Download PDF

Download PDFMarket Overview

The Nigeria Hardware Stores Retail Market is valued at approximately USD ~ billion, assessed through the country’s DIY and hardware store retail categories covering hardware and building materials, tools and machines, paint and wallpaper supplies, bathroom hardware, floor covering, lawn and garden, and heating-related products. Demand is driven by residential construction, owner-builder activity, artisan purchases, power-backup products and repair-led spending. Nigeria’s GDP reached USD ~ billion, while GDP per capita stood at USD 1,084.2, supporting a large but price-sensitive retail base. Lagos, Abuja, Port Harcourt, Kano, Ogun and Onitsha dominate the Nigeria Hardware Stores Retail Market because they combine construction activity, open-market clusters, import distribution, logistics networks, contractor density and household repair demand. Nigeria recorded GDP growth of 3.19% in Q2, compared with 2.51% in the comparable prior period, while trade contributed 15.95% to nominal GDP and construction contributed 8.45%. These indicators support hardware retail concentration in commercial, port-linked and infrastructure-led cities.

Market Segmentation

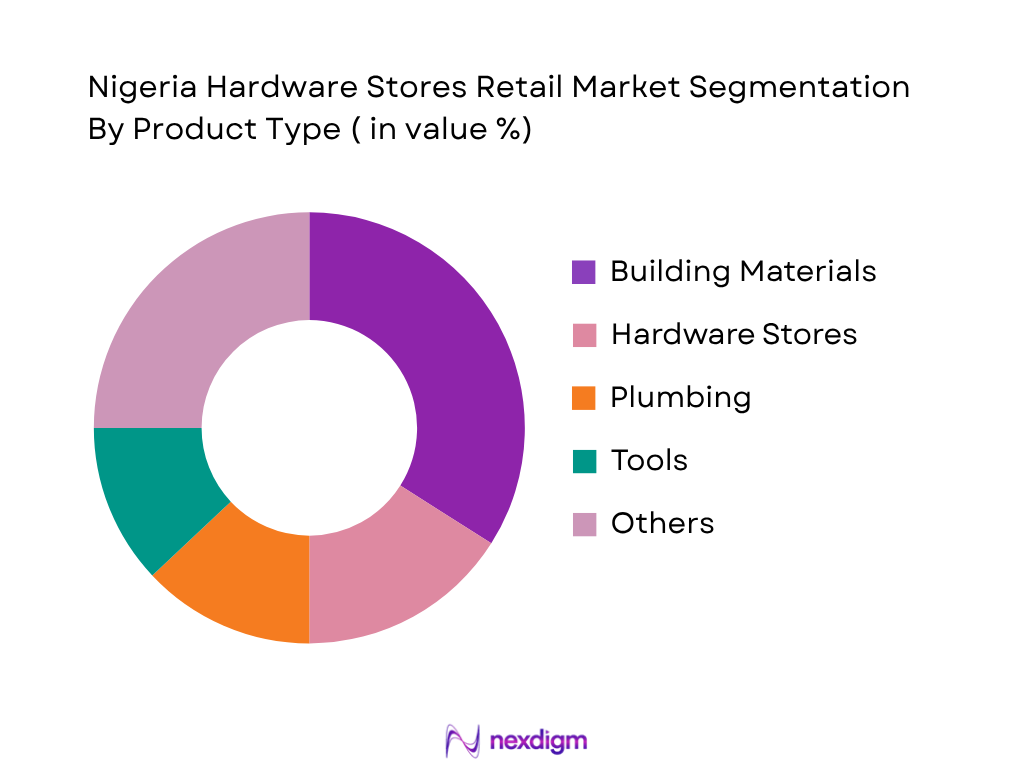

By Product Category

Nigeria Hardware Stores Retail Market is segmented by product category into hardware and building materials, electrical hardware, plumbing supplies, tools and machines, paints, fasteners, safety products, and outdoor hardware. Hardware and building materials hold the dominant market share because Nigerian retail demand is closely linked to incremental housing, small contractor activity, owner-builder projects and repair-led construction. Cement-linked inputs, blocks, steel rods, roofing sheets, timber, boards, binding wire, plastering inputs and basic installation materials generate larger transaction values than standalone tools. This dominance is reinforced by Nigeria’s construction and trade activity, where construction contributed 8.45% to nominal GDP and trade contributed 15.95% in Q2. Hardware stores also serve artisans and informal builders who buy in stages rather than through centralized procurement, making building-material-linked retail the largest revenue pool.

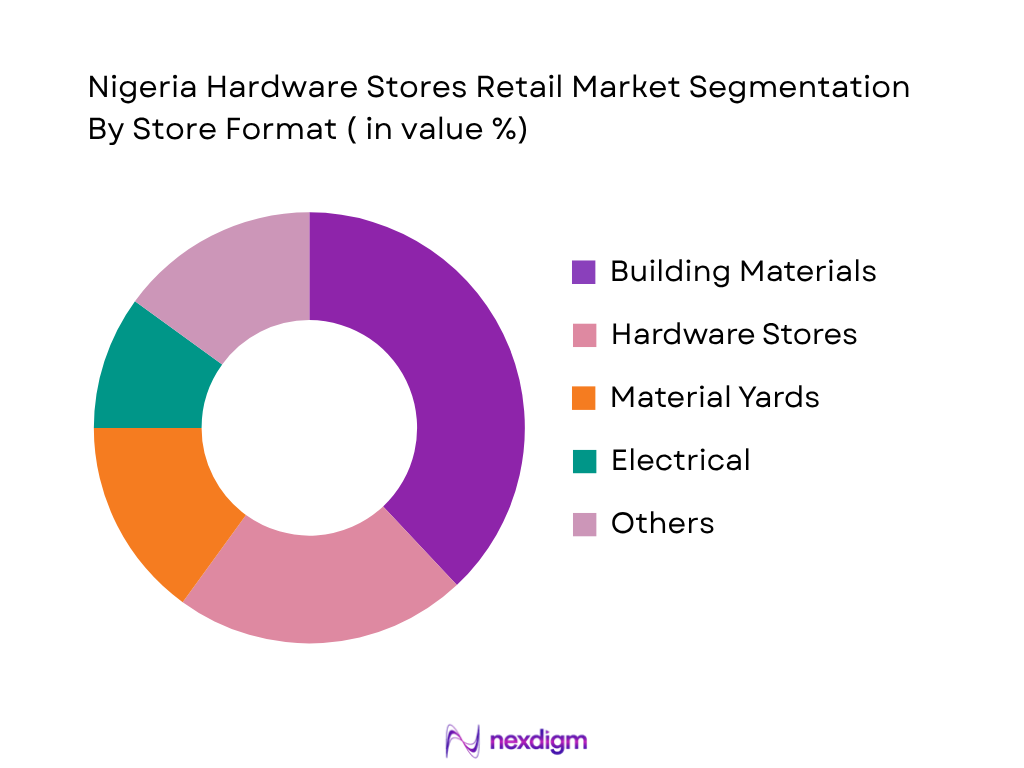

By Store Format

Nigeria Hardware Stores Retail Market is segmented by store format into open-market hardware shops, independent neighbourhood stores, building-material yards, electrical and plumbing counters, specialist tool stores, online retailers and project-based suppliers. Open-market hardware and building-material shops dominate because Nigeria’s hardware distribution is still heavily trader-led, especially in clusters such as Alaba, Ladipo, Dei-Dei, Onitsha, Ariaria and Lagos Island. These clusters combine wholesale, retail, informal credit, bargaining, imported tools, electrical goods, plumbing products and building materials in one location. They also support reseller networks that supply smaller shops across states. Formal online and specialist stores are expanding, but open markets remain dominant because contractors, artisans and owner-builders prioritize immediate availability, price negotiation, product inspection and the ability to source multiple SKUs from adjacent traders in a single trip.

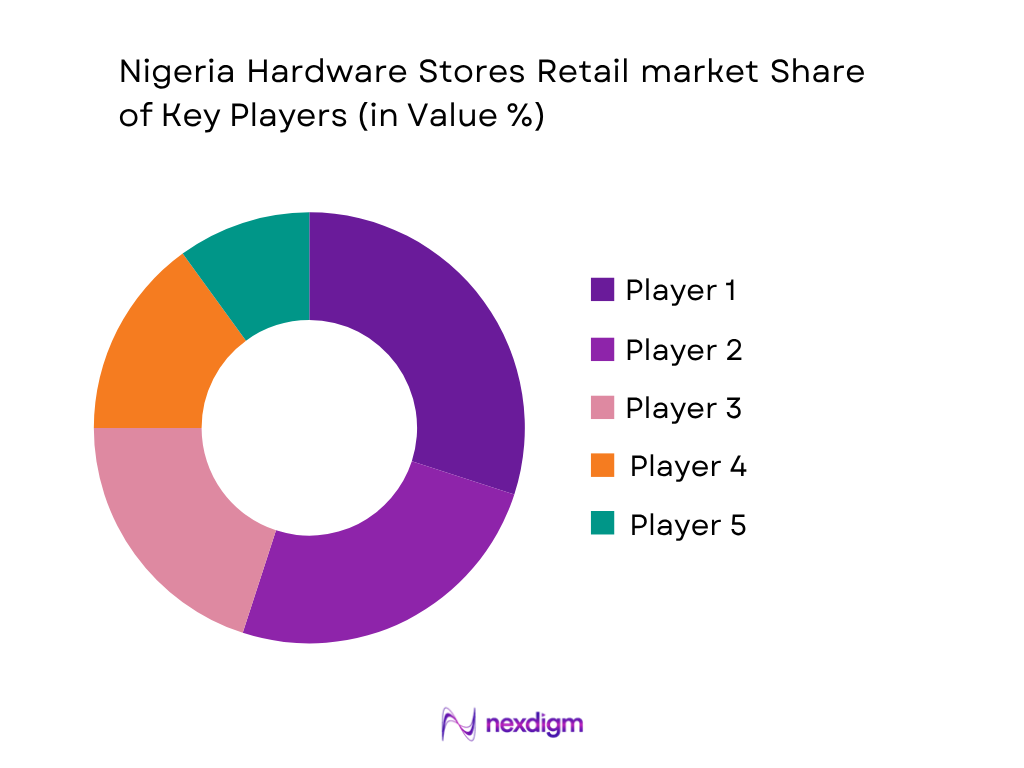

Competitive Landscape

Nigeria Hardware Stores Retail Market is fragmented, with competition spread across open-market traders, independent hardware shops, online tool retailers, industrial suppliers, electrical product manufacturers, cable companies, power-backup distributors and paint retail networks. Mamtus Nigeria and GZ Industrial Supplies serve tool, hardware and industrial-product buyers through online catalogues and specialist positioning. Jumia and Konga provide marketplace visibility for power tools, hand tools and home repair kits. Coleman and Cutix support the electrical hardware channel through cable supply, while Berger Paints supports paint and coating distribution through retail and dealer networks. Mamtus positions itself as a genuine professional hand-tools and hardware supplier, while GZ Industrial Supplies describes itself as an online industrial supplies platform with workshop tools and safety products.

| Major Player | Establishment Year | Headquarters | Core Positioning | Key Product Strength | Primary Customer Base | Sales Channel | Fulfilment Capability | Market-Specific Differentiator |

| Mamtus Nigeria | 2016 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ | ~ |

| GZ Industrial Supplies Nigeria | 2014 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ | ~ |

| Jumia Nigeria Hardware Sellers | 2012 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ | ~ |

| Coleman Technical Industries | 1975 | Ogun, Nigeria | ~ | ~ | ~ | ~ | ~ | ~ |

| Berger Paints Nigeria | 1959 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ | ~ |

Nigeria Hardware Stores Retail Market Analysis

Growth Drivers

Residential Construction and Repair-Led Hardware Consumption

Nigeria Hardware Stores Retail Market is supported by construction-linked retail demand because hardware stores supply building materials, plumbing fittings, cables, switches, paints, fasteners, hand tools and power-tool accessories used in residential building, renovation and repair. The World Bank records Nigeria’s population at 232,679,478 people and GDP at USD 252.26 billion, indicating a large household and contractor base for incremental housing and maintenance purchases. The National Bureau of Statistics reports that trade activity remains central to the economy, while construction is reported as a distinct GDP activity in its official GDP publication. This matters for hardware retail because owner-builders and small contractors typically purchase materials in stages from open markets, building-material yards and neighbourhood stores. Products such as roofing sheets, PVC pipes, steel rods, electrical cables, cement-linked inputs and waterproofing materials are tied directly to ongoing building activity. The market is therefore driven less by one-time discretionary DIY spending and more by recurring purchases connected to housing repairs, informal construction, estate maintenance and artisan-led installation work.

Large Trade Base and Digital Discovery of Hardware Products

Nigeria Hardware Stores Retail Market is also driven by the scale of its trade economy and the growing use of digital discovery for tools, electrical items, plumbing products and building-material sourcing. The World Bank reports GDP per capita at USD 1,084.2 and internet usage at 41 individuals per 100 people, creating a large but price-sensitive consumer base that increasingly searches online before visiting stores or markets. Nigeria’s Q4 merchandise trade reached ₦36,604.83 billion, while Q1 2025 trade reached ₦36,024.66 billion, according to the National Bureau of Statistics foreign trade catalogue. These figures support hardware retail because many SKUs move through importers, wholesalers, open-market traders and resellers before reaching contractors and households. Online marketplaces, WhatsApp ordering and catalogue-led retail are especially useful for fragmented categories such as drill bits, fasteners, valves, switches, pipes, locks, generator accessories and safety gear. Retailers that combine physical availability with digital product visibility can capture both urgent local purchases and planned contractor procurement.

Market Challenges

Import Dependence and Foreign Trade Exposure

Nigeria Hardware Stores Retail Market faces a major challenge from import dependence because technical hardware categories such as power tools, electrical fittings, locks, drill accessories, plumbing components, generator accessories, PPE and branded hand tools often rely on imported supply chains. The National Bureau of Statistics reports Q4 imports of ₦16,590.51 billion, while Q1 2025 imports stood at ₦15,426.17 billion. Manufactured goods imports reached ₦8.47 trillion in Q4, showing the importance of imported finished products and technical goods in Nigeria’s trade mix. This creates direct pressure on hardware retailers because stock availability depends on port clearance, importer liquidity, foreign exchange access, transport reliability and distributor allocation. Open-market traders may respond quickly to availability changes, but formal retailers face higher requirements for documentation, warranty support and product consistency. For contractors and artisans, substitution is often difficult because cables, pipes, switchgear, fasteners and tool accessories must match technical specifications. Import exposure therefore increases the risk of stockouts, delayed project fulfilment and inconsistent assortment quality.

Inflation Pressure and Weak Household Purchasing Capacity

Nigeria Hardware Stores Retail Market is constrained by household affordability pressure, which affects discretionary home improvement, branded tools, decorative paints, bathroom upgrades and premium electrical products. The World Bank reports Nigeria’s GDP per capita at USD 1,084.2, while its annual consumer price inflation indicator is 33.2. These macroeconomic conditions directly affect hardware retail because households and small contractors often purchase project inputs in phases rather than buying full renovation baskets at once. Inflation pressure can shift demand toward economy tools, unbranded fasteners, smaller paint packs, lower-cost plumbing fittings and used or refurbished equipment. It can also reduce store loyalty, as customers compare prices across Alaba, Dei-Dei, Ladipo, Onitsha, Jiji, Jumia and local hardware outlets before purchasing. Retailers must maintain affordable SKUs while still managing working capital across thousands of product variants. The challenge is sharper for independent stores because they cannot always absorb inventory volatility, supplier prepayment terms or transport disruptions. Hardware retailers therefore need disciplined category selection, fast-moving inventory focus and strong supplier relationships.

Market Opportunities

Power-Backup and Electrical Resilience Hardware

Nigeria Hardware Stores Retail Market has a clear opportunity in power-backup and electrical-resilience products, including cables, changeover switches, extension leads, surge protection, inverter accessories, generator spares, battery terminals, solar mounting inputs and electrical safety products. The National Bureau of Statistics reported Q1 electricity supply of 5,769.52 GWh and Q2 supply of 5,612.52 GWh, showing the scale of formal grid supply tracked through distribution companies. NERC’s Q4 report recorded grid-connected quarterly generation of 9,289.95 GWh and average available generation capacity of 5,296.89 MW. These current electricity indicators support hardware demand because households, SMEs, offices, workshops and estates continue to invest in electrical protection, backup systems and installation consumables. Hardware stores and electrical trade counters can grow by stocking certified cables, circuit breakers, switches, sockets, cable ties, conduits, mounting accessories and safety gear for electricians. The opportunity is especially relevant in Lagos, Abuja, Port Harcourt, Kano and industrial corridors, where business continuity and residential power reliability create repeated repair and replacement purchases.

Formalized Omnichannel Hardware Retail and B2B Procurement

Nigeria Hardware Stores Retail Market has an opportunity to formalize hardware buying through digital catalogues, WhatsApp ordering, online marketplaces, quotation systems and store-based fulfilment. The World Bank records 41 internet users per 100 people, while Nigeria’s population is 232,679,478 people, creating a sizeable base for online product discovery even where final purchase remains offline. The National Bureau of Statistics reports total merchandise trade of ₦36,604.83 billion in Q4 and ₦36,024.66 billion in Q1 2025, indicating large movement of goods through importers, wholesalers and domestic distribution channels. Hardware retail is well suited to omnichannel development because buyers often need exact specifications for pipes, cable ratings, fittings, fasteners, valves, tool accessories and safety products. Digital catalogues can reduce search time, while physical stores retain the advantage of inspection, negotiation, pickup and local delivery. Retailers that provide verified product listings, transparent stock availability, invoice-based B2B ordering and delivery coordination can serve contractors, artisans, facility managers and institutional buyers more efficiently than purely informal open-market channels.

Future Outlook

Over the next decade, Nigeria Hardware Stores Retail Market is expected to expand steadily, supported by housing repairs, informal building activity, infrastructure development, artisan procurement and power-resilience purchases. The forecasted CAGR for 2026-2035 is estimated at 6.1%, with growth shaped by urbanization, construction-led demand, electrical backup products, online catalogues and expansion of organized B2B procurement models. Hardware stores will remain highly relevant because Nigerian consumers and contractors often buy building inputs in stages. Owner-builders require cement, roofing sheets, plumbing products, electrical inputs, fasteners, paints and tools throughout the construction cycle. Artisans such as electricians, plumbers, welders, carpenters, masons and painters create recurring demand for tools, accessories, consumables and replacement parts. The future market will not shift fully online because physical inspection, negotiation, local availability and informal credit remain important in Nigeria. However, online hardware discovery will grow for tools, power products, safety products, electrical accessories and industrial supplies. Platforms and specialist online stores will help buyers compare brands, check availability and arrange delivery. The strongest opportunities will emerge in Lagos, Abuja, Port Harcourt, Kano, Ogun and Onitsha due to port access, industrial activity, public infrastructure, estate development and open-market trade networks. Retailers that combine transparent pricing, product authenticity, local delivery, WhatsApp ordering, contractor accounts and reliable sourcing will be best positioned. The main risks will remain naira volatility, inflation, import dependence, counterfeit products, logistics constraints and fragmented competition.

Major Players

- Mamtus Nigeria

- GZ Industrial Supplies Nigeria

- Gibadi Online Store

- Jumia Nigeria Hardware Sellers

- Konga Hardware Sellers

- Jiji Nigeria Hardware and Building Materials Sellers

- Kara Nigeria

- Deinde Online Marketplace

- Mantrac Nigeria

- Jubaili Bros Nigeria

- Mikano International

- Fouani Nigeria

- Coleman Technical Industries

- Cutix PLC

- Berger Paints Nigeria Retail Network

Key Target Audience

- Hardware store chains and independent hardware retailers

- Building-material yards and open-market hardware traders

- Electrical, plumbing and sanitaryware distributors

- Power tool, hand tool and fastener manufacturers

- Construction contractors, artisans and installer networks

- Real estate developers and facility maintenance companies

- Investments and venture capitalist firms

- Government and regulatory bodies, including National Bureau of Statistics, Standards Organisation of Nigeria, Federal Ministry of Industry, Trade and Investment, Federal Inland Revenue Service, Nigeria Customs Service, Federal Ministry of Works and Federal Competition and Consumer Protection Commission

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map for Nigeria Hardware Stores Retail Market. This includes open-market traders, independent hardware stores, building-material yards, industrial suppliers, electrical distributors, plumbing counters, artisans, contractors, online marketplaces and regulatory bodies. The objective is to identify core variables such as product category mix, store format, customer type, channel structure, region and procurement behaviour.

Step 2: Market Analysis and Construction

In this phase, historical and current data is compiled from retail trade, construction, import, macroeconomic and company-level indicators. A top-down approach is used to benchmark the market from DIY, hardware and building-material retail categories, while bottom-up modelling assesses revenue by product category, store format, city cluster and customer group. This helps capture both organized and informal retail structures.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted telephone interviews with hardware retailers, importers, wholesalers, contractors, electricians, plumbers, painters, artisans, online sellers and distributor representatives. These interviews are used to verify fast-moving SKUs, informal credit behaviour, open-market trade dynamics, price sensitivity, brand preference, delivery requirements and product authenticity concerns across Nigerian hardware channels.

Step 4: Research Synthesis and Final Output

The final phase integrates desk research, expert inputs, public macroeconomic data, company information and bottom-up modelling into a structured market report. The output includes market size, segmentation, competitive benchmarking, future outlook and strategic recommendations. The report is designed for business professionals evaluating investment, distribution, expansion, procurement and channel strategy in Nigeria’s hardware retail ecosystem.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Hardware Retail Scope, Building Materials Retail Scope, DIY and Contractor Boundary, Open-Market Retail Boundary, Top-Down Market Sizing Approach, Bottom-Up Store Revenue Modelling, SKU-Level Benchmarking, Primary Interviews with Retailers/Contractors/Distributors/Importers, Market Cluster Checks, Import Flow Review, Limitations and Future Conclusions)

- Definition and Scope

- Market Genesis and Evolution

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (Urbanization, Residential Construction, Informal Housing Upgrades, Infrastructure Development, Artisan Workforce, Power Backup Demand, Real Estate Expansion, Online Retail Adoption)

- Market Challenges (Naira Volatility, Import Dependence, Inflation, Counterfeit Products, Fragmented Retail, Logistics Bottlenecks, Credit Risk, Poor Standards Enforcement, Power Cost Pressure)

- Market Opportunities (Formal Hardware Chains, Digital Catalogues, Contractor Loyalty, Private Label Tools, Certified Electrical Products, Solar-Linked Hardware, Rural Hardware Penetration, B2B Procurement Platforms)

- Market Trends (Hybrid Retail, WhatsApp Ordering, Open-Market Digitization, Professional Tool Premiumization, Value Brand Growth, Solar Accessory Bundling, Local Building Material Sourcing, Retailer-Led Delivery)

- SWOT Analysis

- Porter’s Five Forces Analysis

- By Retail Revenue (2020-2025)

- By Number of Hardware and Building-Material Retail Outlets (2020-2025)

- By Average Revenue per Store (2020-2025)

- By Product Category (In Value %)

Building Materials

Hand Tools

Power Tools

Fasteners and Fixings - By Store Format (In Value %)

Open-Market Hardware Shops

Independent Neighbourhood Hardware Stores

Building-Material Yards

Specialist Tool and Equipment Stores

Electrical and Plumbing Trade Counters - By Customer Type (In Value %)

DIY Households

Owner-Builders

Professional Contractors

Artisans and Trade Professionals

Facility and Property Maintenance Buyers - By Region (In Value %)

Lagos

Federal Capital Territory

Rivers and South-South Region

Kano and Northern Commercial Corridor

Ogun and Oyo

- Market Share of Major Players (Retail Revenue, Store Count, Regional Footprint, Category Sales, Contractor Account Base, Online Visibility)

- Cross Comparison Parameters (Regional Footprint, SKU Depth by Product Category, Open-Market vs Organized Retail Presence, Contractor and Artisan Penetration, E-Commerce and Delivery Capability, Import and Supplier Network, Product Authenticity and Warranty Support, Building-Material and Power-Backup Category Strength)

- Pricing Analysis Basis Key Hardware SKUs (Cordless Drill, Angle Grinder, Screwdriver Set, Cement Bag, Steel Rod, PVC Pipe, Electrical Cable, Silicone Sealant, Door Lock, Roofing Sheet, Safety Boots, Generator Changeover Switch)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Competitors

Mamtus Nigeria

GZ Industrial Supplies Nigeria

Gibadi Online Store

Jumia Nigeria Hardware Sellers

Konga Hardware Sellers

Jiji Nigeria Hardware and Building Materials Sellers

Kara Nigeria

Deinde Online Marketplace

Mantrac Nigeria

Jubaili Bros Nigeria

Mikano International

Fouani Nigeria

Coleman Technical Industries

Cutix PLC

Berger Paints Nigeria Retail Network

- DIY and Household Customer Analysis

- Owner-Builder Analysis

- Contractor and Artisan Analysis

- Trade Professional Analysis

- Facility Maintenance Buyer Analysis

- By Retail Revenue (2026-2035)

- By Number of Hardware and Building-Material Retail Outlets (2026-2035)

- By Average Revenue per Store (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now