Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Oman Cold Chain Logistics Market reached approximately USD ~ million, supported by increasing demand for temperature-controlled logistics across pharmaceuticals, food processing, seafood exports, and modern retail distribution networks. Expansion of organized retail chains and healthcare supply chains has significantly increased the need for refrigerated storage and transportation infrastructure. Investments in logistics hubs such as Sohar Port, Salalah Port, and Duqm Special Economic Zone also strengthen supply chain efficiency for temperature-sensitive cargo.

Muscat functions as the central hub for cold chain logistics due to the presence of major food importers, pharmaceutical distributors, and large retail supply networks. Sohar and Salalah also play important roles because their seaports facilitate international trade for seafood exports, agricultural shipments, and imported food products requiring temperature-controlled storage. These cities benefit from integrated logistics zones, advanced port infrastructure, and proximity to industrial and free trade zones that require reliable refrigerated transportation and cold storage systems.

Market Segmentation

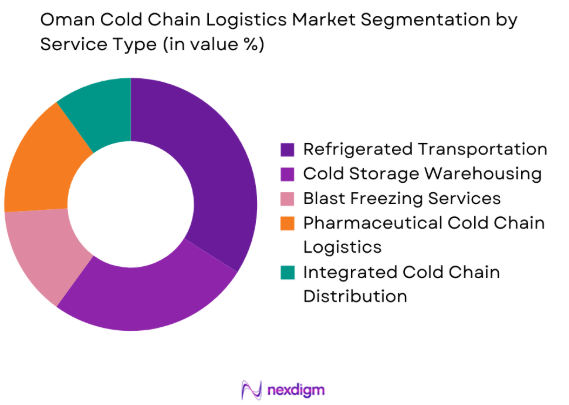

By Service Type

Oman Cold Chain Logistics market is segmented by service type into refrigerated transportation, cold storage warehousing, blast freezing services, pharmaceutical cold chain logistics, and integrated cold chain distribution. Recently, refrigerated transportation has a dominant market share due to strong demand from food imports, seafood exports, and pharmaceutical distribution networks that require reliable temperature-controlled movement of goods across cities and ports. Oman imports large volumes of fresh food, dairy products, and frozen meat, which depend heavily on refrigerated trucking fleets to maintain product integrity during transit. Pharmaceutical distributors also require secure temperature-controlled delivery systems to transport vaccines, biologics, and temperature-sensitive medicines between distribution centers and healthcare facilities. The rapid growth of supermarket chains and organized retail has increased last-mile cold logistics requirements, particularly for fresh food and frozen products. Government initiatives supporting seafood exports further strengthen demand for refrigerated transport vehicles connecting fisheries, processing facilities, and export terminals.

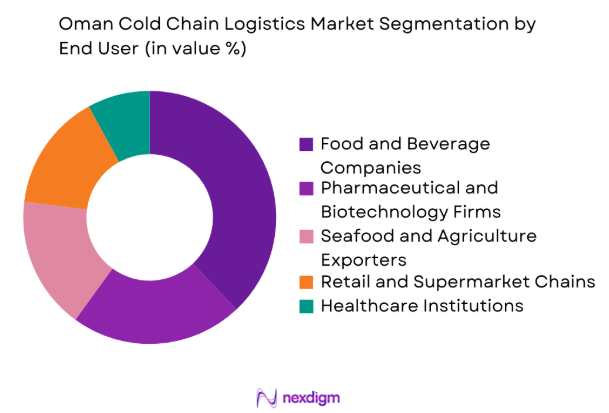

By End-User Industry

Oman Cold Chain Logistics market is segmented by end-user industry into food and beverage companies, pharmaceutical and biotechnology firms, seafood and agriculture exporters, retail and supermarket chains, and healthcare institutions. Recently, food and beverage companies have a dominant market share due to Oman’s heavy reliance on imported food products and the rapid expansion of organized retail distribution networks. Supermarkets and food distributors require large-scale refrigerated warehousing facilities to store dairy products, frozen foods, and fresh produce before distribution to retail outlets across the country. The growth of international restaurant chains and hospitality establishments further increases demand for consistent cold chain distribution to maintain food safety standards. Importers rely on temperature-controlled storage near ports and logistics hubs to maintain quality throughout the supply chain. Government regulations for food safety and product handling also require strict temperature monitoring during storage and transportation, strengthening demand for specialized cold chain infrastructure serving the food industry.

Competitive Landscape

The Oman Cold Chain Logistics Market features a moderately consolidated structure where a combination of international logistics providers and regional supply chain companies operate integrated refrigerated logistics networks. Global companies maintain strong operational capabilities through advanced warehouse automation systems, refrigerated fleet infrastructure, and digital temperature monitoring technologies. Local logistics firms maintain strong regional networks and partnerships with food importers, pharmaceutical distributors, and seafood exporters, allowing them to compete effectively in domestic distribution operations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Chain Infrastructure |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Germany | ~ | ~ | ~ | ~ | ~ |

| Agility Logistics | 1979 | Kuwait | ~ | ~ | ~ | ~ | ~ |

| Aramex | 1982 | UAE | ~ | ~ | ~ | ~ | ~ |

Oman Cold Chain Market Analysis

Growth Drivers

Expansion of Pharmaceutical Distribution Infrastructure in Oman

Oman’s pharmaceutical supply chain is expanding as healthcare demand rises and hospital infrastructure modernizes across major cities and regional medical facilities. Pharmaceutical distributors increasingly require specialized cold storage warehouses and refrigerated transportation systems to protect vaccines, biologics, insulin, and temperature sensitive medicines throughout the supply chain. Government healthcare expansion programs support the development of hospitals and diagnostic centers that rely on reliable pharmaceutical logistics networks. Cold chain providers invest in pharmaceutical grade storage facilities equipped with temperature monitoring systems and automated refrigeration technologies. International pharmaceutical manufacturers distributing medicines in Oman require logistics partners capable of maintaining strict temperature standards across long supply routes. Healthcare authorities also enforce strict storage and distribution regulations to ensure medicine safety.

Growth of Temperature Controlled Food Supply Chains and Retail Distribution Networks

Oman’s food supply chain depends heavily on cold chain logistics because the country imports large volumes of fresh and frozen food that must be transported and stored under controlled temperatures to maintain quality and safety. Expansion of supermarket chains and modern retail outlets increases demand for refrigerated warehouses and temperature controlled transportation linking ports, distribution centers, and retail stores. Retailers rely on cold logistics providers to distribute dairy products, frozen foods, fresh produce, and processed food across national supply networks. Food safety regulations require strict temperature compliance, encouraging investment in advanced cold storage facilities and monitoring technologies. Rising urbanization and growing consumer demand for high quality imported food further strengthen the need for reliable refrigerated logistics systems.

Market Challenges

High Capital Investment Requirements for Cold Chain Infrastructure Development

Cold chain logistics infrastructure requires substantial financial investment because temperature controlled warehouses, refrigerated transport fleets, and monitoring technologies involve high capital costs and specialized engineering. Logistics providers must invest in refrigeration equipment, insulation systems, backup power infrastructure, and temperature monitoring devices to maintain consistent storage conditions for sensitive goods. These requirements increase operational costs compared with conventional logistics facilities. Maintaining refrigeration equipment and ensuring continuous energy supply also creates long term financial burdens for operators. Smaller logistics companies often struggle to secure financing for large cold storage projects due to high upfront capital expenditure. Energy consumption for refrigeration systems further affects profitability, while strict food safety and pharmaceutical storage regulations require continuous facility upgrades and technology investments.

Energy Consumption and Operational Efficiency Constraints in Refrigerated Logistics Systems

Refrigerated logistics operations consume significantly higher energy than conventional logistics systems because maintaining stable low temperatures across warehouses and transportation vehicles requires continuous refrigeration equipment operation. Cooling systems operate throughout the supply chain, including cold storage facilities, refrigerated trucks, and shipping containers transporting temperature sensitive goods. High electricity consumption increases operating costs for cold chain providers, especially where energy prices fluctuate or infrastructure capacity is limited. Logistics companies must also maintain backup power systems to prevent temperature fluctuations during power disruptions, adding additional infrastructure expenses. Inefficient refrigeration systems can lead to product spoilage and financial losses. Cold chain operators therefore invest in energy efficient refrigeration technologies and monitoring systems to reduce operating costs while maintaining regulatory compliance.

Opportunities

Development of Integrated Logistics Zones and Cold Chain Infrastructure Expansion

Oman’s strategic investments in logistics infrastructure create strong opportunities for cold chain logistics providers as integrated logistics zones and port based industrial hubs increasingly require temperature controlled supply chain systems to support food imports, seafood exports, and pharmaceutical distribution. Logistics zones located near major ports enable the development of large refrigerated warehouses and distribution centers capable of managing high cargo volumes for international trade. Free trade zones encourage private investment in logistics facilities through regulatory incentives and tax benefits for companies establishing supply chain infrastructure. Cold chain operators can utilize these hubs to build integrated distribution networks connecting seaports, airports, and domestic transportation corridors while supporting seafood processing and agricultural export industries requiring reliable refrigerated logistics services.

Adoption of Digital Monitoring and Smart Cold Chain Technologies

Advances in digital supply chain technologies create new opportunities for cold chain logistics companies because temperature monitoring sensors, IoT enabled tracking systems, and cloud based logistics platforms allow operators to maintain precise control over storage and transportation conditions. Real time monitoring provides continuous data on temperature and humidity across shipments, improving transparency and operational efficiency for logistics providers. Pharmaceutical and food companies increasingly demand digital traceability solutions to verify product safety and regulatory compliance during transportation and storage. Cold chain operators adopting advanced monitoring technologies can improve service reliability and regulatory adherence. Smart logistics platforms also support predictive maintenance for refrigeration equipment while improving inventory management and optimizing warehouse utilization and transportation routing.

Future Outlook

The Oman Cold Chain Logistics Market is expected to expand steadily as the country strengthens its logistics infrastructure and modern retail supply chains. Increasing pharmaceutical distribution networks, seafood exports, and organized food retail operations will drive sustained demand for refrigerated logistics services. Investments in smart cold storage facilities, IoT-enabled monitoring systems, and integrated logistics hubs will enhance operational efficiency across the supply chain. Government initiatives supporting logistics sector development and international trade will further encourage private sector investment in temperature-controlled logistics infrastructure.

Major Players

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- DSV A/S

- CEVA Logistics

- Agility Logistics

- Aramex

- Gulf Agency Company Logistics

- BahwanLogistics

- AlNowrasLogistics Solutions

- MilahaLogistics

- Yusen Logistics

- Nippon Express

- Expeditors International

- Kerry Logistics

Key Target Audience

- Logistics and cold chain service providers

- Food and beverage manufacturing companies

- Pharmaceutical and biotechnology companies

- Seafood export companies

- Retail and supermarket chains

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key market variables such as refrigerated storage capacity, temperature-controlled transport fleet size, logistics infrastructure development, and sector demand patterns were identified. Data from logistics companies, trade authorities, and supply chain databases were reviewed to understand market structure and operational requirements.

Step 2: Market Analysis and Construction

The market model was constructed by analyzing cold chain demand across food distribution, pharmaceutical logistics, seafood exports, and retail supply chains. Trade statistics, logistics infrastructure investments, and transportation networks were evaluated to determine market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, logistics operators, and supply chain specialists were consulted to validate market assumptions and infrastructure trends. Interviews with cold chain operators helped confirm operational challenges, infrastructure capacity, and service demand patterns.

Step 4: Research Synthesis and Final Output

All collected data sources were synthesized into a structured research framework that evaluates market segmentation, competitive landscape, growth drivers, and infrastructure trends. The final analysis integrates verified industry data and expert insights to produce a comprehensive market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Pharmaceutical and Vaccine Distribution Infrastructure

Rising Demand for Temperature Controlled Food Logistics

Growth of Seafood and Agricultural Export Supply Chains - Market Challenges

High Capital Investment Requirements for Refrigeration Infrastructure

Energy Consumption and Operational Cost Pressures

Limited Skilled Workforce for Cold Chain Management - Market Opportunities

Expansion of E-commerce Grocery Distribution Networks

Development of Integrated Logistics Zones and Free Trade Areas

Adoption of Smart Monitoring and IoT Temperature Tracking Systems - Trends

Deployment of IoT-enabled Cold Chain Monitoring Systems

Integration of Automated Cold Storage Warehousing

Growth of Pharmaceutical Grade Cold Logistics Facilities - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Transportation Services

Temperature Controlled Warehousing

Blast Freezing and Rapid Chilling Systems

Pharmaceutical Cold Storage Solutions

Integrated Cold Chain Distribution Systems - By Platform Type (In Value%)

Road-based Refrigerated Logistics

Air Cargo Cold Chain Logistics

Seaport Cold Storage and Container Handling

Multimodal Temperature Controlled Logistics

Integrated Distribution Hub Platforms - By Fitment Type (In Value%)

Standalone Refrigeration Systems

Integrated Cold Storage Facilities

Modular Cold Chain Units

Mobile Refrigeration Units

Containerized Temperature Controlled Systems - By End User Segment (In Value%)

Food and Beverage Producers

Pharmaceutical and Biotechnology Companies

Retail and Supermarket Chains

Agriculture and Fisheries Exporters

Healthcare and Vaccine Distribution Networks - By Procurement Channel (In Value%)

Direct Logistics Service Contracts

Government and Public Sector Tenders

Third Party Logistics Partnerships

Long-term Distribution Agreements

Cold Chain Infrastructure Leasing

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Temperature Monitoring Technology, Warehouse Automation Level, Geographic Coverage, Multimodal Logistics Capability, Industry Partnerships, Regulatory Compliance Standards, Service Portfolio Diversity, Pharmaceutical Grade Infrastructure)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain

Kuehne + Nagel

DB Schenker

DSV A/S

CEVA Logistics

Aramex

Agility Logistics

Gulf Agency Company Logistics

Bahwan Logistics

Al Nowras Logistics Solutions

Milaha Logistics

Yusen Logistics

Nippon Express

Expeditors International

Kerry Logistics

- Growing Demand from Pharmaceutical Import and Distribution Companies

- Retail Chains Expanding Temperature Controlled Food Supply Networks

- Seafood Exporters Increasing Reliance on Refrigerated Logistics

- Healthcare Sector Expansion Driving Vaccine and Biologic Distribution

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now