Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Oman Last-Mile Delivery Market was valued at approximately USD ~ million according to logistics sector estimates published by the International Trade Administration and regional logistics authorities. Market growth is driven primarily by expanding e-commerce platforms, rising digital payment adoption, and increasing consumer demand for fast home delivery services. The rapid expansion of online retail platforms, food delivery applications, and omnichannel retail strategies has strengthened logistics networks, encouraging investments in fleet infrastructure, route optimization technologies, and advanced delivery management systems.

Muscat dominates delivery activity because it functions as the country’s largest commercial hub with strong e-commerce penetration, dense residential zones, and major retail infrastructure. Sohar and Salalah also serve as key logistics centers due to the presence of major ports, industrial zones, and growing urban populations demanding delivery services. Government investments in logistics infrastructure, smart city initiatives, and digital commerce platforms across these cities strengthen delivery network efficiency while supporting the expansion of courier, grocery, and food delivery operations.

Market Segmentation

By Service Type

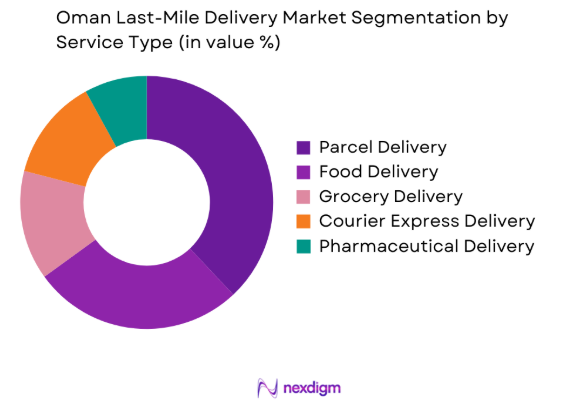

Oman Last-Mile Delivery Market is segmented by product type into parcel delivery, food delivery, grocery delivery, pharmaceutical delivery, and courier express delivery. Recently, parcel delivery has a dominant market share due to strong expansion of e-commerce retail platforms and rising demand for home delivery services. Retailers and online marketplaces increasingly depend on parcel delivery networks to transport consumer electronics, fashion products, and household items directly to customers. Expanding online shopping habits, improvements in digital payment systems, and investments in logistics infrastructure further strengthen parcel delivery demand. Delivery companies continue expanding fleet capacity, smart routing technology, and automated parcel management systems to handle increasing package volumes. Large e-commerce platforms collaborate with logistics providers to ensure faster delivery times and improve customer satisfaction.

By Delivery Vehicle Type

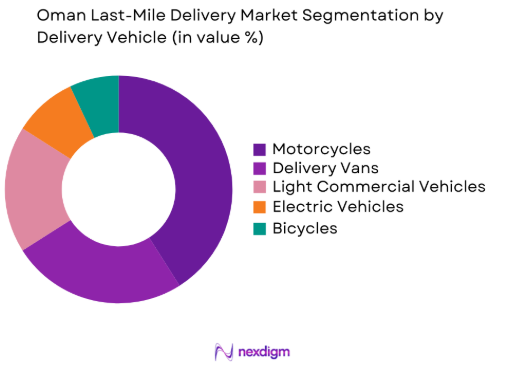

Oman Last-Mile Delivery Market is segmented by product type into motorcycles, delivery vans, light commercial vehicles, bicycles, and electric vehicles. Recently, motorcycles have a dominant market share due to their operational efficiency in dense urban environments where traffic congestion and narrow streets require agile transportation solutions. Motorcycles enable delivery companies to complete high volumes of orders quickly while minimizing fuel consumption and operating costs. Food delivery and courier companies rely heavily on motorcycle fleets to manage rapid delivery schedules and maintain service efficiency. Motorcycles also require lower capital investment compared to larger vehicles, enabling delivery startups and small logistics providers to expand operations quickly. Increasing demand for on-demand food delivery and small parcel shipments further strengthens motorcycle fleet deployment. As urban delivery volumes continue increasing, motorcycles remain the most practical vehicle type for navigating city traffic and maintaining fast delivery turnaround times.

Competitive Landscape

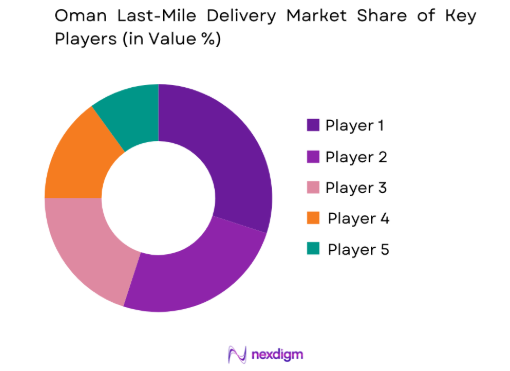

The Oman Last-Mile Delivery Market is moderately consolidated with several international logistics companies and regional delivery platforms competing to capture growing e-commerce logistics demand. Major players leverage strong delivery networks, advanced route optimization technologies, and partnerships with retail and e-commerce platforms to strengthen market presence. Companies continue investing in digital logistics management systems, automated parcel tracking, and mobile delivery platforms to enhance operational efficiency and customer experience while expanding delivery coverage across urban and suburban regions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Size |

| Aramex | 1982 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| DHL eCommerce | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Fetchr | 2012 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| Asyad Express | 2016 | Muscat, Oman | ~ | ~ | ~ | ~ | ~ |

| Shipa Delivery | 2018 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

Oman Last-Mile Delivery Market Analysis

Growth Drivers

Expansion of E-Commerce Retail Platforms Across Oman

The rapid expansion of e-commerce retail platforms across Oman is significantly increasing demand for last-mile delivery services as consumers increasingly purchase products through digital marketplaces and mobile shopping applications. Online retailers require efficient logistics networks capable of delivering goods quickly across urban and suburban areas while maintaining high service reliability and customer satisfaction. Retail platforms invest in logistics partnerships to ensure faster delivery and smooth order fulfillment. Growth in digital payment adoption further encourages frequent online purchases. Logistics companies respond by expanding delivery fleets and implementing advanced delivery management systems that improve route planning and package handling. Investments in automated sorting facilities and real-time tracking technologies also enhance delivery efficiency while supporting growing parcel volumes.

Increasing Urban Population and On-Demand Delivery Expectations

Rapid urban population growth across Oman is increasing demand for fast and reliable last-mile delivery services as consumers expect convenient home delivery for food, groceries, electronics, and daily essentials. Urban residents frequently use mobile applications to place orders requiring immediate or same-day delivery, creating strong pressure on logistics networks. Delivery companies expand fleets and recruit additional drivers to handle growing order volumes. Traffic congestion in major cities encourages the adoption of route optimization software to reduce delivery delays. Retailers also establish local distribution centers near residential areas to shorten delivery distances. Rising demand for convenience services strengthens food and grocery delivery platforms. Real-time tracking and digital communication tools further improve delivery coordination.

Market Challenges

High Operational Costs and Fuel Price Volatility Affecting Delivery Profitability

Rising operational costs pose major challenges for last-mile delivery companies operating in Oman as logistics activities require continuous investment in vehicle fleets, driver wages, maintenance services, and fuel consumption. Fluctuating fuel prices directly affect transportation expenses, making it difficult for companies to maintain stable profit margins. Logistics providers must optimize delivery routes and improve vehicle utilization to control fuel usage and operational inefficiencies. Increasing labor costs also add financial pressure on delivery networks that depend heavily on drivers. Fleet maintenance further increases operating expenses and operational complexity. Companies attempt to manage costs through route optimization systems and automated logistics technologies. However, adopting advanced logistics platforms requires significant investment in software systems and workforce training.

Limited Logistics Infrastructure in Rural and Remote Regions

Delivering goods to rural and remote regions across Oman presents significant logistical challenges due to long travel distances, limited road connectivity, and lower population density compared with urban centers. Delivery companies must allocate additional vehicles, drivers, and fuel resources to serve these areas, which increases operational expenses and delivery times. Rural logistics networks often lack distribution hubs and storage facilities needed for efficient parcel processing. As a result, shipments must travel from centralized urban warehouses to distant destinations, reducing delivery efficiency. Low delivery volumes per route further increase transportation costs. Although government investments aim to improve national logistics infrastructure, service expansion beyond urban centers remains operationally complex.

Opportunities

Integration of Smart Logistics Technologies and AI-Based Route Optimization

Adoption of smart logistics technologies is creating strong growth opportunities for last-mile delivery providers in Oman as companies increasingly implement artificial intelligence, advanced data analytics, and route optimization software to improve delivery efficiency. AI-based logistics platforms analyze traffic patterns, delivery locations, and fleet availability to determine faster and more cost-effective routes. These systems help logistics providers reduce delivery times while lowering fuel consumption and operating costs. Real-time parcel tracking tools also enhance transparency by enabling customers to monitor deliveries through mobile applications. Advanced analytics platforms allow companies to forecast demand patterns and manage delivery resources more efficiently. Automation within parcel sorting facilities further accelerates package processing and improves overall delivery turnaround performance.

Expansion of Electric Delivery Fleets Supporting Sustainable Logistics Operations

Growing environmental awareness and sustainability initiatives are creating new opportunities for logistics providers to introduce electric delivery vehicles across Oman’s last-mile delivery networks. Electric vehicles reduce operational expenses because they require lower maintenance and eliminate fuel consumption costs associated with traditional vehicles. Logistics companies adopting electric fleets can significantly lower carbon emissions while aligning with national environmental policies and sustainability objectives. These vehicles are well suited for short-distance urban deliveries where frequent stops and dense traffic conditions are common. Government programs promoting electric mobility and clean transportation further encourage logistics companies to invest in electric delivery solutions. Expanding charging infrastructure across major cities supports reliable fleet operations and improves delivery efficiency for urban logistics providers.

Future Outlook

The Oman Last-Mile Delivery Market is expected to experience sustained expansion driven by rising e-commerce penetration, increasing digital commerce adoption, and growing consumer demand for rapid home delivery services. Logistics companies are likely to invest heavily in automation technologies, route optimization platforms, and electric vehicle fleets to improve delivery efficiency and sustainability. Government initiatives supporting logistics infrastructure development and digital trade platforms will further strengthen delivery networks. Expanding retail and food delivery ecosystems will continue generating strong demand for last-mile logistics services.

Major Players

- Aramex

- DHL eCommerce

- Fetchr

- ShipaDelivery

- AsyadExpress

- FedEx

- UPS

- NaqelExpress

- SMSA Express

- Careem NOW

- Talabat

- iMileDelivery

- Jeebly

- Kuehne + Nagel

- DB Schenker

Key Target Audience

- E-commerce companies

- Food delivery platforms

- Retail and supermarket chains

- Logistics and supply chain companies

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Pharmaceutical distribution companies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying critical variables influencing the Oman Last-Mile Delivery Market including e-commerce growth, delivery fleet expansion, logistics infrastructure development, and urbanization patterns. Industry reports, government logistics statistics, and international trade publications are analyzed to determine relevant market indicators.

Step 2: Market Analysis and Construction

Market sizing is constructed through evaluation of logistics industry revenue, parcel delivery volumes, fleet infrastructure development, and e-commerce transaction growth across the country. Secondary research sources including logistics associations, government trade authorities, and industry databases support market modeling.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions and forecasts are validated through consultations with logistics industry professionals, transportation planners, and supply chain experts who provide insights regarding delivery operations, infrastructure capacity, and technology adoption trends.

Step 4: Research Synthesis and Final Output

All collected data is synthesized using analytical models to produce a comprehensive market report covering market structure, segmentation, competitive landscape, operational challenges, and long-term growth opportunities within the Oman Last-Mile Delivery Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-Commerce Retail Sector

Increasing Urbanization and Digital Ordering Adoption

Growth of On-Demand Food and Grocery Delivery - Market Challenges

High Operational Costs and Fuel Price Volatility

Urban Traffic Congestion Affecting Delivery Efficiency

Limited Delivery Infrastructure in Remote Regions - Market Opportunities

Adoption of Smart Route Optimization Technologies

Expansion of Same Day and Instant Delivery Services

Integration of Electric Vehicles in Delivery Fleets - Trends

Growth of App Based Delivery Aggregator Platforms

Rising Demand for Contactless Delivery Solutions

Deployment of AI Driven Logistics Management Systems - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Systems

Food Delivery Systems

Grocery Delivery Systems

Courier Express Delivery Systems

Same Day Delivery Systems - By Platform Type (In Value%)

E-Commerce Marketplace Platforms

Retailer Owned Delivery Platforms

Third Party Logistics Platforms

Mobile App Based Delivery Platforms

Omnichannel Delivery Platforms - By Fitment Type (In Value%)

In-House Delivery Fleet

Outsourced Delivery Services

Hybrid Delivery Model

Crowdsourced Delivery Network

Dedicated Contract Delivery - By End User Segment (In Value%)

E-Commerce Retailers

Food and Beverage Companies

Grocery and Supermarket Chains

Pharmaceutical and Healthcare Providers

Electronics and Consumer Goods Retailers - By Procurement Channel (In Value%)

Direct Contracts with Logistics Providers

E-Commerce Platform Partnerships

Third Party Logistics Procurement

Retailer Managed Delivery Procurement

Aggregator Platform Contracts

- Market Share Analysis

- Cross Comparison Parameters (Delivery Speed Capability, Fleet Size, Geographic Coverage, Technology Integration, Partnership Network, Same-Day Delivery Capability, Cost per Delivery Efficiency, Real-Time Tracking Systems, Route Optimization Technology, Reverse Logistics Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Aramex

DHL eCommerce

Fetchr

Jeebly

Shipa Delivery

Asyad Express

Talabat

Careem NOW

iMile Delivery

Naqel Express

SMSA Express

FedEx

UPS

DHL Supply Chain

Kuehne + Nagel

- E-Commerce Retailers Driving High Volume Parcel Deliveries

- Food Delivery Platforms Expanding Urban Logistics Demand

- Retail Chains Integrating Omnichannel Fulfillment Models

- Healthcare and Pharmacy Deliveries Increasing Demand for Rapid Distribution

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now