Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Oman Semiconductor Manufacturing Market demonstrates gradual expansion as the country strengthens its advanced manufacturing ecosystem and electronics value chain across industrial diversification initiatives. Based on a recent historical assessment, the Oman semiconductor manufacturing market is valued at approximately USD ~ million, driven by increasing demand for integrated circuits, power semiconductors, and sensor chips used in telecommunications infrastructure, industrial automation systems, and consumer electronics supply chains. Government-led industrial diversification programs and foreign technology partnerships continue to stimulate semiconductor production investments across Oman’s emerging high-technology manufacturing sector.

Muscat and Sohar function as the most influential semiconductor manufacturing locations due to established industrial zones, export-oriented logistics infrastructure, and proximity to major electronics supply chains operating across the Gulf region and Asia. Sohar Industrial Port hosts several electronics assembly facilities supported by integrated logistics networks, while Muscat benefits from advanced industrial development programs and access to regional research collaborations. Strategic geographic positioning between Asian semiconductor exporters and Middle Eastern electronics markets further strengthens Oman’s role as a developing semiconductor manufacturing hub.

Market Segmentation

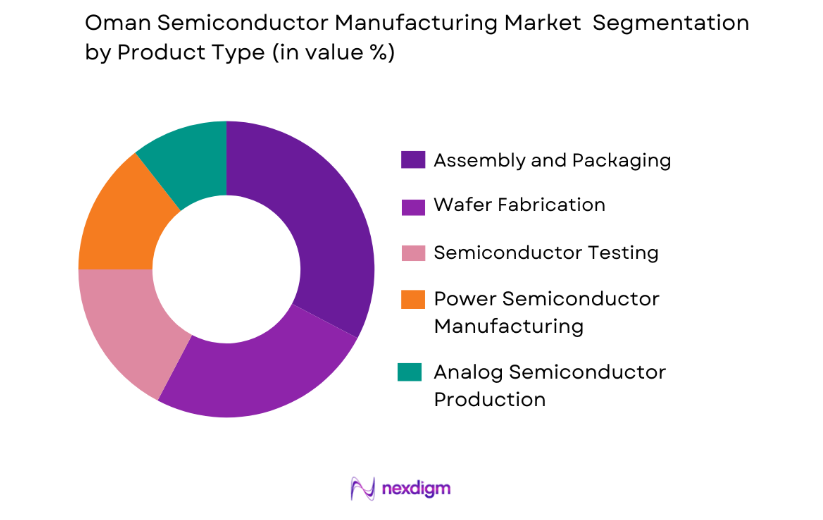

By product Type

Oman Semiconductor Manufacturing Market is segmented by product type into Wafer Fabrication, Assembly and Packaging, Semiconductor Testing, Analog Semiconductor Production, and Power Semiconductor Manufacturing. Recently, Assembly and Packaging has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Assembly and packaging operations require comparatively lower capital investment than full wafer fabrication plants while still supporting the semiconductor value chain through chip packaging, bonding, and final device integration processes. Oman’s industrial strategy emphasizes downstream electronics manufacturing and semiconductor packaging capabilities because these facilities can be integrated within existing industrial zones that already host electronics assembly and telecommunications equipment manufacturing activities. Global semiconductor companies often outsource packaging operations to specialized facilities located near logistics hubs capable of serving regional electronics markets. Sohar and Duqm industrial areas offer integrated logistics infrastructure, free trade zones, and supportive regulatory frameworks that attract semiconductor packaging providers. As consumer electronics imports, telecommunications hardware manufacturing, and industrial automation equipment demand continue expanding across the Gulf region, packaging operations become the most commercially viable semiconductor manufacturing activity within Oman’s developing technology sector.

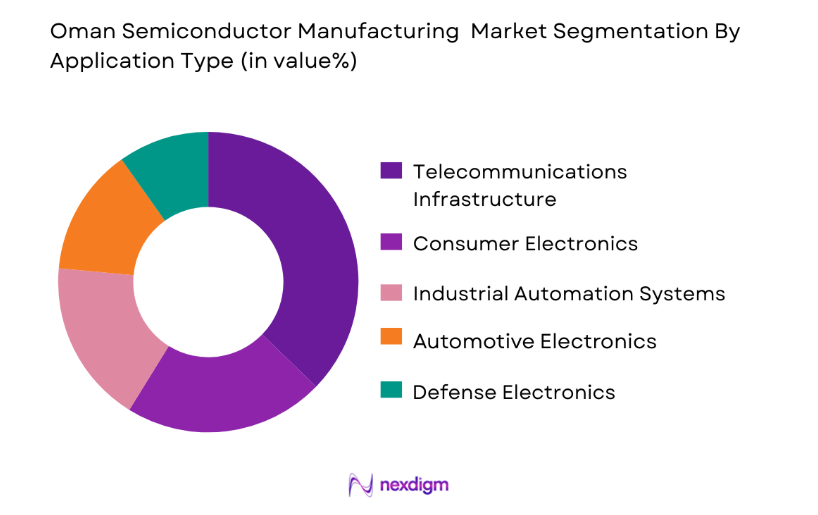

By Application

Oman Semiconductor Manufacturing Market is segmented by Application type into Consumer Electronics, Telecommunications Infrastructure, Automotive Electronics, Industrial Automation Systems, and Defense Electronics. Recently, Telecommunications Infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Telecommunications infrastructure projects across the Gulf region require significant quantities of semiconductor components including signal processors, power management chips, network switching circuits, and RF communication semiconductors used in mobile networks, fiber optic systems, and satellite communication equipment. Oman’s national digital transformation strategy encourages large scale deployment of telecommunications networks that support smart city infrastructure, digital government services, and advanced industrial automation environments. Semiconductor manufacturers supplying these infrastructure projects benefit from steady procurement demand linked to telecommunications network expansion programs implemented by regional operators. Additionally, telecommunications equipment manufacturers often locate assembly operations near logistics hubs capable of distributing networking equipment throughout the Middle East, which further strengthens semiconductor component demand supporting network hardware production across Oman’s technology ecosystem.

Competitive Landscape

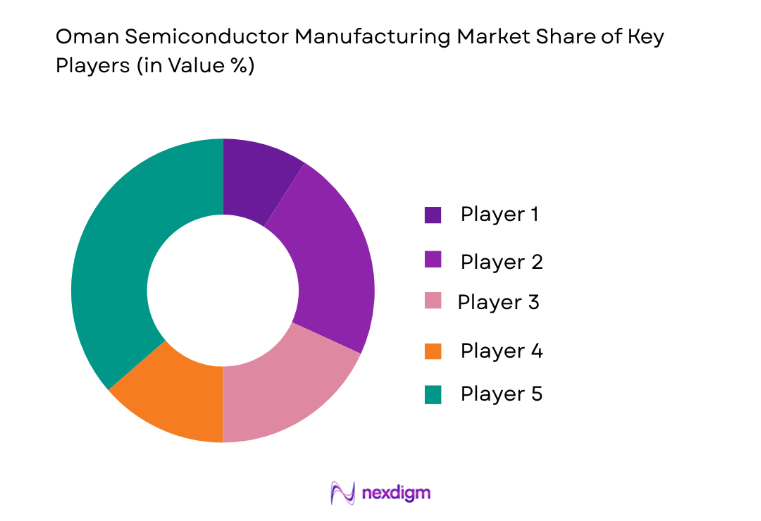

The Oman Semiconductor Manufacturing Market remains moderately concentrated with a combination of multinational semiconductor manufacturers and regional electronics assembly partners supporting the semiconductor value chain through packaging, testing, and specialized chip manufacturing. Global semiconductor companies maintain strong technological influence through equipment supply, fabrication expertise, and intellectual property development while regional manufacturers focus primarily on downstream semiconductor integration, packaging services, and electronics assembly activities. Strategic partnerships between international semiconductor leaders and regional industrial development authorities continue shaping competitive positioning within Oman’s emerging semiconductor ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Manufacturing Capability |

| Intel Corporation | 1968 | United States | ~ | ~ | ~ | ~ | |

| Taiwan Semiconductor Manufacturing Company | 1987 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics Semiconductor | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies | 1999 | Germany | ~ | ~ | ~ | ~ | ~ |

Oman Semiconductor Manufacturing Market Analysis

Growth Drivers

Expansion of Regional Electronics Manufacturing Ecosystem:

Oman’s semiconductor manufacturing sector benefits significantly from the expansion of electronics manufacturing activities occurring throughout the Gulf region as telecommunications hardware, industrial automation systems, and consumer electronic devices require increasing volumes of semiconductor components supporting advanced digital infrastructure development. Governments across the Middle East continue prioritizing domestic electronics production capabilities as part of broader industrial diversification strategies designed to reduce reliance on imported high technology equipment. Oman’s industrial development zones provide manufacturing incentives, logistics connectivity, and export oriented regulatory frameworks capable of supporting electronics manufacturing investments that indirectly stimulate semiconductor demand within the country. Semiconductor components represent essential inputs within nearly every modern electronic device, including communication equipment, industrial control systems, automotive electronics modules, and data processing hardware deployed across commercial and industrial sectors. As electronics manufacturing clusters expand across the region, semiconductor assembly and packaging operations naturally locate near downstream electronics production facilities to reduce logistics costs and shorten supply chain lead times. Oman’s strategic geographic position connecting Asian semiconductor exporters with Middle Eastern electronics markets strengthens the country’s role within the regional semiconductor supply chain ecosystem. Telecommunications infrastructure development across Gulf economies generates particularly strong demand for semiconductor components used in network switching systems, fiber optic communication hardware, satellite communication equipment, and high performance data processing devices supporting digital services infrastructure. These interconnected supply chain developments collectively stimulate semiconductor manufacturing investment and encourage international semiconductor companies to explore collaborative manufacturing opportunities within Oman’s growing advanced technology industrial base.

Government Driven Industrial Diversification Policies:

Oman’s long term economic diversification strategy prioritizes advanced manufacturing sectors capable of generating high value industrial output and technology driven employment opportunities beyond traditional hydrocarbon industries. Semiconductor manufacturing represents a strategically important industry within this diversification framework because semiconductor components form the foundational technology enabling digital economies, telecommunications infrastructure, industrial automation systems, and advanced transportation technologies. Government initiatives encourage foreign semiconductor companies to establish production partnerships within national industrial zones through investment incentives, tax benefits, infrastructure support programs, and simplified regulatory frameworks designed to attract advanced manufacturing investment. Industrial development authorities actively promote electronics manufacturing and semiconductor integration activities within Sohar, Duqm, and other strategic industrial clusters capable of hosting advanced technology manufacturing facilities. Semiconductor manufacturing investments also stimulate technology transfer partnerships that enhance local engineering capabilities and expand the domestic high technology workforce. Collaboration between multinational semiconductor equipment suppliers and regional manufacturing firms further accelerates knowledge transfer and technical skill development necessary for supporting complex semiconductor production processes. Infrastructure investments supporting industrial power supply reliability, advanced logistics connectivity, and digital communication networks also create favorable conditions required for semiconductor manufacturing operations. Through these policy frameworks Oman strengthens its ability to participate in regional semiconductor supply chains while simultaneously supporting national economic diversification goals focused on technology driven industrial development.

Market Challenges

High Capital Intensity of Semiconductor Fabrication Infrastructure:

Semiconductor manufacturing represents one of the most capital intensive industrial sectors globally because advanced chip fabrication facilities require highly specialized cleanroom environments, precision manufacturing equipment, and extremely controlled production conditions capable of maintaining microscopic semiconductor processing tolerances. The construction of modern semiconductor fabrication plants often requires billions of dollars in capital investment along with advanced lithography equipment, chemical deposition systems, plasma etching tools, and complex testing infrastructure necessary for producing integrated circuits and semiconductor devices. For emerging semiconductor manufacturing markets such as Oman, securing sufficient investment to establish full scale wafer fabrication facilities remains a significant barrier limiting rapid industry expansion. Semiconductor manufacturing equipment also requires continuous technological upgrades as chip architectures evolve toward smaller nanometer scale manufacturing nodes capable of delivering improved computing performance and energy efficiency. Maintaining competitive semiconductor fabrication capabilities therefore demands constant reinvestment in manufacturing technology and process optimization infrastructure. Smaller semiconductor markets typically focus on downstream manufacturing activities such as packaging, testing, and electronics integration because these operations require comparatively lower capital expenditure while still supporting semiconductor supply chains. The global semiconductor industry also remains dominated by established manufacturing leaders located in Asia, North America, and parts of Europe where large scale semiconductor fabrication ecosystems have developed over several decades. These structural economic factors create substantial barriers for new semiconductor manufacturing hubs attempting to compete directly with mature semiconductor production regions.

Limited Domestic Semiconductor Supply Chain Ecosystem:

Semiconductor manufacturing relies on highly complex supply chain networks involving specialized materials suppliers, semiconductor equipment manufacturers, chemical processing companies, precision engineering providers, and highly skilled semiconductor engineers capable of managing advanced chip production environments. Oman’s domestic industrial ecosystem currently contains limited local suppliers capable of producing semiconductor grade materials such as high purity silicon wafers, advanced photoresist chemicals, semiconductor gases, and precision manufacturing components required for semiconductor fabrication processes. Semiconductor manufacturing facilities therefore depend heavily on imported equipment, materials, and technical expertise supplied by international technology partners. Logistics complexity associated with importing sensitive semiconductor manufacturing materials can increase operational costs and extend supply chain lead times compared with established semiconductor manufacturing regions possessing dense supplier ecosystems. Additionally, semiconductor manufacturing requires highly specialized technical expertise across semiconductor engineering disciplines including microelectronics design, materials science, semiconductor process engineering, and advanced manufacturing automation. Building a sufficiently skilled semiconductor workforce requires long term education investment, international training partnerships, and technology transfer programs capable of developing domestic semiconductor engineering expertise. Until such supporting industrial and human capital ecosystems mature, semiconductor manufacturing expansion within Oman may progress gradually as companies prioritize collaborative partnerships with established global semiconductor supply chain participants.

Opportunities

Expansion of Semiconductor Packaging and Testing Services:

Semiconductor packaging and testing operations represent one of the most commercially viable entry points for emerging semiconductor manufacturing markets because these activities support the semiconductor value chain without requiring the extreme capital investment associated with advanced wafer fabrication facilities. Packaging operations involve bonding semiconductor chips onto substrates, protecting delicate circuitry through specialized encapsulation processes, and preparing semiconductor devices for integration within electronic systems used across multiple industries. Oman’s logistics infrastructure and export oriented industrial zones create favorable conditions for hosting semiconductor packaging facilities capable of serving electronics manufacturers throughout the Middle East, Africa, and parts of Europe. Telecommunications hardware manufacturers, consumer electronics assemblers, and industrial equipment producers operating within the Gulf region require consistent semiconductor packaging services supporting final device assembly. Semiconductor packaging facilities also integrate efficiently with existing electronics assembly operations already operating within Oman’s industrial clusters. Establishing specialized semiconductor testing laboratories further enhances the country’s semiconductor manufacturing ecosystem by ensuring semiconductor devices meet strict performance, reliability, and quality standards before being integrated into electronic products. International semiconductor companies often outsource packaging and testing services to geographically distributed facilities capable of serving multiple electronics manufacturing hubs simultaneously. These operational dynamics create a strong opportunity for Oman to position itself as a regional semiconductor packaging and testing hub within the broader global semiconductor supply chain.

Development of Power Semiconductor Manufacturing for Energy Systems:

Power semiconductors play a critical role in managing electrical energy within modern industrial systems including renewable energy installations, electric vehicles, smart power grids, and industrial automation equipment requiring efficient electrical power conversion technologies. Global demand for power semiconductor devices continues increasing as energy systems transition toward renewable power generation technologies and electrified transportation infrastructure. Oman’s energy sector transformation initiatives involving renewable energy deployment, grid modernization programs, and industrial electrification projects create strong domestic demand for power semiconductor devices supporting power control and energy management systems. Establishing specialized manufacturing capabilities focused on power semiconductor devices such as insulated gate bipolar transistors, silicon carbide power modules, and advanced voltage regulators could provide a focused semiconductor manufacturing niche aligned with regional energy technology demand. Power semiconductor manufacturing typically requires less advanced lithography technology compared with high performance computing chips, making it more accessible for emerging semiconductor manufacturing markets. Collaborations with global power electronics companies could accelerate technology transfer while enabling local semiconductor manufacturing activities supporting regional energy infrastructure development. By aligning semiconductor manufacturing development with energy sector transformation initiatives, Oman can create a specialized semiconductor manufacturing segment that directly supports national industrial and energy transition priorities.

Future Outlook

The Oman Semiconductor Manufacturing Market is expected to expand steadily as advanced manufacturing initiatives strengthen the country’s technology sector and attract international semiconductor partnerships. Industrial diversification strategies are likely to encourage new semiconductor assembly, packaging, and testing facilities integrated within established industrial zones. Growing demand for telecommunications infrastructure, renewable energy technologies, and industrial automation systems will continue stimulating semiconductor component consumption across regional markets. Technological collaboration with global semiconductor leaders and improved supply chain integration are expected to accelerate Oman’s role within the Middle East semiconductor ecosystem.

Major Players

- Intel Corporation

- Taiwan Semiconductor Manufacturing Company

- Samsung Electronics Semiconductor Division

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- Texas Instruments

- GlobalFoundries

- Micron Technology

- ASE Technology Holding

- Amkor Technology

- Tower Semiconductor

- United Microelectronics Corporation

- Renesas Electronics

- ON Semiconductor

Key Target Audience

- Semiconductor Manufacturing Companies

- Electronics Manufacturing Companies

- Telecommunications Infrastructure Providers

- Industrial Automation Equipment Manufacturers

- Automotive Electronics Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Semiconductor Equipment Manufacturers

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying core market variables influencing semiconductor manufacturing including production capacity, semiconductor technology type, industrial infrastructure availability, and demand patterns across electronics manufacturing sectors. These variables are mapped across national industrial development strategies and semiconductor supply chain dynamics to understand market structure.

Step 2: Market Analysis and Construction

Market construction integrates semiconductor production data, electronics manufacturing trends, industrial development policies, and semiconductor supply chain analysis to estimate market size and segmentation patterns. Supply chain mapping helps identify dominant manufacturing activities including packaging, testing, and semiconductor integration within regional electronics ecosystems.

Step 3: Hypothesis Validation and Expert Consultation

Initial market assumptions are validated through consultation with semiconductor engineers, electronics manufacturing experts, and regional industrial development stakeholders. Industry insights ensure that market segmentation, growth drivers, and supply chain trends reflect realistic semiconductor manufacturing dynamics within emerging industrial economies.

Step 4: Research Synthesis and Final Output

All validated research insights are synthesized into a structured analytical framework covering market size, segmentation, competitive landscape, growth drivers, and strategic opportunities. The final report integrates quantitative data with qualitative industry insights to deliver a comprehensive understanding of the Oman Semiconductor Manufacturing Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of National Electronics Manufacturing Capabilities

Increasing Investment in High Technology Industrial Diversification

Rising Demand for Semiconductor Components in Telecommunications Infrastructure - Market Challenges

High Capital Investment Requirements for Semiconductor Fabrication Facilities

Limited Local Semiconductor Supply Chain Ecosystem

Technological Dependence on International Semiconductor Equipment Providers - Market Opportunities

Strategic Partnerships with Global Semiconductor Foundries

Development of Semiconductor Packaging and Testing Facilities

Growth in Power Electronics Manufacturing for Renewable Energy Systems - Trends

Integration of Advanced Automation in Semiconductor Fabrication

Growing Adoption of AI Driven Semiconductor Process Control

Expansion of Regional Semiconductor Supply Chain Diversification - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Systems

Semiconductor Assembly and Packaging Systems

Testing and Inspection Systems

Photolithography Systems

Etching and Deposition Systems - By Platform Type (In Value%)

Integrated Circuit Manufacturing Platforms

Power Semiconductor Manufacturing Platforms

Analog and Mixed Signal Manufacturing Platforms

Memory Semiconductor Manufacturing Platforms

RF and Communication Chip Manufacturing Platforms - By Fitment Type (In Value%)

Fully Automated Fabrication Facilities

Modular Semiconductor Production Lines

Hybrid Automated Manufacturing Systems

Integrated Smart Fabrication Systems

Retrofit Semiconductor Processing Systems - By EndUser Segment (In Value%)

Consumer Electronics Manufacturers

Telecommunications Equipment Manufacturers

Automotive Electronics Manufacturers

Industrial Electronics Manufacturers

- Market Share Analysis

- CrossComparison Parameters (Technology Node Capability, Fabrication Capacity, Process Automation Level, EndUser Industry Focus, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Intel Corporation

Taiwan Semiconductor Manufacturing Company

Samsung Electronics Semiconductor Division

GlobalFoundries

Micron Technology

Texas Instruments

STMicroelectronics

Infineon Technologies

NXP Semiconductors

ASE Technology HoldingAmkor Technology

Tower Semiconductor

United Microelectronics Corporation

SilTerra Malaysia

Powerchip Semiconductor Manufacturing Corporation

- Telecommunications Infrastructure Providers Increasing Semiconductor Demand

- Automotive Electronics Expansion Supporting Semiconductor Integration

- Industrial Automation Systems Driving Semiconductor Component Consumption

- Defense Electronics Programs Strengthening Domestic Semiconductor Capability

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now