Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Oman Diagnostic Labs market generated approximately USD ~ million in revenue, supported by rising demand for clinical diagnostics, preventive health screening, and hospital-linked laboratory services across the national healthcare system. Growth is driven by expanding hospital infrastructure, increasing prevalence of chronic diseases, and broader adoption of advanced testing technologies including molecular diagnostics and immunoassay platforms. Government investment through the Ministry of Health and private hospital networks continues to strengthen diagnostic capacity and laboratory modernization.

Diagnostic laboratory activity is concentrated primarily in Muscat due to its dense healthcare infrastructure, advanced hospital networks, and the presence of major private diagnostic centers and tertiary medical institutions. Cities including Salalah and Sohar also contribute significantly as regional healthcare hubs supported by government hospitals and expanding private laboratory chains. Strong public healthcare coverage, increasing outpatient diagnostic demand, and the development of integrated hospital laboratories across these urban centers continue to reinforce their leadership within Oman’s diagnostic services ecosystem.

Market Segmentation

By Product Type

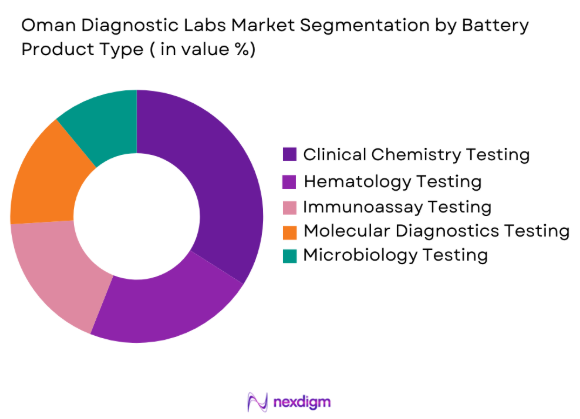

Oman Diagnostic Labs market is segmented by product type into clinical chemistry testing, haematology testing, immunoassay testing, molecular diagnostics testing, and microbiology testing. Recently, clinical chemistry testing has a dominant market share due to factors such as routine diagnostic demand, integration within hospital laboratory workflows, and widespread use for chronic disease monitoring. Clinical chemistry analysers process large volumes of tests related to metabolic disorders, diabetes monitoring, kidney function, and cardiovascular risk assessment. Hospitals and diagnostic centres rely heavily on these tests for daily patient screening and medical decision-making, making them core laboratory services across the healthcare system. Automated chemistry analysers also enable laboratories to process high testing volumes efficiently, reducing operational costs while improving turnaround times.

By End User

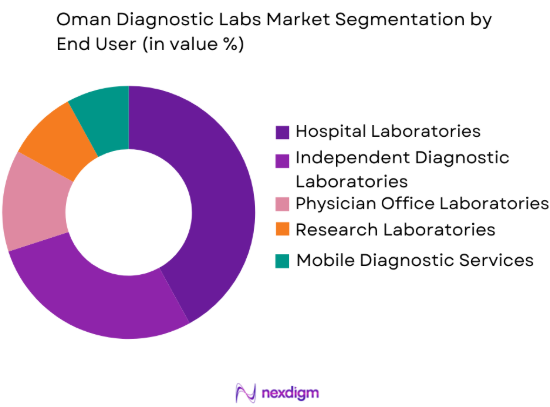

Oman Diagnostic Labs market is segmented by end users into hospital laboratories, independent diagnostic laboratories, physician office laboratories, research laboratories, and mobile diagnostic services. Recently, hospital laboratories have a dominant market share due to factors such as integrated healthcare delivery models, strong patient inflow, and centralized diagnostic capabilities within hospital facilities. Large hospitals across Muscat and other urban regions operate comprehensive diagnostic laboratories capable of performing complex clinical tests ranging from hematology to molecular diagnostics. Hospitals also manage emergency testing, inpatient diagnostics, and routine outpatient laboratory services, allowing them to capture a significant share of testing volumes. Government hospitals in particular maintain extensive laboratory networks supporting public healthcare programs and disease monitoring initiatives.

Competitive Landscape

The Oman Diagnostic Labs market is moderately consolidated, with international diagnostic technology companies partnering with local laboratories and hospital networks to expand testing capabilities. Global diagnostics firms supply advanced laboratory analysers, reagents, and automation systems, while domestic healthcare providers operate laboratory facilities across major urban centres. Strategic collaborations between hospitals, diagnostic companies, and technology providers enable the introduction of advanced testing solutions including molecular diagnostics and automated clinical chemistry platforms.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Distribution Network |

| Roche Diagnostics | 1896 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | United States | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| Sysmex Corporation | 1968 | Japan | ~ | ~ | ~ | ~ | ~ |

| Mindray Medical International | 1991 | China | ~ | ~ | ~ | ~ | ~ |

Oman Diagnostic Labs Market Analysis

Growth Drivers

Expansion of Government Healthcare Infrastructure and National Diagnostic Capacity

Government investment in healthcare infrastructure is a major factor supporting growth in the Oman Diagnostic Labs market. National healthcare programs focus on strengthening diagnostic capabilities within hospitals and expanding laboratory capacity across public medical facilities. Hospitals in Muscat, Sohar, Nizwa, and Salalah are upgrading laboratories with automated analyzers and digital laboratory information systems to improve testing efficiency and accuracy. Rising population levels and increasing healthcare utilization also require greater diagnostic capacity. Public health initiatives promoting early disease detection through routine screenings and health checkups further increase laboratory testing demand. Collaboration with international diagnostic technology providers is also accelerating laboratory modernization across Oman.

Rising Prevalence of Chronic Diseases and Preventive Healthcare Demand

The rising prevalence of chronic diseases in Oman is significantly increasing demand for diagnostic laboratory services and routine medical testing. Conditions such as diabetes, cardiovascular disorders, and metabolic diseases require continuous laboratory monitoring for diagnosis and treatment management. Healthcare providers depend on laboratory tests to evaluate blood glucose levels, lipid profiles, kidney function, and hormonal balance. Growing awareness of preventive healthcare is also encouraging individuals to undertake routine medical screenings. Employers and insurance providers promote health assessment programs that rely heavily on laboratory diagnostics. Hospitals and private laboratories are therefore expanding testing capacity while adopting automated systems to manage increasing diagnostic volumes efficiently.

Market Challenges

High Capital Investment Requirements for Advanced Diagnostic Equipment

The Oman Diagnostic Labs market faces financial constraints due to the high cost of advanced laboratory equipment and automation technologies required for modern diagnostics. Laboratories must invest in systems such as molecular diagnostic platforms, immunoassay analyzers, and automated sample processing units to deliver comprehensive testing services. These technologies involve significant expenses related to procurement, installation, maintenance, and specialized consumables. Smaller diagnostic centers often face difficulties adopting such equipment because of limited budgets. Dependence on imported diagnostic instruments and reagents also raises costs due to logistics and currency fluctuations. These financial pressures can slow technology adoption and limit laboratory expansion across Oman.

Shortage of Skilled Laboratory Professionals and Diagnostic Specialists

The Oman Diagnostic Labs market faces workforce challenges due to the limited availability of skilled laboratory professionals capable of operating advanced diagnostic technologies. Modern laboratories require trained clinical scientists, microbiologists, and molecular diagnostic specialists to manage complex testing procedures and automated systems. Recruiting and retaining qualified personnel is difficult because global healthcare demand increases competition for experienced professionals. Laboratories also require continuous staff training to operate evolving diagnostic technologies and maintain strict quality standards. Many healthcare providers depend on international recruitment to fill specialized roles, increasing operational costs. Workforce shortages can slow testing processes and affect laboratory efficiency, making workforce development a key priority for the sector.

Opportunities

Adoption of Molecular Diagnostics and Precision Medicine Technologies

The adoption of molecular diagnostics and precision medicine is creating strong opportunities for the Oman Diagnostic Labs market. Molecular testing allows laboratories to analyze genetic material and detect infections, genetic disorders, and cancers at an early stage. Hospitals and advanced diagnostic centers are increasingly investing in polymerase chain reaction platforms and genomic testing technologies to support targeted treatment. These methods improve diagnostic accuracy and help physicians develop personalized treatment plans. Government healthcare programs promoting early disease detection further encourage the use of advanced diagnostics. Growing awareness among healthcare professionals and patients is expanding demand for genetic testing, enabling laboratories to broaden specialized diagnostic services and strengthen clinical capabilities.

Expansion of Private Diagnostic Laboratory Networks and Preventive Screening Services

The expansion of private diagnostic laboratory networks and preventive health screening services presents a significant opportunity for the Oman Diagnostic Labs market. Private healthcare providers are establishing diagnostic centers across major cities and regional healthcare hubs to meet growing demand for convenient laboratory testing. These laboratories provide services ranging from routine blood tests to advanced molecular diagnostics. Faster turnaround times and extended service hours improve accessibility compared to traditional hospital laboratories. Preventive health screening programs promoted by employers and insurers further increase testing volumes. Mobile diagnostic services and home sample collection are also expanding access to laboratory testing. Rising awareness of preventive healthcare continues to encourage individuals to undertake routine diagnostic examinations.

Future Outlook

Oman Diagnostic Labs market is expected to experience steady expansion supported by increasing healthcare investment, rising diagnostic demand, and continuous technological advancement in laboratory testing systems. Automation, molecular diagnostics, and digital laboratory information systems will enhance diagnostic accuracy and operational efficiency across healthcare providers. Government healthcare modernization programs and private sector investment will continue strengthening diagnostic infrastructure across major cities. Growing awareness of preventive healthcare and early disease detection will further increase diagnostic testing demand throughout the healthcare system.

Major Players

- Siemens Healthineers

- Roche Diagnostics

- Abbott Laboratories

- Beckman Coulter

- ThermoFisher Scientific

- Sysmex Corporation

- Bio-Rad Laboratories

- Mindray Medical International

- Agilent Technologies

- BD Diagnostics

- DiaSorin S.p.A.

- Horiba Ltd

- Hitachi High-Technologies

- Danaher Corporation

- GE Healthcare

Key Target Audience

- Hospitals and healthcare providers

- Diagnostic laboratory chains

- Medical device manufacturers

- Pharmaceutical companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare technology companies

- Healthcare infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identification of critical market variables including diagnostic technologies, laboratory infrastructure, healthcare spending, and testing demand patterns across Oman. Data sources include government healthcare reports, hospital infrastructure data, and diagnostic equipment market information.

Step 2: Market Analysis and Construction

Collected data is analyzed to construct the market structure by examining laboratory services, testing technologies, and healthcare provider demand. Market segmentation models are developed to evaluate diagnostic product types, laboratory service categories, and end-user demand across healthcare institutions.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary research findings are validated through consultation with healthcare industry experts, diagnostic laboratory professionals, and medical technology specialists. These insights help confirm market dynamics, competitive developments, and operational trends influencing the diagnostic laboratories market.

Step 4: Research Synthesis and Final Output

Validated data and expert insights are integrated into a comprehensive analytical framework that presents market segmentation, competitive positioning, growth drivers, and future outlook. The final report synthesizes quantitative data with qualitative industry analysis to produce actionable market intelligence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Adoption of Advanced Diagnostic Technologies

Rising Demand for Early Disease Detection

Government Initiatives to Expand Healthcare Infrastructure - Market Challenges

High Capital Expenditure for Advanced Equipment

Shortage of Skilled Laboratory Personnel

Regulatory Compliance Complexity - Market Opportunities

Expansion of Tele-diagnostics and Remote Testing Services

Public-Private Partnerships in Healthcare

Integration of AI and Automation in Diagnostic Workflows - Trends

Shift Towards Personalized and Precision Medicine

Growth of Point-of-Care Testing

Digital Transformation in Laboratory Management - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

By Market Value, 2020-2025

By Installed Units, 2020-2025

By Average System Price, 2020-2025

By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Analyzers

Hematology Analyzers

Molecular Diagnostics Systems

Immunoassay Analyzers

Point-of-Care Testing Devices - By Platform Type (In Value%)

Laboratory Information Systems

Automated Robotic Platforms

Manual Benchtop Instruments

Portable/Handheld Platforms

Integrated Multi-diagnostic Platforms - By Fitment Type (In Value%)

On-premise Laboratory Solutions

Outsourced/Contract Laboratory Services

Mobile Diagnostic Units

Hybrid Lab Solutions

Modular Diagnostic Systems - By End User Segment (In Value%)

Hospitals & Healthcare Networks

Diagnostic Centers & Clinics

Research & Academic Institutions

Government Health Departments

Private Sector Corporations - By Procurement Channel (In Value%)

Direct Manufacturer Sales

Distributor Networks

Government Tenders

Online B2B Platforms

Third-party Service Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Adoption Level, Automation Integration, Service Coverage, Regulatory Compliance, Regional Presence, Pricing Model)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Siemens Healthineers

Roche Diagnostics

Abbott Laboratories

Beckman Coulter

Bio-Rad Laboratories

Thermo Fisher Scientific

Sysmex Corporation

Danaher Corporation

Horiba Ltd

Agilent Technologies

Mindray Medical International

Hitachi High-Technologies

GE Healthcare

BD Diagnostics

DiaSorin S.p.A.

- Hospitals Increasing Investment in Advanced Diagnostics

- Government Departments Driving Standardization and Compliance

- Diagnostic Centers Expanding Service Offerings

- Private Corporations Adopting Employee Health Screening Programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now