Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines automotive cameras market is experiencing strong growth, driven by the increasing demand for advanced driver-assistance systems (ADAS) and heightened vehicle safety standards. Based on a recent historical assessment, the market is valued at approximately USD ~ million, as consumer and regulatory pressures push for enhanced safety features in vehicles. The market’s expansion is further supported by the rising adoption of smart technology in automobiles, with the integration of cameras for safety, parking assistance, and autonomous driving features becoming standard in many new vehicle models. The ongoing trend toward digitalization in automotive technologies is a major driver for this growth.

The Philippines market is primarily led by urban centers like Metro Manila, which have seen rapid vehicle ownership growth and infrastructure improvements. Metro Manila’s dominance is driven by its status as the economic hub of the country, along with the higher concentration of both vehicle manufacturers and consumers seeking advanced automotive technologies. The increasing adoption of electric and autonomous vehicles in major cities further supports the growing demand for automotive cameras, making them integral to the evolving vehicle technology landscape.

Market Segmentation

By Product Type

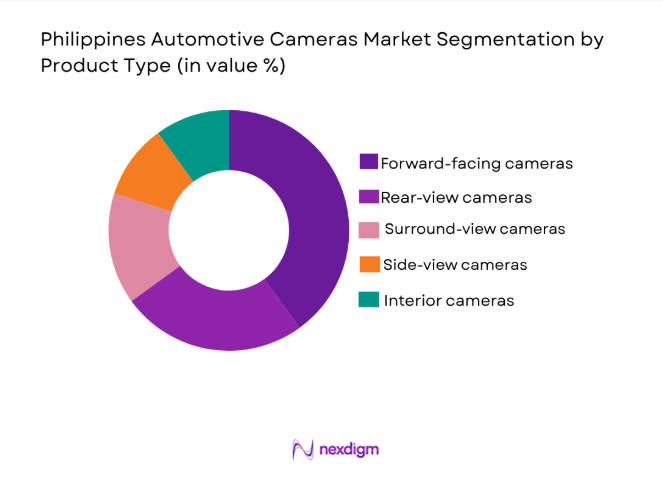

The Philippines automotive cameras market is segmented by product type into forward-facing cameras, rear-view cameras, surround-view cameras, side-view cameras, and interior cameras. Recently, forward-facing cameras have dominated the market share due to their critical role in enhancing driver safety by providing real-time visibility and supporting features such as lane departure warnings and collision detection. The growing demand for these cameras is driven by their widespread integration in modern vehicles, especially with the rise of ADAS technologies. Forward-facing cameras are increasingly favored for their cost-effectiveness and vital role in improving vehicle safety standards.

By Platform Type

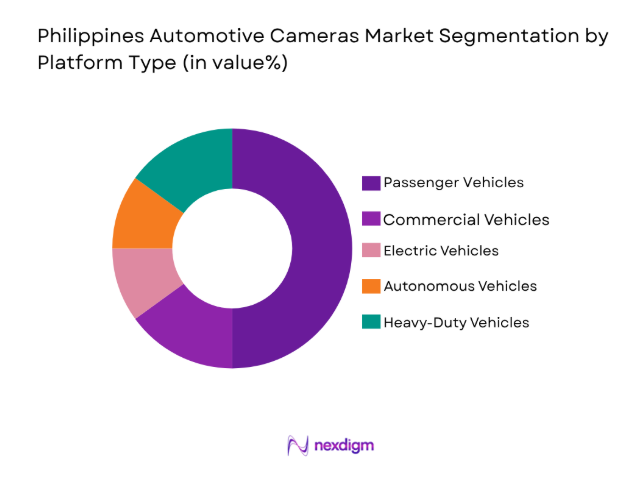

The market is also segmented by platform type into passenger vehicles, commercial vehicles, electric vehicles, autonomous vehicles, and heavy-duty vehicles. Passenger vehicles have recently emerged as the dominant platform type due to the rising demand for vehicle safety features and consumer preference for advanced technology in everyday vehicles. This segment’s growth is largely fueled by the increasing adoption of ADAS features in mainstream consumer vehicles. As more automakers integrate automotive cameras into standard and high-end vehicle models, the segment continues to capture the majority of the market share.

Competitive Landscape

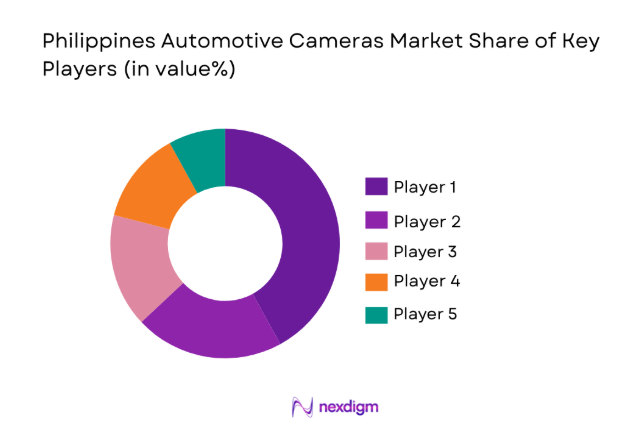

The Philippines automotive cameras market is highly competitive, with several global and local players operating in the space. Consolidation is taking place as major automotive manufacturers partner with technology providers to develop integrated camera solutions. Companies are increasingly focusing on innovation, particularly in the development of cameras that support ADAS technologies and improve vehicle safety. With advancements in camera resolution and AI integration, major players are striving to maintain their market positions and expand their reach within the Philippines automotive sector.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Market-specific Parameter |

| Aptiv | 1994 | Dublin, Ireland | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Hanover, Germany | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Bosch Mobility Solutions | 1886 | Stuttgart, Germany | ~ | ~ | ~ | ~ | ~ |

| Mobileye | 1999 | Jerusalem, Israel | ~ | ~ | ~ | ~ | ~ |

Philippines Automotive Cameras Market Analysis

Growth Drivers

Increase in Vehicle Safety Standards

The adoption of automotive cameras in the Philippines is primarily driven by the rising demand for enhanced vehicle safety systems, which have become increasingly critical for both consumers and policymakers. With stricter government regulations pushing for higher safety standards, the integration of advanced driver-assistance systems (ADAS) into vehicles has become a priority. Automotive cameras play a pivotal role in meeting these regulations, offering essential real-time data that helps prevent accidents, including those caused by human error, such as lane departures, blind spots, and rear-end collisions. Cameras, such as rear-view cameras and forward-facing systems, have been mandated by law for certain types of vehicles to increase safety on the roads. This regulatory push is coupled with growing consumer awareness and demand for vehicle safety, leading automakers to prioritize the inclusion of camera systems in their vehicles. With the increasing number of road accidents in urban areas, particularly in Metro Manila, there is heightened consumer demand for advanced safety features that can mitigate these risks. The market for automotive cameras continues to grow as a result, as both automakers and consumers prioritize the integration of these systems to ensure vehicle safety. As consumers increasingly seek peace of mind while driving, the adoption of automotive cameras is seen as a way to enhance the overall driving experience, making it safer and more convenient. Furthermore, the enforcement of stricter road safety laws, such as those targeting pedestrian protection and road accident prevention, further contributes to the market’s growth.

Technological Advancements in Automotive Cameras

Technological advancements are another critical growth driver in the Philippines automotive cameras market. Camera technologies are constantly evolving to offer higher resolution, broader field-of-views, and smarter functionality through AI and machine learning integration. Manufacturers are investing significantly in these improvements to make driving safer and more efficient. For example, higher-resolution cameras can provide sharper images and better performance in low-light conditions, while advanced algorithms powered by artificial intelligence can detect pedestrians, vehicles, and other objects with greater accuracy, reducing the likelihood of accidents. The increased integration of AI-powered cameras for parking assistance, automatic braking, collision detection, and lane-keeping has created a broader range of applications, contributing to the demand for such cameras. These cameras are no longer limited to simple visual functions but have expanded into intelligent systems that aid in automated driving and help improve the accuracy of driver-assistance systems. As the automotive industry moves toward autonomous vehicles, the reliance on these advanced cameras will only increase. This shift toward automation and smarter vehicles is creating a fertile ground for the adoption of automotive cameras, pushing forward both innovation and market growth. The constant enhancements in camera features, along with the integration of data processing systems, are allowing manufacturers to meet consumer demand for more effective and reliable vehicle safety systems. Furthermore, these technological improvements are also expected to drive down costs over time, allowing for broader adoption, even in the lower-end vehicle segments.

Market Challenges

High Initial Cost of Advanced Camera Systems

One of the primary challenges hindering the widespread adoption of automotive cameras in the Philippines is the high initial cost of advanced camera systems. While the long-term benefits of improved vehicle safety, such as reduced accident rates and lower insurance premiums, justify the investment, the high upfront costs remain a barrier for many consumers and automotive manufacturers. The technology used in high-definition cameras, along with the integration of AI and machine learning capabilities, increases the overall expense of the system, which can be prohibitive for budget-conscious vehicle buyers and manufacturers who need to keep production costs low. This is particularly true for lower-end vehicle segments where cost efficiency is the priority. While premium and luxury vehicles have long integrated advanced cameras as standard features, the cost remains a significant hurdle for mass-market vehicles. Moreover, the development of more complex systems, such as surround-view cameras or 360-degree vision, further increases the cost, as it involves not only cameras but also sensors, wiring, and data processing units. This challenge may limit the adoption of these advanced systems in the short term, particularly in emerging markets where the focus remains on affordable solutions. As such, lowering the cost of automotive camera systems, through technological advancements and economies of scale, will be key to increasing adoption across all vehicle segments in the Philippines.

Regulatory and Certification Challenges

Another significant challenge in the Philippines automotive cameras market is navigating the complex regulatory and certification landscape. As automotive cameras become an integral part of advanced driver-assistance systems (ADAS), manufacturers must ensure that their products meet stringent safety regulations set by local authorities. These regulations are often specific to the country and can vary greatly across regions, which complicates the certification process for international companies looking to enter the market. Certification processes can be lengthy and expensive, particularly for new technologies, and can delay the introduction of new camera systems. Additionally, the lack of standardization in regulations across different regions of the Philippines can lead to confusion, regulatory hurdles, and unnecessary delays in market entry. Manufacturers must also adapt to evolving safety standards, which are becoming stricter over time. The compliance costs associated with certification, including testing and documentation, can significantly increase the cost of automotive cameras and reduce their affordability for local automakers. These challenges can slow down the adoption of new camera technologies and hinder market growth. Companies that are not prepared to meet the regulatory demands and are unable to navigate the certification process efficiently may find it difficult to stay competitive in the market.

Opportunities

Advancements in Camera Resolution and AI Integration

One of the most significant opportunities in the Philippines automotive cameras market lies in the advancements in camera resolution and AI integration. The demand for higher-resolution cameras, which provide better image quality and more precise object detection, is growing rapidly. AI integration is also becoming increasingly important, enabling cameras to perform complex tasks such as real-time analysis of road conditions, detecting pedestrians, and recognizing vehicles or other hazards. These capabilities allow for a higher level of safety and automation in vehicles, which appeals to both consumers and vehicle manufacturers alike. AI-based cameras are expected to play an essential role in the development of fully autonomous vehicles, which are expected to become a prominent feature in the automotive industry in the coming years. The demand for cameras with enhanced resolution and AI-driven functionality is likely to continue growing as the Philippines automotive market becomes more technologically advanced. As vehicle manufacturers integrate more autonomous driving technologies, the need for reliable, high-performance cameras will increase, presenting a major growth opportunity for companies in the sector. This technological advancement will not only enhance vehicle safety but will also drive the demand for more sophisticated camera systems. As the technology becomes more affordable, it is expected that the market will see increased adoption of these advanced camera systems across a wider range of vehicles, from premium to budget models.

Expansion in Electric and Autonomous Vehicle Segments

The Philippines automotive cameras market stands to benefit from the increasing demand for electric and autonomous vehicles, which rely heavily on advanced camera systems for navigation, safety, and autonomous driving features. Electric vehicles (EVs) are gaining popularity due to the government’s focus on sustainability and the growing consumer interest in eco-friendly transportation options. Autonomous vehicles, while still in the early stages of adoption, represent the future of mobility, with their need for sophisticated camera systems that can process real-time data for tasks such as obstacle detection, lane-keeping, and vehicle-to-vehicle communication. As the government pushes for greener transportation solutions and regulatory frameworks for autonomous driving are established, the demand for automotive cameras in these segments is expected to rise. The Philippines, with its increasing focus on infrastructure development and smart cities, presents an ideal environment for the growth of both electric and autonomous vehicles. Companies that focus on developing specialized camera systems tailored to these vehicles will have a distinct competitive advantage. Furthermore, as the demand for EVs and autonomous vehicles rises, manufacturers will be required to integrate cutting-edge camera systems into their vehicles, making this an attractive growth opportunity for market players.

Future Outlook

The Philippines automotive cameras market is set for continued growth over the next five years, driven by technological advancements, increasing demand for vehicle safety features, and the rise of electric and autonomous vehicles. As vehicle manufacturers continue to integrate advanced driver-assistance systems (ADAS) into their models, the market for automotive cameras will see significant expansion. Additionally, regulatory support for safer driving technologies, along with consumer demand for enhanced vehicle safety, will fuel further adoption of camera systems. The future outlook suggests a shift towards more affordable and efficient camera systems, which will help drive market penetration across different vehicle segments.

Major Players

- Aptiv

- Continental AG

- Valeo

- Bosch Mobility Solutions

- Mobileye

- Denso Corporation

- Magna International

- Panasonic Automotive Systems

- Delphi Technologies

- ZF Friedrichshafen AG

- Harman International

- Autoliv

- Kyocera

- Garmin

- Fujitsu Ten

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive manufacturers

- Automotive aftermarket service providers

- Fleet operators

- Technology providers

- Electric vehicle manufacturers

Research Methodology

Step 1: Identification of Key Variables

Identifying critical market variables, including product types, technologies, and consumer demand trends, through comprehensive research and expert consultations.

Step 2: Market Analysis and Construction

Utilizing secondary data, market models, and industry reports to build a comprehensive view of the market size, segments, and trends.

Step 3: Hypothesis Validation and Expert Consultation

Validating market assumptions and hypotheses with industry experts, OEMs, and suppliers to ensure data accuracy and real-world relevance.

Step 4: Research Synthesis and Final Output

Synthesizing data from multiple sources to finalize market forecasts, segmentation insights, and actionable recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Vehicle Safety Standards

Growing Adoption of ADAS

Rising Demand for Electric and Autonomous Vehicles - Market Challenges

High Cost of Advanced Camera Systems

Regulatory and Certification Hurdles

Integration Challenges in Legacy Vehicles - Market Opportunities

Advancements in Camera Resolution and AI Integration

Rising Demand for Autonomous Driving Systems

Government Support for Road Safety Initiatives - Trends

Integration of AI and Machine Learning in Cameras

Growth in Multi-Camera Systems for Enhanced Driver Assistance - Government Regulations

Vehicle Safety and Camera Requirements

Data Privacy and Security Regulations for Automotive Cameras

Certification Standards for ADAS Components - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Forward Facing Cameras

Surround View Cameras

Rear View Cameras

Interior Cameras

Side View Cameras - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Electric Vehicles

Autonomous Vehicles

Heavy Duty Vehicles - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Fitment

Retrofitting Solutions

Integrated Fitment - By End User Segment (In Value%)

Automobile Manufacturers

Vehicle Aftermarket Service Providers

Fleet Operators

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Camera Resolution, Integration Technology, Price Range)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Aptiv

Continental AG

Valeo

ZF Friedrichshafen AG

LG Electronics

Magna International

Delphi Technologies

Mobileye

Panasonic Automotive Systems

Bosch Mobility Solutions

Autoliv

Kyocera

Fujitsu Ten

Garmin

Denso Corporation

- OEM’s Focus on Advanced Driver Assistance Systems

- Aftermarket Service Providers Increasing Adoption of Cameras

- Fleet Operators Looking for Cost-Effective Solutions

- Rising Interest in Retrofitting Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now