Download PDF

Download PDFMarket Overview

The Nigeria Energy Drink Market is valued at USD ~ million, based on a five-year historical analysis, and another published benchmark places the category at USD ~ million in the next base period depending on scope and channel coverage. The forecasted CAGR for the 2026–2035 period is 6.20%. Demand is driven by youth consumption, nightlife, gig work, work fatigue, transport corridors, open-market retail and high-caffeine functional beverage use. The Nigeria Energy Drink Market is concentrated in Lagos, Abuja, Port Harcourt, Kano, Ibadan, Onitsha, Aba and Ogun industrial corridors because these cities combine transport hubs, nightlife, open markets, universities, dispatch riders, supermarkets, kiosks and petrol-station retail. Nigeria’s population reached 232,679,478, compared with 227,882,945 in the preceding base, while GDP stood at USD 252.26 billion and GDP per capita at USD 1,084.2, supporting a large but value-sensitive packaged beverage base.

Market Segmentation

By Product Type

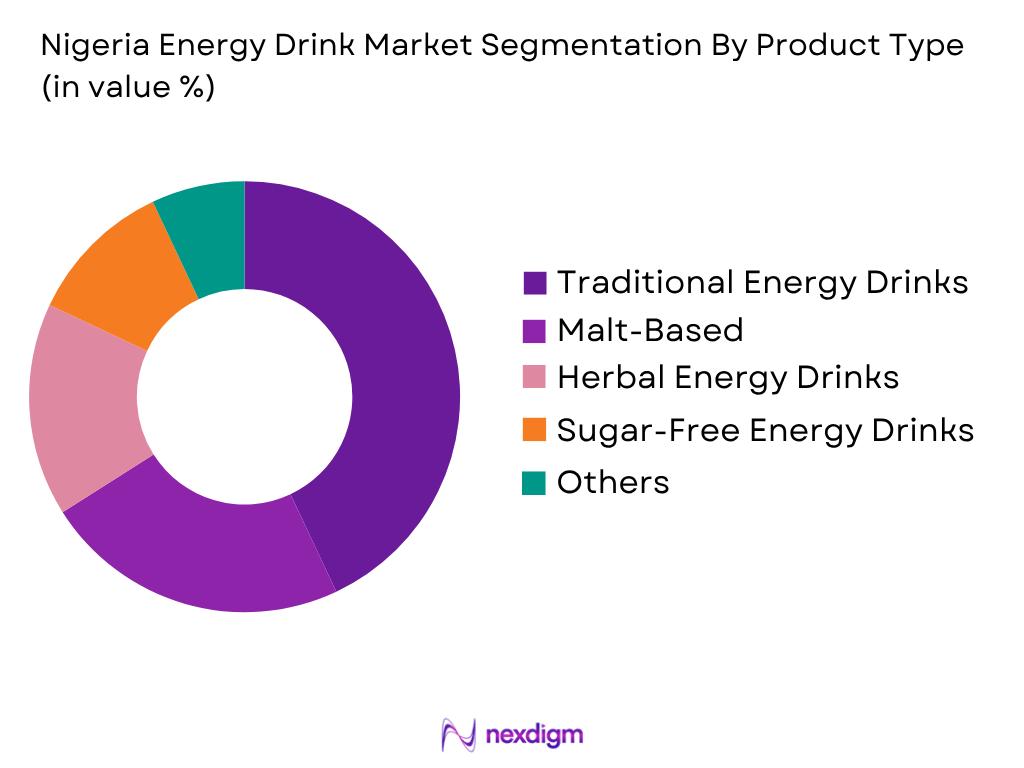

Nigeria Energy Drink Market is segmented by product type into traditional energy drinks, malt-based or glucose energy drinks, herbal energy drinks, sugar-free energy drinks, sports energy drinks, and energy shots or powdered energy mixes. Recently, traditional energy drinks have a dominant market share in Nigeria under product type segmentation due to their strong fit with the country’s mainstream consumption occasions: work fatigue, late-night study, dispatch riding, driving, open-market trading, nightlife and outdoor labour. Brands such as Fearless, Supa Komando, Predator, Red Bull, Monster, Power Horse and Bullet are positioned around alertness, stamina and quick energy. Traditional energy drinks also benefit from wide availability across kiosks, open markets, supermarkets, petrol stations, clubs and street retail. Malt-based and herbal products have local taste relevance, but traditional caffeine-led RTD energy drinks dominate because they have stronger brand recall, wider cold-shelf visibility and broader price-pack availability.

By Packaging Type

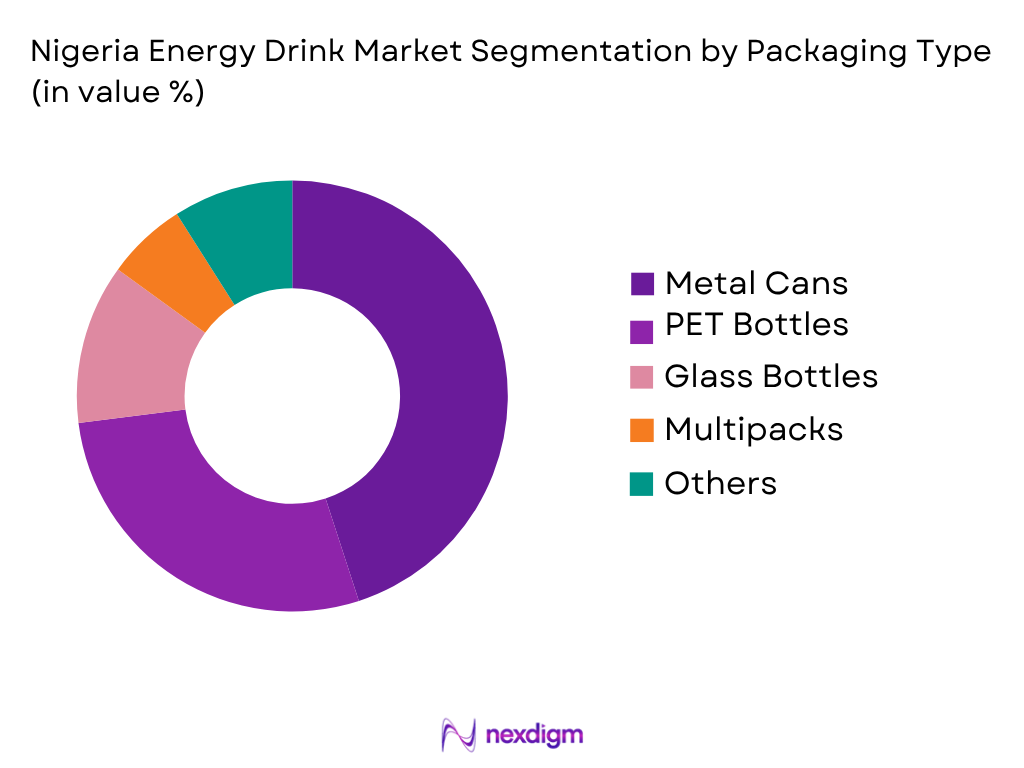

Nigeria Energy Drink Market is segmented by packaging type into metal cans, PET bottles, glass bottles, multipacks, shots, sachets, powder tubs and other formats. Recently, metal cans have a dominant market share under packaging type segmentation because cans are closely linked to mainstream energy drink identity, carbonated stability, fast chilling and visible impulse purchase across supermarkets, kiosks, petrol stations, bars and open-market retail. Fearless, Supa Komando, Predator, Red Bull, Monster, Bullet and Power Horse rely heavily on cans for brand recognition and quick single-serve consumption. PET bottles remain important in Nigeria because affordability, resealability and roadside consumption matter in value-led channels. However, cans remain dominant because energy drinks are typically bought cold and consumed immediately during commuting, study, work breaks, nightlife, dispatch riding and intercity travel. Across Africa, cans held 57.04% of energy drink packaging volume, supporting the format’s regional leadership.

Competitive Landscape

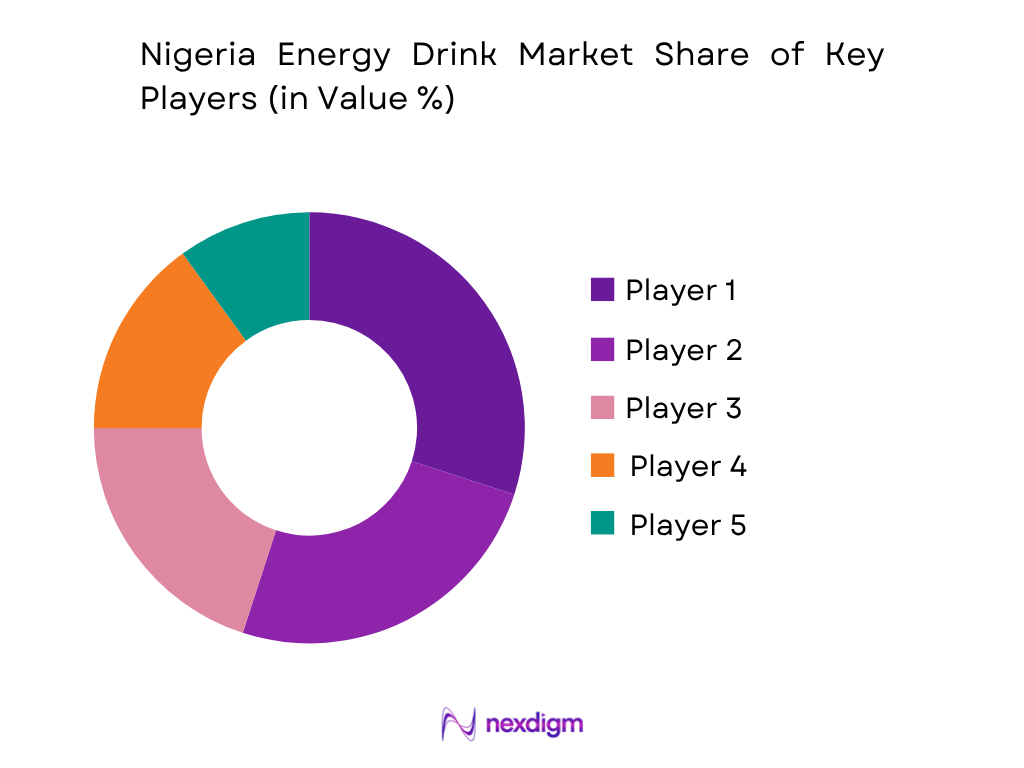

The Nigeria Energy Drink Market is shaped by strong local beverage companies, global premium brands, regional imports and herbal-functional challengers. Rite Foods’ Fearless and Seven-Up Bottling Company’s Supa Komando compete through local manufacturing, affordability, youth marketing and wide distribution, while Red Bull, Monster, Power Horse and Bullet compete through premium imported-style positioning and nightlife relevance. Climax and other herbal energy products add a local functional angle. Competition is intense because products must secure cold visibility across supermarkets, kiosks, open markets, petrol stations and on-trade venues.

| Company | Establishment Year | Headquarters | Core Energy Portfolio | Nigeria Positioning | Packaging Focus | Channel Strength | Product Innovation Focus | Market-Specific Edge |

| Rite Foods Limited | 2007 | Ogun State, Nigeria | ~ | ~ | ~ | ~ | ~ | ~ |

| Seven-Up Bottling Company | 1959 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ | ~ |

| The Coca-Cola Company Nigeria | 1951 | Atlanta, USA / Lagos operations | ~ | ~ | ~ | ~ | ~ | ~ |

| Red Bull GmbH | 1984 | Fuschl am See, Austria | ~ | ~ | ~ | ~ | ~ | ~ |

| Monster Beverage Corporation | 1935 | Corona, California, USA | ~ | ~ | ~ | ~ | ~ | ~ |

Nigeria Energy Drink Market Analysis

Growth Drivers

Large Urban Consumer Base Supporting Kiosk and Roadside Energy Drink Demand

Nigeria Energy Drink Market is supported by a large urban consumer base that fits single-serve, impulse-led beverage consumption through kiosks, open markets, bus parks, petrol stations, supermarkets and roadside retail. World Bank reported Nigeria’s population at 232,679,478 people and urban population at 146,531.22 thousand people in 2024, creating dense demand clusters in Lagos, Abuja, Port Harcourt, Kano, Ibadan and Onitsha. Nigeria’s GDP stood at USD 252.26 billion, while GDP per capita stood at USD 1,084.2, supporting a large but value-sensitive market where local cans, PET packs and chilled kiosk availability are critical.

Work-Fatigue, Informal Employment and Transport-Led Consumption Occasions

Nigeria Energy Drink Market benefits from work-fatigue and transport-led demand because energy drinks are consumed by traders, dispatch riders, drivers, security workers, construction workers, students and nightlife consumers. Nigeria’s labour-force participation reached 79.5 in Q2 2024, while informal employment reached 93.0 in the same quarter, indicating a large base of workers operating through informal, street-level and cash-based channels. NBS also reported urban labour participation at 77.2 and rural participation at 83.2, supporting broad consumption across open markets, road corridors, motor parks, kiosks and neighbourhood stores where energy drinks are bought for alertness and stamina.

Market Challenges

Affordability Pressure and High Consumer Inflation

Nigeria Energy Drink Market faces affordability pressure because consumers are highly value-sensitive and energy drinks compete with soft drinks, malt drinks, sachet beverages, water and herbal bitters. World Bank reported GDP per capita at USD 1,084.2, while consumer inflation reached 33.2 in 2024, creating pressure on disposable income and limiting premium-only energy drink expansion. Nigeria’s population of 232,679,478 people offers scale, but low purchasing power forces brands to manage pack architecture, local production, smaller SKUs, open-market distribution and promotional rotation. For energy drinks, this challenge is market-specific because everyday demand depends on low-ticket purchase behaviour.

Caffeine, Labelling and Product Registration Compliance

Nigeria Energy Drink Market faces regulatory pressure because formulated caffeinated beverages must meet NAFDAC’s composition, labelling and registration rules. NAFDAC states that formulated caffeinated beverages must contain not less than 14.5 mg/100 ml and not more than 32 mg/100 ml of caffeine, and such products cannot be manufactured, imported, exported, advertised, sold or distributed in Nigeria unless registered and permitted. This directly affects energy drink brands using caffeine, taurine, ginseng, guarana, vitamins and other stimulant claims. The rules also require caffeine declarations per serving and per 100 ml, increasing label-compliance workload for local and imported SKUs.

Market Opportunities

Open-Market, Kiosk and Urban Retail Expansion

Nigeria Energy Drink Market has future growth opportunity in open markets, kiosks, roadside retail, bus parks and petrol stations because current urban density supports frequent small-pack beverage purchases. World Bank reported Nigeria’s urban population at 146,531.22 thousand people and total population at 232,679,478 people in 2024, creating large consumption pools in commercial and transport-heavy cities. GDP of USD 252.26 billion supports national beverage manufacturing, wholesale and distribution systems. Energy drink brands can use these current macro indicators to expand local cans, PET packs, cooler placements, motor-park availability, student-area distribution and value-led product formats without relying on future estimates.

Digital Discovery, Youth Activation and E-Commerce Multipacks

Nigeria Energy Drink Market has future growth opportunity through digital discovery, campus activation, gaming communities, Afrobeats-linked campaigns, supermarket apps and e-commerce multipacks. World Bank reported Nigeria’s population at 232,679,478 people and the individuals-using-the-internet indicator at 41 in 2024, supporting online brand discovery, creator-led campaigns and digital retail visibility. GDP growth stood at 4.1, while GDP was USD 252.26 billion, indicating a macro base for packaged beverage distribution and online grocery development. Energy drink brands can use current digital and urban indicators to expand variety packs, imported SKUs, sugar-free products and nightlife-focused online promotions.

Future Outlook

The Nigeria Energy Drink Market is expected to expand steadily, supported by youth demographics, urbanisation, open-market retail, nightlife, dispatch riding, student consumption, work fatigue and growing local manufacturing. The forecasted CAGR for the 2026–2035 period is 6.20%, with long-term demand supported by functional beverage adoption and high-frequency informal retail consumption.

Over the next phase, traditional energy drinks will remain the core revenue driver because they already have strong visibility across Lagos, Abuja, Port Harcourt, Kano, Ibadan, Onitsha and Aba. Local brands are expected to remain important because they can address affordability, open-market access and distribution depth more effectively than purely imported premium products.

Sugar-free and low-sugar energy drinks will gain relevance in modern trade, gyms, pharmacies and e-commerce, but value-led full-sugar products will continue to serve kiosks, motor parks, open markets and roadside retail. Herbal energy and malt-energy formats can also expand because Nigerian consumers are familiar with malt beverages and local functional positioning.

The strongest future opportunities will come from open-market penetration, campus activation, music and nightlife partnerships, petrol-station placement, dispatch-rider and driver-oriented channels, and e-commerce variety packs. Brands that combine NAFDAC compliance, reliable distribution, local taste adaptation, cold availability and value-pack architecture will be better positioned.

Major Players

- Rite Foods Limited

- Seven-Up Bottling Company

- The Coca-Cola Company Nigeria

- Red Bull Nigeria

- Monster Energy Nigeria

- Power Horse Nigeria

- Bullet Energy Drink

- Climax Herbal Energy Drink

- Nigerian Breweries Plc

- Guinness Nigeria Plc

- Cway Group Nigeria

- Amber Energy Drink

- Gidigbo Energy Drink

- Lucozade Boost Nigeria

- Rockstar Energy Nigeria

Key Target Audience

- Energy drink manufacturers and brand owners

- Functional beverage companies

- Carbonated soft drink and packaged beverage companies

- Supermarket, hypermarket and modern retail chains

- Open-market, wholesale, kiosk and roadside retail operators

- Petrol station, gym, pharmacy and nightlife channel operators

- Investments and venture capitalist firms

- Government and regulatory bodies (NAFDAC, Standards Organisation of Nigeria, Federal Ministry of Health, Federal Inland Revenue Service, Nigeria Customs Service, Federal Competition and Consumer Protection Commission)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map for the Nigeria Energy Drink Market, covering brand owners, local manufacturers, importers, wholesalers, open-market distributors, kiosks, supermarkets, petrol stations, gyms, pharmacies, on-trade venues and regulators. The objective is to identify key variables such as product type, caffeine positioning, pack format, sugar profile, NAFDAC registration, distribution reach and regional demand.

Step 2: Market Analysis and Construction

In this phase, historical data for the Nigeria Energy Drink Market is compiled through country-level market benchmarks, company portfolios, SKU listings, retail shelf checks, e-commerce availability and channel mapping. The assessment reviews traditional energy drinks, herbal energy, malt-energy adjacency, metal cans, PET bottles, open markets, kiosks, petrol stations, nightlife and modern retail visibility.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted telephone interviews with beverage manufacturers, distributors, open-market wholesalers, supermarket buyers, petrol-station retailers, kiosk suppliers, gym retailers, e-commerce sellers and on-trade operators. These consultations provide operational insights into SKU movement, cold availability, price-pack performance, brand switching, flavour demand and regional channel acceptance.

Step 4: Research Synthesis and Final Output

The final phase triangulates top-down market benchmarks with bottom-up brand, SKU, pack and channel evidence. Direct engagement with beverage manufacturers, distributors and retail stakeholders helps verify product segmentation, competitive positioning, regional demand, NAFDAC compliance exposure, distribution gaps and future opportunity areas in the Nigeria Energy Drink Market.

- Executive Summary

- Research Methodology (market definitions and assumptions, RTD energy drink classification, formulated caffeinated beverage scope, non-alcoholic stimulant beverage inclusion, NAFDAC registration framework, excise-duty adjustment, top-down sizing, bottom-up sizing, retail audit checks, distributor interviews, SKU-level price-pack benchmarking)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (youth consumers, open-market distribution, affordability, nightlife, transport corridors, work fatigue, gaming, local manufacturing)

- Market Challenges (excise duty, sugar scrutiny, NAFDAC registration, counterfeit risk, affordability pressure, cold-chain limitations)

- Market Opportunities (local energy brands, PET formats, sugar-free variants, herbal energy, open-market expansion, nightlife, transport channels, e-commerce)

- Market Trends (value energy, local challengers, sugar scrutiny, herbal energy, PET formats, nightlife activation, social media marketing)

- SWOT Analysis

- Porter’s Five Forces

- By Value (2020-2025)

- By Volume (2020-2025)

- By Unit Sales (2020-2025)

- By Product Type (In Value %)

Traditional Energy Drinks

Malt-Based Energy Drinks

Herbal Energy Drinks

Sugar-Free Energy Drinks - By Packaging Type (In Value %)

Aluminum Cans

PET Bottles

Glass Bottles

Multipacks

Large Cans

Slim Cans - By Distribution Channel (In Value %)

Open Markets and Wholesale Depots

Kiosks and Roadside Retail

Supermarkets and Hypermarkets

Convenience Stores

Petrol Stations and Forecourts

Pharmacies and Health Retail - By Region (In Value %)

Lagos

Abuja / FCT

South West

South South

South East

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (caffeine mg per 100 ml, sugar grams per 100 ml, NAFDAC registration and label compliance, local manufacturing footprint, open-market and kiosk distribution depth, PET versus can portfolio, music-campus-nightlife activation intensity, affordability and pack-size architecture

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Rite Foods Limited

Seven-Up Bottling Company

The Coca-Cola Company Nigeria

Red Bull Nigeria

Monster Energy Nigeria

Power Horse Nigeria

Bullet Energy Drink

Climax Herbal Energy Drink

Nigerian Breweries Plc

Guinness Nigeria Plc

Cway Group Nigeria

Amber Energy Drink

Gidigbo Energy Drink

Lucozade Boost Nigeria

Rockstar Energy Nigeria

- Market Demand and Utilization

- Purchasing Power and Budget Allocation

- Regulatory and Compliance Requirements

- Needs, Desires and Pain Point Analysis

- Decision-Making Process

- By Value (2026-2035)

- By Volume (2026-2035)

- By Unit Sales (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now