Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Oman’s semiconductor infrastructure market reached approximately USD ~ million based on a recent historical assessment, driven by assembly and test facility development, electronics manufacturing localization initiatives, and demand from defense, telecom, and industrial electronics sectors. Investment in cleanroom systems, specialty gas delivery, and microelectronics packaging environments is expanding through free-zone industrialization programs. National diversification strategies encouraging advanced manufacturing and electronics value-chain participation are sustaining infrastructure deployment across targeted industrial clusters.

Sohar and Duqm dominate semiconductor infrastructure activity due to industrial zone incentives, port-linked manufacturing logistics, and availability of large-scale utilities suitable for cleanroom and packaging facilities. Muscat hosts design, research, and electronics integration entities supporting upstream semiconductor activities. Regional supply partnerships with Asian semiconductor equipment and OSAT firms reinforce coastal industrial zones as emerging microelectronics manufacturing nodes aligned with Oman’s export-oriented industrial strategy.

Market Segmentation

By Product Type

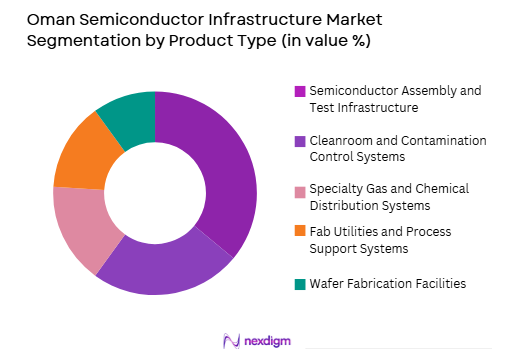

Oman Semiconductor Infrastructure Market is segmented by product type into semiconductor assembly and test infrastructure, cleanroom and contamination control systems, specialty gas and chemical distribution systems, fab utilities and process support systems, and wafer fabrication facilities. Recently, semiconductor assembly and test infrastructure has a dominant market share due to factors such as lower capital intensity compared with wafer fabrication, alignment with electronics manufacturing localization goals, and demand from defense and industrial electronics integration activities. Oman’s industrial policy prioritizes packaging and testing capabilities as entry points into semiconductor value chains, encouraging deployment of assembly lines, reliability testing labs, and microelectronics packaging environments in free zones. Partnerships with Asian OSAT providers and electronics manufacturers are accelerating installation of assembly equipment and test infrastructure.

By End User

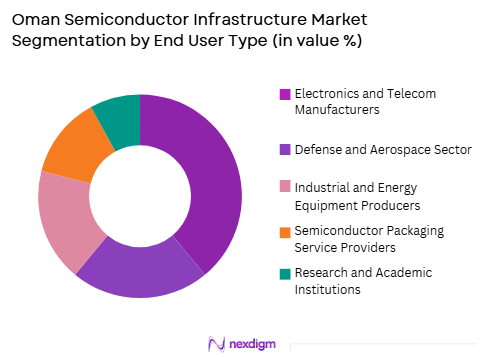

Oman Semiconductor Infrastructure Market is segmented by end user into electronics and telecom manufacturers, defense and aerospace sector, industrial and energy equipment producers, semiconductor packaging service providers, and research and academic institutions. Recently, electronics and telecom manufacturers have a dominant market share due to factors such as localization of electronics assembly, telecom equipment integration, and demand for sensor and communication module packaging facilities within industrial zones. Telecom and electronics firms operating in Sohar and Duqm require packaging, cleanroom, and test environments to support domestic assembly of communication devices, IoT modules, and embedded systems.

Competitive Landscape

Oman’s semiconductor infrastructure market is emerging and moderately concentrated among global semiconductor equipment suppliers, cleanroom engineering firms, and industrial infrastructure providers working with government industrial zones and electronics manufacturers. Market development is shaped by assembly and test partnerships, cleanroom system integration, and utilities engineering for microelectronics facilities. International equipment vendors collaborate with regional industrial developers and local contractors to establish packaging and testing infrastructure across Oman’s coastal industrial clusters.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Oman Role |

| Applied Materials | 1967 | USA | ~ | ~ | ~ | ~ | ~ |

| ASM Pacific Technology | 1975 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Tokyo Electron | 1963 | Japan | ~ | ~ | ~ | ~ | ~ |

| Air Liquide | 1902 | France | ~ | ~ | ~ | ~ | ~ |

| M+W Group (Exyte) | 1912 | Germany | ~ | ~ | ~ | ~ | ~ |

Oman Semiconductor Infrastructure Market Analysis

Growth Drivers

Electronics Manufacturing Localization and Packaging Capability Development

Oman’s semiconductor infrastructure market growth is strongly driven by national industrial diversification strategies promoting domestic electronics manufacturing and localized semiconductor packaging capability as feasible entry points into the global semiconductor value chain. Industrial policy frameworks emphasize assembly, testing, and electronics integration activities aligned with Oman’s logistics advantages and export orientation, encouraging investment in packaging lines, cleanroom environments, and semiconductor handling infrastructure. Telecom equipment assembly, sensor module production, and embedded electronics manufacturing for industrial and energy applications require localized packaging and testing facilities, creating sustained infrastructure demand. Partnerships with Asian OSAT providers and electronics manufacturers are transferring packaging technologies and process expertise into Oman’s industrial zones, accelerating facility deployment. Packaging infrastructure requires moderate capital compared with wafer fabrication, enabling scalable industrial participation with lower risk exposure. Defense electronics integration programs and secure supply requirements further stimulate domestic packaging capacity investment. Export-oriented electronics clusters in Sohar and Duqm rely on assembly and test infrastructure to add value to imported semiconductor components. Government incentives for advanced manufacturing facilities reduce investment barriers for microelectronics infrastructure projects.

Industrial Zone Infrastructure and Utilities Availability for Microelectronics Facilities

Expansion of specialized industrial zones in Sohar and Duqm providing reliable utilities, logistics connectivity, and regulatory incentives is a major driver of semiconductor infrastructure deployment in Oman. Microelectronics packaging and cleanroom facilities require stable power, high-purity water, specialty gas systems, and controlled environments, which are increasingly available in these coastal industrial clusters. Port-adjacent manufacturing zones enable efficient import of semiconductor components and export of packaged electronics products, enhancing supply-chain viability. Government-led industrial infrastructure development programs provide land, utilities, and regulatory facilitation tailored for advanced manufacturing sectors including microelectronics. Integration of electronics manufacturing with petrochemical and materials industries in these zones supports local supply chains for packaging materials and chemicals. Availability of large-scale utilities reduces operational risk for cleanroom and semiconductor process facilities. Industrial free-zone incentives and foreign investment frameworks attract international semiconductor equipment and packaging firms into Oman. Clustered manufacturing ecosystems encourage shared infrastructure such as gas distribution and contamination control systems. Proximity to ports and logistics corridors supports export competitiveness for electronics products. These industrial zone infrastructure advantages significantly lower barriers to semiconductor facility establishment, accelerating infrastructure market growth in Oman.

Market Challenges

Limited Domestic Semiconductor Design and Fabrication Ecosystem

Oman’s semiconductor infrastructure market faces structural constraints from the absence of a mature domestic semiconductor design and wafer fabrication ecosystem, limiting demand breadth for advanced semiconductor facilities. Packaging and testing infrastructure depends heavily on imported semiconductor components rather than locally fabricated wafers, reducing upstream integration potential. Lack of semiconductor foundries and large-scale chip design firms constrains development of full semiconductor value-chain clusters. Domestic electronics manufacturing remains focused on integration rather than chip innovation, limiting infrastructure sophistication requirements. Research capacity in semiconductor materials and device engineering is still nascent, affecting technology depth. Without local wafer fabrication, high-end fab utilities and process infrastructure demand remains limited. Talent availability in semiconductor engineering and process technology is also constrained. International semiconductor firms may prefer established Asian ecosystems for advanced operations. Infrastructure utilization may depend on external component supply chains vulnerable to global disruptions. These ecosystem gaps restrict expansion toward higher-value semiconductor infrastructure segments in Oman.

High Capital and Technology Barriers for Advanced Semiconductor Facilities

Semiconductor infrastructure development in Oman is challenged by high capital requirements and advanced technology complexity associated with microelectronics manufacturing environments. Cleanroom facilities, specialty gas systems, and precision packaging equipment require substantial investment and technical expertise. Financing mechanisms for semiconductor manufacturing infrastructure remain limited domestically, increasing reliance on foreign investment. Technology transfer and intellectual property considerations may restrict access to advanced packaging or fabrication capabilities. Import dependence for semiconductor equipment increases cost volatility and project risk. Skilled workforce requirements for microelectronics processes exceed current domestic training capacity. Small domestic market scale may limit economies of scale for advanced semiconductor facilities. Global semiconductor cycles and demand fluctuations affect investment stability. Environmental and contamination control standards impose stringent facility requirements. These financial and technological barriers constrain rapid scaling of semiconductor infrastructure in Oman.

Opportunities

Regional Electronics Assembly and Semiconductor Packaging Hub Positioning

Oman has opportunity to position itself as a regional hub for electronics assembly and semiconductor packaging serving Middle East and African markets lacking localized microelectronics manufacturing infrastructure. Logistics connectivity, industrial zones, and export orientation enable competitive packaging and testing operations. Regional electronics importers can outsource packaging and module integration to Oman-based facilities. Telecom, automotive, and industrial electronics markets in adjacent regions create demand for packaged semiconductor modules. Neutral trade positioning supports cross-regional supply partnerships. Government incentives for advanced manufacturing attract international packaging firms. Shared infrastructure clusters reduce cost barriers for entrants. Export-focused packaging facilities can scale with regional electronics demand growth. Collaboration with Asian OSAT leaders can accelerate capability development. This hub positioning can expand Oman’s semiconductor infrastructure market beyond domestic demand.

Advanced Electronics Manufacturing and Sensor Integration for Energy and Smart Infrastructure

Growth of energy digitalization, smart infrastructure, and industrial automation in Oman creates opportunity for localized semiconductor packaging and electronics manufacturing supporting sensors, control systems, and communication modules. Oilfield monitoring, smart grid systems, and industrial automation require integrated electronics assemblies. Local packaging and integration reduce supply-chain dependency for critical infrastructure electronics. Smart city and transport systems increase demand for embedded semiconductor modules. Defense and secure infrastructure projects require trusted electronics manufacturing environments. Industrial IoT adoption expands sensor module production needs. Integration of renewable energy and grid control electronics supports domestic manufacturing potential. Government digital infrastructure programs stimulate electronics demand. Packaging facilities can specialize in ruggedized and industrial semiconductor modules suited to regional environments. These application-driven electronics manufacturing opportunities can expand semiconductor infrastructure demand in Oman.

Future Outlook

Oman’s semiconductor infrastructure market is expected to expand steadily over the next five years as electronics manufacturing localization and packaging partnerships deepen across industrial zones. Assembly and test facilities will scale with export-oriented electronics production and regional demand. Industrial diversification policies and advanced manufacturing incentives will sustain infrastructure investment. Integration of semiconductor packaging with energy, telecom, and smart infrastructure sectors will broaden application demand across Oman’s microelectronics ecosystem.

Major Players

- Applied Materials

- ASML

- Tokyo Electron

- Lam Research

- KLA Corporation

- ASM Pacific Technology

- Amkor Technology

- ASE Technology

- Kulicke & Soffa

- JCET Group

- Powertech Technology

- Air Liquide

- Linde

- Exyte

- Edwards Vacuum

Key Target Audience

- Electronics and telecom manufacturers

- Defense and aerospace companies

- Industrial and energy equipment producers

- Semiconductor packaging service providers

- Industrial zone developers

- Government and regulatory bodies

- Advanced manufacturing investors

- Investments and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Key variables including assembly and test facility deployments, cleanroom installations, packaging equipment demand, and electronics manufacturing expansion were identified across Oman’s semiconductor ecosystem. Demand drivers across electronics, telecom, defense, and industrial sectors were mapped to infrastructure requirements. Supply-side variables such as industrial zone capacity and utilities availability were defined.

Step 2: Market Analysis and Construction

Primary and secondary inputs were integrated to construct the Oman semiconductor infrastructure market model, incorporating packaging partnerships, electronics manufacturing projects, and industrial diversification initiatives. Segmentation by product type and end user was applied to estimate shares. Competitive roles of equipment and cleanroom providers were assessed.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding packaging demand, electronics manufacturing growth, and industrial zone expansion were validated through consultations with semiconductor equipment specialists, industrial developers, and regional electronics manufacturers. Alignment with Oman’s industrial policy and manufacturing programs was verified. Sensitivity checks were applied to infrastructure scenarios.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into a structured Oman semiconductor infrastructure market report covering segmentation, competitive landscape, and strategic outlook. Quantitative estimates were aligned with facility deployment evidence and industrial strategy direction. The final output integrates drivers, constraints, and opportunities shaping semiconductor infrastructure growth in Oman.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National industrial diversification into advanced manufacturing

Strategic investments in electronics and semiconductor capability

Government-backed technology and research infrastructure programs - Market Challenges

High capital intensity and long gestation of semiconductor fabs

Limited domestic semiconductor manufacturing expertise

Dependence on imported semiconductor equipment and materials - Market Opportunities

Development of compound semiconductor and power device fabs

Regional semiconductor packaging and testing hub positioning

Public–private semiconductor R&D infrastructure initiatives - Trends

Shift toward modular and scalable fab infrastructure models

Integration of advanced packaging within fabrication ecosystems

Adoption of energy-efficient cleanroom and utility systems - Government regulations

Industrial localization and technology transfer frameworks

Foreign investment and strategic manufacturing incentives

Advanced manufacturing and technology development policies - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Facilities

Semiconductor Assembly and Packaging Lines

Cleanroom and Contamination Control Systems

Semiconductor Process Support Utilities

Testing and Metrology Infrastructure - By Platform Type (In Value%)

200mm and 300mm Fabrication Platforms

Advanced Packaging Platforms

Compound Semiconductor Platforms

MEMS and Sensor Platforms

Pilot and R&D Fab Platforms - By Fitment Type (In Value%)

Greenfield Semiconductor Fabs

Brownfield Fab Expansions

Modular Semiconductor Facilities

Pilot and Prototype Facilities

Retrofitted Legacy Fabs - By End User Segment (In Value%)

Integrated Device Manufacturers

Foundry Operators

OSAT Providers

Research and Academic Institutes

Government Semiconductor Programs - By Procurement Channel (In Value%)

Direct OEM Procurement

EPC Semiconductor Projects

Government Technology Programs

Strategic Technology Partnerships

Turnkey Fab Integrators

- Market Share Analysis

- Cross Comparison Parameters (Infrastructure Scope and Fab Type, Technology Node and Wafer Size Capability, Fab Capacity and Throughput, Cleanroom Class and Contamination Control, Process Integration Depth, Utilities and Subfab Systems Capability, EPC and Turnkey Delivery Model, Automation and Smart Fab Enablement, Energy Efficiency and Sustainability Design, Regional Service and Support Presence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ASML

Applied Materials

Lam Research

KLA Corporation

Tokyo Electron

ASM International

Advantest

Teradyne

Kulicke & Soffa

ASMPT

AIXTRON

EV Group

SUSS MicroTec

Air Liquide Electronics

Linde Electronics

- Government entities developing sovereign semiconductor capability

- Research institutes building pilot semiconductor fabrication lines

- Industrial firms seeking localized electronics supply chains

- Packaging and testing providers targeting regional demand

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now