Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Nigeria home finance market is projected to reach USD ~ billion, driven by factors such as increased urbanization, a growing middle class, and a rising demand for affordable housing. The adoption of various mortgage schemes by both government and private institutions has significantly contributed to this growth. Additionally, favorable interest rates, increasing housing development projects, and enhanced access to financial services are expected to further stimulate the market’s growth, providing home finance solutions to more Nigerians.

The key dominant regions in Nigeria’s home finance market are Lagos, Abuja, and Port Harcourt, driven by their economic significance, population density, and infrastructure development. Lagos remains the financial hub, offering diverse housing options and housing finance schemes. Abuja, as the capital city, also presents substantial growth due to government policies that promote homeownership and the expansion of residential areas. Port Harcourt, with its growing industrial base, also contributes to the increasing demand for home finance in the region.

Market Segmentation

By Product Type

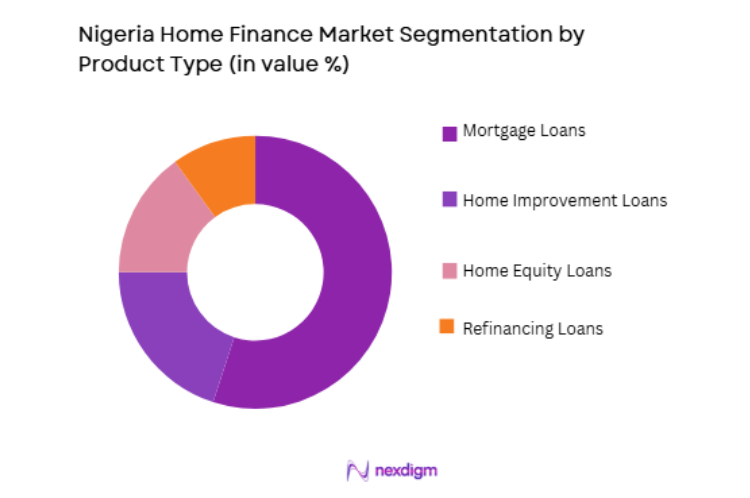

The Nigeria home finance market is segmented by product type into mortgage loans, home improvement loans, home equity loans, and refinancing loans. Mortgage loans have the dominant market share, primarily due to the rising demand for homeownership as more Nigerians seek financial products to afford homes. The government’s initiatives, such as the National Housing Fund (NHF), alongside the low-interest mortgage options provided by banks, have made homeownership more accessible. These loans cater to a growing middle class that increasingly views owning a home as a significant long-term investment.

By Distribution Channel

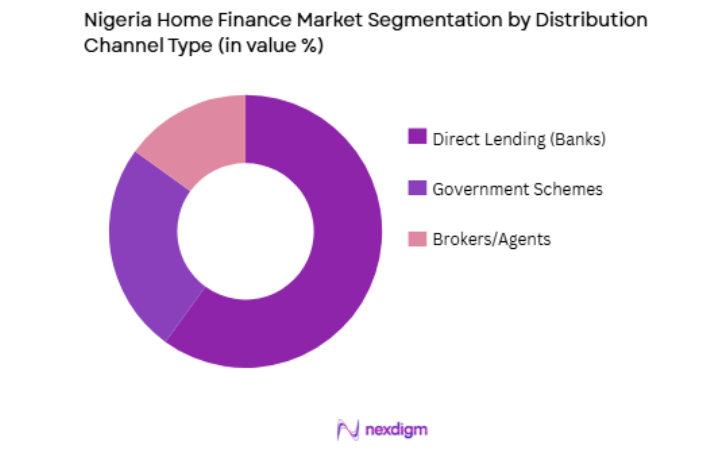

The Nigeria home finance market is segmented by distribution channel into direct lending from banks, government-backed schemes, and brokers/agents. Direct lending through banks holds the dominant market share, driven by their established reputation, customer trust, and access to capital. Nigerian banks continue to expand their lending services, offering home loans with flexible terms to meet the growing demand for homeownership. Government-backed schemes like the NHF and Federal Mortgage Bank of Nigeria (FMBN) also play a critical role in making home finance more affordable, though they cater to a more specific demographic.

Competitive Landscape

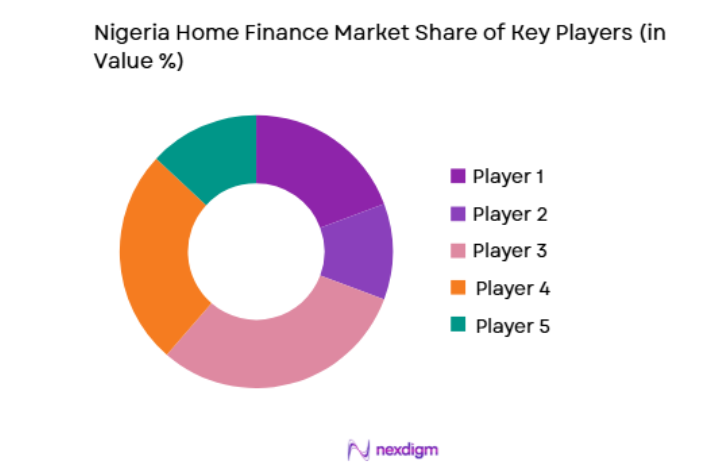

The Nigerian home finance market is highly competitive, with both established financial institutions and new entrants vying for market share. Key players, such as commercial banks and microfinance institutions, offer a variety of loan products tailored to different customer needs. Additionally, the involvement of government-backed mortgage schemes adds further competition to the sector. The market is seeing gradual consolidation as banks partner with real estate developers and technology firms to offer innovative home finance solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Million) | Key Service Areas |

| First Bank of Nigeria | 1894 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| Stanbic IBTC Bank | 1989 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| Access Bank | 1989 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| FBNQuest | 1994 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| Union Bank | 1917 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

Nigeria Home Finance Market Analysis

Growth Drivers

Government Housing Initiatives

One of the major growth drivers in Nigeria’s home finance market is the government’s active involvement in promoting homeownership through various initiatives. Programs like the National Housing Fund (NHF) and the Federal Mortgage Bank of Nigeria (FMBN) provide low-interest mortgage loans and subsidies for homebuyers, especially for the low and middle-income populations. Furthermore, the government’s commitment to infrastructure development and building affordable housing has made it easier for more Nigerians to access home finance products. These initiatives are especially beneficial in urban areas where housing demand is highest. As the government continues to push for greater access to affordable housing, these programs are expected to play a pivotal role in driving the market’s growth.

Technological Advancements and Digital Lending

The rapid advancement of digital banking platforms has facilitated the growth of home finance solutions in Nigeria. Mobile and online banking platforms now allow customers to easily apply for home loans, check eligibility, and track the progress of their applications, reducing the barriers to accessing home finance. Additionally, the rise of fintech startups providing digital mortgage services has increased the availability of home loan products, making it easier for potential buyers to find competitive offers. Technology has also improved the loan approval process, with many banks utilizing digital tools and AI to offer faster and more efficient services. These technological advancements are critical in making home loans more accessible to a larger portion of the population and are expected to continue driving growth in the market.

Market Challenges

High Interest Rates and Affordability

One of the key challenges faced by the Nigeria home finance market is the high interest rates on home loans. While banks and financial institutions offer various home loan products, many Nigerians find these loans unaffordable due to high interest rates and lengthy repayment terms. This is exacerbated by inflation and economic instability, which make it more difficult for individuals to save for a down payment. Consequently, many potential homebuyers are either unable to afford homes or are forced to look for less expensive and substandard housing options. Efforts to lower interest rates and introduce more affordable financing options are essential to make homeownership accessible to a broader segment of the population.

Lack of Financial Literacy and Awareness

Another significant challenge is the lack of financial literacy among a large portion of the Nigerian population. Many potential homebuyers are unaware of the various home finance products available to them, or they lack the knowledge to navigate the complex process of securing a mortgage. Without proper education on how to manage personal finances, invest in property, or take advantage of government-backed housing schemes, many Nigerians continue to be excluded from the home finance market. To address this, financial institutions and the government need to invest in consumer education programs that teach individuals about home financing options, the benefits of owning property, and the process of securing home loans.

Opportunities

Affordable Housing Development

As the Nigerian middle class continues to grow, the demand for affordable housing is expected to increase. This presents a significant opportunity for both financial institutions and real estate developers to cater to this market segment by offering affordable home loan products and developing low-cost housing units. Many Nigerians are eager to own their homes, but the high costs of construction and purchasing property in urban centers make it difficult for them to do so. By focusing on the development of affordable housing, banks and developers can tap into an underserved market, while also contributing to the country’s economic development and urbanization goals.

Fintech Solutions and Digital Mortgages

The rise of fintech companies and digital mortgage platforms offers an exciting opportunity in Nigeria’s home finance market. These platforms allow homebuyers to access financial services more conveniently and at lower costs, particularly for younger, tech-savvy consumers. With mobile banking and digital applications becoming more prevalent, fintech solutions can help reduce the cost of accessing home loans, making homeownership more attainable. These solutions also allow for faster loan approvals, more flexible repayment options, and improved customer service, all of which contribute to the overall growth of the home finance market in Nigeria. As more Nigerians turn to online platforms for financial services, this trend is expected to continue growing in the coming years.

Future Outlook

The future outlook for the Nigeria home finance market is promising, driven by continued urbanization, the growing middle class, and advancements in digital technology. The demand for home loans and affordable housing will likely rise, fueled by government housing initiatives and the increased availability of digital mortgage services. Technological advancements, particularly in mobile banking and fintech platforms, will further drive growth by improving accessibility and efficiency in the home finance sector. Regulatory support and increased financial literacy programs will also play vital roles in shaping the future of the market, making homeownership more attainable for a broader segment of the Nigerian population.

Major Players

- First Bank of Nigeria

- Stanbic IBTC Bank

- Access Bank

- FBNQuest

- Union Bank

- Zenith Bank

- GTBank

- UBA

- Diamond Bank

- Fidelity Bank

- Citibank

- HSBC

- Standard Chartered

- Ecobank

- Wema Bank

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Financial institutions

- Housing developers

- Homebuyers

- Insurance companies

- Mortgage brokers

- Real estate investors

Research Methodology

Step 1: Identification of Key Variables

The first step in market research is identifying key variables, such as government policies, housing demand, interest rates, and demographic factors, that influence the home finance market in Nigeria.

Step 2: Market Analysis and Construction

The market is segmented into product types, distribution channels, and consumer profiles. Comprehensive analysis is done through a combination of market surveys, financial reports, and industry consultations.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions are validated through consultations with industry experts, including bankers, real estate developers, and financial advisors, to ensure the accuracy of the insights and forecast.

Step 4: Research Synthesis and Final Output

The data collected is synthesized into comprehensive reports, offering key insights into market growth drivers, challenges, and opportunities. The final report provides actionable insights for stakeholders in the home finance sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Urbanization and Population Growth

Government Support for First-time Homebuyers

Rise in Property Values and Investment Opportunities - Market Challenges

High Loan Default Rates

Regulatory Compliance Costs

Limited Access to Financing in Rural Areas - Market Opportunities

Increasing Middle-Class Population

Shift to Online Mortgage Platforms

Integration of Smart Home Financing Solutions - Trends

Shift Toward Digital Lending Solutions

Growth in Green and Sustainable Home Financing - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Mortgage Lending

Home Loan Insurance

Property Investment Financing

Renovation Financing

Real Estate Backed Securities - By Platform Type (In Value%)

Online Platforms

Traditional Banks

Non-Banking Financial Companies (NBFCs)

Mortgage Brokers

Fintech Solutions - By Fitment Type (In Value%)

Owner-Occupied Financing

Rental Property Financing

Refinancing Options

Government Subsidized Programs - By End User Segment (In Value%)

Homebuyers

Property Investors

Real Estate Developers

- Market Share Analysis

- Cross Comparison Parameters (Loan Amount, Interest Rate, Loan Tenure, Lender Type, Customer Type, Property Type, Loan-to-Value Ratio, Default Rate, Processing Time, Repayment Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Standard Bank

ABSA Bank

First National Bank (FNB)

Nedbank

Investec

Capitec

SA Home Loans

HSBC South Africa

Old Mutual

SANTAM

Renasa Insurance

Momentum Metropolitan

Woolworths Financial Services

AfrAsia Bank

Nedgroup Investments

- Increased Demand for Affordable Housing

- Rise in Single-Property Investments

- Preference for Long-Term Financing

- Adoption of Digital Mortgage Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now