Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Autoimmune Disorder Testing market is valued at approximately USD ~ million based on a recent historical assessment. The market is primarily driven by the increasing prevalence of autoimmune diseases in the region, leading to a higher demand for diagnostic tests. Government initiatives focusing on healthcare access, along with technological advancements in diagnostic tools, are also significant contributors to the market’s growth. The rising awareness and improvements in healthcare infrastructure have further stimulated demand for autoimmune disorder testing services.

Dominant cities like Manila and Cebu have emerged as key centers for autoimmune disorder testing, largely due to their advanced healthcare infrastructure and higher population density. These urban areas are supported by well-established healthcare providers and diagnostic centers, making them hubs for medical diagnostics. Furthermore, the adoption of international diagnostic standards and the increasing number of healthcare partnerships contribute to the dominance of these regions in the market. These factors help drive the adoption of advanced autoimmune testing technologies across the country.

Market Segmentation

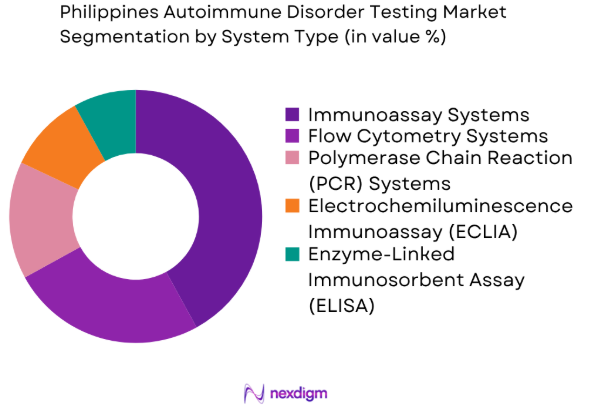

By System Type

The Philippines Autoimmune Disorder Testing market is segmented by system type into immunoassay systems, flow cytometry systems, polymerase chain reaction (PCR) systems, electrochemiluminescence immunoassay (ECLIA) systems, and enzyme-linked immunosorbent assay (ELISA) systems. Immunoassay systems currently dominate the market due to their high accuracy, ease of use, and cost-effectiveness. These systems are widely adopted in both laboratory and point-of-care settings, offering reliable results for autoimmune disease diagnostics. The increasing availability of advanced immunoassay platforms with enhanced capabilities is driving further market penetration, especially in major urban centers.

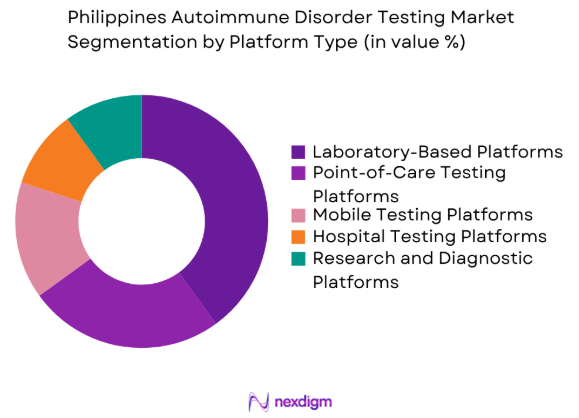

By Platform Type

The Philippines Autoimmune Disorder Testing market is segmented by platform type into laboratory-based platforms, point-of-care testing platforms, mobile testing platforms, hospital testing platforms, and research and diagnostic platforms. Laboratory-based platforms have the dominant market share due to their established presence in diagnostic centers and hospitals. These platforms are preferred for their high throughput, precision, and ability to conduct various tests simultaneously, which is crucial for diagnosing autoimmune disorders effectively. As healthcare providers seek more efficient diagnostic tools, laboratory-based platforms are expected to continue their market leadership.

Competitive Landscape

The competitive landscape of the Philippines Autoimmune Disorder Testing market is marked by significant consolidation, with several large multinational corporations dominating the market. These players focus on technological advancements, expanding distribution networks, and ensuring regulatory compliance to enhance their market presence. The influence of major players, such as Abbott Laboratories and Thermo Fisher Scientific, has driven innovations in testing systems, making accurate and efficient autoimmune disorder testing more accessible to healthcare providers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Market-Specific Parameter |

| Abbott Laboratories | 1888 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

| Thermo Fisher Scientific | 1956 | Waltham, USA | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Basel, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

| Bio-Rad Laboratories | 1952 | Hercules, USA | ~ | ~ | ~ | ~ | ~ |

Philippines Autoimmune Disorder Testing Market Analysis

Growth Drivers

Rising Prevalence of Autoimmune Diseases

The growing incidence of autoimmune diseases, especially among the aging population, is one of the major drivers for the autoimmune disorder testing market. Autoimmune diseases, including rheumatoid arthritis, lupus, and multiple sclerosis, are becoming more prevalent due to lifestyle changes, environmental factors, and genetic predisposition. As awareness increases regarding the early diagnosis of such conditions, there is a growing demand for diagnostic tests. The availability of advanced testing systems that provide accurate and timely results plays a pivotal role in facilitating early detection, which is crucial for managing autoimmune diseases effectively. The increasing awareness among healthcare professionals and patients about the benefits of early diagnosis further strengthens the demand for autoimmune disorder testing.

Technological Advancements in Testing Systems

Technological advancements in autoimmune disorder testing systems are significantly driving market growth. The introduction of more accurate, efficient, and user-friendly diagnostic tools has transformed healthcare diagnostics. Technologies such as electrochemiluminescence immunoassays (ECLIA), PCR-based methods, and next-generation sequencing (NGS) are enhancing diagnostic precision and speed, leading to improved clinical outcomes. Additionally, the integration of artificial intelligence and machine learning in diagnostic platforms is expected to further enhance accuracy and operational efficiency in laboratories. These innovations enable healthcare providers to offer quicker and more accurate diagnoses, ensuring timely treatment for autoimmune disorders. With these technological advancements, the testing process has become more streamlined, improving both the patient experience and the effectiveness of autoimmune disorder management.

Market Challenges

Regulatory Hurdles and Testing Standards

The regulatory challenges in the Philippines present a significant barrier to the growth of the autoimmune disorder testing market. Strict testing standards and approval processes imposed by government agencies such as the Philippine Food and Drug Administration (FDA) make it difficult for new products to enter the market. These regulations ensure that only high-quality, accurate, and reliable testing systems are approved for clinical use, but they also slow down the speed at which innovations can be introduced. As a result, manufacturers face long waiting periods for approvals, which can hinder the adoption of the latest technologies and testing methods, impacting the overall growth of the market.

High Cost of Diagnostic Systems and Equipment

The high cost of diagnostic equipment remains a major challenge for the autoimmune disorder testing market in the Philippines. Advanced diagnostic systems, especially those based on molecular diagnostics and immunoassay technologies, require significant upfront investments. These high costs limit the adoption of such technologies, especially in smaller healthcare facilities and rural areas with lower healthcare budgets. The need for specialized technicians and regular maintenance further increases the operational costs, making it difficult for many diagnostic centers to afford the latest testing systems. Consequently, the market is constrained by the financial limitations of smaller institutions, despite the increasing demand for advanced autoimmune testing.

Opportunities

Expansion of Point-of-Care Testing Solutions

Point-of-care (POC) testing presents a significant growth opportunity for the autoimmune disorder testing market in the Philippines. The demand for faster and more accessible testing solutions is driving the growth of POC testing platforms, especially in remote and rural areas where access to traditional laboratories is limited. These solutions offer the advantage of providing immediate results at the patient’s location, improving patient outcomes and reducing the need for hospital visits. With the government’s focus on expanding healthcare infrastructure and increasing the availability of diagnostic services in underserved areas, there is a growing opportunity for manufacturers to introduce affordable and portable POC testing solutions tailored to autoimmune diseases. This shift toward decentralizing diagnostic testing could significantly drive market growth.

Collaborations with Biotech and Pharma Companies

Collaborations between autoimmune disorder testing companies and biotech or pharmaceutical firms present another key opportunity for growth. These partnerships can facilitate the development of more targeted and personalized diagnostic tests, which are critical for managing autoimmune diseases. For example, advances in biomarker discovery and genetic testing can lead to the development of precision medicine that offers better treatment outcomes. By working with pharmaceutical companies, diagnostic firms can improve the accuracy of their tests, while also benefiting from the growing trend of personalized healthcare. This collaboration will likely drive innovation in autoimmune disorder testing, creating new market opportunities in the coming years.

Future Outlook

The Philippines Autoimmune Disorder Testing market is expected to witness substantial growth over the next five years. With the increasing incidence of autoimmune diseases and the growing demand for early-stage diagnosis, the market is poised to expand. Technological advancements, such as the integration of AI and machine learning in diagnostic platforms, will drive the development of more efficient and accurate testing solutions. Furthermore, the government’s investment in healthcare infrastructure and initiatives to improve healthcare access in underserved areas will contribute to the market’s growth. The expansion of point-of-care testing solutions and collaborations with biotech firms will also fuel innovation and create new opportunities for market participants.

Major Players

- Abbott Laboratories

- ThermoFisher Scientific

- Roche Diagnostics

- Siemens Healthineers

- Bio-Rad Laboratories

- Danaher Corporation

- PerkinElmer

- Medtronic

- Astellas Pharma

- Johnson & Johnson

- BD Biosciences

- Biomerieux

- Quidel Corporation

- LabCorp

- Eurofins Scientific

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers and diagnosticcenters

- Diagnostic equipment manufacturers

- Research and development institutions

- Biotech and pharmaceutical companies

- Healthcare distributors and suppliers

- Healthcare policymakers

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the key variables that influence the autoimmune disorder testing market, such as technology advancements, regulatory factors, and market trends.

Step 2: Market Analysis and Construction

Market trends are analyzed by examining current market conditions, historical data, and emerging opportunities. The market size, demand patterns, and key drivers are examined to estimate future growth.

Step 3: Hypothesis Validation and Expert Consultation

Expert opinions and consultations are sought to validate hypotheses and projections, ensuring that market forecasts are accurate and reflect current trends.

Step 4: Research Synthesis and Final Output

The data collected from various sources are synthesized to create a comprehensive report that includes all relevant market factors, growth drivers, challenges, and opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Autoimmune Disease Incidence

Advancements in Testing Technologies

Rising Healthcare Expenditure and Awareness - Market Challenges

Regulatory Challenges and Testing Standards

High Cost of Advanced Testing Equipment

Limited Access to Remote Areas for Testing - Market Opportunities

Expansion of Point-of-Care Testing Solutions

Rising Demand for Early-Stage Diagnosis

Collaborations with Biotech and Pharma Companies - Trends

Increased Adoption of Digital Health Solutions

Growth in Personalized Medicine for Autoimmune Disorders

Integration of AI and Machine Learning in Diagnostic Tools - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Immunoassay Systems

Flow Cytometry Systems

Polymerase Chain Reaction (PCR) Systems

Electrochemiluminescence Immunoassay (ECLIA) Systems

Enzyme-Linked Immunosorbent Assay (ELISA) Systems - By Platform Type (In Value%)

Laboratory-Based Platforms

Point-of-Care Testing Platforms

Mobile Testing Platforms

Hospital Testing Platforms

Research and Diagnostic Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By End User Segment (In Value%)

Hospitals

Diagnostic Laboratories

Research Institutions

Clinics

Homecare Settings - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Market Growth Drivers, Regulatory Compliance, Technological Advancements, Testing Accuracy, Cost Efficiency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Abbott Laboratories

Siemens Healthineers

Thermo Fisher Scientific

Roche Diagnostics

Johnson & Johnson

Bio-Rad Laboratories

Danaher Corporation

PerkinElmer

AbbVie

Medtronic

AstraZeneca

Becton Dickinson

Genentech

Abbott Diagnostics

Novartis

- Growth of Diagnostic Centers and Laboratories

- Increase in Health Consciousness Among the Population

- Government Initiatives to Improve Healthcare Access

- Technological Advancements in Testing Methodologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now