Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Charging Connectors market demonstrates a total valuation of USD ~ billion based on a recent historical assessment, driven primarily by increasing electric vehicle adoption and expansion of public charging infrastructure. Government-backed electrification programs, combined with rising urban mobility demand, have accelerated deployment of AC and DC charging systems. Investments from private charging operators and OEM partnerships have further strengthened connector demand, especially for fast-charging solutions integrated into commercial and passenger vehicle ecosystems.

Metro Manila, Cebu, and Davao emerge as dominant regions due to higher electric vehicle penetration and infrastructure readiness supported by urban density and policy focus. These cities benefit from concentrated investments in smart mobility projects and charging networks. International influences from Japan, China, and South Korea contribute to technology adoption, while proximity to manufacturing hubs supports supply chain efficiency. Urban commercial fleets and logistics operators in these regions are key contributors to sustained connector demand.

Market Segmentation

By Product Type

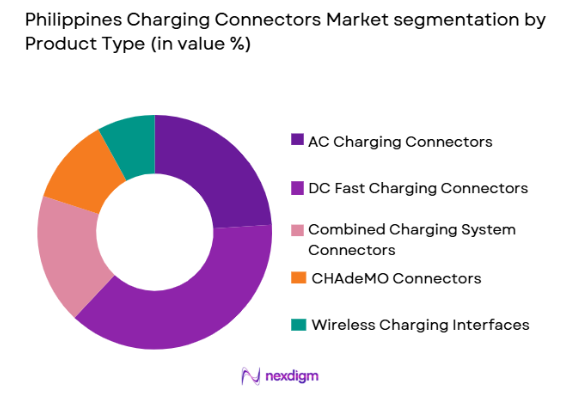

Philippines Charging Connectors market is segmented by product type into AC Charging Connectors, DC Fast Charging Connectors, Combined Charging System Connectors, CHAdeMO Connectors, and Wireless Charging Interfaces. Recently, DC Fast Charging Connectors has a dominant market share due to factors such as increasing demand for rapid charging infrastructure, rising adoption among commercial fleets, growing urban mobility needs, and expansion of high-capacity charging stations across major cities. Faster turnaround times and compatibility with modern EV platforms have further strengthened their position in both public and private charging networks.

By End User

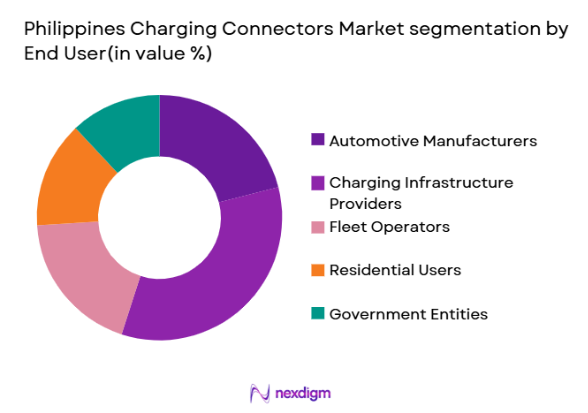

Philippines Charging Connectors market is segmented by end user into Automotive Manufacturers, Charging Infrastructure Providers, Fleet Operators, Residential Users, and Government Entities. Recently, Charging Infrastructure Providers has a dominant market share due to factors such as aggressive deployment of public charging stations, strong private investments, and partnerships with automotive OEMs. Their role in scaling nationwide networks and integrating fast charging solutions across highways and urban centers has driven consistent demand for high-performance connector systems.

Competitive Landscape

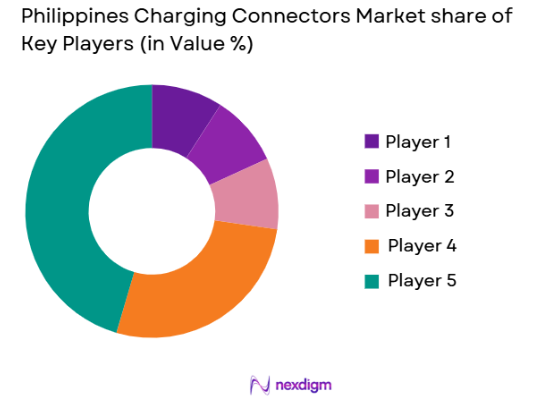

The Philippines Charging Connectors market exhibits moderate consolidation, with global electrical component manufacturers and regional suppliers competing alongside emerging local distributors. Large multinational firms dominate through technological capabilities, product standardization, and established supply chains. Strategic collaborations with EV manufacturers and infrastructure developers strengthen market positioning, while smaller players focus on niche applications and aftermarket solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Connector Standard Compatibility |

| Yazaki Corporation | 1941 | Japan | ~ | ~ | ~ | ~ | ~ |

| TE Connectivity | 2007 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Amphenol Corporation | 1932 | USA | ~ | ~ | ~ | ~ | ~ |

| ABB Ltd | 1988 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Siemens AG | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

Philippines Charging Connectors Market Analysis

Growth Drivers

Rapid Expansion of Electric Vehicle Ecosystem and Charging Infrastructure

The increasing adoption of electric vehicles across urban and semi-urban areas is significantly driving the demand for charging connectors in the Philippines market. Government incentives supporting EV purchases and infrastructure deployment are accelerating ecosystem development and creating demand for reliable charging interfaces. Public and private stakeholders are actively investing in fast-charging networks, particularly in major cities and highways. The integration of EVs into commercial fleets such as ride-hailing and logistics services is further increasing usage intensity of charging connectors. Rising fuel costs are encouraging consumers and businesses to shift toward electric mobility, thereby boosting connector demand. Automotive manufacturers are also expanding EV offerings, requiring standardized connector solutions for compatibility. Infrastructure providers are focusing on high-capacity connectors to support faster charging cycles. Additionally, international technology transfer from advanced EV markets is improving product quality and availability. The cumulative effect of these factors is creating a strong foundation for sustained growth in connector demand.

Increasing Government Support and Policy Framework for Electrification

Government policies promoting sustainable transportation and reducing carbon emissions are playing a critical role in driving the charging connectors market. Regulatory frameworks supporting EV infrastructure development are encouraging investments from both domestic and international players. Fiscal incentives such as tax exemptions and subsidies are making EV adoption more attractive, indirectly boosting demand for connectors. Public sector initiatives are facilitating installation of charging stations in urban centers and along highways. Policy-driven mandates for fleet electrification are also increasing connector usage in commercial sectors. Infrastructure development programs are emphasizing interoperability standards, ensuring compatibility across connector types. The government is collaborating with private stakeholders to accelerate deployment of charging networks. Increased focus on renewable energy integration is further supporting sustainable charging infrastructure. These policy measures are collectively enhancing market confidence and encouraging long-term investments in charging connector technologies.

Market Challenges

Lack of Standardization Across Charging Connector Technologies

The absence of a unified standard for charging connectors poses a significant challenge in the Philippines market. Multiple connector types such as CCS, CHAdeMO, and proprietary systems create compatibility issues across vehicles and charging stations. This fragmentation complicates infrastructure planning and increases costs for stakeholders. Consumers face inconvenience due to limited interoperability, which can hinder EV adoption. Charging infrastructure providers must invest in multi-standard systems, raising capital expenditure requirements. Automotive manufacturers also face design complexities when catering to different connector standards. The lack of clear regulatory enforcement on standardization slows down market harmonization. Import dependency on specific connector technologies further adds to supply chain challenges. Additionally, maintenance and servicing become more complex due to varied connector specifications. These issues collectively restrict the efficiency and scalability of charging infrastructure deployment.

High Cost of Advanced Charging Connector Systems and Infrastructure Deployment

The high cost associated with advanced charging connectors and supporting infrastructure remains a major barrier to market growth. Fast-charging connectors require sophisticated materials and cooling systems, increasing manufacturing costs. Installation of high-capacity charging stations involves significant capital investment, limiting expansion in less developed regions. Smaller players and local businesses face financial constraints in adopting advanced connector technologies. Consumers may also be discouraged by higher charging costs associated with premium infrastructure. The need for grid upgrades to support high-power charging further escalates overall expenses. Import reliance on advanced components increases price volatility due to currency fluctuations. Maintenance and operational costs of charging systems add to long-term financial burdens. Limited access to financing options for infrastructure projects further restricts growth. These cost-related challenges slow down the pace of market expansion and adoption.

Opportunities

Development of Smart and Connected Charging Connector Technologies

The integration of smart technologies into charging connectors presents a significant opportunity for market growth in the Philippines. Advanced connectors equipped with IoT capabilities enable real-time monitoring and efficient energy management. These technologies enhance user convenience through features such as remote diagnostics and automated billing systems. Infrastructure providers can optimize network performance by analyzing usage data and improving load distribution. Smart connectors also support integration with renewable energy sources, promoting sustainable charging solutions. Increasing digitalization in urban infrastructure is creating demand for connected charging systems. Automotive manufacturers are incorporating smart features into EVs, requiring compatible connector technologies. The adoption of software-driven solutions is opening new revenue streams for service providers. Enhanced safety features in smart connectors further improve reliability and consumer confidence. This technological shift is expected to drive innovation and competitiveness in the market.

Expansion of Charging Infrastructure in Emerging Urban and Rural Areas

The growing focus on expanding charging infrastructure beyond major cities offers substantial opportunities for connector manufacturers. Emerging urban centers and rural regions are gradually adopting electric mobility, creating new demand for charging solutions. Government initiatives aimed at inclusive infrastructure development are supporting expansion in underserved areas. Deployment of decentralized charging networks can improve accessibility and encourage EV adoption in smaller towns. Infrastructure providers are exploring cost-effective solutions such as modular connectors to reduce deployment expenses. Partnerships with local businesses and municipalities are facilitating faster network expansion. The increasing electrification of public transportation systems in regional areas is further driving connector demand. Renewable energy integration in rural charging stations is enhancing sustainability. Improved connectivity between urban and rural charging networks is strengthening the overall ecosystem. These developments are expected to unlock new growth avenues for the market.

Future Outlook

The Philippines Charging Connectors market is expected to witness steady expansion over the next five years, supported by increasing EV adoption and infrastructure investments. Advancements in fast-charging and smart connector technologies will enhance system efficiency and user experience. Government policies promoting sustainable mobility will continue to drive infrastructure deployment. Rising demand from commercial fleets and logistics sectors will further strengthen market growth. Integration with renewable energy and digital platforms will shape the next phase of development.

Step 1: Identification of Key Variables

Market variables such as connector types, EV adoption rates, infrastructure density, and regulatory frameworks were identified. Data points were collected to establish relationships between demand drivers and supply trends across regions.

Step 2: Market Analysis and Construction

Comprehensive analysis was conducted using historical data and industry insights to construct market models. Segmentation frameworks were developed to understand product distribution and end-user dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, manufacturers, and infrastructure providers were consulted to validate assumptions. Feedback was incorporated to refine data accuracy and ensure alignment with real market conditions.

Step 4: Research Synthesis and Final Output

All findings were synthesized into structured insights, ensuring consistency across segments. Final outputs were reviewed for accuracy, completeness, and alignment with industry standards.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of electric vehicle adoption across urban regions

Government incentives supporting EV charging infrastructure development

Rising investment in public fast charging networks - Market Challenges

High cost of advanced fast charging connector systems

Compatibility issues across different connector standards

Limited availability of domestic manufacturing capabilities - Market Opportunities

Growth in fleet electrification requiring standardized connectors

Increasing demand for smart and connected charging solutions

Expansion of rural and semi urban charging infrastructure - Trends

Adoption of combined charging system standards across platforms

Integration of IoT enabled smart connectors

Development of ultra fast liquid cooled connectors

Shift toward compact and lightweight connector designs

Emergence of wireless charging connector alternatives - Government Regulations & Defense Policy

Implementation of national EV roadmap and infrastructure policies

Standardization of charging connector types under regulatory bodies

Incentives and subsidies for domestic EV component manufacturing - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AC Charging Connectors

DC Fast Charging Connectors

Wireless Charging Interfaces

Combined Charging System Connectors

Proprietary Connector Systems - By Platform Type (In Value%)

Passenger Electric Vehicles

Commercial Electric Vehicles

Electric Two Wheelers

Public Charging Infrastructure

Private Residential Charging Systems - By Fitment Type (In Value%)

OEM Integrated Connectors

Aftermarket Replacement Connectors

Portable Charging Connectors

Fixed Charging Station Connectors

Modular Connector Assemblies - By EndUser Segment (In Value%)

Automotive Manufacturers

Charging Infrastructure Providers

Fleet Operators

Residential Users

Government and Municipal Authorities - By Procurement Channel (In Value%)

Direct OEM Procurement

Government Tender Contracts

Distributor and Dealer Networks

Online B2B Platforms

Third Party Infrastructure Partnerships - By Material / Technology (in Value %)

Copper Based Conductive Connectors

High Temperature Resistant Polymers

Liquid Cooled Connector Systems

Smart Sensor Integrated Connectors

Corrosion Resistant Alloy Connectors

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Connector Type Compatibility, Charging Speed Capacity, Thermal Management Efficiency, Material Durability, Cost Structure, Integration Capability, Smart Connectivity Features, Standard Compliance, Installation Flexibility, After Sales Support)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Yazaki Corporation

Sumitomo Electric Industries

TE Connectivity

Aptiv PLC

Amphenol Corporation

Phoenix Contact

Leoni AG

HARTING Technology Group

Molex LLC

Rosenberger Group

Furukawa Electric Co Ltd

Schneider Electric

ABB Ltd

Siemens AG

Delta Electronics Inc

- Automotive manufacturers are prioritizing standardized connectors for interoperability across vehicle platforms

- Charging infrastructure providers are expanding networks with fast charging compatible connectors

- Fleet operators are adopting durable connectors for high utilization commercial applications

- Residential users are increasingly installing home charging connectors with safety features

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now