Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Nigeria last-mile delivery market is valued at approximately USD ~ Billion based on a recent historical assessment, supported by the rapid expansion of e-commerce platforms, urban retail logistics, and food delivery services. Data from the Nigerian Communications Commission and the National Bureau of Statistics indicates that the increasing number of digital transactions and online retail orders significantly expands parcel delivery demand. Logistics companies invest in fleet expansion, digital tracking systems, and urban distribution hubs, strengthening delivery capacity and supporting sustained growth of last-mile logistics operations nationwide.

Major logistics activity is concentrated in Lagos, Abuja, and Port Harcourt because these cities function as the country’s primary commercial, administrative, and consumer markets. Lagos dominates logistics operations due to its dense population, large retail sector, and the presence of major e-commerce fulfillment centers and logistics headquarters. Abuja serves as a central distribution hub supporting administrative institutions and corporate offices, while Port Harcourt benefits from oil industry supply chains and port connectivity, enabling efficient parcel distribution across southern Nigeria’s commercial corridors.

Market Segmentation

By Product Type

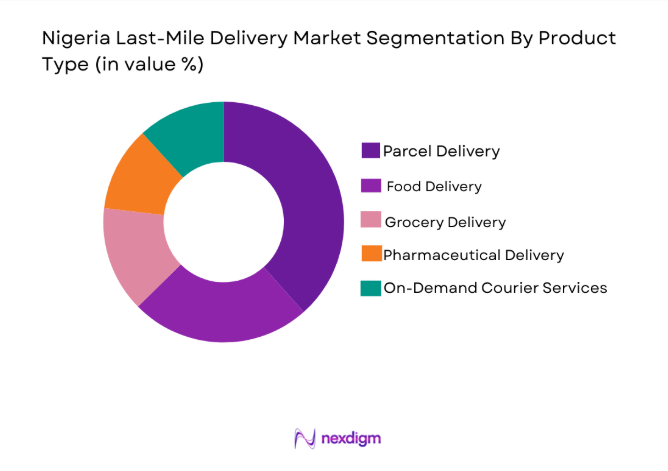

Nigeria Last-Mile Delivery market is segmented by product type into Parcel Delivery, Food Delivery, Grocery Delivery, Pharmaceutical Delivery, and On-Demand Courier Services. Recently, Parcel Delivery has a dominant market share due to the rapid expansion of e-commerce platforms and rising consumer demand for home delivery of retail products. Large online marketplaces and retailers rely heavily on parcel delivery networks to transport consumer electronics, fashion goods, and household items from distribution centers to customers. Logistics providers therefore expand sorting hubs, delivery fleets, and digital tracking platforms designed to process high volumes of e-commerce shipments efficiently.

By Platform Type

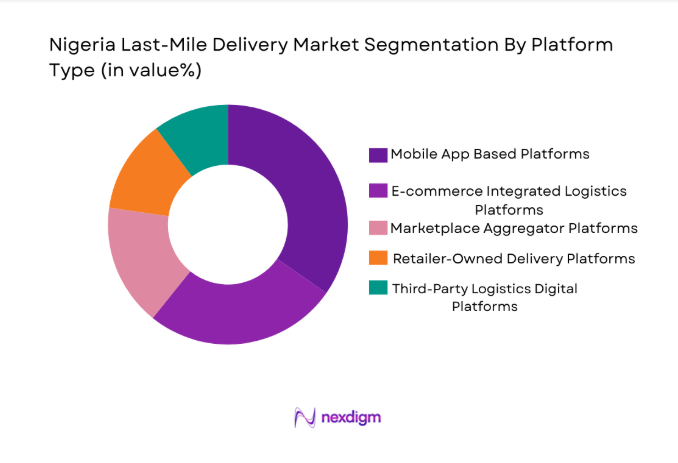

Nigeria Last-Mile Delivery market is segmented by platform type into Mobile App Based Platforms, E-commerce Integrated Logistics Platforms, Marketplace Aggregator Platforms, Retailer-Owned Delivery Platforms, and Third-Party Logistics Digital Platforms. Recently, Mobile App Based Platforms have a dominant market share due to widespread smartphone usage and the growth of app-based delivery aggregators that connect consumers with delivery drivers in real time. These platforms enable customers to track deliveries, schedule pickups, and make digital payments, improving convenience and operational efficiency while enabling logistics companies to process large volumes of urban deliveries across densely populated cities.

Competitive Landscape

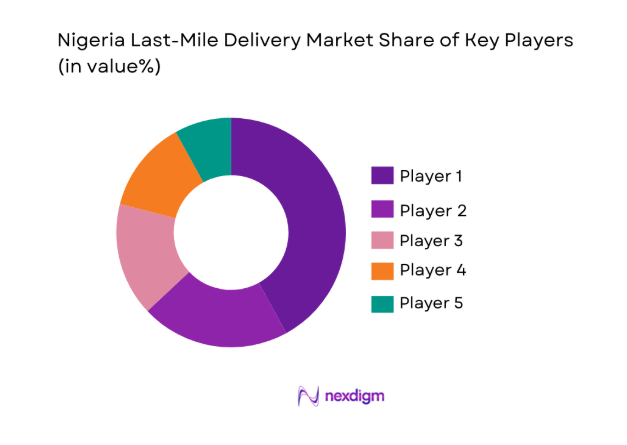

The Nigeria last-mile delivery market is moderately fragmented, with both domestic logistics companies and international courier operators competing for e-commerce and parcel delivery contracts. Major players focus on expanding delivery fleets, strengthening digital logistics platforms, and building urban fulfillment networks to improve delivery speed and service reliability. Strategic partnerships with e-commerce platforms, retail chains, and food delivery providers strengthen market positioning, while investment in automated sorting facilities and real-time parcel tracking technologies enhances operational efficiency across nationwide logistics networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet Capacity |

| GIG Logistics | 2012 | Lagos, Nigeria | Digital logistics platforms | ~ | ~ | ~ | ~ |

| Jumia Logistics | 2012 | Lagos, Nigeria | E-commerce fulfillment systems | ~ | ~ | ~ | ~ |

| DHL Nigeria | 1978 | Lagos, Nigeria | Global logistics technology | ~ | ~ | ~ | ~ |

| UPS Nigeria | 1991 | Lagos, Nigeria | Integrated logistics systems | ~ | ~ | ~ | ~ |

| Red Star Express | 1992 | Lagos, Nigeria | Courier and logistics technology | ~ | ~ | ~ | ~ |

Nigeria Last-Mile Delivery Market Analysis

Growth Drivers

Expansion of E-commerce Platforms and Digital Retail Ecosystems

The rapid expansion of digital retail platforms across Nigeria significantly increases demand for last-mile delivery services capable of transporting high volumes of parcels from fulfillment centers to residential and commercial consumers. Online marketplaces, social commerce platforms, and direct-to-consumer brands increasingly rely on logistics partners to complete the final stage of order distribution efficiently across urban and semi-urban markets. Rising smartphone penetration and mobile internet accessibility enable millions of consumers to place online orders through digital platforms, directly increasing parcel movement throughout national delivery networks. Retailers integrate digital inventory management and automated order processing systems that require synchronized delivery operations capable of meeting short delivery timelines. Logistics providers respond by expanding urban distribution hubs, delivery fleets, and route optimization technologies designed to handle large volumes of daily shipments. Investments in automated sorting systems and real-time parcel tracking platforms further enhance operational efficiency and transparency for both retailers and consumers. As online shopping habits continue strengthening among urban populations, parcel delivery services become an essential component of Nigeria’s retail distribution infrastructure. These structural changes position last-mile delivery networks as a core logistics layer supporting the continuous expansion of Nigeria’s digital commerce ecosystem and consumer goods distribution channels nationwide.

Rapid Urbanization and Rising Demand for Hyperlocal Delivery Services

Nigeria’s accelerating urban population growth significantly strengthens demand for efficient last-mile logistics capable of supporting high-density consumer markets across major metropolitan areas. Large cities such as Lagos, Abuja, and Port Harcourt experience continuous expansion of residential neighborhoods, commercial districts, and retail infrastructure that collectively generate substantial parcel delivery requirements. Dense urban environments encourage businesses to adopt rapid delivery models that enable consumers to receive orders within hours rather than days. Restaurants, grocery retailers, pharmacies, and convenience stores increasingly integrate digital ordering systems linked directly with courier platforms responsible for immediate delivery services. Logistics companies therefore deploy motorcycle fleets, compact delivery vans, and micro distribution hubs strategically positioned near high demand neighborhoods. Hyperlocal delivery networks supported by mobile applications and real-time dispatch systems allow companies to process thousands of daily delivery requests within city boundaries. Businesses also expand partnerships with delivery aggregators that provide scalable logistics capacity without requiring retailers to operate their own fleets. As urban consumption continues increasing alongside population density, demand for efficient last-mile delivery solutions strengthens across Nigeria’s rapidly expanding metropolitan economies.

Market Challenges

Urban Traffic Congestion and Inadequate Transportation Infrastructure

Severe traffic congestion across major Nigerian cities creates significant operational difficulties for last-mile delivery providers attempting to maintain predictable delivery schedules. Urban road networks in cities such as Lagos and Abuja experience persistent congestion caused by high vehicle density, limited road expansion, and inconsistent traffic management systems. Delivery fleets frequently encounter delays that extend delivery timelines and reduce the number of orders drivers can complete within a single operational shift. These inefficiencies increase operational costs because logistics companies must deploy additional vehicles and drivers to maintain service levels across densely populated areas. Congestion also increases fuel consumption and vehicle maintenance requirements, further raising logistics operating expenses for delivery providers. Businesses relying on same-day delivery commitments face particular challenges when traffic conditions prevent drivers from meeting promised service timelines. Delivery companies attempt to mitigate these disruptions by utilizing motorcycle fleets and advanced route optimization technologies capable of navigating congested road corridors. However, infrastructure limitations continue to create unpredictable delivery cycles and reduce operational efficiency across Nigeria’s urban logistics ecosystem.

Addressing and Location Identification Limitations in Urban and Semi-Urban Areas

Many areas across Nigeria lack standardized addressing systems, creating operational challenges for delivery companies attempting to accurately locate customer destinations. Informal settlements, newly developed residential areas, and rapidly expanding urban neighborhoods often do not possess clearly defined street numbering or consistent mapping infrastructure. Delivery drivers frequently rely on verbal directions, landmarks, or phone communication with customers to identify final delivery locations. These additional steps significantly extend delivery time per order and reduce overall fleet productivity for logistics companies. Inconsistent addressing also increases the risk of failed delivery attempts when drivers cannot accurately locate the recipient’s address during the first visit. Logistics providers attempt to mitigate these difficulties through mobile navigation tools, customer location pin sharing, and digital address verification systems integrated into delivery applications. Despite these technological solutions, large portions of urban and suburban regions still lack precise mapping infrastructure required for efficient logistics operations. As a result, addressing limitations remain a persistent structural barrier affecting delivery speed, operational costs, and service reliability across Nigeria’s last-mile logistics networks.

Opportunities

Expansion of Hyperlocal Commerce and On-Demand Delivery Platforms

The rapid growth of hyperlocal commerce platforms creates significant opportunities for logistics providers to expand on-demand delivery services across Nigeria’s urban consumer markets. Restaurants, grocery stores, pharmacies, and convenience retailers increasingly adopt digital ordering platforms that require immediate delivery fulfillment within short time windows. Consumers prefer fast delivery for daily essentials, prepared food, and household goods, encouraging businesses to integrate real-time logistics capabilities into their retail operations. Delivery aggregators provide technology platforms that connect merchants, drivers, and customers through mobile applications capable of managing thousands of orders simultaneously. Logistics companies therefore expand fleets of motorcycles and small delivery vehicles designed specifically for rapid urban transportation. Strategic partnerships between retailers and logistics providers further strengthen hyperlocal delivery ecosystems that allow businesses to serve nearby consumers efficiently. Urban micro-fulfillment hubs also emerge as critical infrastructure supporting fast order processing and dispatch across densely populated districts. As digital ordering continues expanding among urban consumers, hyperlocal logistics services offer delivery companies substantial growth opportunities throughout Nigeria’s evolving retail distribution landscape.

Adoption of Logistics Technology and Data Driven Fleet Optimization Systems

Advanced logistics technologies present significant opportunities for last-mile delivery providers to improve operational efficiency and scale their distribution networks across Nigeria. Route optimization software powered by data analytics allows logistics companies to design delivery routes that reduce travel distance, minimize fuel consumption, and increase driver productivity. Real-time parcel tracking platforms improve shipment visibility for retailers and consumers while enabling logistics companies to monitor delivery progress and address operational disruptions immediately. Automated dispatch systems match delivery drivers with orders based on location proximity and vehicle availability, improving order allocation efficiency across large fleets. Digital payment integration further streamlines order processing by enabling customers to complete transactions directly within delivery applications. Logistics providers also deploy data analytics platforms capable of forecasting delivery demand across different neighborhoods and time periods. These predictive systems help companies allocate vehicles, drivers, and warehouse resources more effectively throughout urban logistics networks. Continuous adoption of logistics technology therefore creates substantial opportunities for delivery companies to expand service capacity, reduce operational costs, and strengthen service reliability across Nigeria’s growing last-mile delivery industry.

Future Outlook

The Nigeria Last-Mile Delivery Market is expected to experience steady expansion as digital commerce ecosystems continue strengthening across major urban regions. Technology-driven logistics platforms, route optimization systems, and mobile delivery applications will significantly improve operational efficiency across delivery networks. Increasing urban population density and rising online retail adoption will continue generating high parcel volumes requiring efficient delivery infrastructure. Supportive regulatory initiatives encouraging digital payments and logistics modernization will further strengthen distribution networks. Continued investments in delivery fleets, automated sorting systems, and hyperlocal fulfillment hubs will support long-term growth of the Nigeria Last-Mile Delivery Market.

Major Players

- GIG Logistics

- Jumia Logistics

- DHL Nigeria

- UPS Nigeria

- FedEx Nigeria

- Red Star Express

- CourierPlus Nigeria

- Kwik Delivery

- Sendbox

- Max.ng

- Kobo360

- Glovo Nigeria

- Bolt Food

- Chowdeck

- Tranex Nigeria

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- E-commerce platforms

- Logistics and courier companies

- Retail and consumer goods companies

- Technology platform providers

- Food delivery and grocery delivery platforms

Research Methodology

Step 1: Identification of Key Variables

The Nigeria Last-Mile Delivery Market research begins with identifying critical market variables including delivery infrastructure, logistics technology adoption, e-commerce transaction growth, and urban distribution patterns. These variables establish the foundation for evaluating market dynamics and operational structures. Industry publications, logistics databases, and regulatory reports support the identification process.

Step 2: Market Analysis and Construction

Market construction for the Nigeria Last-Mile Delivery Market involves evaluating supply chain structures, logistics provider networks, and parcel delivery ecosystems across major cities. Data from logistics associations, digital commerce platforms, and transportation infrastructure reports is analyzed to construct the market structure. This step establishes relationships between demand drivers and delivery network expansion.

Step 3: Hypothesis Validation and Expert Consultation

Findings from preliminary analysis are validated through consultation with logistics executives, supply chain specialists, and e-commerce operations professionals. Expert interviews help confirm operational patterns, delivery demand trends, and technology adoption levels within the Nigeria Last-Mile Delivery Market. Industry feedback ensures that market assumptions reflect realistic operational conditions.

Step 4: Research Synthesis and Final Output

The final stage consolidates validated insights into a structured research framework describing the Nigeria Last-Mile Delivery Market. Market segmentation, competitive landscape evaluation, and operational dynamics are synthesized into a comprehensive report. The final output provides strategic insights supporting decision-making for stakeholders across logistics and digital commerce ecosystems.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-commerce Platforms and Online Retail Transactions

Rapid Urbanization Increasing Urban Parcel Demand

Growth of Digital Payment Ecosystems Enabling Online Commerce - Market Challenges

Urban Traffic Congestion and Infrastructure Limitations

High Logistics Operating Costs and Fuel Price Volatility

Addressing and Delivery Location Identification Constraints - Market Opportunities

Expansion of Same Day and On Demand Delivery Services

Growth of Micro Fulfillment Centers in Urban Areas

Adoption of Electric Delivery Vehicles and Sustainable Logistics - Trends

Expansion of Mobile App Based Delivery Aggregators

Growth of Hyperlocal Delivery Networks Across Major Cities - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Courier Delivery Services

Food and Grocery Delivery Services

E-commerce Order Fulfillment Delivery

Pharmaceutical and Healthcare Delivery

On-Demand Express Delivery Services - By Platform Type (In Value%)

Mobile App Based Delivery Platforms

Integrated E-commerce Logistics Platforms

Marketplace Aggregator Delivery Platforms

Direct Retailer Delivery Platforms

Third-Party Logistics Digital Platforms - By Fitment Type (In Value%)

In-House Retailer Delivery Networks

Third-Party Logistics Partnerships

Crowdsourced Delivery Networks

Hybrid Delivery Operations - By End User Segment (In Value%)

E-commerce Retailers

Food and Grocery Platforms

Healthcare and Pharmaceutical Providers

- Market Share Analysis

- Cross Comparison Parameters (Service Coverage Network, Delivery Speed Capability, Technology Platform Integration, Fleet Size and Vehicle Mix, Urban Fulfillment Infrastructure, Pricing Structure, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

- GIG Logistics

Kwik Delivery

Jumia Logistics

DHL Nigeria

UPS Nigeria

FedEx Nigeria

Sendbox

Max.ng

CourierPlus Nigeria

Red Star Express

Tranex Nigeria

Kobo360

Glovo Nigeria

Bolt Food

Chowdeck

- E-commerce Platforms Driving High Parcel Volumes

- Food Delivery Platforms Expanding Hyperlocal Logistics Networks

- Healthcare Sector Increasing Demand for Medical Deliveries

- Retail Chains Integrating Omnichannel Distribution Models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now