Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines CEP (Courier, Express, and Parcel) market was valued at approximately USD ~ billion based on a recent historical assessment, supported by strong parcel shipment volumes generated by expanding e-commerce platforms and rising digital retail transactions. According to logistics industry datasets referenced by Statista and Philippine Statistics Authority trade and transport indicators, growing cross-border trade, urban retail distribution, and business-to-consumer parcel deliveries significantly support CEP network expansion across the national logistics sector.

Metro Manila remains the dominant operational hub within the Philippines CEP market due to its dense population concentration, major commercial districts, and central logistics infrastructure. The metropolitan region hosts primary distribution centers, airline cargo terminals, and port facilities supporting nationwide parcel movement. Cebu and Davao also play important regional roles due to expanding consumer markets, airport cargo connectivity, and industrial activity that supports domestic courier distribution and last-mile delivery operations.

Market Segmentation

By Product Type

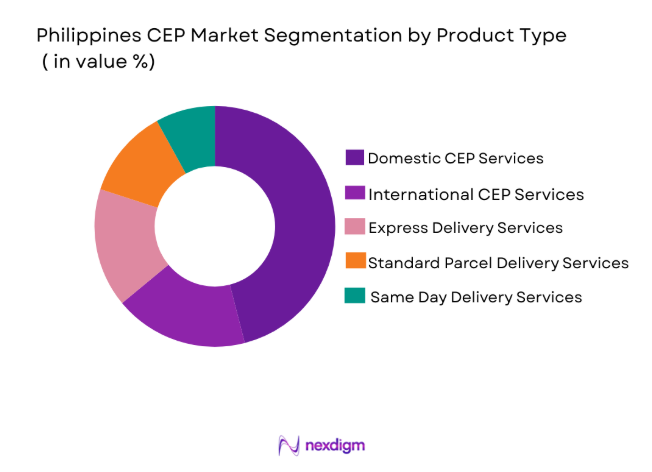

Philippines CEP Market is segmented by product type into domestic CEP services, international CEP services, express delivery services, standard parcel delivery services, and same day delivery services. Recently, domestic CEP services has a dominant market share due to factors such as rising e-commerce orders, increasing urban parcel shipments, and expanding business-to-consumer logistics operations across metropolitan areas. Domestic deliveries account for the majority of parcel movements generated by online retail transactions, food delivery logistics, and intercity commercial shipments. Logistics companies continue expanding last-mile delivery fleets, automated parcel sorting hubs, and distribution warehouses across major cities. The increasing reliance on online marketplaces and digital payment platforms further supports high parcel volume circulation within domestic logistics networks, making domestic CEP services the most dominant product category within the Philippines courier ecosystem.

By Platform Type

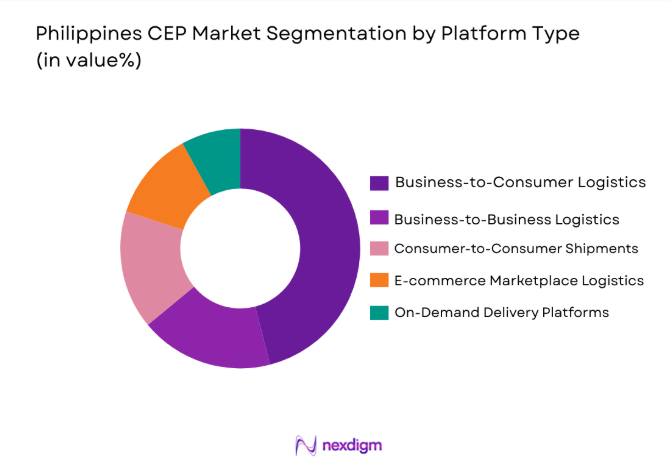

Philippines CEP Market market is segmented by platform type into business-to-consumer logistics, business-to-business logistics, consumer-to-consumer shipments, e-commerce marketplace logistics, and on-demand delivery platforms. Recently, business-to-consumer logistics has a dominant market share due to factors such as expanding online shopping activity, increased parcel volumes generated by digital marketplaces, and growing consumer demand for fast home deliveries. Retailers and online merchants depend on CEP networks to deliver products directly to consumers located across metropolitan and provincial regions. Logistics platforms continue integrating digital tracking systems, route optimization technology, and automated dispatch management to support higher shipment volumes. The expansion of online marketplaces such as Lazada and Shopee further strengthens business-to-consumer parcel flows, making this segment the leading logistics platform structure in the national CEP ecosystem.

Competitive Landscape

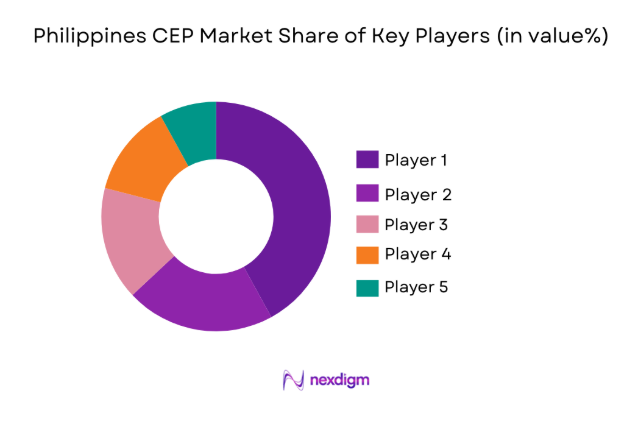

The Philippines CEP market demonstrates moderate consolidation where several international logistics companies operate alongside strong domestic courier providers. Global firms bring advanced logistics technology, cross-border shipping capabilities, and integrated supply chain networks, while local players maintain strong last-mile delivery coverage across islands and provincial regions. Competition increasingly focuses on delivery speed, parcel tracking technology, route optimization platforms, and e-commerce logistics integration. Strategic partnerships between logistics providers and digital marketplaces are strengthening parcel delivery infrastructure across the country.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Network Coverage |

| DHL Express | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| FedEx | 1971 | Memphis, USA | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta, USA | ~ | ~ | ~ | ~ | ~ |

| LBC Express | 1945 | Manila, Philippines | ~ | ~ | ~ | ~ | ~ |

| J&T Express | 2015 | Jakarta, Indonesia | ~ | ~ | ~ | ~ | ~ |

Philippines CEP Market Analysis

Growth Drivers

Rapid Expansion of E-commerce Platforms and Online Retail Logistics Demand

Rapid expansion of e-commerce platforms and online retail logistics demand significantly strengthens parcel shipment volumes within the Philippines CEP market. Digital marketplaces including Shopee and Lazada generate high daily order volumes that require reliable courier networks capable of supporting nationwide parcel distribution. Consumers increasingly prefer home delivery for electronics, fashion products, groceries, and household goods, which directly increases parcel flow through courier networks. Logistics providers continue investing in automated parcel sorting centers, urban fulfillment hubs, and motorcycle delivery fleets capable of navigating dense metropolitan traffic. The integration of mobile payment platforms also simplifies the online purchasing process and encourages frequent digital retail transactions. Expanding internet penetration and smartphone usage allow a larger portion of the population to participate in online commerce activities. Retail businesses are increasingly relying on CEP networks to reach customers located across island provinces where traditional retail infrastructure is limited. Logistics technology including route optimization software and parcel tracking systems improves delivery efficiency and customer experience. As online retail adoption continues increasing across urban and secondary cities, CEP networks remain critical logistics infrastructure supporting the digital commerce ecosystem.

Expansion of Cross Border Trade and International Parcel Shipments

Expansion of cross border trade and international parcel shipments significantly drives growth within the Philippines CEP market by increasing demand for reliable international shipping services. The country maintains active trade relationships with major global economies including China, Japan, South Korea, and the United States which generates continuous parcel movements through courier networks. Export sectors including electronics, apparel manufacturing, and consumer goods production rely on CEP providers for document shipping, product samples, and international small parcel deliveries. The rapid growth of international online shopping also increases inbound parcel shipments from overseas e-commerce platforms. Logistics providers operate integrated air cargo networks connecting major airports such as Ninoy Aquino International Airport and Mactan Cebu International Airport with global logistics hubs. Customs clearance technology and digital documentation systems further accelerate cross-border parcel processing. Businesses engaged in global supply chains require dependable express shipping to maintain efficient trade operations. International courier providers continue expanding logistics partnerships and airline cargo agreements to improve global delivery speed. As global commerce becomes increasingly digitalized and interconnected, cross-border parcel shipments continue strengthening CEP logistics demand across the Philippines.

Market Challenges

Geographic Fragmentation and Complex Island Logistics Infrastructure

Geographic fragmentation and complex island logistics infrastructure represents a significant challenge for the Philippines CEP market due to the country’s archipelagic structure consisting of thousands of islands. Parcel delivery networks must coordinate transportation across sea routes, domestic air cargo flights, and inter-island ferry systems to reach customers located outside major urban centers. This fragmented geography increases delivery time variability and operational costs for courier companies attempting to maintain nationwide coverage. Logistics providers often rely on multiple transportation modes including trucks, boats, and aircraft to move parcels between distribution hubs and provincial destinations. Limited logistics infrastructure in remote islands can also restrict warehouse availability and parcel handling capacity. Courier companies must therefore develop complex logistics routing systems and regional distribution centers to ensure consistent service coverage. Weather disruptions including typhoons and heavy rainfall also frequently impact transportation routes and delivery schedules. These logistical complexities require significant operational planning and investment in resilient supply chain networks. The cost of maintaining nationwide delivery coverage across dispersed islands remains a major structural challenge for CEP providers operating within the Philippines logistics environment.

Traffic Congestion and Urban Delivery Inefficiencies in Major Cities

Traffic congestion and urban delivery inefficiencies in major cities significantly impact CEP operational efficiency across the Philippines logistics sector. Metro Manila experiences some of the highest traffic congestion levels in Southeast Asia, which directly affects courier delivery schedules and vehicle productivity. Delivery drivers frequently encounter delays caused by dense road networks, limited parking availability, and high vehicle traffic during peak business hours. Logistics companies must deploy large fleets of motorcycles and smaller vehicles capable of navigating congested urban streets to maintain delivery speed. Urban infrastructure constraints also complicate parcel distribution in densely populated residential zones where road access may be limited. Courier companies therefore invest heavily in route optimization technology and dynamic dispatch systems to improve fleet efficiency. Rising fuel costs and extended delivery times further increase operational expenses for logistics providers operating in congested urban environments. Parcel demand generated by online shopping continues increasing faster than infrastructure improvements in major cities. These operational inefficiencies present ongoing challenges for CEP companies attempting to maintain fast delivery performance while controlling logistics costs.

Opportunities

Expansion of Digital Logistics Platforms and Smart Delivery Technologies

Expansion of digital logistics platforms and smart delivery technologies presents a major opportunity for CEP providers operating within the Philippines logistics ecosystem. Technology driven logistics systems including artificial intelligence routing software, automated parcel sorting systems, and real time shipment tracking platforms allow companies to improve operational efficiency and delivery accuracy. Mobile applications used by courier drivers enable faster dispatch coordination and improved communication with distribution hubs. Consumers also benefit from transparent parcel tracking features that provide real time shipment updates and estimated delivery times. Logistics companies increasingly deploy warehouse automation technologies to handle growing parcel volumes generated by e-commerce marketplaces. Digital logistics platforms also support predictive demand forecasting and dynamic route optimization which reduce delivery delays. Integration with online retail platforms allows courier networks to synchronize order fulfillment processes with logistics operations. Investment in digital logistics infrastructure therefore improves both service reliability and operational cost management. As technology adoption accelerates across the logistics sector, CEP providers have significant opportunities to modernize delivery networks and enhance nationwide parcel distribution capabilities.

Growth of Regional Logistics Hubs and Secondary City Distribution Networks

Growth of regional logistics hubs and secondary city distribution networks presents a major expansion opportunity for CEP providers seeking to improve nationwide parcel coverage across the Philippines. Logistics companies increasingly establish distribution centers in emerging regional cities including Cebu, Davao, Iloilo, and Cagayan de Oro to support decentralized parcel handling operations. These regional hubs reduce delivery distances between warehouses and consumers located outside Metro Manila. Expansion of airport cargo facilities and seaport logistics infrastructure further supports regional parcel distribution networks. E-commerce adoption is rising rapidly in secondary cities where consumers increasingly purchase goods through digital platforms. Courier companies therefore expand motorcycle delivery fleets and local parcel sorting facilities to support rising shipment volumes in provincial markets. Government infrastructure investments including road improvements and airport modernization programs also strengthen regional logistics connectivity. The development of multi city distribution networks allows CEP companies to improve delivery speed and reduce transportation costs. As consumer markets expand beyond metropolitan centers, regional logistics infrastructure will play a critical role in supporting future CEP market growth.

Future Outlook

The Philippines CEP market is expected to experience steady expansion supported by growing digital commerce activity, increasing smartphone adoption, and rising parcel shipment volumes across urban and regional cities. Logistics companies are investing heavily in warehouse automation, route optimization software, and advanced parcel tracking systems to improve operational efficiency. Government infrastructure development and airport cargo capacity expansion will further strengthen national logistics connectivity. Rising international trade activity and cross-border e-commerce are also expected to generate sustained demand for courier and express delivery services across the Philippines logistics sector.

Major Players

- DHL Express

- FedEx

- UPS

- LBC Express

- J&T Express

- Ninja Van

- Entrego

- 2GO Express

- GrabExpress

- Shopee Xpress

- Lazada Logistics

- Flash Express

- Air21

- Xend Business Solutions

- JRS Express

Key Target Audience

- Logistics and supply chain companies

- E-commerce marketplace operators

- Retail and distribution companies

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Technology and logistics platform providers

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying core market variables including parcel shipment volumes, courier network infrastructure, logistics technology adoption, and e-commerce transaction growth. Industry databases, logistics associations, and government trade data sources are used to identify the key indicators influencing the Philippines CEP market ecosystem.

Step 2: Market Analysis and Construction

Collected datasets are analyzed to construct market size estimations and segmentation structures across product types and logistics platforms. Shipment flows, logistics infrastructure capacity, and courier network distribution models are evaluated to understand market dynamics and competitive positioning.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics managers, courier operators, and e-commerce supply chain specialists validate the market assumptions. Their operational insights help confirm shipment trends, distribution network strategies, and infrastructure developments affecting the CEP market.

Step 4: Research Synthesis and Final Output

All validated findings are synthesized into a structured research framework combining quantitative market data with qualitative logistics industry insights. The final report provides a comprehensive understanding of market structure, growth drivers, competitive dynamics, and future logistics infrastructure developments.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid Expansion of E Commerce and Digital Retail Platforms

Increasing Demand for Fast Last Mile Delivery Services in Urban Areas

Growth of Cross Border Online Trade and International Parcel Volumes - Market Challenges

Infrastructure Constraints and Traffic Congestion Affecting Delivery Timelines

High Logistics Costs Across Archipelagic Transport Routes

Operational Complexity in Managing Last Mile Delivery Across Remote Islands - Market Opportunities

Expansion of Same Day and Hyperlocal Delivery Services

Investment in Automated Parcel Sorting and Smart Logistics Technologies

Growth of Regional Distribution Hubs Supporting Inter Island Commerce - Trends

Adoption of Digital Parcel Tracking and Real Time Logistics Platforms

Expansion of Micro Fulfillment Centers in Major Urban Regions - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Courier Delivery Services

Express Parcel Services

Same Day Delivery Services

International Parcel Services

Document and Small Parcel Delivery - By Platform Type (In Value%)

Road Transportation Networks

Air Cargo Logistics Networks

Inter Island Maritime Logistics

Urban Micro Fulfillment Networks

Integrated Multi Modal Logistics - By Fitment Type (In Value%)

Domestic CEP Services

Cross Border CEP Services

Business to Business Delivery Services

Business to Consumer Delivery Services - By End User Segment (In Value%)

E Commerce Retailers

Corporate and Business Enterprises

Individual Consumers

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio, Delivery Speed, Geographic Coverage, Pricing Strategy, Technology Integration, Fleet Capacity, International Logistics Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

LBC Express

JRS Express

2GO Group

DHL Express Philippines

FedEx Philippines

UPS Philippines

Entrego

Ninja Van Philippines

J&T Express Philippines

GrabExpress Philippines

Shopee Xpress Philippines

Air21

Xend Business Solutions

Flash Express Philippines

Zoom Logistics

- Rising Order Volumes from E Commerce Retailers Driving Parcel Delivery Demand

- Corporate Sector Dependence on Reliable Document and Parcel Distribution Networks

- Increasing Demand from Individual Consumers for Fast and Affordable Delivery Services

- Growing SME Participation in Online Retail Requiring Scalable Logistics Support

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now