Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines cloud infrastructure market is embedded within the national digital and data center ecosystem, valued at approximately USD ~ billion based on a recent historical assessment of cloud platform capacity, hyperscale data centers, and enterprise cloud deployments. Growth is driven by enterprise digital transformation, e-commerce expansion, and rapid adoption of SaaS and platform services across telecom, finance, government, and IT-BPM sectors. Investments in hyperscale facilities, hybrid cloud architecture, and sovereign cloud initiatives are expanding domestic computing and storage infrastructure.

Metro Manila dominates cloud infrastructure concentration due to hyperscale data center presence, dense enterprise demand, and international connectivity through major submarine cable landing systems enabling regional cloud integration. Laguna and Cavite host emerging cloud facilities within industrial and technology parks supported by power and land availability. Cebu is developing as a secondary cloud node driven by regional enterprise demand and IT-BPM operations. The Philippines is integrated with regional cloud hubs in Singapore and Indonesia, enabling cross-border cloud service delivery and redundancy architectures.

Market Segmentation

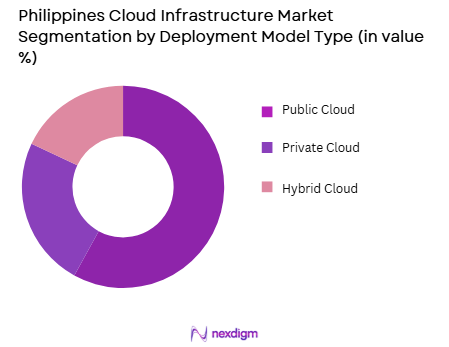

By Deployment Model

Philippines Cloud Infrastructure market is segmented by deployment model into public cloud, private cloud, and hybrid cloud. Recently, public cloud has a dominant market share due to factors such as rapid enterprise migration, hyperscale provider presence, and cost-efficient scalability for digital services. Enterprises in telecom, finance, retail, and IT-BPM sectors prioritize public cloud platforms for application hosting, data storage, and analytics workloads without capital expenditure requirements. Hyperscale providers deliver on-demand computing resources with regional integration and compliance features suitable for Philippine enterprises. Private and hybrid cloud adoption is expanding but remains dependent on organizational maturity and regulatory requirements compared to widespread public cloud accessibility and service breadth.

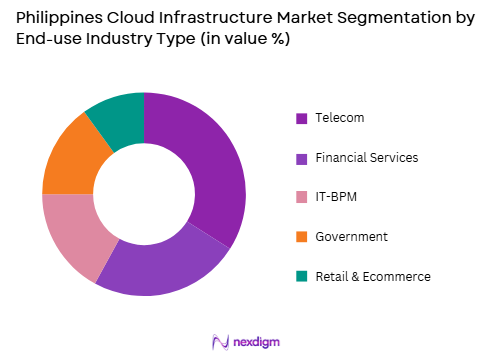

By End-Use Industry

Philippines Cloud Infrastructure market is segmented by end-use industry into telecom, financial services, government, IT-BPM, and retail & e-commerce. Recently, telecom has a dominant market share due to factors such as network virtualization, digital service platforms, and large-scale subscriber data processing requirements. Telecom operators deploy cloud infrastructure to support core network functions, customer analytics, and digital content services across nationwide user bases. IT-BPM and financial services sectors also drive cloud adoption, but telecom infrastructure ownership and continuous digital service delivery position it as the largest investor in cloud computing capacity across the Philippines digital ecosystem.

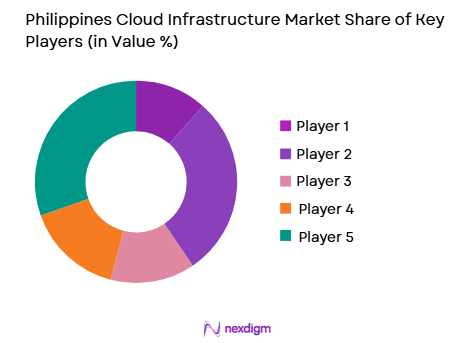

Competitive Landscape

The Philippines cloud infrastructure market is dominated by global hyperscale cloud providers and regional data center operators supplying computing capacity to enterprises and telecom networks. Market concentration is increasing as hyperscalers establish local availability zones and partner with domestic telecom and colocation firms. Local telecom operators influence connectivity and hybrid cloud integration, while global providers lead in platform services and scalability. Competition focuses on data center presence, service ecosystem breadth, and regulatory compliance capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cloud Deployment Strategy |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | USA | ~ | ~ | ~ | ~ | ~ |

| Alibaba Cloud | 2009 | China | ~ | ~ | ~ | ~ | ~ |

| PLDT | 1928 | Philippines | ~ | ~ | ~ | ~ | ~ |

Philippines Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Cloud Migration Acceleration

The Philippines is undergoing rapid enterprise digitalization across sectors including telecom, banking, retail, healthcare, and IT-BPM, creating sustained demand for scalable cloud infrastructure capable of supporting digital platforms, analytics, and automation systems. Organizations are replacing legacy on-premise IT systems with cloud-based applications to improve operational efficiency, flexibility, and service innovation. Cloud platforms enable rapid deployment of digital services including e-commerce platforms, mobile banking, and enterprise collaboration systems. Data-driven decision making and analytics workloads require elastic compute and storage capacity accessible through cloud environments. The IT-BPM sector is transitioning toward cloud-hosted service delivery platforms enabling global client integration. Financial institutions adopt cloud infrastructure for digital banking and transaction processing modernization. Government digital services initiatives increase demand for secure cloud platforms supporting citizen services and administration. Small and medium enterprises access advanced computing capabilities through public cloud without infrastructure investment. Hybrid cloud adoption allows enterprises to integrate existing systems with scalable cloud resources. As digital transformation expands across Philippine industries, cloud infrastructure becomes the foundational platform for modern business operations nationwide.

Hyperscale Data Center Expansion and Regional Cloud Integration

Global cloud providers and data center operators are investing in hyperscale facilities and regional availability zones in the Philippines to support domestic demand and reduce reliance on overseas cloud regions, significantly expanding national cloud infrastructure capacity. Hyperscale data centers provide high-density computing, storage, and networking infrastructure enabling cloud platform services at scale. Localization of cloud regions improves latency, data sovereignty compliance, and service reliability for Philippine enterprises. Telecom operators partner with hyperscalers to integrate connectivity and cloud services across nationwide networks. Regional cloud ecosystems in Southeast Asia interconnect Philippine facilities with Singapore and Indonesian data hubs enabling redundancy and scalability. Enterprises migrating mission-critical workloads require local cloud availability to meet regulatory and performance requirements. Government policies encouraging domestic data hosting stimulate infrastructure investment. E-commerce and digital platform growth generate continuous cloud workload demand. Data center colocation providers expand facilities to host cloud infrastructure equipment. As hyperscale and regional cloud infrastructure matures domestically, adoption of cloud services accelerates across industries and organizations nationwide.

Market Challenges

Data Sovereignty Concerns and Regulatory Compliance Complexity

Cloud infrastructure adoption in the Philippines faces regulatory and compliance challenges related to data localization, privacy protection, and sector-specific information governance requirements affecting enterprise and government cloud migration decisions. Sensitive sectors including finance, healthcare, and public administration require strict data handling and storage controls, necessitating localized cloud infrastructure or private cloud deployments. Cross-border data transfer regulations and compliance obligations create complexity for organizations utilizing international cloud providers. Enterprises must evaluate legal and security implications of hosting data outside national jurisdiction. Cloud providers must implement domestic availability zones and compliance frameworks to address regulatory expectations. Certification and audit requirements increase deployment costs and timelines. Government agencies often mandate sovereign or private cloud solutions rather than public cloud environments. Industry-specific regulations vary across sectors complicating standardized cloud adoption strategies. Data protection concerns affect enterprise trust in shared cloud infrastructure. Regulatory evolution and interpretation uncertainty slow migration of critical workloads. These governance constraints moderate cloud infrastructure adoption despite strong demand.

Connectivity and Infrastructure Reliability Constraints Outside Major Cities

The Philippines’ uneven telecommunications infrastructure and connectivity reliability across regions create operational challenges for cloud infrastructure deployment and adoption beyond metropolitan centers. High-capacity fiber networks and data center facilities are concentrated in Metro Manila and selected industrial zones, limiting cloud access performance in provincial areas. Enterprises in secondary cities may experience latency and bandwidth limitations affecting cloud application performance. Power reliability variations across regions affect data center operations and uptime guarantees. Geographic dispersion across islands increases cost and complexity of nationwide connectivity infrastructure. Submarine cable dependence and routing redundancy limitations affect network resilience. Cloud providers require robust connectivity ecosystems to ensure service quality across the country. Regional enterprises face barriers in accessing advanced cloud services comparable to metropolitan organizations. Infrastructure investment outside urban centers remains limited relative to demand growth. Nationwide cloud adoption depends on improved connectivity and digital infrastructure expansion. These structural infrastructure gaps constrain uniform cloud infrastructure penetration across the Philippines.

Opportunities

Development of Sovereign and Government Cloud Infrastructure

The Philippine government’s digital transformation agenda and data sovereignty priorities are creating opportunities for development of sovereign cloud infrastructure dedicated to public sector and regulated industries, driving investment in domestic cloud computing capacity. Government agencies require secure, locally controlled cloud platforms for citizen data, public administration, and national systems. Sovereign cloud initiatives encourage domestic data center construction and cloud platform localization. Partnerships between global hyperscalers and national telecom or technology firms enable compliant cloud deployment models. Public sector digital services including health, taxation, and identity systems require scalable cloud infrastructure. Defense and national security applications demand sovereign compute environments. Local cloud ecosystems stimulate domestic technology capability development. Government procurement programs create stable demand for cloud infrastructure providers. Data localization regulations incentivize domestic hosting. Public sector cloud adoption encourages private sector migration. As sovereign cloud initiatives expand, domestic cloud infrastructure investment increases significantly.

Cloud Adoption Across IT-BPM and Digital Services Industries

The Philippines’ globally significant IT-BPM and digital services industries are rapidly adopting cloud infrastructure to support scalable service delivery platforms, automation tools, and data-driven operations, creating strong domestic demand for cloud computing capacity. Outsourcing providers deploy cloud-based contact center, analytics, and workflow platforms serving international clients. Cloud infrastructure enables remote service delivery, workforce mobility, and global integration. AI and automation technologies integrated into IT-BPM platforms require scalable cloud resources. Digital content, e-commerce support, and back-office services depend on cloud-hosted applications. Enterprises serving global markets require reliable and compliant cloud infrastructure within the Philippines. Local data hosting supports privacy and contractual requirements for clients. Cloud adoption improves operational efficiency and service scalability across outsourcing firms. Data-intensive service analytics drive storage and compute demand. IT-BPM sector growth directly translates into increased cloud infrastructure utilization. As outsourcing evolves into digital service delivery, cloud infrastructure demand expands significantly within the Philippines economy.

Future Outlook

The Philippines cloud infrastructure market is expected to expand strongly as enterprise digital transformation and hyperscale data center investment continue nationwide. Local cloud regions and sovereign cloud initiatives will increase domestic computing capacity. Telecom and IT-BPM sectors will remain primary adopters of cloud platforms. Regional connectivity and data center expansion beyond Metro Manila will support nationwide adoption. Cloud infrastructure will become a core digital backbone for Philippine economic modernization.

Major Players

- Amazon Web Services

- Microsoft

- Google Cloud

- Alibaba Cloud

- PLDT

- Globe Telecom

- NTT Ltd.

- Equinix

- Digital Realty

- ST Telemedia Global Data Centres

- Huawei Cloud

- Oracle Cloud

- Tencent Cloud

- VMWare

- Rackspace

Key Target Audience

- Telecom operators

- Cloud service providers

- Data center operators

- Financial institutions

- IT-BPM companies

- E-commerce platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Cloud infrastructure capacity, hyperscale data center presence, enterprise cloud adoption intensity, and connectivity availability were identified as primary variables. Regulatory and data sovereignty factors were mapped. Industry cloud workload demand was assessed.

Step 2: Market Analysis and Construction

Market structure was constructed through analysis of deployment models, sector adoption, and infrastructure distribution across regions. Public, private, and hybrid cloud architectures were evaluated. End-use demand linkages were modeled.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding adoption drivers, regulatory impacts, and infrastructure constraints were validated through ecosystem benchmarking and technology analysis. Regional cloud trends were incorporated. Competitive positioning factors were verified.

Step 4: Research Synthesis and Final Output

All insights were synthesized into a structured market model describing segmentation, competition, growth drivers, and opportunities. Infrastructure investment and demand dynamics were integrated. Final outputs reflected technology and digitalization trends shaping the Philippines cloud infrastructure outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid enterprise migration to cloud-based applications and services

Expansion of hyperscale and colocation data center investments

Growth of digital economy and online platforms in Philippines - Market Challenges

Data sovereignty and compliance requirements for cloud hosting

Limited domestic hyperscale capacity outside major hubs

Power and connectivity reliability for large-scale data centers - Market Opportunities

Localized sovereign cloud and government cloud platforms

Industry-specific cloud adoption in finance and healthcare

Edge cloud deployment for low-latency digital services - Trends

Shift toward hybrid and multi-cloud architectures

Adoption of hyperconverged and software-defined infrastructure

Integration of edge and telecom cloud environments - Government regulations

National cloud-first and digital government initiatives

Data privacy and cross-border data transfer regulations

Investment incentives for data center and cloud facilities - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Platforms

Cloud Storage Infrastructure

Cloud Networking Infrastructure - By Platform Type (In Value%)

Hyperscale Data Centers

Colocation Facilities

Enterprise On-Premise Cloud

Telecom Cloud Platforms

Edge Cloud Infrastructure - By Fitment Type (In Value%)

Greenfield Cloud Deployment

Data Center Cloud Retrofit

Hyperconverged Infrastructure Integration

Containerized Cloud Modules

Cloud Expansion Clusters - By EndUser Segment (In Value%)

Banking and Financial Services

Telecommunications Providers

E-commerce and Digital Platforms

Government and Public Sector

Healthcare and Life Sciences - By Procurement Channel (In Value%)

Direct Hyperscaler Contracts

Cloud Service Providers

System Integrators and MSPs

Telecom Operator Partnerships

Public Sector Procurement

- Market Share Analysis

- Cross Comparison Parameters (Compute Density, Storage Performance Scalability, Network Throughput Capacity, Data Center Power Efficiency, Cloud Platform Integration, Multi-Cloud Interoperability, Security and Compliance Controls, Automation and Orchestration Capability, Edge Cloud Integration, Service Availability SLA)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services Philippines

Microsoft Azure Philippines

Google Cloud Philippines

Alibaba Cloud Philippines

Huawei Cloud Philippines

PLDT

ePLDT

Globe Telecom

ST Telemedia Global Data Centres Philippines

Converge ICT Solutions

NTT Global Data Centers Philippines

Equinix Philippines

Digital Edge Philippines

VITRO Data Center

Schneider Electric Philippines

- Banks and financial institutions migrating core workloads to cloud

- Telecom operators building cloud-native network platforms

- E-commerce and digital firms scaling cloud capacity rapidly

- Government agencies adopting sovereign and public cloud

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now