Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines advanced materials market is expected to see strong growth driven by demand from key industries such as automotive, aerospace, and electronics. The market size, based on a recent historical assessment, is valued at approximately USD ~ billion. The increasing need for high-performance materials in these industries, along with government initiatives supporting infrastructure and manufacturing growth, is propelling this market’s expansion. Moreover, the development of advanced materials like composites, polymers, and nanomaterials is fostering innovation across these sectors.

The dominant countries and cities in the Philippines advanced materials market include Metro Manila, Cebu, and Davao. Metro Manila leads the charge due to its strategic location and the presence of several multinational companies, while Cebu and Davao are emerging as key hubs due to strong local demand. The rapid industrialization in these areas, combined with access to advanced technologies, strengthens their position as major contributors to the market’s development.

Market Segmentation

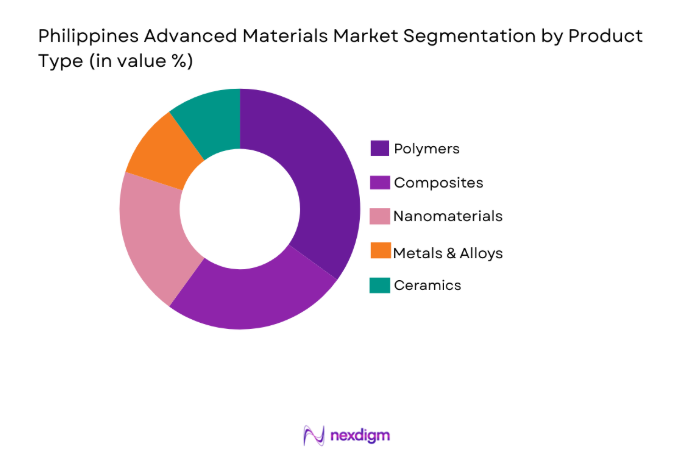

By Product Type

The Philippines advanced materials market is segmented by product type into polymers, composites, nanomaterials, metals & alloys, and ceramics. Recently, polymers have had a dominant market share due to their widespread use in the automotive, electronics, and construction industries. The versatility of polymers, combined with their cost-effectiveness and ease of processing, drives demand in a variety of applications. Additionally, the automotive industry’s increasing adoption of lightweight materials further propels the growth of the polymer sub-segment, making it a key player in the market’s overall performance.

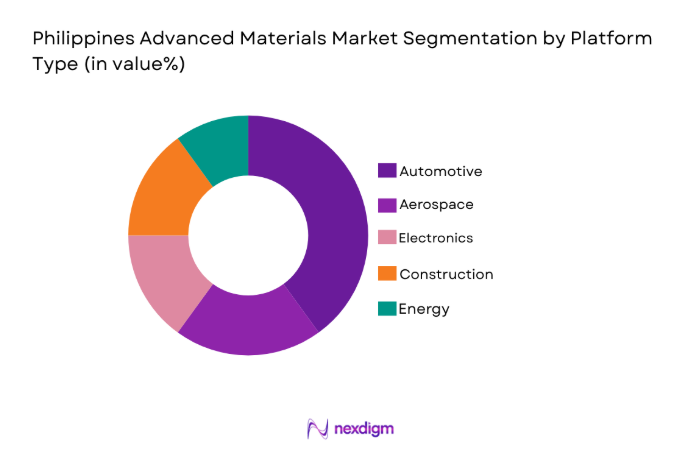

By Platform Type

The market is segmented by platform type into automotive, aerospace, electronics, construction, and energy. The automotive platform is currently dominating the market share. This is largely attributed to the rising demand for lightweight, durable materials used in vehicle manufacturing, which enhances fuel efficiency and reduces emissions. As automakers continue to focus on electric vehicles and sustainable transportation, the use of advanced materials such as composites and polymers is expected to remain a critical component of the automotive industry’s growth trajectory.

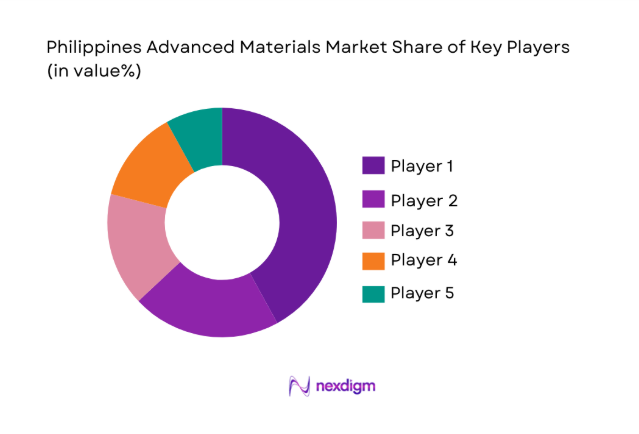

Competitive Landscape

The competitive landscape in the Philippines advanced materials market is characterized by a mix of established global players and local companies that have a strong foothold in the region. Major players influence the market by leveraging technological innovations, expanding production capabilities, and forging strategic alliances. As the market grows, consolidation through mergers and acquisitions is likely, as companies seek to enhance their market position and capacity to meet rising demand across various sectors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| BASF Philippines | 1997 | Manila | ~ | ~ | ~ | ~ | ~ |

| Dow Chemical Co. | 1897 | USA | ~ | ~ | ~ | ~ | ~ |

| Hyundai Motor Co. | 1967 | Seoul | ~ | ~ | ~ | ~ | ~ |

| JFE Steel | 1944 | Tokyo | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Chemical | 1927 | Tokyo | ~ | ~ | ~ | ~ | ~ |

Philippines Advanced Materials Market Analysis

Growth Drivers

Technological Advancements in Material Science

The development of new materials and innovations in production technologies is a key growth driver for the Philippines advanced materials market. As industries such as automotive, electronics, and aerospace demand higher-performance, lighter, and more durable materials, advances in material science are critical to meeting these needs. Innovations such as nanotechnology and the development of new composites offer superior properties, such as higher strength-to-weight ratios and improved thermal resistance, further stimulating demand for advanced materials. The evolution of material science is also fostering breakthroughs in environmental sustainability, such as the development of biodegradable and recyclable materials. This drive for continuous material innovation is likely to contribute to the market’s expansion, fostering collaborations and partnerships with technology providers, research institutions, and universities to further push the boundaries of material science. Additionally, industries focusing on energy efficiency and sustainability are continuously looking for better-performing materials, which is further accelerating the demand for advanced materials, creating new market opportunities.

Government Support for Infrastructure Development

The Philippine government’s focus on infrastructure growth and manufacturing modernization is a major driver of the advanced materials market. Government initiatives such as the “Build, Build, Build” program have led to significant investments in infrastructure development across the nation, particularly in urbanization and transportation networks. These projects require advanced materials for construction, including polymers, composites, and high-strength alloys, fueling demand in this sector. Government initiatives to modernize the manufacturing sector also focus on advanced technologies and materials to boost the country’s competitiveness globally. The construction and real estate sectors are expected to continue their upward trajectory with the development of new infrastructure, residential, and commercial projects, driving the consumption of advanced materials. As government investments continue to grow, this will create a favorable environment for advanced materials producers, driving the market’s expansion in both residential and commercial projects. Moreover, the implementation of sustainable construction practices backed by government policies is likely to boost the demand for eco-friendly advanced materials.

Market Challenges

High Cost of Production

One of the significant challenges faced by the Philippines advanced materials market is the high cost of production. Advanced materials such as composites, nanomaterials, and high-performance alloys often involve complex manufacturing processes, which can be costly. For example, composite materials require sophisticated equipment for molding and curing, which increases the capital investment and operational costs for manufacturers. This factor may limit their widespread adoption, particularly in cost-sensitive sectors like construction and small-to-medium-sized manufacturing firms. Additionally, fluctuations in raw material prices and supply chain disruptions further complicate cost management for manufacturers. Trade tariffs, import duties, and logistics expenses for sourcing specialized materials from international markets add to the overall cost burden. Companies must invest in advanced manufacturing techniques, automation, and lean production methods to reduce costs and improve competitiveness in a highly price-sensitive market. Companies must also focus on improving efficiency through the adoption of digital technologies, such as AI-driven manufacturing, to optimize their production processes.

Limited Local R&D Investment

Another challenge in the Philippines advanced materials market is the relatively limited local investment in research and development (R&D). While global companies continue to push the boundaries of innovation, local players often lack the resources and infrastructure to undertake significant R&D efforts. This disparity hinders the development of new materials and processes, potentially slowing down the market’s growth. The limited availability of skilled scientists, engineers, and researchers in the country further exacerbates this challenge. Furthermore, the Philippines’ reliance on imported advanced materials means that domestic manufacturers may not have enough control over material quality and performance. To overcome this challenge, companies in the Philippines must collaborate with international research organizations and invest in building a stronger local R&D infrastructure to develop competitive products and solutions. By forging partnerships with universities and research institutions, firms can promote the local innovation ecosystem and reduce dependency on foreign materials. Increased R&D investment will also help local players address the specific needs of the Philippines’ industries and tailor advanced materials accordingly.

Opportunities

Rising Demand for Lightweight Materials in Automotive

The increasing demand for lightweight materials in the automotive industry presents significant opportunities for the advanced materials market in the Philippines. As the automotive sector shifts towards electric vehicles (EVs) and energy-efficient models, there is a growing need for advanced materials that can reduce vehicle weight, thereby improving fuel efficiency, vehicle performance, and reducing emissions. Materials such as composites, polymers, and lightweight alloys are being increasingly used in vehicle manufacturing, particularly in electric cars, to enhance performance and optimize energy consumption. Furthermore, the need for lightweight materials is driven by the global trend towards sustainable automotive solutions, including the transition to electric and hybrid vehicles. As a result, the Philippines has a unique opportunity to leverage its emerging manufacturing capabilities to become a key supplier of lightweight materials, helping automotive companies meet their sustainability goals. Manufacturers in the Philippines have the opportunity to capitalize on this trend by developing and supplying these advanced materials to the growing automotive sector. By embracing innovation, manufacturers can also tap into the global supply chain for EV production, creating long-term market growth opportunities.

Expansion of Renewable Energy Infrastructure

The Philippines’ growing investment in renewable energy infrastructure is another key opportunity for the advanced materials market. As the country seeks to increase its share of renewable energy sources, materials like advanced composites, metals, and ceramics This will be critical in manufacturing wind turbines, solar panels, and energy storage systems. The government’s push towards renewable energy, especially solar and wind energy projects, offers ample opportunities for the local advanced materials industry. Moreover, energy storage solutions that rely on advanced materials such as lithium-ion batteries are in high demand due to the intermittent nature of renewable energy sources. With government incentives and increasing demand for sustainable energy solutions, there is a significant opportunity for advanced material producers to contribute to the development of the renewable energy sector. The shift towards cleaner and greener energy technologies is expected to continue gaining momentum, providing a steady and long-term demand for advanced materials in the energy sector. This growth will not only benefit local manufacturers but will also help position the Philippines as a key player in the global renewable energy market.

Future Outlook

The Philippines advanced materials market is poised for steady growth over the next five years, driven by technological advancements, increased demand from key industries, and government support for infrastructure development. The market will benefit from emerging trends in sustainability and innovation, such as the growing adoption of lightweight materials in automotive and aerospace sectors. Furthermore, the expanding renewable energy market will provide new opportunities for material producers. The evolution of the market will depend on how well companies can innovate, optimize production costs, and cater to the growing demand for high-performance materials across various sectors.

Major Players

- BASF Philippines

- Dow Chemical Co.

- Hyundai Motor Co.

- JFE Steel

- Mitsubishi Chemical

- 3M Philippines

- Sumitomo Chemical

- PPG Industries

- Eastman Chemical Company

- Aboitiz Equity Ventures

- ICI Philippines

- Lotte Chemical

- Nippon Steel & Sumitomo Metal

- LG Chem

- Arkema

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive manufacturers

- Aerospace manufacturers

- Electronics manufacturers

- Energy companies

- Construction companies

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the key market variables, such as industry growth drivers, market trends, and competitive dynamics.

Step 2: Market Analysis and Construction

Data is gathered from various sources, including industry reports, market surveys, and financial data, to analyze the current market size and future growth potential.

Step 3: Hypothesis Validation and Expert Consultation

Experts and industry leaders are consulted to validate hypotheses about market trends, technological advancements, and regulatory impacts.

Step 4: Research Synthesis and Final Output

The research is synthesized into a comprehensive report, highlighting key findings, growth drivers, challenges, and future opportunities in the market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Technological Advancements in Material Science

Growing Demand from Automotive and Electronics Sectors

Government Support for Infrastructure Development - Market Challenges

High Manufacturing Costs of Advanced Materials

Limited Research and Development Funding

Lack of Skilled Labor in Emerging Technologies - Market Opportunities

Rising Demand for Lightweight Materials in Automotive

Increasing Use of Nanotechnology in Manufacturing

Growth in Renewable Energy Applications - Trends

Adoption of 3D Printing in Material Manufacturing

Shift Towards Sustainable and Eco-friendly Materials - Government Regulations

Environmental Regulations on Manufacturing Processes

Safety Standards for Advanced Materials in Construction

Import and Export Regulations on Material Technologies - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Advanced Polymers

Composites

Nanomaterials

Metals & Alloys

Ceramics - By Platform Type (In Value%)

Automotive

Aerospace

Electronics

Construction

Energy - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Modular Solutions

Integrated Solutions - By End User Segment (In Value%)

Manufacturing Industry

Electronics & Semiconductors

Automotive Industry

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology, Market Share)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BASF Philippines

Dow Chemical Company

Hyundai Engineering & Construction Co.

JFE Steel Corporation

Mitsubishi Chemical Holdings Corporation

Acer Inc.

Samsung Electronics Co.

Taiwan Semiconductor Manufacturing Company

Vanguard Steel Corporation

Suntory Beverage & Food Limited

Eastman Chemical Company

BASF Group

Saint-Gobain Philippines

Sumitomo Electric Industries

LG Chem

- Rising Demand for High-performance Materials in Manufacturing

- Shift Towards Sustainable Materials in the Electronics Sector

- Increased Investment in Aerospace and Automotive Industries

- Growing Adoption of Advanced Materials in the Renewable Energy Sector

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now