Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Axles market demonstrates a structured expansion with a recorded valuation of USD ~ billion, supported by rising commercial vehicle demand, infrastructure development, and increasing vehicle parc. Growth is driven by logistics expansion, public transport modernization, and construction sector activities requiring durable drivetrain components. OEM production and aftermarket demand both contribute significantly, supported by government infrastructure initiatives and steady automotive assembly activity across the country.

Metro Manila, Cebu, and Davao emerge as dominant regions due to concentrated vehicle ownership, logistics hubs, and industrial activity. These cities benefit from higher commercial fleet density and infrastructure investments, enabling consistent axle demand. The Philippines also relies on imports from Japan, Thailand, and China, as these countries maintain strong automotive manufacturing ecosystems, technological expertise, and established supply chains supporting the domestic market.

Market Segmentation

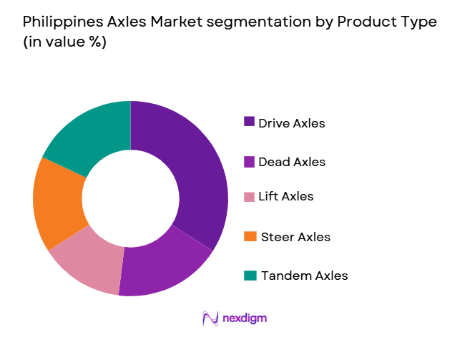

By Product Type:

Philippines Axles market is segmented by product type into drive axles, dead axles, lift axles, steer axles, and tandem axles. Recently, drive axles has a dominant market share due to factors such as high demand in commercial vehicles, logistics expansion, and infrastructure-related transport needs. The rising number of heavy-duty vehicles and increased freight movement contribute to higher adoption of drive axles, which are essential for power transmission. Additionally, fleet operators prioritize durability and performance, further strengthening the position of drive axles in both OEM and aftermarket segments.

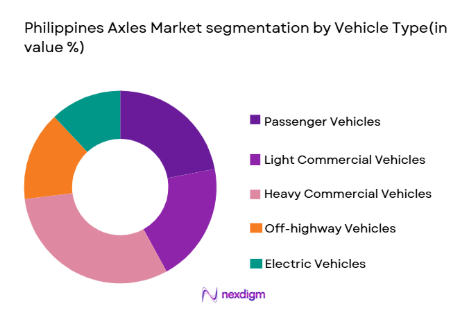

By Vehicle Type:

Philippines Axles market is segmented by vehicle type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, off-highway vehicles, and electric vehicles. Recently, heavy commercial vehicles has a dominant market share due to strong infrastructure growth, mining activities, and logistics demand across the country. The expansion of construction projects and freight transportation increases reliance on durable axle systems in trucks and buses. These vehicles require high load-bearing capacity and reliability, making them a primary driver of axle consumption in both OEM production and replacement markets.

Competitive Landscape

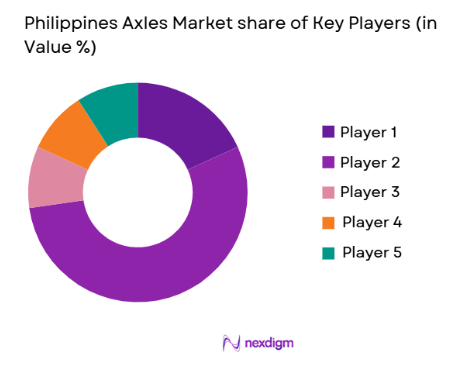

The Philippines Axles market reflects a moderately consolidated structure where global automotive component manufacturers and regional suppliers dominate through strong OEM partnerships and aftermarket distribution networks. Key players leverage technological innovation, localized supply chains, and cost optimization strategies to maintain competitiveness. Market participants focus on durability, efficiency, and integration with electric drivetrain systems to address evolving automotive requirements.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Supply Chain Integration |

| Dana Incorporated | 1904 | USA | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| American Axle & Manufacturing | 1994 | USA | ~ | ~ | ~ | ~ | ~ |

| Meritor Inc | 1909 | USA | ~ | ~ | ~ | ~ | ~ |

| GKN Automotive | 1759 | UK | ~ | ~ | ~ | ~ | ~ |

Philippines Axles Market Analysis

Growth Drivers

Expansion of Infrastructure and Logistics Networks:

The Philippines Axles market is significantly driven by increasing investments in infrastructure and logistics networks, which directly influence the demand for commercial vehicles requiring advanced axle systems. Government-led initiatives focusing on road construction, port development, and urban connectivity have accelerated the need for efficient transportation systems, thereby increasing fleet expansion. This surge in commercial vehicle deployment directly boosts demand for heavy-duty axles capable of supporting high load capacities and long-distance operations. Logistics companies are expanding their fleets to meet the growing demand for e-commerce and goods transportation, further contributing to axle consumption. Additionally, urbanization trends are increasing public transportation requirements, including buses and utility vehicles that depend on robust axle configurations. The continuous development of industrial zones and economic corridors also supports vehicle movement, increasing wear and replacement cycles of axles in the aftermarket. As fleet operators focus on reliability and performance, they increasingly invest in technologically advanced axle systems. The overall expansion of logistics infrastructure thus serves as a foundational driver of sustained axle market growth.

Rising Vehicle Parc and Aftermarket Demand:

The Philippines Axles market is also propelled by the growing vehicle parc, which significantly enhances aftermarket demand for axle components. As vehicle ownership increases across urban and semi-urban areas, the need for maintenance, repair, and replacement of axle systems becomes more frequent. Aging vehicles require periodic component replacements, particularly in axle assemblies subjected to continuous stress and load-bearing conditions. The expansion of ride-hailing services, delivery fleets, and small commercial transport operators contributes to higher vehicle utilization rates, accelerating wear and tear. This leads to a steady demand for replacement axles and associated components within the aftermarket ecosystem. Furthermore, local workshops and service centers are expanding their capabilities to cater to rising maintenance requirements, supporting aftermarket growth. Consumers and fleet operators are increasingly prioritizing cost-effective yet durable axle solutions, encouraging suppliers to offer diversified product ranges. The combination of increased vehicle usage and longer ownership cycles reinforces consistent aftermarket demand, making it a critical growth driver.

Market Challenges

Dependence on Imported Components and Supply Chain Volatility:

The Philippines Axles market faces a major challenge due to its heavy reliance on imported components and raw materials, which exposes the industry to global supply chain disruptions. Limited domestic manufacturing capabilities for advanced axle systems necessitate imports from countries with established automotive production ecosystems. This dependency results in vulnerability to fluctuating shipping costs, trade restrictions, and geopolitical uncertainties that can impact availability and pricing. Supply chain disruptions can delay production schedules for OEMs and increase lead times for aftermarket suppliers. Additionally, currency fluctuations further affect procurement costs, leading to pricing instability within the market. Local distributors often face challenges in maintaining consistent inventory levels, which impacts service delivery to fleet operators. The lack of localized production also restricts technological advancement and innovation within the domestic market. As a result, the industry remains susceptible to external shocks, making supply chain resilience a critical concern.

High Cost of Advanced Axle Technologies:

The Philippines Axles market also encounters challenges related to the high cost associated with advanced axle technologies, particularly those integrated with electric drivetrains and smart monitoring systems. Modern axle systems designed for electric vehicles or equipped with sensors for predictive maintenance require significant investment in research, development, and manufacturing. These costs are often passed on to consumers and fleet operators, limiting widespread adoption, especially among small and medium enterprises. High upfront costs discourage fleet upgrades and delay the transition to more efficient and technologically advanced axle solutions. Additionally, limited technical expertise and infrastructure for maintaining such systems further hinder their adoption. The price sensitivity of the local market amplifies this challenge, as buyers often prioritize affordability over advanced features. Consequently, while technological advancements present opportunities, their high cost acts as a barrier to rapid market penetration.

Opportunities

Adoption of Electric Vehicle Axle Systems: The Philippines

Axles market presents significant opportunities through the adoption of electric vehicle axle systems, driven by the gradual transition toward sustainable mobility solutions. Electric vehicles require specialized e-axles that integrate motors, power electronics, and transmission systems into a single unit, creating demand for innovative axle technologies. Government initiatives promoting cleaner transportation and reduced emissions are encouraging the adoption of electric vehicles across urban areas. As automotive manufacturers introduce more electric models, the need for compatible axle systems increases. This shift also opens opportunities for suppliers to develop lightweight and efficient axle solutions tailored for electric drivetrains. Additionally, the integration of advanced technologies such as regenerative braking and energy-efficient components enhances the value proposition of e-axles. Local assembly and potential manufacturing of electric vehicle components further strengthen market prospects. The growing focus on sustainability thus positions electric axle systems as a key growth avenue.

Localization of Manufacturing and Supply Chain Development:

The Philippines Axles market has the potential to benefit from increased localization of manufacturing and supply chain development, which can reduce dependency on imports and enhance market stability. Establishing domestic production facilities for axle components can lower transportation costs, improve supply chain efficiency, and enable faster response to market demand. Government support for industrialization and foreign investments can attract global manufacturers to set up local operations. This would not only create employment opportunities but also facilitate technology transfer and skill development within the country. Localization also allows customization of products based on local requirements, improving competitiveness in both OEM and aftermarket segments. Furthermore, developing a robust supplier ecosystem can strengthen resilience against global disruptions. The shift toward localized production thus represents a strategic opportunity for long-term market growth and sustainability.

Future Outlook

The Philippines Axles market is expected to witness steady growth over the next five years, supported by infrastructure expansion, increasing vehicle ownership, and advancements in automotive technology. The transition toward electric vehicles will drive demand for innovative axle systems, while government initiatives will support industrial growth. Additionally, improvements in supply chain efficiency and localization efforts will enhance market resilience. Rising aftermarket demand and fleet modernization will further contribute to sustained market expansion.

Major Players

- Dana Incorporated

- ZF Friedrichshafen AG

- American Axle & Manufacturing

- Meritor Inc

- GKN Automotive

- Hyundai Transys

- Bharat Forge

- Schaeffler Group

- Toyota Motor Philippines

- Mitsubishi Motors Philippines

- Isuzu Philippines

- Hino Motors Philippines

- AxleTech International

- Rane Madras

- Talbros Automotive Components

Key Target Audience

- Automotive manufacturers

- Logistics and fleet operators

- Construction companies

- Mining companies

- Auto component distributors

- E-commerce logistics providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Primary variables such as vehicle parc, axle demand by vehicle category, and aftermarket replacement cycles were identified. Secondary variables included logistics growth, infrastructure investment, and import dependency influencing market dynamics.

Step 2: Market Analysis and Construction

Data was analyzed using industry reports, trade statistics, and automotive production insights. Market sizing involved triangulating supply-demand data, OEM production figures, and aftermarket consumption trends.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, distributors, and supply chain participants validated assumptions. Feedback was incorporated to refine market segmentation, growth drivers, and competitive positioning insights.

Step 4: Research Synthesis and Final Output

All findings were consolidated into a structured framework. Quantitative and qualitative insights were combined to ensure accuracy, consistency, and relevance for strategic decision-making.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising commercial vehicle demand driven by infrastructure development

Expansion of logistics and e commerce sectors increasing fleet sizes

Government investments in road and transport infrastructure modernization

Growing adoption of heavy duty vehicles in mining and construction

Increasing vehicle parc leading to higher aftermarket demand - Market Challenges

Fluctuations in raw material prices affecting production costs

Limited domestic manufacturing capabilities leading to import dependence

Supply chain disruptions impacting component availability

High maintenance costs for advanced axle systems

Regulatory compliance challenges related to emissions and safety standards - Market Opportunities

Growing adoption of electric vehicles creating demand for e axle systems

Localization of manufacturing to reduce import dependency

Technological advancements in lightweight axle solutions - Trends

Shift towards lightweight and fuel efficient axle systems

Integration of smart sensors for predictive maintenance

Increased adoption of electric drive axles in urban fleets

Expansion of aftermarket service networks

Focus on durability and performance optimization in heavy duty axles - Government Regulations & Defense Policy

Implementation of vehicle safety and roadworthiness standards

Emission regulations influencing axle design efficiency

Infrastructure development policies boosting commercial vehicle demand - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Drive Axles

Dead Axles

Lift Axles

Steer Axles

Tandem Axles - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Off Highway Vehicles

Electric Vehicles - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Replacement

Retrofit Installations

Fleet Maintenance Contracts

Customized Vehicle Builds - By EndUser Segment (In Value%)

Automotive Manufacturers

Logistics and Fleet Operators

Construction Companies

Agriculture Sector

Mining Operators - By Procurement Channel (In Value%)

Direct OEM Contracts

Authorized Dealers

Third Party Distributors

Online Procurement Platforms

Fleet Procurement Agreements - By Material / Technology (in Value %)

Forged Steel Axles

Alloy Steel Axles

Lightweight Composite Axles

Electric Drive Axle Systems

Integrated Smart Axles

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio, Manufacturing Capacity, Technology Integration, Pricing Strategy, Distribution Network, Aftermarket Support, Regional Presence, OEM Partnerships, Innovation Capability, Supply Chain Efficiency)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

AAM Philippines Inc

Toyota Motor Philippines Corporation

Isuzu Philippines Corporation

Mitsubishi Motors Philippines Corporation

Hino Motors Philippines Corporation

Dana Incorporated

ZF Friedrichshafen AG

Meritor Inc

GKN Automotive Limited

Hyundai Transys Inc

Bharat Forge Limited

Talbros Automotive Components Limited

Rane Madras Limited

AxleTech International

Schaeffler Group

- Fleet operators focusing on cost efficiency and durability in axle systems

- OEMs prioritizing lightweight and performance optimized axle designs

- Construction and mining sectors demanding heavy duty axle solutions

- Aftermarket players expanding service offerings to cater to aging vehicle fleets

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now