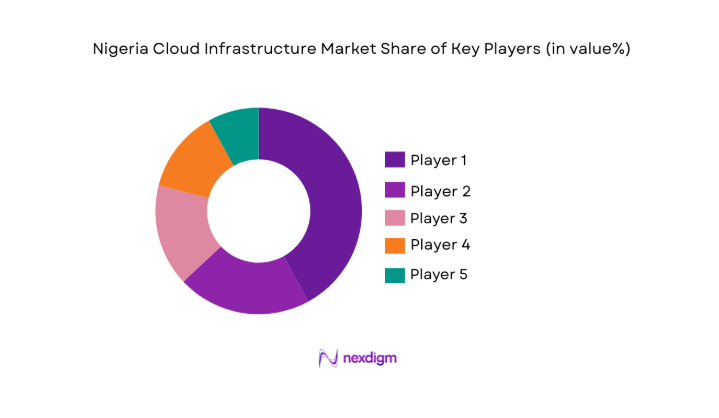

Competitive Landscape

Nigeria’s cloud infrastructure market shows moderate consolidation with global hyperscale providers and regional data center operators controlling core capacity while telecom operators and managed service firms expand hybrid and edge offerings. Strategic partnerships between hyperscalers, carriers, and colocation providers shape competitive positioning. Domestic firms compete through localized services and compliance-aligned hosting, whereas multinational providers leverage scale, advanced platforms, and ecosystem reach to influence enterprise and government cloud adoption.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Data Center Capacity |

| Amazon Web Services | 2006 | United States | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | United States | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | United States | ~ | ~ | ~ | ~ | ~ |

| MainOne | 2010 | Nigeria | ~ | ~ | ~ | ~ | ~ |

| Rack Centre | 2013 | Nigeria | ~ | ~ | ~ | ~ | ~ |

Nigeria Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Cloud Migration Acceleration

Nigeria’s enterprise technology landscape is undergoing structural transformation as organizations migrate legacy IT workloads to scalable cloud environments to improve operational efficiency, service agility, and resilience across distributed operations, creating sustained demand for infrastructure-as-a-service and platform-based deployment models nationwide. Financial institutions, fintech platforms, telecommunications operators, and e-commerce ecosystems increasingly require elastic compute and storage resources capable of supporting real-time transactions, digital channels, and data analytics, pushing enterprises toward outsourced cloud infrastructure instead of capital-intensive on-premise data centers. Rapid growth in mobile broadband penetration and digital service consumption has expanded user-generated data volumes, compelling enterprises to deploy cloud-based data processing, application hosting, and disaster recovery architectures that can scale dynamically with demand fluctuations. Cloud adoption also reduces infrastructure management complexity, enabling organizations to redirect technical resources toward innovation, product development, and customer experience rather than physical hardware maintenance and upgrades. Multinational cloud providers entering Nigeria with localized regions and partnerships have improved trust, compliance alignment, and service reliability, encouraging regulated sectors such as banking and government agencies to shift mission-critical workloads to domestic cloud platforms. Hybrid and multi-cloud architectures are gaining traction because enterprises require interoperability between private environments and public hyperscale platforms, stimulating demand for integration services, orchestration tools, and high-capacity interconnection infrastructure. Cost optimization is another powerful driver, as pay-as-you-use cloud pricing models allow Nigerian firms to align IT spending with business activity cycles instead of committing to large upfront infrastructure investments that strain capital budgets. Competitive pressure across industries is intensifying digital transformation initiatives, and companies without scalable digital infrastructure risk losing market relevance, further accelerating migration to cloud-based operational foundations across sectors. Government digitization initiatives and regulatory frameworks promoting secure data localization also reinforce enterprise confidence in domestic cloud ecosystems, making cloud infrastructure a strategic enabler of Nigeria’s broader digital economy transition.

Hyperscale Data Center Expansion and Connectivity Infrastructure Growth

Nigeria’s position as West Africa’s primary digital connectivity hub is strengthening through continuous expansion of hyperscale and carrier-neutral data centers interconnected with multiple submarine cable systems, creating the physical foundation required for large-scale cloud infrastructure deployment across the region. Lagos hosts major cable landing stations linking international bandwidth corridors to domestic fiber backbones, enabling low-latency access to global cloud networks and supporting the establishment of high-density data center campuses capable of housing hyperscale compute clusters. Global cloud providers and colocation operators are investing in modular data center expansions and advanced cooling, power, and redundancy architectures that allow efficient hosting of AI-ready servers and high-performance storage arrays demanded by enterprise and digital platforms. Telecom operators are integrating network virtualization and cloud-native core infrastructure within these facilities, enabling convergence of telecom cloud and enterprise cloud workloads while improving network performance and service availability nationwide. The growth of content delivery networks, streaming platforms, and digital media services also requires localized caching and compute nodes, reinforcing demand for hyperscale facilities with robust interconnection ecosystems linking carriers, internet exchanges, and service providers. As enterprises increasingly adopt hybrid cloud strategies, proximity to hyperscale hubs reduces latency and bandwidth costs, making domestic data center infrastructure strategically valuable for application performance and user experience. Energy infrastructure upgrades and private power generation within data center campuses are improving reliability, addressing historical power constraints and enabling continuous high-availability operations required by cloud platforms. Regional enterprises from neighboring West African markets are colocating workloads in Nigerian facilities due to connectivity advantages and ecosystem maturity, positioning the country as a regional cloud hosting center. These structural connectivity and infrastructure developments collectively accelerate hyperscale deployment cycles and create a reinforcing loop in which expanded data center capacity attracts additional cloud providers, platforms, and enterprise workloads into Nigeria’s cloud infrastructure ecosystem.

Market Challenges

Power Reliability Constraints for Large-Scale Cloud Infrastructure Operations

Nigeria’s national electricity grid instability and frequent outages present a structural constraint for cloud infrastructure providers that require uninterrupted power supply to maintain data center uptime, service reliability, and compliance with stringent service level agreements expected by enterprise and government customers. Hyperscale and carrier-neutral data centers rely heavily on diesel generators, battery systems, and redundant power architectures to ensure continuous operation, significantly increasing operational expenditures and infrastructure complexity compared with markets that possess stable utility grids. Fuel logistics, maintenance costs, and environmental considerations associated with backup generation systems reduce profitability margins for data center operators and cloud providers, potentially increasing service pricing for enterprise customers and slowing adoption among cost-sensitive organizations. Intermittent power also introduces risk to smaller regional facilities and edge deployments that may lack large-scale redundancy infrastructure, limiting expansion of distributed cloud architectures beyond major urban hubs such as Lagos and Abuja. Sustainable energy integration is challenging because renewable power infrastructure and grid-scale storage solutions remain underdeveloped, constraining the ability of cloud operators to transition toward greener and more cost-efficient energy sources. High power costs can deter international hyperscale providers from aggressive capacity expansion, as energy availability and pricing directly influence data center site selection decisions in global infrastructure planning. Enterprises considering private or hybrid cloud deployments face similar challenges in maintaining reliable on-premise or colocation-based infrastructure, reinforcing dependence on a limited number of large facilities capable of guaranteeing uptime. Power instability also affects cooling systems and environmental control mechanisms essential for maintaining optimal server performance and hardware longevity, raising operational risk and maintenance requirements. Without sustained national energy infrastructure improvements, power reliability remains a persistent structural barrier that constrains Nigeria’s ability to scale cloud infrastructure capacity proportionally with accelerating digital demand.

Cybersecurity Capability Gaps and Data Sovereignty Compliance Pressures

Nigeria’s rapidly expanding digital economy and cloud adoption expose organizations to increasing cybersecurity threats while domestic cybersecurity capacity, skilled workforce availability, and institutional readiness are still developing relative to the sophistication required for hyperscale cloud environments. Enterprises migrating sensitive financial, government, and citizen data to cloud platforms must comply with evolving data protection regulations and localization mandates, yet many organizations lack mature governance frameworks and risk management capabilities to ensure secure cloud configuration and compliance alignment. Shortage of advanced cybersecurity professionals capable of managing cloud-native security architectures, threat monitoring, and incident response creates dependence on external expertise, raising operational costs and slowing secure cloud deployment across regulated sectors. Data sovereignty requirements mandate that certain data categories remain within national borders, compelling cloud providers to establish localized infrastructure and certification frameworks, which increases capital expenditure and operational complexity for global providers entering the Nigerian market. Fragmented regulatory interpretation and evolving compliance standards can create uncertainty for enterprises and providers regarding acceptable data storage, transfer, and processing practices, potentially delaying cloud adoption decisions. Cyber threats targeting financial institutions, telecom networks, and government systems highlight the need for robust cloud security architectures, yet inconsistent implementation of encryption, identity management, and monitoring tools across organizations increases systemic vulnerability. Small and medium enterprises often lack awareness or resources to implement secure cloud migration strategies, exposing them to misconfiguration risks and data breaches that undermine trust in cloud platforms. Public sector agencies also face institutional challenges in aligning procurement, governance, and cybersecurity policies with modern cloud deployment models, slowing sovereign cloud initiatives. These combined cybersecurity capability gaps and regulatory compliance pressures create a challenging environment that requires coordinated development of skills, standards, and infrastructure to ensure secure and trusted cloud infrastructure expansion in Nigeria.

Opportunities

Regional Edge Cloud Expansion and Low-Latency Service Ecosystems

Nigeria’s geographic scale, urban distribution, and growing digital service demand create strong potential for regional edge cloud deployments that bring compute and storage resources closer to end users, reducing latency and improving performance for applications such as fintech transactions, streaming, e-commerce, and real-time analytics across multiple cities. Telecom operators upgrading 4G and emerging 5G networks require distributed cloud nodes to support virtualized network functions and content delivery, creating a natural convergence between telecom infrastructure and edge cloud platforms across metropolitan and regional locations. Enterprises in sectors such as oil and gas, manufacturing, and logistics increasingly adopt IoT and real-time monitoring solutions that benefit from localized data processing and analytics, driving demand for edge computing infrastructure integrated with central cloud environments. Regional data centers in cities such as Port Harcourt, Kano, and Ibadan can host edge clusters that support local enterprises and reduce reliance on Lagos-based facilities, improving national infrastructure resilience and service availability. Government digital services, smart city platforms, and public safety systems also require low-latency processing and localized hosting, presenting opportunities for public-private partnerships in distributed cloud infrastructure deployment. Hyperscale providers can extend availability zones through modular edge facilities interconnected with core data center campuses, enabling nationwide cloud coverage while maintaining centralized management and orchestration. Content delivery networks and media platforms benefit from edge caching nodes that reduce bandwidth consumption and improve user experience across geographically dispersed populations. Edge cloud expansion also stimulates regional economic development by attracting digital businesses and service providers to secondary cities with improved digital infrastructure. These dynamics position regional edge cloud ecosystems as a significant opportunity for Nigeria to enhance nationwide digital service performance while expanding overall cloud infrastructure capacity and geographic reach.

Sovereign Cloud and Government Digital Infrastructure Modernization

Nigeria’s public sector digitization agenda and data sovereignty requirements create substantial opportunity for sovereign cloud infrastructure tailored to government agencies, public institutions, and regulated industries that require secure domestic hosting aligned with national cybersecurity and privacy frameworks. Government ministries, defense agencies, healthcare institutions, and public service platforms are transitioning toward digital service delivery, requiring scalable infrastructure capable of hosting citizen databases, e-governance applications, and national digital identity systems within controlled domestic environments. Sovereign cloud models operated through partnerships between government entities and certified domestic or international providers can ensure compliance with localization mandates while leveraging advanced cloud technologies and operational expertise. Public sector adoption of cloud infrastructure reduces reliance on fragmented legacy IT systems and enables integrated data platforms that improve administrative efficiency, policy analytics, and service accessibility for citizens. National digital transformation initiatives, including smart governance, electronic procurement, and digital taxation systems, require secure and resilient cloud backbones capable of supporting high transaction volumes and nationwide access. Investment in sovereign cloud infrastructure can also stimulate domestic technology ecosystems by fostering local data center expansion, cybersecurity capability development, and cloud service innovation aligned with government standards. International cloud providers entering sovereign partnerships gain access to large public sector workloads while contributing technical expertise and infrastructure investment to domestic markets. Sovereign cloud deployment further strengthens national digital sovereignty by ensuring critical data and infrastructure remain under domestic jurisdiction and regulatory oversight. As government digitization accelerates, sovereign cloud platforms represent a major opportunity to anchor long-term cloud infrastructure demand while enhancing national cybersecurity, governance capability, and digital public service delivery.

Future Outlook

Nigeria’s cloud infrastructure market is expected to expand steadily over the next five years as enterprise digitalization, hyperscale investments, and data localization policies reinforce domestic cloud adoption. Growth will be supported by new data center capacity, telecom cloud integration, and regional edge deployments improving nationwide coverage. Regulatory emphasis on cybersecurity and sovereign data hosting will accelerate public sector cloud migration. Increasing AI workloads and digital services demand will further strengthen infrastructure modernization and hybrid cloud architectures.

Major Players

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Oracle Cloud Infrastructure

- Huawei Cloud

- IBM Cloud

- Equinix

- Digital Realty

- MainOne

- Rack Centre

- MTN Nigeria

- Globacom

- Vodacom Business Nigeria

- Layer3

- 21st Century Technologies

Key Target Audience

- Telecommunications operators

- Banking and financial institutions

- Government and regulatory bodies

- Cloud service providers

- Data center operators

- Large enterprises

- Digital platform companies

- Investment and venture capital firms

Research Methodology

Step 1: Identification of Key Variables

Key variables such as cloud deployment models, data center capacity, connectivity infrastructure, enterprise adoption patterns, regulatory frameworks, and sector demand drivers were identified through secondary research and industry databases. These variables defined market structure and segmentation.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed using infrastructure capacity data, enterprise IT spending patterns, and cloud deployment trends across sectors. Supply-side data from providers and demand-side adoption indicators were triangulated to build market estimates.

Step 3: Hypothesis Validation and Expert Consultation

Findings and assumptions were validated through consultations with cloud providers, telecom operators, data center experts, and enterprise IT decision-makers. Expert insights refined segmentation shares, growth drivers, and infrastructure deployment dynamics.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into a structured analytical framework covering market size, segmentation, competitive landscape, and future outlook. Consistency checks and cross-verification ensured reliability of conclusions and projections.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of hyperscale and carrier neutral data centers

Accelerating enterprise digital transformation initiatives

Rising demand for secure data localization infrastructure

Growth of fintech and digital service ecosystems

Government cloud adoption and e governance programs - Market Challenges

Power reliability constraints for large data centers

High capital cost of hyperscale infrastructure deployment

Limited domestic semiconductor and hardware supply chains

Cybersecurity capability gaps and threat exposure

Connectivity bottlenecks outside major urban hubs - Market Opportunities

Development of regional edge cloud zones

Public sector sovereign cloud initiatives

Partnerships between telecom operators and hyperscalers - Trends

Shift toward hybrid and multi cloud architectures

Adoption of AI ready GPU accelerated cloud nodes

Localization of data hosting and compliance driven cloud

Integration of edge and 5G cloud platforms

Growth of managed cloud and platform services - Government Regulations & Defense Policy

Data protection and privacy compliance frameworks

National cloud and data localization policies

Critical infrastructure cybersecurity regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Multi Cloud Management Systems

Edge Cloud Infrastructure - By Platform Type (In Value%)

Data Center Platforms

Telecom Network Cloud

Enterprise IT Environments

Government Cloud Platforms

Hyperscale Cloud Facilities - By Fitment Type (In Value%)

On Premise Cloud Deployment

Hosted Cloud Deployment

Colocation Based Cloud

Managed Cloud Services

Integrated Hybrid Deployment - By End User Segment (In Value%)

Telecommunications Providers

Banking and Financial Services

Government and Public Sector

Large Enterprises and Conglomerates

Digital Native and E Commerce Firms - By Procurement Channel (In Value%)

Direct Vendor Procurement

System Integrator Contracts

Telecom Operator Partnerships

Government Tender Programs

Cloud Marketplace Platforms - By Material / Technology (in Value %)

Virtualization and Containerization

Software Defined Networking

Hyperconverged Infrastructure

AI Optimized Compute Hardware

High Density Storage Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Deployment Model, Data Center Scale, Network Integration, Security Capabilities, Pricing Structure, Service Portfolio, Industry Focus, Geographic Presence, Partnership Ecosystem)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud

Oracle Cloud Infrastructure

Huawei Cloud

IBM Cloud

Equinix

Digital Realty

MainOne

Rack Centre

MTN Nigeria

Globacom

Vodacom Business Nigeria

Layer3

21st Century Technologies

- Telecom operators expanding cloud core and edge capacity

- Banks migrating mission critical workloads to private cloud

- Government agencies adopting sovereign cloud platforms

- Large enterprises integrating hybrid cloud environments

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now