Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Nigeria Oral Care Market is valued at USD ~ million, as per Nexdigm’s base-year market assessment, and is forecast by the same source to reach USD ~ million by 2033 at 6.99% CAGR for 2026–2033; for the requested 2026–2035 horizon, this report applies the same published Nigeria-specific CAGR as the closest validated forecast benchmark. Growth is driven by daily toothpaste usage, pharmacy expansion, urban retail access, and oral-health concerns such as adolescent dental caries prevalence of 23.0% in Nigerian studies.

Lagos, Abuja, Kano, Ibadan, Port Harcourt and Onitsha dominate Nigeria oral care consumption because they concentrate urban households, pharmacies, supermarkets, wholesalers, dental clinics and modern trade visibility. Nigeria’s urban population is reported at 128.04 million and 55.03% of total population, while Lagos alone is estimated at 16.54 million metro population, giving brands immediate scale for toothpaste, toothbrush, mouthwash, sensitivity SKUs and promotional multipacks.

Market Segmentation

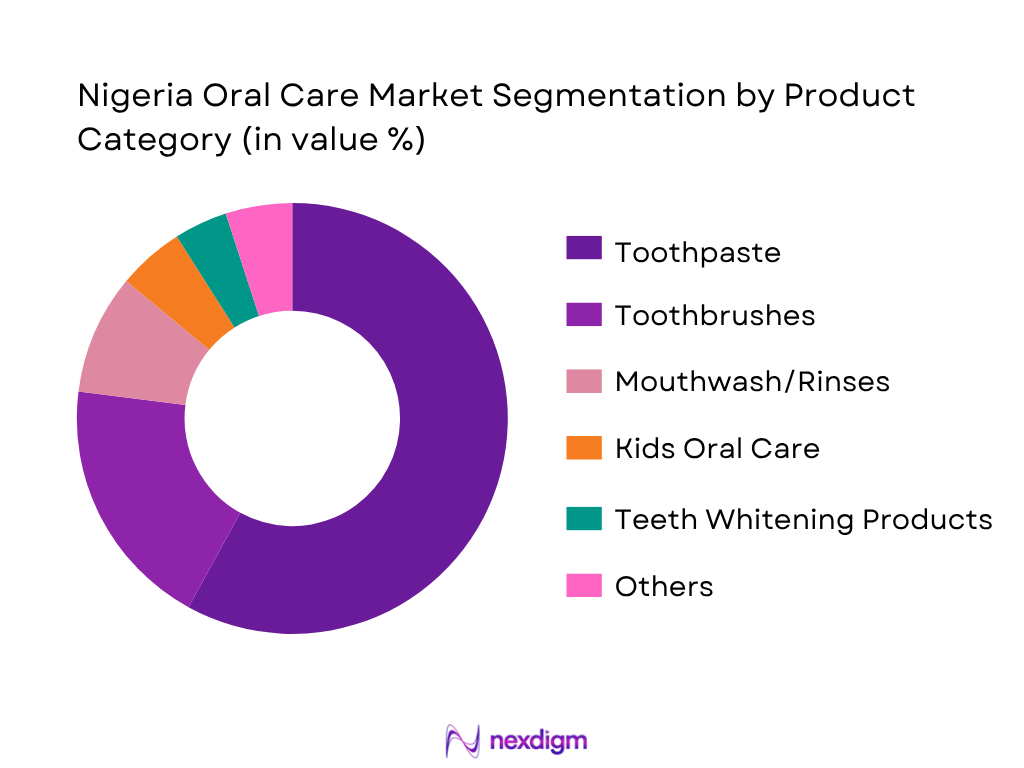

By Product Category

Nigeria Oral Care Market is segmented by product category into toothpaste, toothbrush, mouthwash/rinses, dental floss/interdental products, denture care, teeth whitening products and kids oral care. Toothpaste dominates the product category because it is the most habitual, highest-frequency oral care item and is available across open markets, supermarkets, chemists, pharmacies and online channels. Deep Market Insights identifies toothpaste as the largest Nigeria oral care product segment, while global oral care research also identifies toothpaste as the largest oral care category due to daily usage, affordability and wide SKU availability. In Nigeria, toothpaste dominance is reinforced by mass brands such as Closeup, Colgate, Pepsodent, Oral-B and Dabur, plus benefit-led variants such as fluoride, herbal, whitening, cavity protection and sensitivity formulations.

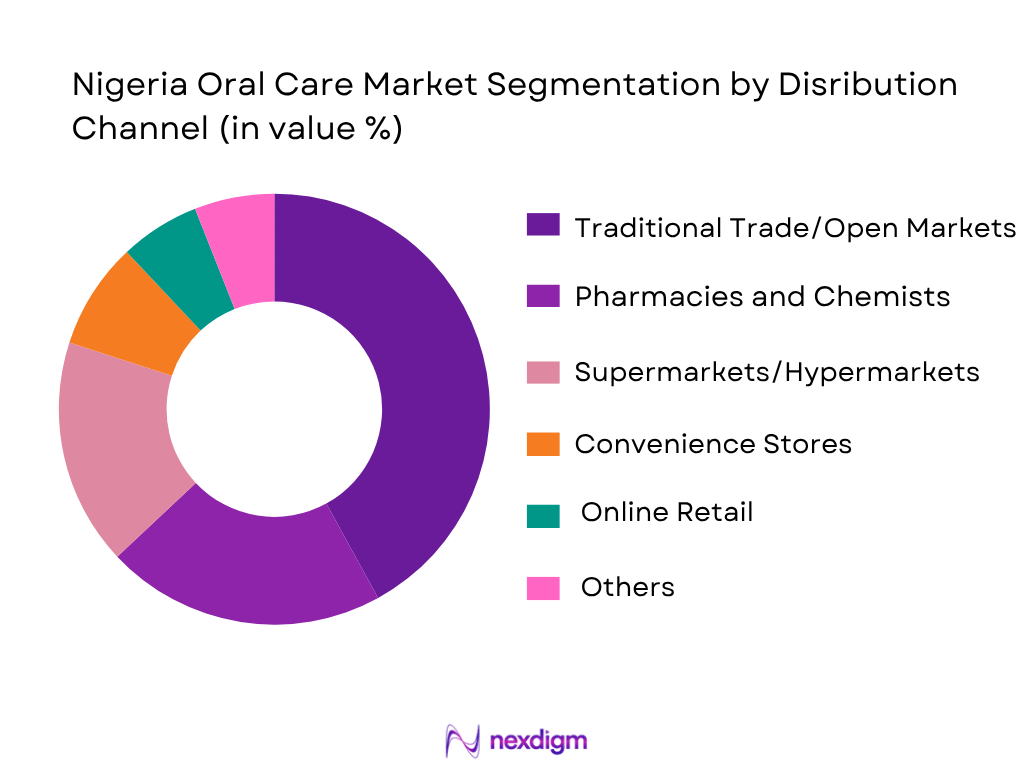

By Distribution Channel

Nigeria Oral Care Market is segmented by distribution channel into traditional trade/open markets, pharmacies and chemists, supermarkets/hypermarkets, convenience stores, online retail, dental clinics and wholesalers. Traditional trade/open markets dominate because they provide the widest household reach, especially for economy toothpaste tubes, manual toothbrushes and small-pack oral care products. Pharmacies and chemists are gaining importance for sensitivity toothpaste, mouthwash and dentist-recommended SKUs, while supermarkets support premiumization through family packs, multipacks and whitening products. Online retail is still smaller but relevant in Lagos and Abuja due to marketplace discovery, bundled offers and imported premium SKUs. Consumer-store dominance is consistent with broader oral care market research because shoppers prefer immediate availability, comparison across brands and frequent replenishment.

Competitive Landscape

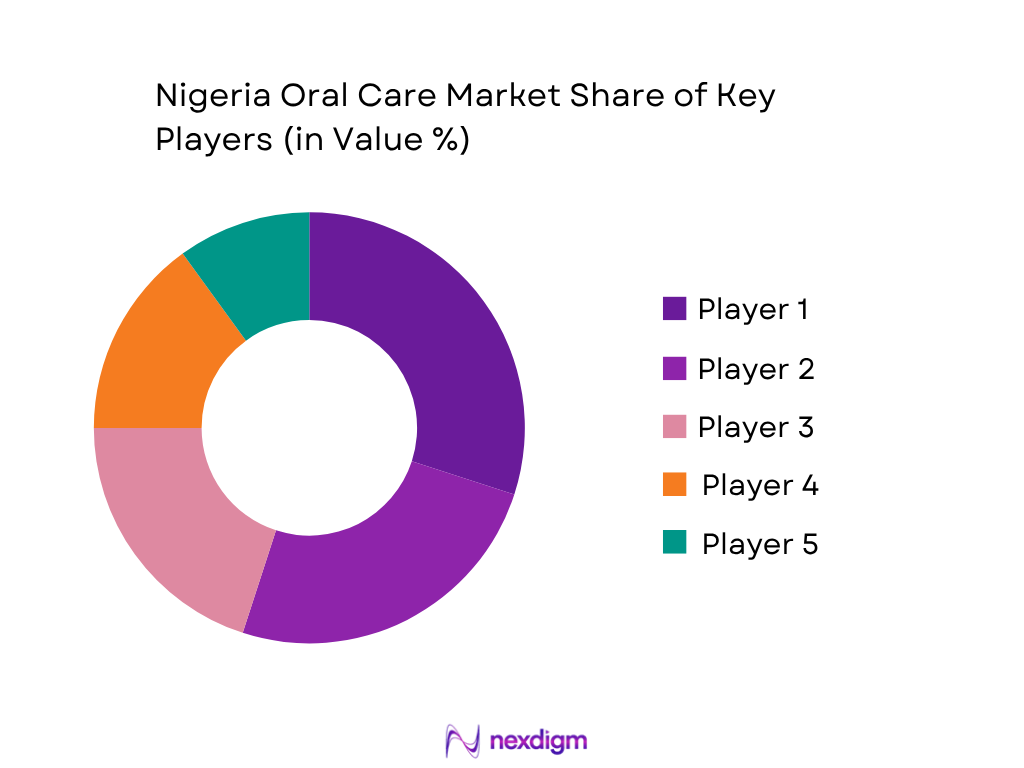

The Nigeria Oral Care Market is led by multinational FMCG brands and locally distributed mass-market brands. Colgate-Palmolive, Unilever, Procter & Gamble/Oral-B, Haleon/Sensodyne and Dabur-linked oral care brands compete across toothpaste, toothbrushes, sensitivity care, herbal formulations and pharmacy-led premium SKUs. Competition is shaped by price-pack architecture, traditional trade depth, pharmacy recommendation, dentist endorsement, fluoride/herbal claims and availability across Lagos, Abuja, Kano and other high-density retail corridors.

| Company | Establishment Year | Headquarters | Key Nigeria Oral Care Brands | Dominant Product Strength | Route-to-Market Strength | Price Positioning | Market-Specific Edge | Key Channel Focus |

| Colgate-Palmolive | 1806 | New York, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Unilever | 1929 | London, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Procter & Gamble | 1837 | Cincinnati, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Haleon | 2022 | Weybridge, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Dabur / African Consumer Care | 1884 | Ghaziabad, India | ~ | ~ | ~ | ~ | ~ | ~ |

Nigeria Oral Care Market Analysis

Growth Drivers

Population Base

Nigeria’s large consumer base directly supports repeat-demand oral care categories such as toothpaste, toothbrushes, mouthwash and children’s oral hygiene products. The World Bank reports Nigeria’s total population at 232,679,478 people in 2024, while UNFPA places Nigeria’s 2025 population at 237.5 million people, creating one of Africa’s largest daily-use hygiene consumer pools. The category benefits from household-level replenishment because toothpaste and toothbrushes are basic personal-care products used across income groups, schools, workplaces, pharmacies, chemists, supermarkets and open-market channels. The World Bank also reports 95,430,802 people aged 0–14 in Nigeria in 2024, which is highly relevant for kids toothpaste, soft-bristle toothbrushes, school oral-hygiene campaigns and family-pack demand. This population depth allows oral care brands to build volume through mass-market fluoride toothpaste and economy toothbrushes, while premium brands can target urban adults through pharmacies and modern retail.

Urbanization

Urbanization strengthens Nigeria Oral Care Market demand because oral care brands depend heavily on retail density, pharmacy access, dental clinics, supermarkets, chemists and distributor coverage. World Bank data shows Nigeria’s urban population reached 128,043,517 people in 2024, up from 123,701,699 people in 2023, adding more than 4.3 million urban residents in one year. This expansion is market-specific because urban consumers have higher access to toothpaste variants such as whitening, fresh-breath, herbal, sensitivity and gum-care products, while modern retail and pharmacies improve visibility for premium SKUs. Urban households also support higher replacement frequency for toothbrushes and wider trial of mouthwash compared with rural informal channels. For oral care companies, cities such as Lagos, Abuja, Kano, Ibadan, Port Harcourt and Onitsha become core distribution nodes because wholesalers, supermarkets, chemists, dentists and e-commerce operators are concentrated there. The same urban base also reduces route-to-market friction for multipacks and benefit-led toothpaste launches.

Market Challenges

FX Volatility

FX volatility is a direct challenge for Nigeria Oral Care Market because several toothpaste inputs, specialty formulations, toothbrushes, mouthwash SKUs, packaging materials and imported finished goods depend on foreign-currency procurement. The IMF reported that Nigeria’s exchange rate depreciated by another 40 in January–February 2024, while the World Bank’s official exchange-rate indicator is sourced from IMF International Financial Statistics and tracks Nigeria’s period-average local currency per U.S. dollar. This matters for oral care because imported dentifrices, toothbrushes, flavoring systems, active ingredients, bristles, electric toothbrushes and pharmacy-led sensitivity products are exposed to currency conversion risk before reaching distributors and retailers. UN Comtrade data shows Nigeria imported 48,550,700 toothbrush items from China in 2024, alongside 5,753,880 toothbrush items from Malaysia, showing how dependent the toothbrush category remains on international supply. When the naira moves sharply, oral care companies face tighter SKU planning, reduced promotional flexibility, and pressure to prioritize fast-moving mass toothpaste over slower premium items.

Import Cost

Import dependence remains a structural challenge for Nigeria Oral Care Market, especially across toothbrushes, oral/dental hygiene preparations, mouthwash-type products, premium dental-care SKUs and imported toothpaste variants. WITS/UN Comtrade reports Nigeria imported 231,898 kilograms of preparations for oral or dental hygiene under HS 330690 in 2024, with South Africa supplying 140,438 kilograms, China 69,674 kilograms, the United Arab Emirates 10,140 kilograms, Thailand 8,883 kilograms and India 420 kilograms. The same database shows toothbrush exports to Nigeria in 2024 from China at 48,550,700 items and Malaysia at 5,753,880 items, underscoring reliance on external supply for a core oral care product. This creates pressure for brand owners because oral care supply chains must manage freight, customs documentation, foreign exchange access and distributor working capital before products reach chemists, supermarkets and open markets. Import exposure is particularly relevant for sensitivity toothpaste, premium brushes, interdental products and mouthwash, where local production depth is limited and imported SKUs often define category availability.

Opportunities

Herbal Toothpaste

Herbal toothpaste is a future-growth opportunity in Nigeria Oral Care Market because the country has a young, expanding mass consumer base, high household formation potential and broad acceptance of plant-based personal-care claims across FMCG categories. The World Bank reports Nigeria’s total population at 232,679,478 people in 2024, while UNFPA reports 237.5 million people in 2025 and 41 out of every 100 people in the 0–14 age group, supporting long-term family oral-care consumption. This creates a large addressable base for herbal toothpaste variants positioned around clove, neem, charcoal, mint, aloe vera, gum care and fresh breath. The Federal Government also introduced oral-health policy documents covering 2024–2029 and 2024–2026, indicating official attention toward preventive oral health and public awareness. Herbal toothpaste brands can use this setting to position natural formulations as daily-use, family-safe, affordable and accessible through chemists, supermarkets and traditional trade. The opportunity is strongest where consumers seek functional benefits but remain price-sensitive and familiar with herbal personal-care narratives.

Sensitivity Care

Sensitivity care is a future-growth opportunity in Nigeria Oral Care Market because older adults, urban pharmacy users and dental-clinic consumers are more likely to seek therapeutic toothpaste, gum-care products and dentist-recommended oral hygiene solutions. World Bank data reports Nigeria’s population aged 65 and above at 7,093,611 people in 2024, while Nigeria’s life expectancy at birth is reported at 55 years in 2024. These numbers indicate a sizeable adult and ageing consumer base for sensitivity toothpaste, gum protection, enamel repair claims and premium pharmacy-led oral care. Urbanization further supports this opportunity: Nigeria had 128,043,517 urban residents in 2024, giving premium sensitivity brands a concentrated base of pharmacies, chemists, dentists and modern retail outlets for education-led selling. Sensitivity care is also supported by preventive oral-health policy attention, as the Federal Government stated in December 2024 that oral health would be addressed through an integrated primary healthcare approach. This creates space for pharmacy activation, dentist referrals and smaller therapeutic toothpaste SKUs.

Future Outlook

The Nigeria Oral Care Market is expected to grow steadily as oral hygiene becomes more embedded in daily household routines and brands widen access through affordable packs, mass retail, pharmacies and e-commerce. Toothpaste will remain the anchor category, but faster growth opportunities will come from sensitivity toothpaste, herbal formulations, mouthwash, kids oral care and premium toothbrushes. Urbanization, dental awareness, higher pharmacy penetration and benefit-led claims will continue to reshape the category.

Major Players

- Colgate-Palmolive

- Procter & Gamble / Oral-B

- Unilever Nigeria / Closeup

- Unilever Nigeria / Pepsodent

- Haleon / Sensodyne

- African Consumer Care / Dabur

- Daraju Industries / MyMy

- PZ Cussons Nigeria

- Johnson & Johnson / Listerine

- Church & Dwight / Arm & Hammer

- Lion Corporation

- Himalaya Wellness

- Dentaid

- Dr. Fresh

- Tolaram Group

Key Target Audience

- Oral care product manufacturers

- Toothpaste and toothbrush brands

- FMCG distributors and wholesalers

- Supermarket and pharmacy chains

- Dental clinic chains and oral-health service providers

- Packaging suppliers for tubes, cartons and multipacks

- Investments and venture capitalist firms

- Government and regulatory bodies (NAFDAC, Standards Organisation of Nigeria, Federal Ministry of Health and Social Welfare, Federal Competition and Consumer Protection Commission)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping Nigeria Oral Care Market stakeholders, including toothpaste manufacturers, toothbrush brands, pharmacies, supermarkets, distributors, open-market wholesalers, dental clinics and regulators. Variables include category revenue, SKU pricing, pack size, channel mix, urban penetration, benefit claims and consumer usage frequency.

Step 2: Market Analysis and Construction

Historical and base-year market data is compiled from published market databases, trade sources, retail observations and company-level oral care positioning. The analysis evaluates toothpaste-led category revenue, toothbrush replacement cycles, pharmacy-led therapeutic demand and the contribution of traditional trade versus modern trade.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions are validated through structured discussions with FMCG distributors, pharmacists, dentists, category managers and importers. These consultations help test assumptions around toothpaste dominance, sensitivity-care growth, counterfeit exposure, pack-size affordability and the pricing gap between mass and premium SKUs.

Step 4: Research Synthesis and Final Output

The final stage triangulates top-down market sizing with bottom-up channel and SKU-level estimates. Segment shares, competitive positioning and future outlook are refined using published market size benchmarks, oral-health indicators, retailer checks and expert validation to build a commercially relevant Nigeria Oral Care Market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Toothpaste-to-Total Oral Care Estimation, Retail Audit Approach, SKU Price Basket, Pharmacy and Supermarket Checks, Distributor Interviews, Dentist/Pharmacist Inputs, Consumer Usage Frequency Mapping, Limitations and Forecast Assumptions)

- Definition and Scope

- Market Genesis

- Evolution of Oral Hygiene Habits

- Timeline of Major Oral Care Brands

- Business Cycle

- Supply Chain and Value Chain Analysis

- Import, Local Manufacturing and Contract Manufacturing Structure

- Route-to-Market Structure

- Consumer Purchase Journey

- Growth Drivers(Population Base, Urbanization, Dental Awareness, Preventive Healthcare, Modern Retail, Pharmacist Recommendation, Premiumization, Kids Oral Hygiene)

- Market Challenges(FX Volatility, Import Cost, Inflation, Counterfeit Risk, Price Sensitivity, Informal Trade Fragmentation, Low Dental Visit Frequency)

- Opportunities(Herbal Toothpaste, Sensitivity Care, Whitening Claims, Kids SKUs, Dentist Endorsement, Fluoride-Free Products, Multipacks, Digital Retail)

- Nigeria Oral Care Market Regulatory and Quality Landscape (NAFDAC Registration, SON Standards, Labelling, Fluoride Claims, Import Documentation, Counterfeit Control, Advertising Claims)

- SWOT Analysis(Brand trust, pharmacy reach, imported premium exposure, affordability pressure, private-label threat, oral health education whitespace)

- Stakeholder Ecosystem (Manufacturers, importers, distributors, retailers, pharmacists, dentists, dental associations, schools, medical aid/wellness programmes, e-commerce platforms)

- Porter’s Five Forces(Brand concentration, retailer bargaining power, private-label threat, substitutes, premiumization barriers, new entrant constraints)

- Competition Ecosystem(Multinational FMCG brands, therapeutic oral care brands, private labels, dental-specialist brands, online imported brands)

- By Value (2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Per Capita Oral Care Spend (2020-2025)

- By Toothpaste Consumption Volume (2020-2025)

- By Retail Channel Revenue Contribution (2020-2025)

- By Product Category (In Value%)

Toothpaste

Toothbrush

Mouthwash/Rinses

Dental Floss and Interdental Products

Denture Care Products

Teeth Whitening Products

Kids Oral Care Products - By Toothpaste Type (In Value%)

Fluoride Toothpaste

Herbal/Natural Toothpaste

Whitening Toothpaste

Sensitivity Toothpaste

Anti-Cavity Toothpaste

Fresh Breath Toothpaste

Charcoal Toothpaste

Kids Toothpaste - By Toothbrush Type (In Value%)

Manual Toothbrush

Medium Bristle Toothbrush

Soft Bristle Toothbrush

Kids Toothbrush

Battery/Electric Toothbrush

Premium Toothbrush - By Price Tier (In Value%)

Mass/Economy

Mid-Priced

Premium

Therapeutic/Premium Pharmacy SKUs - By Pack Size (In Value%)

Small Tubes

Standard Family Tubes

Value Packs

Sachets/Trial Packs

Multipacks - By Distribution Channel (In Value%)

Open Markets and Traditional Trade

Supermarkets/Hypermarkets

Pharmacies

Chemists/Drug Stores

Convenience Stores

Online Retail

Dental Clinics

Wholesalers and Distributors - By Consumer Group (In Value%)

Adults

Children

Family Households

Urban Professionals

Sensitive Teeth Consumers

Dental-Advice Consumers - By Region (In Value%)

Lagos and South West

Abuja and North Central

South East

South South

North West

North East

- Market Share of Major Players by Value, by Volume, by Product Category, by Toothpaste Type, by Distribution Channel)

- Cross Comparison Parameters (Product Portfolio Breadth, Toothpaste Benefit Claims, SKU/Pack-Size Ladder, Average Selling Price, Traditional Trade Reach, Modern Trade Visibility, Pharmacy/Dental Clinic Presence, Local Manufacturing/Import Model, local manufacturing/import model, dentist/pharmacist endorsement strategy, recent developments)

- SWOT Analysis of Major Players (Brand equity, therapeutic credibility, price architecture, retailer dependence, innovation pipeline, private-label exposure)

- Pricing Analysis by SKU (75ml toothpaste, 100ml toothpaste, 500ml mouthwash, twin toothbrush packs, electric toothbrushes, denture adhesive, whitening kits, floss packs)

- Promotional and Trade Scheme Benchmarking

- Detailed Profiles of Major Companies

Colgate-Palmolive

Procter & Gamble / Oral-B

Unilever Nigeria / Closeup

Unilever Nigeria / Pepsodent

GlaxoSmithKline / Sensodyne

African Consumer Care / Dabur

Daraju Industries / MyMy

PZ Cussons Nigeria

Johnson & Johnson / Listerine

Church & Dwight / Arm & Hammer

Lion Corporation

Himalaya Wellness

Dentaid

Dr. Fresh

Tolaram Group

- Demand and Utilization(Brushing Frequency, Mouthwash Usage, Electric Toothbrush Ownership, Dental Floss Adoption, Kids Oral Hygiene Routine)

- Consumer Purchasing Power(Premium Toothpaste Basket, Multi-Pack Buying, Promotion Sensitivity, Online Discount Dependency)

- Needs, Desires and Pain Points(Cavity Prevention, Sensitivity Relief, Gum Bleeding, Whitening, Bad Breath, Enamel Protection, Child-Safe Fluoride, Denture Hygiene)

- Decision-Making Process(Dentist Recommendation, Retail Shelf Visibility, Brand Trust, Price Promotion, Ingredient Claims, Online Ratings, Family Usage)

- Dental Professional Influence (Dentist-Recommended Brands, Post-Treatment Product Advice, Sensitivity and Gum Care Referrals, Clinic Retailing)

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

- By Per Capita Oral Care Spend (2026-2035)

- By Product Category Revenue Pool (2026-2035)

- By Channel Revenue Pool (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now