Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Nigeria’s warehousing market reached an estimated value of USD ~ Billion based on a recent historical assessment supported by logistics industry data from the Nigerian Shippers’ Council and international supply chain analyses. Growth is driven by expanding retail distribution networks, increasing import and manufacturing activity, and the rapid development of organized logistics infrastructure. Rising e-commerce transactions, large consumer goods supply chains, and increased investment in industrial storage facilities are strengthening demand for modern warehouse infrastructure across major commercial corridors.

Lagos remains the most dominant warehousing hub because it hosts the country’s largest ports, major distribution centers, and high consumer demand concentration. Industrial activity across Ogun and Oyo also supports significant warehouse development due to manufacturing clusters and proximity to Lagos logistics corridors. Abuja and Kano function as strategic inland distribution hubs connecting northern trade routes and regional agricultural supply chains. These cities benefit from stronger transport connectivity, concentration of logistics providers, and proximity to major consumption and production centers.

Market Segmentation

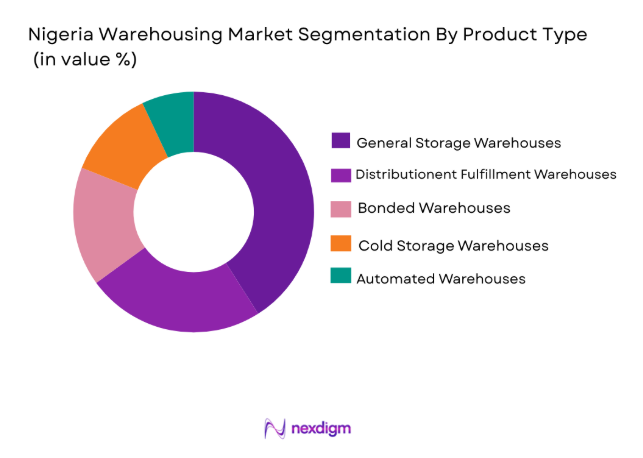

By Product Type

Nigeria Warehousing market is segmented by product type into general storage warehouses, cold storage warehouses, bonded warehouses, distribution fulfillment warehouses, and automated warehouses. Recently, general storage warehouses have a dominant market share due to factors such as strong demand from fast moving consumer goods distributors, large retail supply chains, and import driven inventory storage requirements. Consumer goods importers and manufacturing companies depend heavily on large scale general storage facilities located near ports and industrial zones. Nigeria’s heavy reliance on imported packaged goods, electronics, and consumer products further increases demand for flexible storage capacity capable of handling high inventory turnover and diverse product categories across national distribution networks.

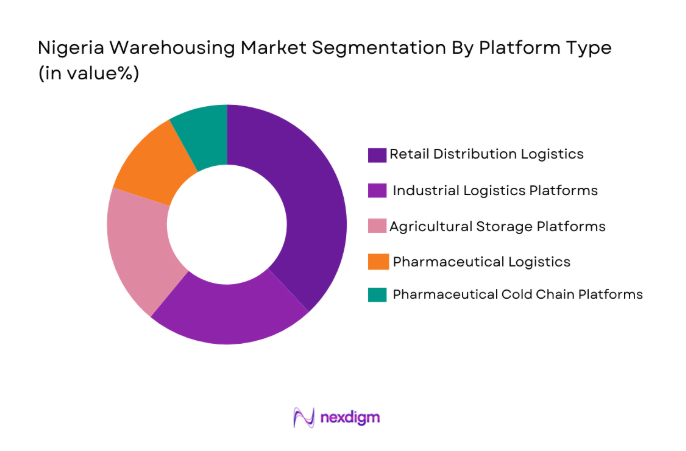

By Platform Type

Nigeria Warehousing market is segmented by platform type into e-commerce fulfillment platforms, retail distribution platforms, industrial logistics platforms, agricultural storage platforms, and pharmaceutical cold chain platforms. Recently, retail distribution platforms have a dominant market share due to factors such as strong supermarket expansion, national FMCG distribution networks, and centralized inventory management strategies adopted by major consumer goods companies. Retailers and distributors operate large regional distribution centers that support product flows between manufacturers, wholesalers, and thousands of retail outlets nationwide. This centralized distribution model improves inventory efficiency and reduces logistics costs, making retail distribution platforms the backbone of Nigeria’s organized supply chain infrastructure.

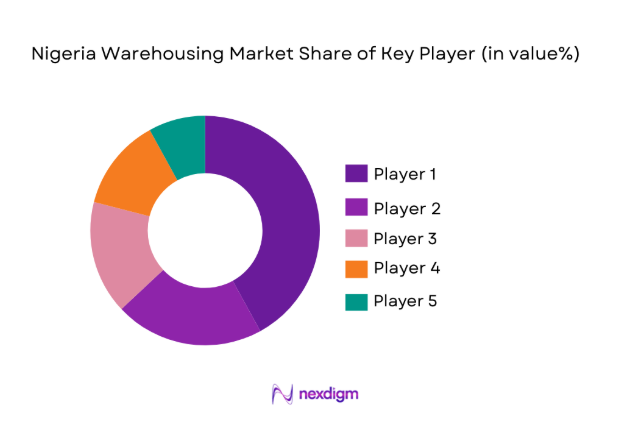

Competitive Landscape

Nigeria’s warehousing market remains moderately consolidated with several international logistics providers operating alongside strong domestic supply chain companies. Global logistics firms bring advanced warehouse management technologies, integrated freight services, and international distribution capabilities, while local operators leverage regional networks and strong relationships with manufacturing and retail sectors. Increasing investment in logistics parks, cold storage infrastructure, and e-commerce fulfillment centers is intensifying competition. Strategic partnerships between logistics firms, retailers, and manufacturers are strengthening nationwide warehousing networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity |

| DHL Supply Chain Nigeria | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Bolloré Logistics | 1822 | Puteaux, France | ~ | ~ | ~ | ~ | ~ |

| Sifax Logistics | 1988 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| Red Star Logistics | 1992 | Lagos, Nigeria | ~ | ~ | ~ | ~ | ~ |

| ColdHubs Limited | 2015 | Abuja, Nigeria | ~ | ~ | ~ | ~ | ~ |

Nigeria Warehousing Market Analysis

Growth Drivers

Expansion of E Commerce Fulfillment and Retail Distribution Infrastructure

Nigeria’s warehousing sector is expanding rapidly as the country’s digital commerce ecosystem increases demand for efficient inventory storage and order fulfillment facilities capable of supporting high shipment volumes across urban markets. Large online retail platforms including Jumia and rapidly expanding local digital marketplaces require modern distribution centers equipped with advanced inventory management systems and automated order processing infrastructure. Warehousing facilities increasingly function as integrated fulfillment hubs connecting suppliers manufacturers retailers and final consumers through centralized logistics networks. Logistics providers therefore expand warehouse footprints near major urban markets such as Lagos Abuja and Port Harcourt to reduce transportation time and improve delivery efficiency. Growing consumer adoption of digital shopping platforms increases the volume of parcels requiring temporary storage sorting and dispatch before final delivery to customers. Retailers increasingly adopt omnichannel distribution strategies combining online sales with physical store networks which requires warehouses to serve as centralized inventory management nodes. Logistics companies also invest in technology driven warehouse management systems automated picking solutions and real time inventory monitoring tools that significantly improve operational efficiency. These technological and structural developments increase demand for larger and more technologically advanced warehouse infrastructure nationwide. The continued expansion of Nigeria’s consumer economy combined with the growth of digital commerce platforms therefore remains one of the most significant structural drivers accelerating investment in modern warehousing infrastructure across the country.

Growth of Industrial Manufacturing and Import Driven Supply Chains

Nigeria’s warehousing demand continues increasing as manufacturing expansion and large scale import trade create significant requirements for long term inventory storage and logistics infrastructure supporting domestic distribution networks. Industrial sectors including consumer goods food processing construction materials pharmaceuticals and electronics depend heavily on warehouse facilities capable of storing raw materials finished goods and imported products before national distribution. Lagos ports including Apapa and Tin Can Island handle substantial volumes of imported consumer goods machinery and industrial inputs which require large scale storage infrastructure located near port logistics corridors. Manufacturing clusters located across Ogun Oyo and Lagos states depend on strategically located warehouses that allow companies to manage production inventories and maintain steady supply chain flows across regional markets. Logistics providers therefore expand warehouse capacity within industrial zones and near major transportation corridors connecting ports highways and rail terminals. Increasing domestic manufacturing activity under industrial development initiatives also requires specialized storage facilities capable of supporting production supply chains and nationwide distribution networks. Warehouse operators increasingly integrate transport management systems inventory tracking technologies and cross docking infrastructure that enable companies to move goods more efficiently between production facilities distribution centers and retail outlets. As Nigeria continues strengthening industrial production and expanding trade volumes the demand for large scale logistics storage infrastructure increases significantly. These structural developments position warehousing facilities as critical infrastructure supporting the country’s expanding manufacturing and trade based economy.

Market Challenges

Infrastructure Constraints and Unreliable Power Supply Affecting Warehouse Operations

Nigeria’s warehousing industry faces operational difficulties due to infrastructure constraints including unreliable electricity supply road congestion and limited transport connectivity across key logistics corridors. Warehouse facilities require consistent electricity to operate inventory management systems refrigeration equipment security infrastructure and automated storage technologies that support modern logistics operations. However frequent power interruptions across industrial zones force warehouse operators to depend heavily on diesel generators which significantly increases operating costs and reduces overall efficiency. Transportation infrastructure limitations also affect warehousing productivity because poor road conditions traffic congestion and port delays disrupt the movement of goods between ports warehouses and distribution centers. Lagos the country’s primary logistics hub experiences persistent congestion around port corridors that slows cargo clearance and increases storage time within warehouses. Logistics companies therefore experience higher operational expenses related to transportation delays fuel consumption and inventory management inefficiencies. Limited rail freight connectivity across major industrial regions further increases dependence on road transportation for cargo movement which places additional pressure on highway infrastructure. Warehouse developers must therefore invest additional capital in backup power systems internal logistics infrastructure and security systems to maintain operational continuity. These infrastructure related constraints continue affecting warehousing efficiency and increase the overall cost structure of logistics service providers operating within Nigeria’s supply chain ecosystem.

High Land Acquisition Costs and Limited Availability of Modern Logistics Parks

Nigeria’s warehousing sector faces significant development challenges due to high land acquisition costs limited availability of industrial zoned land and insufficient development of large scale logistics parks near major commercial centers. Urban regions such as Lagos Abuja and Port Harcourt experience strong demand for industrial land suitable for logistics facilities because these cities serve as major distribution hubs supporting national trade networks. However rapid urbanization real estate competition and regulatory complexity significantly increase land prices for warehouse development projects. Developers often encounter challenges related to land title verification infrastructure connectivity and zoning approvals which slow the establishment of new logistics facilities. Many existing warehouse structures also lack modern features such as automated storage systems temperature controlled environments and integrated transport infrastructure required for efficient large scale logistics operations. Limited availability of purpose built logistics parks forces many companies to operate from outdated storage facilities that do not meet international supply chain efficiency standards. Logistics companies therefore face higher capital expenditure when constructing modern distribution centers capable of handling large inventory volumes and advanced material handling technologies. These constraints slow the pace of warehouse infrastructure expansion despite growing demand from manufacturing retail and e commerce sectors. Addressing these structural limitations requires coordinated investment in industrial land development infrastructure planning and modern logistics park ecosystems capable of supporting Nigeria’s evolving supply chain environment.

Opportunities

Development of Integrated Logistics Parks and Industrial Warehousing Zones

Nigeria’s warehousing market presents strong growth opportunities through the development of integrated logistics parks designed to consolidate storage transportation distribution and value added logistics services within strategically located industrial zones. Logistics parks allow warehouse operators manufacturers distributors and freight companies to operate within a unified infrastructure ecosystem that significantly improves supply chain coordination and transportation efficiency. Government initiatives supporting industrial corridor development and free trade zones create favorable conditions for establishing modern logistics hubs near ports airports and major highway networks. Integrated logistics parks provide centralized facilities including automated warehouses truck terminals customs processing zones and inventory management infrastructure which enable companies to streamline cargo handling operations. These developments reduce transportation delays improve cargo security and enhance inventory visibility across supply chains serving domestic and international markets. Large industrial parks also attract third party logistics providers e commerce fulfillment companies and manufacturing firms seeking scalable storage infrastructure capable of supporting long term business expansion. The clustering of logistics services within organized infrastructure zones improves operational efficiency and lowers distribution costs for companies operating across multiple sectors. As Nigeria continues investing in industrial development and trade facilitation initiatives logistics park development represents a major opportunity for expanding modern warehousing infrastructure nationwide.

Expansion of Cold Chain Storage for Agriculture Food and Pharmaceutical Distribution

Nigeria’s warehousing sector has significant opportunity to expand through the development of specialized cold chain storage infrastructure supporting agricultural food processing and pharmaceutical supply chains across the country. Agricultural producers require temperature controlled storage facilities capable of preserving perishable commodities including fruits vegetables dairy products meat and seafood before distribution to domestic markets and export channels. Post harvest losses remain a major challenge for Nigeria’s agricultural sector due to inadequate refrigerated storage and limited cold chain logistics infrastructure. Investment in modern cold storage warehouses equipped with refrigeration systems temperature monitoring technology and controlled atmosphere storage facilities can significantly improve product preservation and supply chain efficiency. Pharmaceutical distribution networks also require temperature controlled storage infrastructure capable of maintaining strict regulatory standards for vaccines biologics insulin and other temperature sensitive medicines. Healthcare providers pharmaceutical companies and medical distributors increasingly depend on reliable cold chain logistics to maintain product safety and regulatory compliance across national distribution networks. Expansion of cold storage infrastructure therefore supports both food security objectives and healthcare supply chain reliability. As consumer demand for processed foods pharmaceutical products and high quality agricultural exports increases the development of temperature controlled warehousing facilities represents a major opportunity for logistics companies and infrastructure investors across Nigeria’s supply chain ecosystem.

Future Outlook

Nigeria’s warehousing market is expected to experience steady expansion as logistics infrastructure continues evolving to support national trade and distribution networks. Increasing adoption of digital warehouse management systems, automation technologies, and integrated logistics platforms will improve operational efficiency. Government support for industrial zones and transport corridor development is also strengthening the logistics ecosystem. Growing retail distribution, manufacturing activity, and e commerce expansion will further increase demand for large scale storage and fulfillment facilities across major commercial regions.

Major Players

- DHL Supply Chain Nigeria

- Bolloré Logistics Nigeria

- Sifax Logistics Limited

- Red Star Logistics

- ColdHubs Limited

- Maersk Logistics Nigeria

- UPS Supply Chain Solutions Nigeria

- FedEx Nigeria Logistics Services

- AG Leventis Logistics

- Trans Africa Logistics

- Kobo360 Logistics

- Dangote Logistics

- Lagos Free Zone Logistics Company

- SGS Nigeria Logistics

- Imperial Logistics Nigeria

Key Target Audience

- Logistics and supply chain companies

- Retail and e-commerce companies

- Manufacturing and industrial companies

- Agricultural supply chain operators

- Pharmaceutical distribution companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying core variables affecting the Nigeria Warehousing Market including storage capacity, logistics infrastructure, trade flows, industrial activity, and retail distribution networks. These variables form the analytical framework used to evaluate supply chain demand and warehouse infrastructure development across major commercial regions.

Step 2: Market Analysis and Construction

Comprehensive analysis of logistics networks, warehousing facilities, trade activity, and supply chain distribution patterns is conducted to construct the Nigeria Warehousing Market structure. Data from industry databases, trade associations, government publications, and logistics operators are used to assess infrastructure capacity and operational trends.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings for the Nigeria Warehousing Market are validated through consultations with logistics professionals, supply chain managers, warehouse operators, and industry analysts. Expert insights help verify operational trends, infrastructure development patterns, and demand drivers influencing warehouse investments.

Step 4: Research Synthesis and Final Output

All validated data points and expert insights are synthesized to produce a structured analysis of the Nigeria Warehousing Market. The final research output integrates qualitative analysis, infrastructure evaluation, and logistics industry insights to present a comprehensive assessment of market dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E Commerce Distribution Networks

Growth of Organized Retail Supply Chains

Increasing Industrial Production and Import Trade Volumes - Market Challenges

Infrastructure Constraints and Power Supply Limitations

High Land Acquisition and Construction Costs

Limited Cold Chain and Automated Storage Infrastructure - Market Opportunities

Development of Modern Logistics Parks and Industrial Zones

Expansion of Cold Storage Infrastructure for Agriculture and Pharmaceuticals

Adoption of Smart Warehouse Technologies and Automation - Trends

Growth of Technology Enabled Warehouse Management Systems

Increasing Demand for Urban Fulfillment and Micro Distribution Centers - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

General Storage Warehousing

Temperature Controlled Warehousing

Automated Warehousing Systems

Bonded Warehousing Facilities

Distribution Fulfillment Warehousing - By Platform Type (In Value%)

E Commerce Fulfillment Platforms

Retail Distribution Platforms

Industrial Logistics Platforms

Agricultural Storage Platforms

Pharmaceutical Cold Chain Platforms - By Fitment Type (In Value%)

Built to Suit Warehouses

Leased Warehouse Facilities

Shared Multi Client Warehouses

Dedicated Private Warehouses - By End User Segment (In Value%)

Retail and E Commerce Companies

Manufacturing and Industrial Firms

Agriculture and Food Processing Companies

- Market Share Analysis

- Cross Comparison Parameters (Storage Capacity, Temperature Control Capability, Automation Level, Geographic Coverage, Industry Focus, Logistics Integration, Technology Adoption)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain Nigeria

Maersk Logistics Nigeria

Bolloré Logistics Nigeria

Imperial Logistics Nigeria

Sifax Logistics Limited

Lagos Free Zone Logistics Company

Trans Africa Logistics

Dangote Logistics

Red Star Logistics

AG Leventis Logistics

UPS Supply Chain Solutions Nigeria

FedEx Nigeria Logistics Services

SGS Nigeria Logistics

ColdHubs Limited

Kobo360 Logistics

- Retailers Increasing Investment in Distribution Infrastructure

- Manufacturers Expanding Inventory Storage Capacity

- Agricultural Producers Requiring Post Harvest Storage Solutions

- Logistics Providers Developing Multi Client Warehousing Networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now