Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Nigeria’s diagnostic laboratories sector demonstrates steady expansion, supported by increased testing demand and public health surveillance initiatives. Based on a recent historical assessment, the diagnostic laboratory services market in Nigeria is valued at approximately USD ~ billion according to healthcare expenditure insights compiled by the World Health Organization and Nigeria’s Federal Ministry of Health. Growth is driven by expanding clinical laboratory networks, rising incidence of infectious and chronic diseases, and government-supported screening programs that strengthen testing capacity across public and private healthcare systems nationwide.

Major diagnostic activity is concentrated in urban healthcare hubs such as Lagos, Abuja, and Port Harcourt, where advanced hospital infrastructure and specialized laboratories are located. These cities host large tertiary hospitals, multinational diagnostic providers, and research facilities that process a high volume of clinical samples. Strong population density, corporate healthcare demand, and private hospital investment support laboratory utilization in these locations. Access to modern equipment, skilled laboratory professionals, and medical research institutions further reinforces their leadership in Nigeria’s diagnostic testing ecosystem.

Market Segmentation

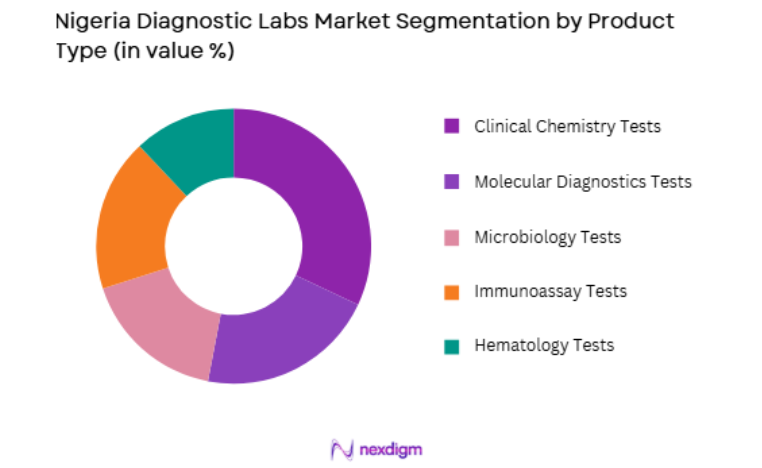

By Product Type

Nigeria Diagnostic Labs market is segmented by product type into clinical chemistry tests, molecular diagnostics tests, microbiology tests, immunoassay tests, and hematology tests. Recently, clinical chemistry tests have a dominant market share due to factors such as high demand for routine health screenings, strong hospital laboratory adoption, and widespread availability of automated chemistry analyzers in tertiary healthcare facilities. These tests are widely used for metabolic panels, kidney function evaluation, and liver function monitoring, which are frequently required in patient diagnosis and treatment management. The prevalence of lifestyle diseases and chronic conditions in urban populations has also increased demand for blood chemistry testing. Additionally, private diagnostic chains and hospital laboratories prefer clinical chemistry platforms due to their scalability, cost efficiency, and ability to process large testing volumes daily.

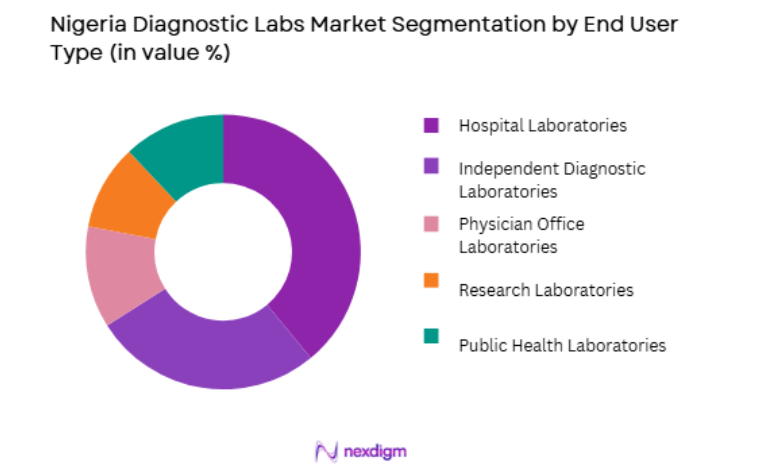

By End User

Nigeria Diagnostic Labs market is segmented by end user into hospital laboratories, independent diagnostic laboratories, physician office laboratories, research laboratories, and public health laboratories. Recently, hospital laboratories have a dominant market share due to factors such as strong patient inflow, integrated healthcare services, and established testing infrastructure within large medical facilities. Hospitals conduct a broad spectrum of tests including blood diagnostics, infectious disease screening, and pathology services, allowing them to manage high daily testing volumes. Government investment in hospital modernization and expansion of tertiary medical centers also strengthens hospital laboratory capacity. Furthermore, hospitals maintain in-house laboratories to reduce turnaround time for critical tests, ensuring faster diagnosis and treatment decisions for patients requiring urgent medical care.

Competitive Landscape

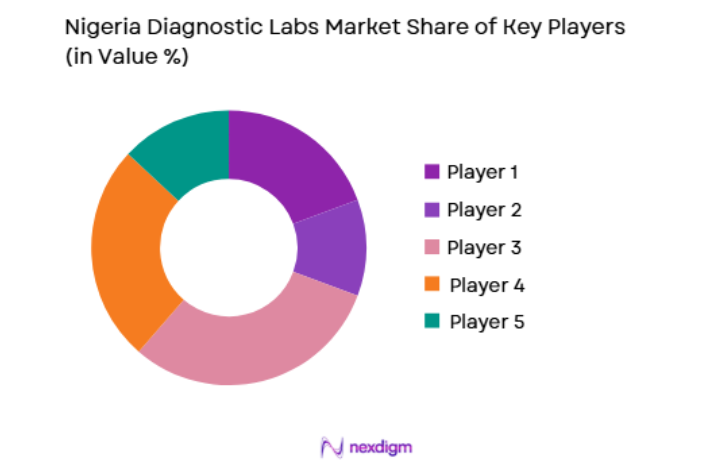

The Nigeria diagnostic laboratories market exhibits a moderately fragmented competitive structure with a combination of multinational diagnostic corporations and established regional laboratory networks. Large hospital-based laboratories dominate high-volume testing while private diagnostic chains expand services through urban laboratory centers. Strategic partnerships with healthcare providers and investments in automated testing technologies enable leading players to strengthen service capabilities. Competition focuses on laboratory accreditation, test portfolio expansion, and improved turnaround times, while multinational diagnostic companies influence technology adoption and specialized testing services.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Laboratory Network Size |

| Synlab Nigeria | 2016 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| PathCare Nigeria | 1923 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| Cerba Lancet Nigeria | 2009 | Abuja, Nigeria | ~ | ~ | ~ | ~ | ~ |

| 54gene Diagnostics | 2019 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| Clina-Lancet Laboratories | 2007 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

Nigeria Diagnostic Labs Market Analysis

Growth Drivers

Increasing Burden of Infectious and Chronic Diseases Requiring Diagnostic Testing

Nigeria’s diagnostic laboratory market continues to expand due to the rising incidence of communicable and non-communicable diseases requiring regular testing and monitoring. Infectious diseases such as malaria, tuberculosis, HIV, and hepatitis remain prevalent in many parts of the country and require continuous diagnostic surveillance through laboratory testing. Public health screening initiatives conducted by government agencies and international health organizations have also increased the demand for laboratory testing services across hospitals and independent laboratories. At the same time, lifestyle-related diseases such as diabetes, cardiovascular disorders, and kidney diseases are becoming more common in urban populations. These conditions require frequent blood chemistry tests, lipid panels, and other diagnostic evaluations that laboratories must provide consistently. The growing awareness of preventive healthcare and early disease detection has further encouraged individuals to undergo routine diagnostic checkups in both public and private laboratories. In addition, health insurance coverage expansion in urban areas allows more patients to access laboratory testing services through hospital networks. As a result, diagnostic laboratories are witnessing steady growth in sample volumes and testing demand across multiple medical specialties.

Government Health Programs and Laboratory Infrastructure Development

Government investment in healthcare infrastructure and disease surveillance programs has significantly strengthened Nigeria’s diagnostic laboratory capacity. Public sector initiatives coordinated by the Federal Ministry of Health and international organizations have supported the establishment of new diagnostic centers and modernization of existing laboratories. National programs focusing on HIV monitoring, tuberculosis screening, malaria detection, and maternal health testing require extensive laboratory services across public hospitals and community health centers. These programs increase the demand for diagnostic equipment, reagents, and skilled laboratory technicians to process clinical samples efficiently. In addition, national disease surveillance systems rely heavily on laboratory confirmation of infectious diseases, encouraging laboratories to adopt advanced testing technologies such as PCR and molecular diagnostics. Government partnerships with private healthcare providers also promote diagnostic network expansion in urban and semi-urban regions. Investment in training programs for laboratory professionals further improves diagnostic service quality and testing accuracy. As healthcare authorities continue strengthening diagnostic infrastructure, laboratory testing becomes an essential component of disease management and public health monitoring in Nigeria.

Market Challenges

Limited Laboratory Infrastructure and Uneven Diagnostic Access Across Regions

Nigeria’s diagnostic laboratory market faces challenges related to unequal distribution of laboratory infrastructure across different geographic regions. While large cities such as Lagos and Abuja have relatively advanced diagnostic facilities, many rural and semi-urban communities lack adequate laboratory services. Healthcare facilities in these areas often operate with limited diagnostic equipment and insufficient testing capabilities. This disparity restricts access to essential laboratory testing for millions of residents who rely on small clinics with minimal diagnostic capacity. Transportation of samples from remote areas to urban laboratories also increases turnaround time for test results and delays medical treatment decisions. Limited laboratory infrastructure can reduce disease detection efficiency, particularly for infectious diseases that require rapid diagnostic confirmation. Additionally, shortages of trained laboratory technologists and pathologists in underserved regions further constrain diagnostic service availability. These challenges create a gap between healthcare demand and laboratory capacity in many parts of the country. Addressing regional disparities in diagnostic infrastructure remains essential to improving nationwide healthcare access and strengthening Nigeria’s medical testing ecosystem.

High Cost of Advanced Diagnostic Technologies and Equipment Maintenance

The adoption of advanced diagnostic technologies in Nigeria is constrained by the high cost of laboratory equipment, reagents, and maintenance services. Molecular diagnostic platforms, automated analyzers, and specialized pathology equipment require substantial capital investment for procurement and installation. Many small and mid-sized diagnostic laboratories face financial limitations that prevent them from upgrading their testing infrastructure. Imported diagnostic equipment also requires regular servicing and calibration, which increases operational expenses for laboratory operators. Additionally, fluctuations in foreign exchange rates can raise the cost of imported reagents and laboratory consumables, affecting laboratory profitability and service affordability. Hospitals and diagnostic centers must balance the need for advanced testing capabilities with financial sustainability in a competitive healthcare market. The cost barrier can also limit the availability of specialized tests such as genetic diagnostics and advanced molecular testing. As a result, laboratories may rely on outsourcing certain complex tests to international facilities, increasing turnaround time and costs for patients.

Opportunities

Expansion of Private Diagnostic Laboratory Networks in Urban Healthcare Markets

Private diagnostic laboratory networks are expanding rapidly in Nigeria’s urban healthcare landscape, creating opportunities for modern diagnostic centers with advanced testing capabilities. Growing middle-income populations in cities such as Lagos and Abuja increasingly seek reliable laboratory services for preventive health screening and chronic disease monitoring. Private diagnostic chains are responding by establishing standalone laboratory centers equipped with automated analyzers and digital reporting systems. These facilities often partner with private hospitals and corporate healthcare providers to deliver comprehensive diagnostic services to patients and employers. In addition, private laboratories can offer specialized tests that are not always available in public healthcare institutions. Investment from healthcare entrepreneurs and international diagnostic providers is accelerating laboratory expansion in metropolitan areas. These developments enable diagnostic networks to increase service capacity and introduce innovative testing technologies. As urban healthcare demand continues to rise, private laboratory operators are positioned to strengthen diagnostic accessibility and service quality within Nigeria’s healthcare system.

Adoption of Molecular Diagnostics and Digital Laboratory Technologies

The integration of molecular diagnostics and digital laboratory technologies represents a major opportunity for Nigeria’s diagnostic laboratory sector. Molecular testing platforms enable laboratories to detect infectious diseases, genetic disorders, and cancer markers with greater accuracy and speed. These technologies are particularly valuable for managing disease outbreaks and improving early diagnosis of complex medical conditions. Digital laboratory systems such as laboratory information management systems improve workflow efficiency by automating sample tracking, data management, and result reporting. Telepathology and digital diagnostic platforms also allow specialists to analyze laboratory results remotely, supporting healthcare facilities in regions with limited medical expertise. International collaborations with research institutions and biotechnology companies are encouraging the introduction of advanced diagnostic tools in Nigerian laboratories. As healthcare providers seek to improve diagnostic precision and patient outcomes, adoption of modern laboratory technologies is expected to accelerate across hospital and independent diagnostic networks.

Future Outlook

Nigeria’s diagnostic laboratories market is expected to experience continued expansion as healthcare access improves and diagnostic awareness grows. Increasing investments in hospital infrastructure, laboratory equipment, and workforce training will enhance national testing capacity. Technological advancements in molecular diagnostics and digital laboratory systems are likely to improve diagnostic accuracy and operational efficiency. Public health initiatives focused on disease surveillance and preventive screening will also drive testing demand. Growing urban healthcare markets and private laboratory network expansion will further strengthen the diagnostic ecosystem over the coming years.

Major Players

- SynlabNigeria

- PathCare Nigeria

- Cerba Lancet Nigeria

- Clina-Lancet Laboratories

- 54gene Diagnostics

- Medbury Medical Services

- DNA Labs Nigeria

- Union Diagnostic and Clinical Services

- Bio-Medical Laboratories Nigeria

- Echo Scan Diagnostics

- Avon Medical Practice Diagnostics

- Reddington Hospital Laboratories

- Euracare Diagnostics

- Lagoon Hospitals Laboratory Services

- Cedarcrest Hospitals Diagnostics

Key Target Audience

- Hospital networks and healthcare providers

- Diagnostic laboratory operators

- Pharmaceutical and biotechnology companies

- Medical device and diagnostic equipment manufacturers

- Health insurance providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying critical variables influencing the Nigeria diagnostic labs market, including testing demand, disease prevalence, laboratory infrastructure, and regulatory frameworks. These variables establish the analytical scope for evaluating market growth patterns and healthcare service dynamics.

Step 2: Market Analysis and Construction

Primary and secondary healthcare data sources are analyzed to construct the diagnostic laboratory market structure. Hospital networks, private laboratories, and healthcare expenditure indicators are examined to determine market composition and service utilization patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions are validated through consultations with laboratory professionals, healthcare administrators, and diagnostic equipment providers. Expert insights help refine analytical models and confirm realistic demand patterns within Nigeria’s healthcare ecosystem.

Step 4: Research Synthesis and Final Output

All validated data and expert insights are synthesized into a structured research framework. The final analysis integrates market segmentation, competitive positioning, and industry dynamics to produce a comprehensive assessment of the Nigeria diagnostic laboratories market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising Burden of Infectious and Chronic Diseases

Government Investments in Public Health and Laboratory Infrastructure

Expansion of Private Diagnostic Laboratory Chains - Market Challenges

Limited Advanced Laboratory Infrastructure in Rural Areas

Dependence on Imported Diagnostic Equipment and Reagents

Shortage of Skilled Laboratory Technicians - Market Opportunities

Expansion of Preventive Health Screening Services

Adoption of Molecular and Genetic Testing Technologies

Growth of Private Diagnostic Laboratory Networks - Trends

Automation and Digitalization of Laboratory Testing Workflows

Increasing Demand for Rapid and Point-of-Care Diagnostics - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Testing

Molecular Diagnostics Testing

Hematology Testing

Microbiology Testing

Immunoassay Testing - By Platform Type (In Value%)

Hospital-Based Diagnostic Laboratories

Independent Diagnostic Laboratories

Public Health Laboratories

Mobile Diagnostic Units - By Fitment Type (In Value%)

Standalone Laboratory Facilities

Hospital-Integrated Laboratories

Diagnostic Laboratory Networks

Public Health Laboratory Centers - By End User Segment (In Value%)

Hospitals

Diagnostic Centers

Research and Academic Institutes

- Market Share Analysis

- Cross Comparison Parameters (Test Portfolio Breadth, Laboratory Network Coverage, Technology Adoption Level, Accreditation and Quality Standards, Turnaround Time Efficiency, Pricing Structure, Partnership with Hospitals)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Synlab Nigeria

PathCare Laboratories

54gene Diagnostics

Clina Lancet Laboratories

Echo-Scan Services

Medbury Medical Services

Union Diagnostic and Clinical Services

Total Medical Services

Lancet Laboratories

Eurofins Scientific

Laboratory Corporation of America Holdings

Quest Diagnostics

Roche Diagnostics

Abbott Diagnostics

Randox Laboratories

- Hospitals Expanding In-House Laboratory Testing Facilities

- Private Diagnostic Chains Increasing Regional Laboratory Coverage

- Government Public Health Programs Driving Demand for Diagnostic Testing

- Research Institutes Expanding Use of Molecular and Genomic Testing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now