Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Oman’s cloud infrastructure market reached approximately USD ~ million based on a recent historical assessment, driven by sovereign cloud deployments, hyperscale region launches, and enterprise migration to public and hybrid cloud platforms across government, telecom, and energy sectors. National data localization policies and digital transformation programs are accelerating demand for compute, storage, and cloud networking infrastructure within domestic data centers. Expansion of cloud-ready facilities and telecom-operated cloud platforms is sustaining infrastructure investment across Oman’s digital economy.

Muscat dominates cloud infrastructure deployment due to concentration of telecom data centers, government digital platforms, and enterprise IT workloads requiring centralized cloud hosting. Sohar and Duqm are emerging through industrial cloud adoption linked to logistics, port operations, and energy sector digitalization within coastal economic zones. International hyperscale cloud partnerships with national operators reinforce Oman’s positioning as a regional cloud hosting node bridging Gulf, Africa, and South Asia digital connectivity corridors.

Market Segmentation

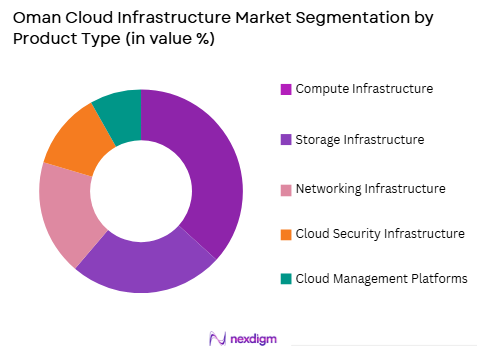

By Product Type

Oman Cloud Infrastructure Market is segmented by product type into compute infrastructure, storage infrastructure, networking infrastructure, cloud security infrastructure, and cloud management platforms. Recently, compute infrastructure has a dominant market share due to factors such as hyperscale cloud region deployments, sovereign cloud compute clusters, and enterprise workload migration requiring virtualized and containerized compute environments. Telecom operators and cloud providers prioritize scalable server farms and virtualization platforms to host government and enterprise applications. Expansion of AI-ready and high-performance cloud compute nodes further reinforces this segment’s leadership. Sovereign cloud initiatives mandate domestic compute hosting capacity, increasing investment in servers and hyperconverged infrastructure. Enterprise digital transformation programs shift on-premise workloads to cloud compute environments, accelerating procurement. Public sector platforms in energy, smart governance, and logistics rely heavily on cloud compute resources. Continuous refresh cycles and scaling of compute clusters sustain infrastructure spending concentration in this segment across Oman’s cloud ecosystem.

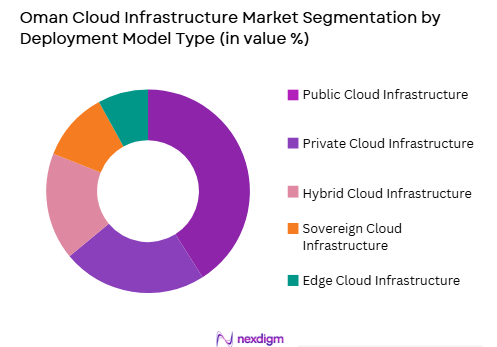

By Deployment Model

Oman Cloud Infrastructure Market is segmented by deployment model into public cloud infrastructure, private cloud infrastructure, hybrid cloud infrastructure, sovereign cloud infrastructure, and edge cloud infrastructure. Recently, public cloud infrastructure has a dominant market share due to factors such as hyperscale cloud region establishment, enterprise migration to managed cloud services, and telecom-hosted public cloud platforms serving multiple sectors. Public cloud environments allow scalable resource access without capital ownership, aligning with enterprise digitalization strategies. International cloud providers entering Oman through telecom partnerships expand public cloud availability. Government and enterprises adopt public cloud for non-sensitive workloads, increasing infrastructure demand. Shared cloud platforms maximize utilization of domestic data center capacity. SaaS and platform services growth further drives underlying public cloud infrastructure expansion. These dynamics position public cloud infrastructure as the leading deployment model in Oman’s cloud infrastructure market.

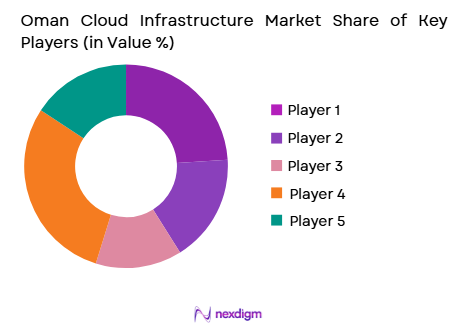

Competitive Landscape

Oman’s cloud infrastructure market is moderately consolidated among global hyperscale cloud providers, telecom operators, and enterprise infrastructure vendors delivering compute, storage, and cloud platforms within domestic data centers. Market dynamics are shaped by sovereign cloud initiatives, hyperscale region partnerships, and enterprise cloud migration programs. International cloud vendors collaborate with national telecom and data center operators to localize cloud services and infrastructure deployment across Oman.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Oman Cloud Presence |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| Oracle | 1977 | USA | ~ | ~ | ~ | ~ | ~ |

| 1998 | USA | ~ | ~ | ~ | ~ | ~ | |

| Huawei | 1987 | China | ~ | ~ | ~ | ~ | ~ |

Oman Cloud Infrastructure Market Analysis

Growth Drivers

Sovereign Cloud Policies and National Data Localization Mandates

Oman’s cloud infrastructure market growth is fundamentally driven by government policies mandating domestic data hosting and sovereign cloud capability for sensitive public sector and strategic industry workloads. National cybersecurity frameworks and data governance regulations require in-country storage and processing of government, energy, and critical infrastructure data, compelling investment in domestic cloud compute and storage infrastructure. Ministries and state-owned enterprises are migrating legacy IT systems to sovereign cloud environments hosted in national data centers. Telecom operators are establishing sovereign cloud platforms compliant with local data residency requirements. Public sector digital transformation programs across smart governance, energy, and logistics depend on scalable cloud infrastructure within national jurisdiction. Localization policies also encourage multinational enterprises operating in Oman to host regional data domestically. Expansion of sovereign cloud frameworks increases demand for secure compute, storage, and networking infrastructure. Government procurement programs prioritize domestic cloud deployment over offshore hosting. National digital platforms and shared government clouds require continuous scaling of infrastructure. These sovereign policy dynamics structurally anchor long-term investment in Oman’s cloud infrastructure ecosystem.

Hyperscale Cloud Region Partnerships and Enterprise Cloud Migration

Expansion of hyperscale cloud regions in partnership with Oman’s telecom and data center operators is a major driver of cloud infrastructure investment as enterprises and government entities migrate workloads from on-premise IT environments to scalable cloud platforms. International cloud providers entering Oman through joint ventures and localized regions deploy large-scale compute and storage infrastructure within domestic facilities. Enterprise digital transformation initiatives across banking, telecom, energy, and logistics sectors rely on cloud platforms for application modernization and data analytics. Migration of enterprise workloads to infrastructure-as-a-service and platform-as-a-service environments increases demand for underlying server, storage, and networking hardware. Cloud-native application adoption and SaaS growth further expand infrastructure utilization. Telecom providers integrate hyperscale cloud services with national connectivity assets, enhancing adoption. Regional enterprises also utilize Oman-hosted cloud platforms due to connectivity advantages. Continuous scaling and refresh cycles of hyperscale infrastructure sustain investment momentum. These hyperscale partnership and migration dynamics position Oman as an emerging regional cloud hosting hub.

Market Challenges

Limited Domestic Cloud Software Ecosystem and Skills Availability

Oman’s cloud infrastructure market expansion is constrained by limited domestic cloud-native software ecosystems and shortage of specialized cloud engineering skills required to fully utilize deployed infrastructure capacity. Enterprises and public sector entities often lack expertise in cloud architecture, DevOps, and application modernization necessary for effective migration and optimization. Availability of locally developed cloud applications and SaaS solutions tailored to Oman’s industries remains limited. Dependence on foreign cloud expertise increases deployment cost and slows adoption. Workforce development programs in cloud engineering are expanding but still insufficient relative to demand. Underutilization of cloud infrastructure may occur where workloads remain legacy or non-cloud-ready. Local startups and developers face barriers in building scalable cloud-native solutions. Skills gaps in cybersecurity and cloud governance also affect enterprise confidence. Limited domestic software ecosystems reduce multiplier effects of infrastructure investment. These talent and ecosystem constraints slow the pace and breadth of cloud infrastructure adoption in Oman.

High Energy, Cooling, and Connectivity Costs for Data Center Operations

Cloud infrastructure deployment in Oman faces challenges from high operational costs associated with powering and cooling data centers in a hot climate environment and ensuring high-capacity connectivity. Cloud data centers require energy-dense server clusters and continuous cooling systems, increasing electricity consumption and operational expenditure. Energy pricing structures and grid capacity influence cost competitiveness of domestic cloud hosting. Advanced cooling technologies necessary for hyperscale environments increase capital and operating costs. Connectivity redundancy and international bandwidth capacity also affect infrastructure economics. Smaller domestic market scale may limit economies of scale compared with major regional cloud hubs. Import dependence for data center equipment increases cost volatility. Environmental and efficiency standards impose additional engineering requirements. Financing large-scale cloud facilities may face long payback horizons. These operational cost pressures challenge rapid scaling and price competitiveness of Oman’s cloud infrastructure market.

Opportunities

Regional Sovereign Cloud Hosting and Cross-Border Data Services

Oman has strong opportunity to position itself as a neutral regional sovereign cloud hosting hub serving Middle East, African, and South Asian markets requiring compliant and secure data processing environments. Connectivity through submarine cable landings and geopolitical neutrality support cross-border data hosting demand. Governments and enterprises in neighboring regions lacking domestic cloud capacity can host workloads in Oman-based sovereign clouds. Telecom operators can export cloud infrastructure services regionally. Disaster recovery and backup hosting demand from adjacent markets increase infrastructure utilization. Neutral jurisdiction positioning enhances trust for cross-regional data hosting. International cloud providers can use Oman as a gateway for multi-region deployments. Regulatory frameworks emphasizing compliance and sovereignty strengthen competitiveness. Export-oriented cloud infrastructure services create new digital economy revenue streams. These regional hosting dynamics can expand Oman’s cloud infrastructure market beyond domestic demand.

Green and Renewable-Powered Cloud Data Centers

Expansion of renewable energy projects in Oman creates opportunity to develop energy-efficient and sustainable cloud infrastructure powered by solar and wind resources, improving operational economics and attracting environmentally conscious cloud clients. Renewable integration can reduce electricity costs and carbon footprint of data centers. Green cloud infrastructure aligns with sustainability goals of multinational enterprises selecting hosting locations. Industrial zones with renewable energy access can host hyperscale cloud campuses. Advanced cooling and energy recovery technologies can enhance efficiency under desert conditions. Government incentives for renewable-powered infrastructure reduce investment barriers. Sustainable cloud positioning differentiates Oman from competing regional hubs. Energy-cloud partnerships can accelerate green data center deployment. Renewable-backed cloud services can attract regional workloads seeking low-carbon hosting. This convergence of energy transition and digital infrastructure demand presents long-term growth opportunity for Oman’s cloud market.

Future Outlook

Oman’s cloud infrastructure market is expected to expand steadily over the next five years as sovereign cloud adoption, hyperscale region deployment, and enterprise cloud migration accelerate infrastructure demand. Renewable-powered data centers and regional hosting services will enhance competitiveness. Government localization policies and digital transformation programs will sustain investment. Expansion of hybrid and edge cloud architectures across industrial and logistics sectors will diversify deployment footprints across Oman.

Major Players

- Amazon Web Services

- Microsoft

- Oracle

- Google Cloud

- Huawei Cloud

- Oman Data Park

- Omantel

- Ooredoo Oman

- Datamount

- Cloud Acropolis

- Gulf Business Machines Oman

- Gulf Infotech

- Equinix

- VMware

- Cisco

Key Target Audience

- Telecom operators

- Hyperscale cloud providers

- Banking and financial institutions

- Government and regulatory bodies

- Energy and utilities companies

- Logistics and transport operators

- Industrial enterprises

- Investments and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Key variables including cloud data center capacity, compute and storage deployments, hyperscale region presence, and enterprise cloud adoption were identified across Oman’s cloud ecosystem. Demand drivers across government, telecom, banking, and energy sectors were mapped to infrastructure requirements. Supply-side variables such as data center operators and connectivity assets were defined.

Step 2: Market Analysis and Construction

Primary and secondary inputs were integrated to construct the Oman cloud infrastructure market model, incorporating hyperscale partnerships, sovereign cloud initiatives, and enterprise migration trends. Segmentation by product type and deployment model was applied to estimate shares. Competitive positioning of cloud providers and infrastructure vendors was analyzed.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding cloud adoption growth, hyperscale expansion, and sovereign data policies were validated through consultations with telecom operators, cloud architects, and data center specialists. Alignment with national digital strategies and connectivity developments was verified. Sensitivity checks were applied to infrastructure deployment scenarios.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into a structured Oman cloud infrastructure market report covering segmentation, competitive landscape, and strategic outlook. Quantitative estimates were aligned with deployment evidence and policy direction. The final output integrates drivers, constraints, and opportunities shaping cloud infrastructure growth in Oman.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National digital transformation and cloud-first government policies

Expansion of regional and domestic data center capacity

Enterprise migration to cloud across regulated sectors - Market Challenges

Data sovereignty and localization compliance requirements

Limited domestic cloud engineering talent pool

High energy and cooling cost for data centers - Market Opportunities

Sovereign cloud development for government and critical sectors

Regional cloud hub positioning for GCC markets

Edge cloud deployment for smart infrastructure and IoT - Trends

Growth of hybrid and multi-cloud deployment models

Integration of AI-ready GPU cloud infrastructure

Shift toward energy-efficient modular data centers - Government regulations

National data protection and privacy regulations

Cloud service provider licensing frameworks

Critical information infrastructure protection policies - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Cloud Data Center Infrastructure

Multi-Cloud Management Platforms - By Platform Type (In Value%)

IaaS Platforms

PaaS Platforms

Container and Kubernetes Platforms

Edge Cloud Platforms

AI-Ready Cloud Platforms - By Fitment Type (In Value%)

Greenfield Cloud Data Centers

Colocation Cloud Deployments

On-Premise Private Cloud

Hybrid Integrated Environments

Edge Micro Data Centers - By EndUser Segment (In Value%)

Government and Public Sector

Energy and Utilities

Telecom and Digital Service Providers

Financial Services Institutions

Healthcare and Education - By Procurement Channel (In Value%)

Direct Hyper scaler Contracts

Managed Service Providers

System Integrators

Telecom Cloud Partnerships

Government Digital Programs

- Market Share Analysis

- Cross Comparison Parameters (Cloud Deployment Architecture, Data Center Scale and Tier Certification, Sovereign and Regulated Cloud Compliance, AI and High-Performance Compute Enablement, Hybrid and Multi-Cloud Orchestration Capability, Managed and Professional Services Depth,)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud

Oracle Cloud

Alibaba Cloud

IBM Cloud

Huawei Cloud

Tencent Cloud

OVHcloud

Equinix

Digital Realty

Omantel

Ooredoo

Nawras

Meeza

- Government agencies adopting sovereign and regulated cloud

- Energy firms deploying hybrid cloud for operations analytics

- Telecom operators integrating cloud for digital services

- Banks migrating workloads to compliant cloud environments

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now