Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Philippines’ AI infrastructure market reached approximately USD ~ million based on a recent historical assessment, driven by hyperscale cloud expansion, telecom AI network investment, and enterprise adoption of accelerated computing for analytics and automation. Global technology vendors increased deployment of GPU servers and AI-ready data center capacity to support digital services, fintech platforms, and business process outsourcing analytics workloads. Government digital transformation initiatives and national AI strategies further stimulated localized AI compute and data infrastructure development.

Metro Manila dominates AI infrastructure deployment due to concentration of hyperscale and colocation data centers, telecom backbone connectivity, and dense enterprise IT demand across finance, retail, and outsourcing sectors. Adjacent provinces including Cavite and Laguna host industrial and technology parks supporting enterprise AI workloads. Cebu and Davao emerge as regional digital hubs with growing data center investments and smart city programs. These regions provide connectivity, power, and enterprise demand essential for AI infrastructure deployment.

Market Segmentation

By Product Type

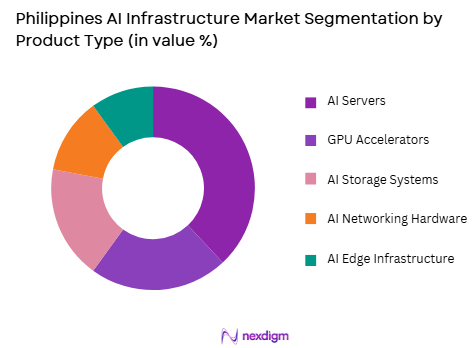

Philippines AI Infrastructure market is segmented by product type into AI servers, GPU accelerators, AI storage systems, AI networking hardware, and AI edge infrastructure. Recently, AI servers has a dominant market share due to factors such as hyperscale cloud deployment, enterprise AI platform adoption, and centralized compute architecture for training and inference workloads. AI workloads in fintech, e-commerce, and outsourcing analytics require high-density compute clusters deployed in centralized data centers. Cloud providers and telecom operators procure integrated AI servers combining GPUs, CPUs, and high-speed interconnects. Enterprises prefer turnkey AI server systems rather than discrete accelerators to simplify deployment. Expansion of hyperscale-ready data centers in Metro Manila further concentrates demand for AI servers. As centralized AI compute remains foundational to national digital infrastructure, AI servers continue to dominate AI infrastructure spending in the Philippines.

By End User

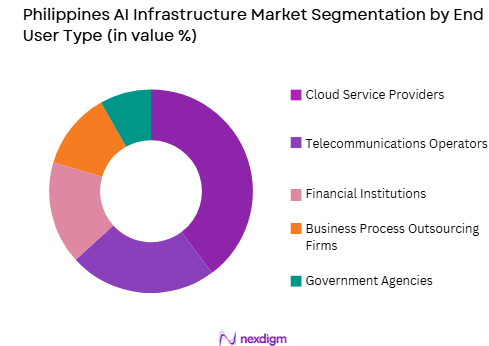

Philippines AI Infrastructure market is segmented by end user into cloud service providers, telecommunications operators, financial institutions, business process outsourcing firms, and government agencies. Recently, cloud service providers has a dominant market share due to factors such as hyperscale infrastructure expansion, AI platform hosting demand, and centralized compute economics. Domestic and international cloud providers deploy large AI clusters to deliver analytics and machine learning services to enterprises lacking in-house infrastructure. The Philippines’ strong digital services and outsourcing economy relies on cloud-hosted AI platforms for customer analytics and automation. Telecom and government sectors increasingly consume AI infrastructure via cloud environments. As enterprises shift toward AI-as-a-service consumption models, cloud providers remain the largest investors in AI compute infrastructure across the Philippines.

Competitive Landscape

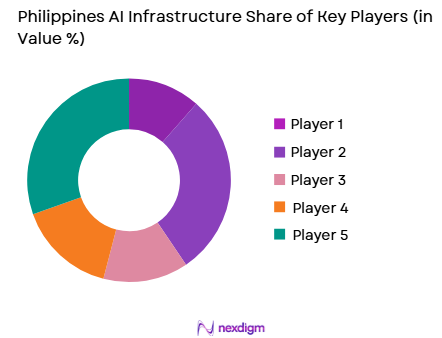

Philippines’ AI infrastructure market is shaped by global AI hardware vendors and hyperscale cloud providers collaborating with domestic telecom and data center operators deploying national compute capacity. International firms dominate supply of GPU servers and AI platforms, while local telecom and cloud companies control infrastructure deployment and enterprise access. Partnerships between hyperscale providers and Philippine data center operators accelerate localized AI cloud availability. Competition centers on compute density, energy efficiency, and integrated AI software ecosystems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI Compute Capacity |

| PLDT | 1928 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Globe Telecom | 1935 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Converge ICT | 2007 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

Philippines AI Infrastructure Market Analysis

Growth Drivers

Hyperscale Cloud Expansion and AI Service Demand

The Philippines’ rapidly expanding digital economy and strong business process outsourcing sector have accelerated hyperscale cloud infrastructure deployment, driving demand for AI-ready data centers and accelerated computing platforms across the country. Cloud providers are investing in GPU clusters and AI servers to deliver analytics, automation, and machine learning services to enterprises in finance, e-commerce, healthcare, and outsourcing industries. Enterprises prefer cloud-hosted AI infrastructure due to scalability and reduced capital investment requirements, concentrating demand within centralized hyperscale facilities. Telecom operators partner with global cloud firms to localize AI infrastructure compliant with data residency requirements. Growth of digital platforms and online services increases AI processing workloads including recommendation engines, fraud detection, and conversational AI. As AI adoption expands across Philippine industries, hyperscale cloud infrastructure investment remains a primary structural driver of national AI infrastructure growth.

Enterprise and BPO AI Adoption for Automation and Analytics

The Philippines’ globally competitive business process outsourcing industry and enterprise services sector are rapidly adopting artificial intelligence to automate customer interactions, analytics, and decision support systems, driving increased deployment of AI compute infrastructure. BPO firms deploy AI models for speech analytics, sentiment analysis, and automation of customer service workflows requiring GPU-accelerated computing. Financial institutions adopt AI for fraud detection, risk modeling, and digital banking platforms. Enterprises across retail and logistics deploy machine learning for demand forecasting and operational optimization. Many organizations procure AI infrastructure through cloud or hybrid deployments to manage cost and scalability. Technology integrators and telecom providers support deployment of enterprise AI environments across Metro Manila and industrial corridors. As AI adoption scales from pilot to production across Philippine enterprises, demand for AI servers and accelerators continues expanding nationwide.

Market Challenges

Dependence on Imported AI Hardware and Limited Domestic Manufacturing

The Philippines’ AI infrastructure market depends heavily on imported GPUs, AI servers, and semiconductor components sourced from global vendors, creating vulnerability to supply constraints, currency fluctuations, and geopolitical trade disruptions. Absence of domestic semiconductor or AI hardware manufacturing limits local value addition and supply chain resilience. Import costs and logistics complexity increase infrastructure procurement expense relative to larger regional markets. Rapid technological evolution in GPU architectures also risks obsolescence for early deployments. These structural dependencies constrain scalability and cost competitiveness of Philippine AI infrastructure development.

Power, Cooling, and Data Center Infrastructure Constraints

AI infrastructure deployment requires high-density compute environments with stable electricity supply and advanced cooling systems, presenting challenges in certain Philippine regions where grid reliability and energy costs vary. Hyperscale AI data centers consume substantial power and require redundant infrastructure to ensure uptime. Tropical climate conditions increase cooling demand and operational costs. Land availability and infrastructure readiness influence data center site selection and expansion timelines. These physical infrastructure constraints affect pace and geographic spread of AI compute deployment across the Philippines.

Opportunities

AI Infrastructure for Digital Services and BPO Transformation

The Philippines’ strong digital services and outsourcing economy presents significant opportunity for AI infrastructure deployment supporting automation, analytics, and intelligent customer engagement platforms. BPO firms increasingly adopt AI-driven conversational agents, predictive analytics, and process automation requiring scalable compute capacity. Cloud providers can deliver industry-specific AI platforms tailored to outsourcing and services sectors. Localization of AI compute improves latency and data governance for Philippine enterprises. As outsourcing transitions toward AI-augmented services, demand for national AI infrastructure will expand substantially.

Development of National AI Cloud and Sovereign Data Infrastructure

Government digital strategies and data sovereignty considerations create opportunity for development of national AI cloud infrastructure hosted within Philippine jurisdiction. Public sector AI initiatives in healthcare, governance, and education require localized compute capacity and secure data environments. Telecom and technology firms can partner with government to deploy sovereign AI infrastructure supporting national digital services. Investment in domestic AI cloud platforms reduces dependence on foreign infrastructure providers. Such initiatives would stimulate sustained AI hardware and data center investment across the Philippines.

Future Outlook

The Philippines’ AI infrastructure market is expected to expand rapidly as hyperscale cloud investments increase and enterprise AI adoption deepens across industries. BPO transformation and digital services growth will drive sustained AI compute demand. Expansion of localized AI data centers will improve national capacity. Partnerships between telecom, cloud, and global hardware vendors will strengthen ecosystem maturity. Government digital and AI strategies will support long-term infrastructure investment and technological capability development.

Major Players

- ePLDT / VITRO

- ST Telemedia Global Data Centres Philippines

- NTT Global Data Centers Philippines

- Digital Edge

- Globe Telecom

- Converge ICT

- Equinix

- PLDT

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Huawei

- Inspur

- Supermicro

- Cisco Systems

Key Target Audience

- Cloud service providers

- Telecommunications operators

- Financial institutions

- Business process outsourcing firms

- Government and regulatory bodies

- Data center operators

- Investments and venture capitalist firms

- AI platform developers

Research Methodology

Step 1: Identification of Key Variables

Key variables including AI server shipments, GPU deployment, hyperscale data center expansion, and enterprise AI adoption were identified. Infrastructure deployment patterns across cloud, telecom, and enterprise sectors were mapped to estimate AI compute demand.

Step 2: Market Analysis and Construction

Bottom-up modeling combined hardware procurement, data center capacity, and cloud infrastructure investment to estimate market size. Segmentation reflected product categories and end-user adoption patterns across Philippine industries.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with telecom operators, cloud providers, and infrastructure vendors validated deployment trends, costs, and adoption drivers. Technical experts confirmed AI infrastructure requirements and regulatory influences shaping the Philippine ecosystem.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights were synthesized into market estimates, segmentation, and competitive analysis. Cross-verification ensured consistency across infrastructure deployment, enterprise adoption, and vendor supply chains.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of hyperscale and colocation data center capacity in Metro Manila

Enterprise AI adoption across finance BPO and digital services sectors

Government digital transformation and AI strategy initiatives - Market Challenges

Limited domestic high performance computing expertise

Dependence on imported AI hardware and GPU supply chains

High power and cooling requirements of AI infrastructure - Market Opportunities

Development of national and sovereign AI compute platforms

Regional AI data center hub potential in Southeast Asia

Growth of AI enabled digital services and analytics platforms - Trends

Deployment of GPU dense AI clusters in urban data centers

Partnerships between telecom operators and cloud providers for AI platforms

Adoption of AI inference infrastructure in enterprise environments - Government regulations

National AI strategy and digital transformation roadmap

Data privacy and cybersecurity compliance requirements

Technology import and high performance computing regulations - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Unitsm, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Compute Servers and GPU Systems

AI Training and HPC Clusters

AI Inference Infrastructure

AI Edge Computing Systems

AI Data Storage and Networking Infrastructure - By Platform Type (In Value%)

Hyperscale AI Data Center Platforms

Enterprise AI Infrastructure Platforms

Telecom AI Network Platforms

Government and Research AI Platforms

Cloud AI Service Platforms - By Fitment Type (In Value%)

On-Premise AI Infrastructure

Colocation AI Deployments

Hyperscale AI Campuses

Integrated AI Appliances

Modular AI Infrastructure Systems - By End User Segment (In Value%)

Cloud and Data Center Providers

Telecommunications Operators

Financial Services Institutions

Government and Public Sector

Digital Enterprises and Platforms - By Procurement Channel (In Value%)

Direct OEM AI Hardware Procurement

Cloud Provider AI Infrastructure Contracts

System Integrator AI Deployments

Telecom Infrastructure Procurement

Government Technology Procurement Programs

- Market Share Analysis

- Cross Comparison Parameters (Compute Density and Scalability, GPU and Accelerator Architecture Support, Data Center Integration and Cooling Capability, AI Software and Framework Ecosystem Compatibility, Regional Infrastructure and Network Presence, Hyperscale Partnership Strength)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

PLDT Enterprise

Globe Telecom

ST Telemedia Global Data Centres Philippines

ePLDT

VITRO Data Center

NVIDIA Philippines

Dell Technologies Philippines

Hewlett Packard Enterprise Philippines

Lenovo Philippines

Huawei Philippines

Cisco Philippines

AWS Philippines

Microsoft Philippines

Google Cloud Philippines

Alibaba Cloud Philippines

- Cloud providers drive large scale AI infrastructure deployment

- Telecom operators integrate AI into network and service platforms

- Financial and digital enterprises adopt AI compute for analytics

- Government agencies invest in national AI computing capacity

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now