Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines 3D printing in the automotive market is valued at USD ~ million in 2024, witnessing a surge in demand driven by advancements in additive manufacturing technologies. The market is primarily fueled by the need for cost-effective and efficient solutions in automotive part production, prototyping, and tooling. Key drivers include the increasing demand for lightweight and durable automotive components, the adoption of electric vehicles (EVs), and the growing trend of mass customization in vehicle manufacturing. As a result, automotive OEMs and suppliers in the region are increasingly turning to 3D printing technologies to streamline production processes and reduce time-to-market.

Metro Manila and Cavite dominate the 3D printing landscape in the Philippines. Metro Manila is the epicenter of the automotive industry, with a significant concentration of OEMs, tier suppliers, and R&D institutions. This urban cluster is also home to key players in additive manufacturing, providing easy access to both technology and expertise. Cavite, with its established industrial parks and proximity to Metro Manila, is another hub for automotive manufacturing and 3D printing. These regions benefit from favorable infrastructure, government initiatives, and the growing integration of 3D printing in automotive production processes.

Market Segmentation

By Technology

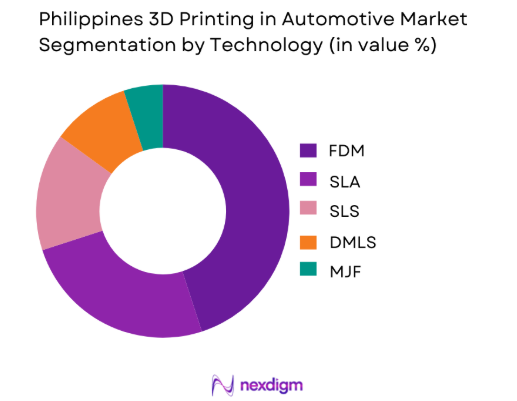

The Philippines 3D printing in automotive market is segmented by technology into FDM, SLA, SLS, DMLS, and MJF. Among these, FDM technology dominates the market due to its widespread adoption for automotive prototyping and tooling. FDM offers the advantage of being cost-effective and versatile, making it an attractive option for local automotive manufacturers who are looking to streamline the development of prototype parts, jigs, and fixtures. The ease of material compatibility and affordability makes FDM technology the leading choice for companies looking to reduce production costs while improving part functionality.

By Material Type

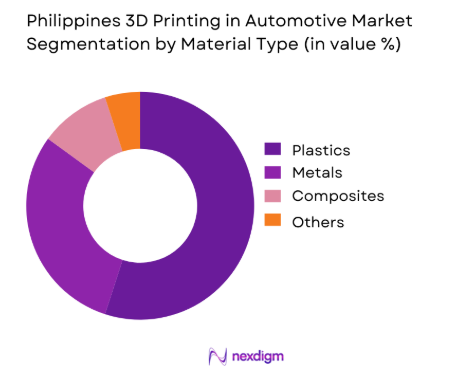

The material segment in the Philippines 3D printing automotive market is dominated by plastics, especially ABS and PLA. Plastics are preferred due to their versatility, ease of use, and cost-effectiveness. Automotive manufacturers, especially in prototyping, rely heavily on plastic materials for creating lightweight parts that meet performance requirements without increasing overall costs. The use of metals and composites is growing, but plastics still dominate due to their accessibility and lower cost compared to high-performance materials like titanium or carbon fiber.

Competitive Landscape

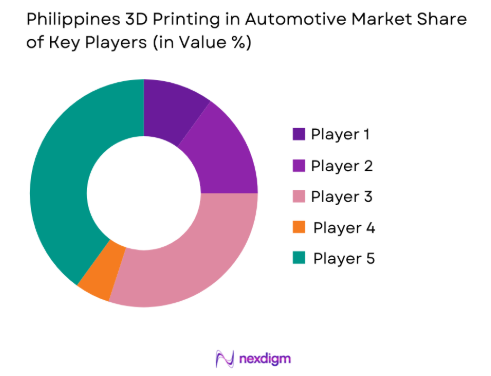

The Philippines 3D printing in automotive market is dominated by a few major players, including Stratasys and global or regional brands like 3D Systems, HP, and Proto Labs. This consolidation highlights the significant influence of these key companies. These players offer a range of solutions, from high-performance 3D printers to post-processing services, establishing strong positions in the market due to their technological innovations and extensive expertise in the automotive sector.

| Company | Establishment Year | Headquarters | Technology Focus | Product Offering | Market Focus | Sales Channels |

| Stratasys | 1989 | USA | ~ | ~ | ~ | ~ |

| 3D Systems | 1986 | USA | ~ | ~ | ~ | ~ |

| HP | 1939 | USA | ~ | ~ | ~ | ~ |

| Proto Labs | 1999 | USA | ~ | ~ | ~ | ~ |

| Cubizone | 2013 | Philippines | ~ | ~ | ~ | ~ |

Philippines 3D Printing in Automotive Market Analysis

Growth Drivers

Rising Demand for Faster Product Development Cycles

As industries, particularly automotive and manufacturing, focus on increasing their competitiveness, there is a growing demand for faster product development cycles. The need to reduce time-to-market is driving the demand for advanced manufacturing technologies, including additive manufacturing, 3D printing, and rapid prototyping. These technologies enable companies to quickly iterate designs, produce prototypes, and test products more efficiently. With the increasing pressure to innovate and meet customer demands in shorter timeframes, companies are adopting faster and more agile product development methods, boosting the need for advanced tooling and fixture production capabilities.

Need for Cost-Effective Tooling and Fixture Production

The growing emphasis on cost reduction across industries is leading to a significant need for more cost-effective tooling and fixture production. Traditional methods of tooling often involve high upfront costs and long production times. With the adoption of advanced manufacturing technologies such as 3D printing and additive manufacturing, companies can produce custom tools and fixtures more affordably and quickly. This ability to streamline production, reduce material waste, and lower overall manufacturing costs provides a competitive advantage, making cost-effective tooling solutions a crucial growth driver in industries like automotive, aerospace, and consumer goods manufacturing.

Challenges

High Capex and Imported Equipment Dependence

One of the key challenges in modern manufacturing is the high capital expenditure (capex) associated with acquiring advanced equipment, such as high-end 3D printers, CNC machines, and specialized tooling machinery. These technologies are often expensive to purchase, maintain, and operate, making it difficult for smaller manufacturers or those with limited budgets to access the latest advancements. Furthermore, many industries remain heavily dependent on imported equipment, which adds additional costs related to shipping, import taxes, and longer lead times. This dependence on foreign equipment can also make companies vulnerable to supply chain disruptions and currency fluctuations.

Limited Materials Availability and Qualification Capability

Another significant challenge is the limited availability of suitable materials and the qualification capability needed for advanced manufacturing processes. For industries like automotive and aerospace, material selection and qualification are critical to ensuring product durability, safety, and performance. However, many advanced manufacturing technologies face limitations in terms of the range of materials that can be used, particularly for high-performance applications. Additionally, qualification processes to ensure materials meet industry standards are often complex, time-consuming, and costly. This can delay production and make it difficult to adopt newer materials or technologies without going through extensive testing and certification.

Opportunities

On-Demand Spare Parts and Digital Inventory Programs

On-demand spare parts and digital inventory programs present significant opportunities for improving operational efficiency in manufacturing. By leveraging digital inventory and on-demand production technologies like 3D printing, manufacturers can create spare parts as needed, reducing the need for large inventories and improving supply chain agility. This approach allows for quicker response times to equipment failures, reducing downtime and improving overall operational efficiency. Additionally, digital inventory systems enable manufacturers to better track part usage, manage stock levels, and ensure the availability of critical components, which can help reduce storage costs and optimize resource management.

Local Service Bureau Expansion for Automotive Accounts

The expansion of local service bureaus for automotive accounts is a valuable opportunity for manufacturers looking to streamline their production processes. Local service bureaus provide on-demand, customized tooling, parts, and prototypes, allowing automotive companies to rapidly scale their production and reduce lead times. These service bureaus can leverage advanced manufacturing technologies such as 3D printing, CNC machining, and injection molding to offer fast, cost-effective solutions tailored to automotive requirements. By expanding local service bureaus, companies can gain more control over their supply chains, reduce transportation costs, and enhance their ability to meet the specific needs of automotive clients, ultimately improving efficiency and competitiveness.

Future Outlook

Over the next few years, the Philippines 3D printing in automotive market is expected to continue growing as adoption increases across OEMs and tier suppliers. With a favorable regulatory environment and the ongoing push toward digital manufacturing and sustainability, 3D printing is poised to become a critical component of automotive production processes. Advances in 3D printing technologies, such as metal printing and material innovations, will further enhance the capabilities of the market, leading to increased efficiency and cost savings for automotive manufacturers.

Major Players

- Stratasys

- 3D Systems

- HP

- Proto Labs

- Cubizone

- EOS GmbH

- Markforged

- Materialise

- Desktop Metal

- Formlabs

- ExOne

- Carbon

- Renishaw

- Arcam AB

- SLM Solutions

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive OEMs

- Tier 1 suppliers

- 3D printing technology providers

- Additive manufacturing service providers

- Automotive aftermarket companies

- Automotive industry associations

Research Methodology

Step 1: Identification of Key Variables

In this phase, we identify and define the critical variables influencing the Philippines 3D printing automotive market, including technology adoption rates, material preferences, and industry-specific challenges.

Step 2: Market Analysis and Construction

This phase involves gathering historical data from secondary sources and synthesizing it with primary data obtained through interviews and surveys. The goal is to construct an accurate market model that reflects the dynamics of the industry.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through consultations with industry experts, including manufacturers, suppliers, and service providers. This provides actionable insights into the market’s evolution and key growth factors.

Step 4: Research Synthesis and Final Output

The final phase includes synthesizing all collected data, conducting a thorough analysis of trends, challenges, and opportunities, and producing a comprehensive report that outlines the key drivers and dynamics of the Philippines 3D printing automotive market.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, automotive additive manufacturing taxonomy, market sizing logic by part value and service spend, printed part and material consumption estimation logic, primary interview program with OEMs Tier 1s and service bureaus, data triangulation and validation approach, assumptions limitations and data gaps)

- Definition and Scope

- Market Genesis and Adoption Maturity in the Philippines Automotive Base

- Automotive Manufacturing Footprint and Tier Supplier Landscape

- Use Case Mapping Across Prototyping Tooling and End Use Parts

- Value Chain Structure Across OEMs Tier Suppliers and Service Bureaus

- Growth Drivers

Rising demand for faster product development cycles

Need for cost effective tooling and fixture production

Growth of localized aftermarket customization

Supply chain resilience focus for low volume parts

Increasing engineering capability in industrial zones - Challenges

High capex and imported equipment dependence

Limited materials availability and qualification capability

Skills gap in design for additive manufacturing

Quality assurance and repeatability constraints

Low scale economics for metal additive production - Opportunities

On demand spare parts and digital inventory programs

Local service bureau expansion for automotive accounts

Light weighting and part consolidation for EV components

Partnerships with universities for AM talent pipelines

Certification and process validation services for Tier suppliers - Trends

Shift from prototyping to production intent applications

Rising use of polymer powder bed fusion for functional parts

Growing adoption of simulation and topology optimization

Increased emphasis on traceability and process control

Expansion of hybrid manufacturing combining CNC and AM - Regulatory & Policy Landscape

SWOT Analysis

Stakeholder & Ecosystem Analysis

Porter’s Five Forces Analysis

Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Printed Parts Output, 2019–2024

- By Material Consumption, 2019–2024

- By In House vs Service Bureau Spend Split, 2019–2024

- By Fleet Type (in Value %)

Passenger vehicle programs

Commercial vehicle programs

Two and three wheeler manufacturing programs

Motorsport and performance builds

Aftermarket customization segment - By Application (in Value %)

Design and rapid prototyping

Jigs fixtures and assembly aids

Tooling and low volume molds

Spare parts and service parts production

End use functional components - By Technology Architecture (in Value %)

FDM and material extrusion systems

SLA and photopolymer resin systems

SLS polymer powder bed fusion systems

Metal powder bed fusion systems

Binder jetting and metal sintering workflows - By Connectivity Type (in Value %)

Standalone printer operations

CAD CAM and PLM integrated workflows

Digital inventory and on demand spare parts platforms

MES integrated shop floor production control

Cloud based print management and remote monitoring - By End-Use Industry (in Value %)

Automotive OEMs and assembly plants

Tier 1 and Tier 2 component suppliers

Aftermarket parts manufacturers and fabricators

Service bureaus and contract manufacturers

Dealership service and maintenance networks - By Region (in Value %)

NCR

CALABARZON

Central Luzon

Visayas

Mindanao

- Positioning driven by throughput capability material breadth and quality systems

- Partnership models between printer OEMs materials suppliers and local integrators

- Cross Comparison Parameters (automotive grade material portfolio, achievable tolerance and repeatability, build volume and throughput, metal capability and post processing readiness, quality control and traceability features, local applications support and training, lead time for parts delivery, total cost per part)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Porter’s Five Forces

- Detailed Profiles of Companies

Stratasys

3D Systems

EOS

HP

GE Additive

Renishaw

Desktop Metal

Markforged

Carbon

Materialise

Proto Labs

Xometry

SLM Solutions

Formlabs

BASF Forward AM

- OEM and Tier supplier sourcing models for AM work

- Prototype and tooling buyer decision criteria

- Service bureau selection and contracting expectations

- Quality documentation and validation requirements

- Cost sensitivity and ROI thresholds by use case

- By Value, 2025–2030

- By Printed Parts Output, 2025–2030

- By Material Consumption, 2025–2030

- By In House vs Service Bureau Spend Split, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now