Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Oman Medical Tourism market generated approximately USD ~ billion in healthcare and related tourism revenue, supported by rising cross-border patient inflows and growing private hospital investments. Expansion of advanced medical infrastructure, internationally accredited hospitals, and specialized treatment centers has strengthened Oman’s healthcare service capabilities. Government initiatives promoting healthcare sector diversification and tourism development have also stimulated demand. Competitive treatment costs, modern medical technology, and integrated hospitality services further enhance Oman’s attractiveness for international medical travelers.

Muscat dominates the Oman Medical Tourism market due to its concentration of tertiary hospitals, advanced specialty clinics, and internationally accredited healthcare facilities that attract patients from the GCC region, Africa, and South Asia. Cities such as Sohar and Salalah are also gaining prominence because of expanding private healthcare networks and improved tourism infrastructure. Strategic air connectivity through Muscat International Airport, government investment in medical facilities, and integrated wellness tourism offerings contribute to the country’s growing position as a regional healthcare destination.

Market Segmentation

By Treatment Type

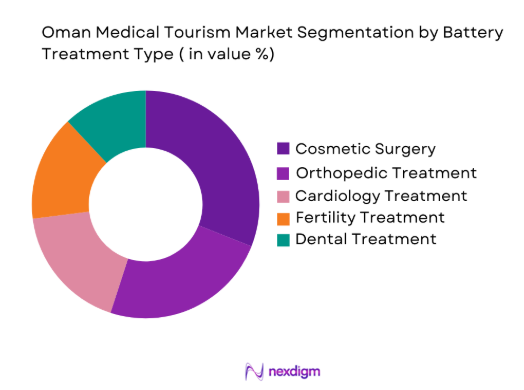

Oman Medical Tourism market is segmented by treatment type into cosmetic surgery, orthopaedic treatment, cardiology treatment, fertility treatment, and dental treatment. Recently, cosmetic surgery has a dominant market share due to factors such as growing demand for elective procedures, advanced aesthetic treatment facilities, and high patient inflows from neighbouring Gulf countries. Private hospitals and specialized cosmetic clinics in Muscat offer internationally accredited surgeons and modern surgical technology that attract international patients seeking quality aesthetic treatments at competitive costs. Cosmetic procedures such as rhinoplasty, liposuction, skin rejuvenation, and facial reconstruction have become particularly popular among regional travelers. The integration of luxury hospitality services, personalized recovery programs, and advanced dermatology clinics further enhances patient experience. Increasing social acceptance of aesthetic treatments and rising disposable incomes across GCC economies also contribute to strong demand for cosmetic procedures in Oman’s medical tourism sector.

By Service Provider

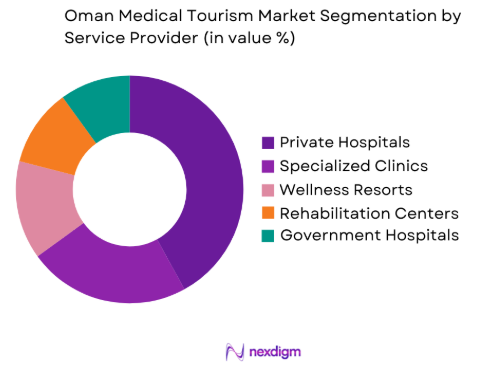

Oman Medical Tourism market is segmented by service provider into private hospitals, specialized clinics, wellness resorts, rehabilitation centers, and government hospitals. Recently, private hospitals have a dominant market share due to factors such as superior infrastructure, internationally accredited medical services, and advanced medical technologies available within these facilities. Leading private healthcare groups in Oman invest heavily in modern surgical equipment, robotic treatment systems, and specialized medical departments to attract international patients. Many private hospitals offer dedicated international patient departments that coordinate medical consultations, travel arrangements, accommodation, and post-treatment recovery programs. Strategic partnerships between private hospitals and global healthcare providers further strengthen clinical capabilities and treatment quality. High service standards, shorter waiting times, and comprehensive treatment packages continue to position private hospitals as the preferred service providers for international medical travelers visiting Oman.

Competitive Landscape

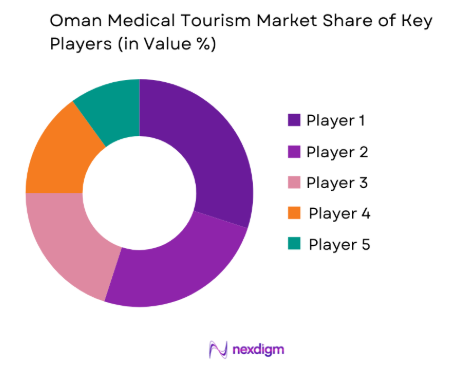

The Oman Medical Tourism market is moderately consolidated with a mix of regional hospital groups and international healthcare providers operating specialized treatment facilities. Major players focus on expanding tertiary care infrastructure, obtaining international hospital accreditations, and strengthening partnerships with global healthcare networks. Investments in advanced surgical technologies, international patient departments, and integrated hospitality services are strengthening competitive positioning. Private healthcare groups continue to dominate the market due to superior service quality and broader treatment portfolios.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | International Patient Services |

| Aster DM Healthcare | 1987 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| NMC Healthcare | 1975 | Abu Dhabi, UAE | ~ | ~ | ~ | ~ | ~ |

| Badr Al Samaa Group | 2002 | Muscat, Oman | ~ | ~ | ~ | ~ | ~ |

| KIMS Healthcare | 2002 | Trivandrum, India | ~ | ~ | ~ | ~ | ~ |

| Burjeel Holdings | 2007 | Abu Dhabi, UAE | ~ | ~ | ~ | ~ | ~ |

Oman Medical Tourism Market Analysis

Growth Drivers

Expansion of Advanced Private Healthcare Infrastructure in Oman

Expansion of advanced private healthcare infrastructure in Oman is a major driver for the medical tourism market because modern hospitals and specialized treatment centres improve the country’s capacity to manage complex medical procedures for international patients. Private healthcare providers in Muscat and other cities are investing in advanced diagnostics, robotic surgery, and specialized clinical departments that enhance treatment quality. International accreditation strengthens the credibility of Omani hospitals and builds trust among overseas patients. Hospitals increasingly provide multilingual support and integrated travel coordination services to improve patient experience. Strong regional healthcare demand and government support for private healthcare investment further strengthen Oman’s position as a growing medical tourism destination.

Rising Demand for Cost Effective Specialized Treatments among International Patients

Rising demand for cost effective specialized treatments among international patients is a key driver for the Oman medical tourism market as patients increasingly travel abroad to access high quality healthcare at lower costs. Treatment expenses in many developed countries remain high due to complex healthcare systems and operational costs. Oman offers competitive pricing for procedures such as cosmetic surgery, orthopedic treatments, dental procedures, and fertility services while maintaining strong clinical standards. Shorter waiting periods for specialized procedures further attract international patients. Adoption of internationally recognized treatment protocols and advanced medical technologies strengthens patient confidence and increases cross border healthcare travel to Oman.

Market Challenges

Limited Global Brand Recognition of Oman as a Medical Tourism Destination

Limited global brand recognition of Oman as a medical tourism destination presents a major challenge for market expansion because international patients often prefer established healthcare hubs with strong reputations. Countries such as Thailand, India, and Turkey have invested heavily in global healthcare marketing and international hospital networks that attract patients from multiple regions. Although Oman provides high quality medical services and advanced treatment facilities, its international visibility remains comparatively limited. Participation in global healthcare exhibitions, international accreditation programs, and medical tourism partnerships is still developing. Strengthening global promotion strategies and hospital branding will be essential for Oman to compete effectively in the international medical tourism market.

Dependence on Foreign Healthcare Professionals and Specialized Medical Expertise

Dependence on foreign healthcare professionals and specialized medical expertise represents a structural challenge for the Oman medical tourism market because a large share of the country’s specialized workforce comes through international recruitment. Surgeons, specialists, and advanced technicians from countries such as India and Europe support many high complexity procedures. While this expertise strengthens clinical capabilities, reliance on expatriate staff can create workforce vulnerabilities if recruitment pipelines are disrupted. Hospitals must offer competitive compensation to retain skilled professionals in a competitive global healthcare labor market. Expanding domestic medical education programs and specialist training initiatives will be essential to strengthen long term workforce sustainability.

Opportunities

Development of Integrated Medical and Wellness Tourism Packages

Development of integrated medical and wellness tourism packages represents a significant opportunity for the Oman medical tourism market because the country’s tourism assets complement healthcare services. Scenic coastlines, desert landscapes, luxury resorts, and cultural attractions enhance recovery experiences for international patients. Hospitals and wellness resorts can collaborate to offer treatment packages that combine medical procedures with rehabilitation therapies and hospitality services. Post treatment wellness programs such as physiotherapy and spa therapies support patient recovery while improving travel experiences. Government tourism initiatives promoting health and wellness travel, along with partnerships among hospitals, travel agencies, and resorts, can strengthen Oman’s competitiveness as an integrated medical tourism destination.

Expansion of Specialized Centers of Excellence for Complex Medical Procedures

Expansion of specialized centers of excellence for complex medical procedures presents a strong opportunity for the Oman medical tourism market as highly specialized facilities attract international patients seeking advanced treatment expertise. Centers dedicated to cardiology, orthopedic surgery, fertility treatment, oncology, and cosmetic surgery strengthen Oman’s ability to offer high quality specialized care. Establishing these centers requires investment in advanced surgical technologies, internationally trained medical professionals, and accredited treatment protocols. Collaboration with global medical institutions and healthcare networks enhances credibility and referral potential. As hospitals build strong reputations in specialized treatments, Oman can attract international patients while strengthening its healthcare infrastructure and clinical capabilities.

Future Outlook

The Oman Medical Tourism market is expected to experience steady expansion as healthcare infrastructure continues to improve and international patient inflows increase. Investments in advanced medical technologies, specialized treatment centers, and hospital accreditation programs will enhance treatment capabilities. Government initiatives promoting healthcare diversification and tourism development will further support sector growth. Growing regional demand for affordable specialized healthcare services and integrated wellness tourism packages will strengthen Oman’s position as an emerging medical tourism destination.

Major Players

- Aster DM Healthcare

- NMC Healthcare

- Badr Al Samaa Group of Hospitals

- KIMS Healthcare

- BurjeelHoldings

- Apollo Hospitals

- Cleveland Clinic Abu Dhabi

- MedcareHospitals

- Saudi German Hospital

- ThumbayHospital Group

- American Hospital Dubai

- Al Zahra Hospital Dubai

- Fortis Healthcare

- Riyadh Care Hospital

- Mediclinic Middle East

Key Target Audience

- Hospitals and healthcare providers

- Medical tourism facilitators

- Healthcare infrastructure developers

- Pharmaceutical companies

- Medical device manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare technology companies

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the critical variables influencing the Oman Medical Tourism market, including international patient flows, healthcare infrastructure capacity, treatment specialization, and government tourism policies. These variables form the foundation of the analytical framework used for the study.

Step 2: Market Analysis and Construction

A detailed market model is constructed using healthcare industry databases, tourism statistics, and hospital performance indicators. Secondary sources such as healthcare authorities, tourism ministries, and international medical tourism organizations are used to evaluate market size and demand patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including healthcare administrators, hospital executives, and medical tourism facilitators are consulted to validate market assumptions and emerging trends. Their insights help refine the analysis and ensure that the research reflects real operational dynamics within the sector.

Step 4: Research Synthesis and Final Output

The collected data and validated insights are synthesized into a comprehensive market report that evaluates market structure, competitive dynamics, growth drivers, and future opportunities. The final analysis provides actionable intelligence for stakeholders operating within the Oman Medical Tourism market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of High Quality Private Healthcare Infrastructure

Government Initiatives Promoting Healthcare Tourism

Rising Demand for Affordable Specialized Medical Treatments - Market Challenges

Limited Global Brand Recognition of Healthcare Facilities

Complex Medical Visa and Travel Coordination Processes

Dependence on Foreign Healthcare Specialists - Market Opportunities

Development of Integrated Medical and Wellness Tourism Packages

Strategic Partnerships with International Healthcare Networks

Expansion of Specialized Treatment Centers for International Patients - Trends

Integration of Hospitality Services with Medical Treatment Facilities

Growing Popularity of Cosmetic and Elective Medical Procedures

Digital Medical Tourism Platforms Enhancing Patient Coordination - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Cosmetic and Aesthetic Treatment Services

Orthopedic Treatment Services

Cardiology Treatment Services

Fertility and Reproductive Treatment Services

Dental Treatment Services - By Platform Type (In Value%)

Hospital Based Medical Tourism Programs

Specialized Private Clinics

Integrated Healthcare Resorts

Telemedicine Assisted Medical Tourism Platforms

Wellness and Rehabilitation Centers - By Fitment Type (In Value%)

Inpatient Treatment Packages

Outpatient Treatment Programs

Integrated Surgery and Recovery Packages

Diagnostic and Preventive Health Packages

Post Treatment Rehabilitation Services - By End User Segment (In Value%)

International Medical Tourists

Regional GCC Patients

Self Funded International Patients

Insurance Covered International Patients

Corporate Sponsored Medical Travelers - By Procurement Channel (In Value%)

Direct Hospital Bookings

Medical Tourism Facilitator Agencies

Government Medical Referral Programs

Insurance Network Referrals

Online Healthcare Booking Platforms

- Market Share Analysis

- Cross Comparison Parameters (Treatment Specialization, International Patient Services, Hospital Accreditation, Medical Tourism Partnerships, Treatment Cost Competitiveness, International Insurance Acceptance, Post Treatment Rehabilitation Services, Multilingual Patient Support, Digital Patient Coordination Platforms)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Aster Hospitals Oman

NMC Healthcare

Burjeel Medical City

KIMS Oman Hospital

Badr Al Samaa Group of Hospitals

Apollo Hospitals

Cleveland Clinic Abu Dhabi

Medcare Hospitals

Al Zahra Hospital Dubai

Saudi German Hospital

Thumbay Hospital Group

American Hospital Dubai

Fortis Healthcare

Aster DM Healthcare

Riyadh Care Hospital

- Growing demand from GCC patients seeking specialized treatments

- Increasing inflow of self funded international patients for elective procedures

- Rising corporate sponsored health travel programs for employees

- Expansion of insurance linked cross border treatment networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now