Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Agrochemical market is a key sector in the agricultural landscape, driven by increasing agricultural production demands and the growing need for efficient pest management solutions. The market size for agrochemicals in the Philippines is expected to reach USD ~ billion by 2024, as farmers seek advanced solutions to enhance crop yield and protect against pests. The adoption of modern technologies and the increasing trend of commercial agriculture are major drivers of this market’s expansion.

The Philippines remains one of the leading agricultural markets in Southeast Asia, with key players focusing their efforts on the vast agricultural lands. The major regions driving growth are Luzon and Mindanao, where rice, corn, and sugarcane are the primary crops. These areas benefit from favorable climatic conditions and government support for agricultural initiatives, making them key players in the agrochemical industry. The continued urbanization of agricultural hubs and infrastructure improvements further contribute to the market’s dominance.

Market Segmentation

By Product Type:

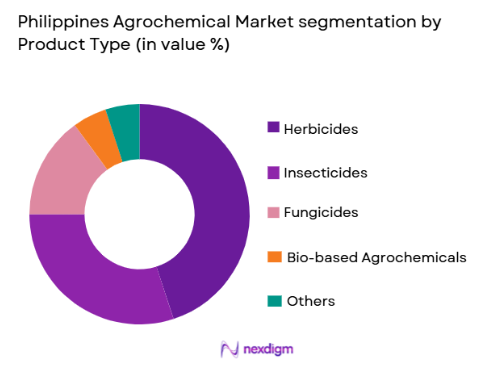

The Philippines Agrochemical market is segmented by product type into herbicides, insecticides, fungicides, bio-based agrochemicals, and others. Recently, herbicides have a dominant market share due to factors such as demand patterns, brand presence, and consumer preference. Herbicides are widely used in the Philippines due to their effectiveness in controlling weeds, which are a significant problem in rice, corn, and sugarcane cultivation. Farmers are increasingly adopting herbicide-based solutions to enhance crop production and improve efficiency in field management, particularly in large-scale operations. This shift is supported by the government’s initiatives to promote high-yield farming.

By Application Area:

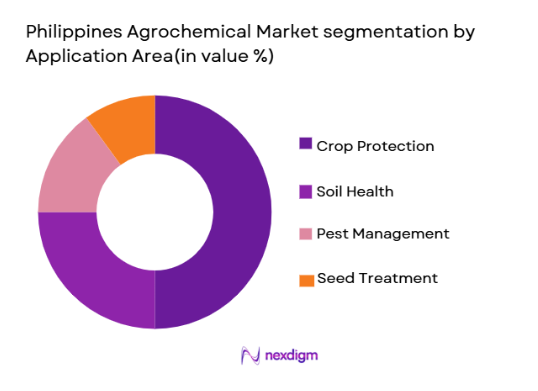

The market is further segmented into crop protection, soil health, pest management, and seed treatment solutions. Crop protection has emerged as the leading sub-segment due to growing concerns about pest attacks, particularly during the wet season. With the rise in commercial agriculture, large-scale farms are investing heavily in crop protection technologies. This dominance can be attributed to the effectiveness of crop protection in safeguarding yields and its critical role in ensuring food security across the country. This trend is also driven by the need for farmers to adopt advanced agricultural technologies to stay competitive.

Competitive Landscape

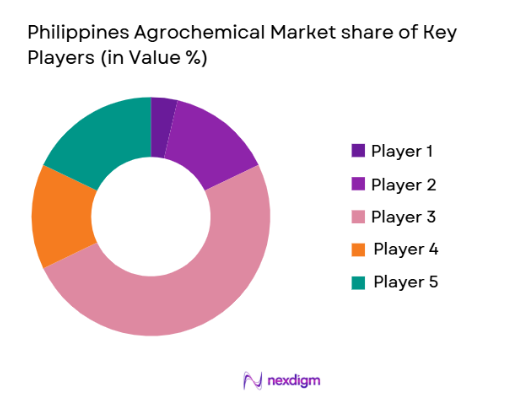

The Philippines Agrochemical market is competitive, with both global and local players contributing to the sector’s growth. The market has seen significant consolidation, with multinational companies acquiring regional players to enhance market reach and strengthen their product offerings. Major players are increasingly focusing on innovation and sustainability in product development. The agrochemical sector continues to see growth in demand driven by increased agricultural activities, government support for food security, and the adoption of modern farming techniques.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Parameter |

| BASF | 1865 | Germany | ~ | ~ | ~ | ~ | ~ |

| Syngenta | 2000 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Corteva Agriscience | 2019 | USA | ~ | ~ | ~ | ~ | ~ |

| Bayer CropScience | 1863 | Germany | ~ | ~ | ~ | ~ | ~ |

| UPL Ltd. | 1980 | India | ~ | ~ | ~ | ~ | ~ |

Philippines Agrochemical Market Analysis

Growth Drivers

Government Support for Agricultural Development:

The Philippine government has been focusing heavily on improving agricultural productivity and ensuring food security. This support is driving demand for agrochemicals, as farmers require effective solutions to maintain and improve crop yields. The government’s initiatives, including subsidies for agricultural inputs and support for modern farming technologies, are expected to continue fueling growth in the agrochemical sector. In addition, favorable trade agreements and export initiatives promote the use of agrochemicals to meet international quality standards. This supportive environment is expected to increase the adoption of advanced agrochemical products, particularly among large-scale farmers.

Increase in Commercial Agriculture and Crop Specialization:

The shift towards commercial agriculture, particularly in regions such as Luzon and Mindanao, is driving the demand for agrochemical products. As farmers move towards larger-scale operations to meet growing domestic and international food demand, the need for efficient crop protection solutions becomes critical. Specialized farming of high-value crops like fruits, vegetables, and sugarcane has increased the demand for tailored agrochemical products. These products are designed to meet the unique requirements of specific crops, contributing to the overall growth of the agrochemical market. As the demand for high-quality, pest-free crops rises, the market for insecticides, herbicides, and fungicides continues to expand.

Market Challenges

Environmental Concerns and Regulation:

Environmental sustainability remains a major challenge for the agrochemical industry in the Philippines. The environmental impact of chemical-based agrochemicals has raised concerns among stakeholders, especially with regard to water contamination and soil degradation. Government regulations and public awareness on the adverse effects of synthetic chemicals are prompting the agrochemical industry to shift toward more eco-friendly and sustainable solutions. However, the pace at which new sustainable agrochemicals can be developed and adopted is slow due to the complexities of product development, regulatory approval processes, and market acceptance.

Dependence on Imported Raw Materials:

The Philippines’ agrochemical market is heavily reliant on the importation of raw materials for agrochemical manufacturing. This dependence on imported chemicals creates challenges related to supply chain disruptions, fluctuating prices, and reliance on foreign suppliers. These factors can result in higher production costs for local agrochemical manufacturers, which can ultimately be passed on to farmers. The volatility in the cost of raw materials further exacerbates challenges for the industry, particularly in periods of economic instability or trade disruptions. Overcoming this reliance on imports will be crucial for ensuring long-term stability in the sector.

Opportunities

Growth of Organic and Bio-Based Agrochemicals:

The growing consumer preference for organic and sustainably produced food presents significant opportunities for the agrochemical market. Bio-based agrochemicals, including bio-pesticides and bio-fertilizers, are gaining popularity due to their environmental benefits and reduced impact on human health. Farmers in the Philippines are increasingly adopting these products to cater to the demand for organic produce. The market for organic and bio-based agrochemicals is expected to grow as awareness about sustainable farming practices increases. This trend presents a lucrative opportunity for agrochemical manufacturers to innovate and develop new bio-based solutions.

Technological Advancements in Precision Agriculture:

Precision agriculture is revolutionizing the way agrochemicals are applied, leading to more efficient and targeted use of resources. The adoption of digital farming tools, such as GPS-based systems and drones, is increasing the precision of agrochemical applications, reducing waste, and improving crop yields. This shift towards precision agriculture presents an opportunity for agrochemical companies to develop products that are compatible with digital farming technologies. Furthermore, precision application reduces environmental impacts, making it a highly attractive option for farmers seeking sustainable farming practices. The integration of technology into farming will continue to drive demand for more efficient and effective agrochemical products.

Future Outlook

The Philippines Agrochemical market is expected to grow steadily over the next five years, driven by technological advancements in crop protection and increasing agricultural demand. The market will witness greater adoption of bio-based and organic agrochemicals as consumer preferences shift towards sustainable farming practices. Enhanced government support for agriculture and the expansion of commercial farming will further bolster growth in the agrochemical sector. Technological developments in precision farming will continue to improve efficiency and reduce the environmental footprint of agrochemicals, positioning the market for sustained growth in the coming years.

Major Players

- BASF

- Syngenta

- Corteva Agriscience

- Bayer CropScience

- UPL Ltd.

- Dow AgroSciences

- Monsanto Philippines

- FMC Corporation

- ADAMA Philippines

- BioBest Philippines

- Nufarm Philippines

- Iscotec

- K+S AG

- AkzoNobel Philippines

- Sumitomo Chemical

Key Target Audience

- Investors and venture capitalist firms

- Government and regulatory bodies

- Large-scale agricultural firms

- Agrochemical distributors

- Food and agriculture manufacturers

- Agricultural cooperatives

- Exporters of agricultural products

- Commercial farming enterprises

Research Methodology

Step 1: Identification of Key Variables

The first step in the research methodology involves identifying key variables influencing the market, including regulatory impacts, technological advancements, and consumer trends.

Step 2: Market Analysis and Construction

Market analysis involves the collection of quantitative and qualitative data, which is then used to construct the market model and assess trends over time.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultation and hypothesis validation are critical steps to ensure the data is accurate and aligned with real-world market dynamics, validated by industry professionals.

Step 4: Research Synthesis and Final Output

In the final step, all collected data and insights are synthesized to produce a comprehensive market report that outlines current trends, future outlook, and key players.

- Executive Summary

- Research Methodology(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for food security

Increase in pest outbreaks

Government subsidies for agriculture

Technological advancements in agrochemicals

Expanding agricultural land under cultivation - Market Challenges

Environmental impact of chemical agrochemicals

Regulatory hurdles in chemical usage

High dependency on imported raw materials

Limited awareness of alternative agrochemicals

Inefficient distribution networks - Market Opportunities

Rising demand for organic and bio-based agrochemicals

Growth in precision farming

Adoption of digital tools for farm management - Trends

Increased adoption of integrated pest management

Shift towards sustainable agrochemicals

Focus on water-saving agrochemical technologies

Rising demand for precision farming solutions

Expansion of agrochemical exports - Government Regulations & Defense Policy

Pesticide regulation enforcement

Environmental sustainability laws

Export compliance for agrochemicals - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Herbicides

Insecticides

Fungicides

Bio-based Agrochemicals

Others - By Platform Type (In Value%)

Crop Protection Platforms

Soil Health Platforms

Water Management Systems

Pest Management Systems

Seed Treatment Platforms - By Fitment Type (In Value%)

Spray Solutions

Soil Treatment Solutions

Integrated Pest Management

Seed Coating Solutions

In-furrow Solutions - By EndUser Segment (In Value%)

Farmers

Agrochemical Distributors

Agro-industries

Government and Regulatory Bodies

Agricultural Research Institutions - By Procurement Channel (In Value%)

Direct Procurement

Retail Sales

Online Platforms

Third-party Distributors

Wholesale Procurement - By Material / Technology (in Value%)

Chemical-based Agrochemicals

Biological Agrochemicals

Nano-enabled Agrochemicals

Organic Agrochemicals

Hybrid Agrochemicals

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Market Value, Technology Adoption, Regulatory Compliance, Distribution Channels, R&D Investment, Pricing Strategies, Customer Reach, Brand Strength, Customer Service, Market Share)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

BASF Philippines

Syngenta Philippines

Corteva Agriscience

Bayer CropScience

Dow AgroSciences

Sumitomo Chemical

Monsanto Philippines

UPL Ltd.

FMC Corporation

ADAMA Philippines

BioBest Philippines

Nufarm Philippines

Iscotec

K+S AG

AkzoNobel Philippines

- Farmers increasingly adopting agrochemical solutions

- Government’s role in promoting agricultural efficiency

- Agro-industries driving product demand

- Agricultural research institutions pushing for innovation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now