Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines cold chain logistics market demonstrates steady expansion supported by growing demand for temperature controlled food distribution and pharmaceutical supply chains. Based on a recent historical assessment, the Philippines cold chain logistics market generated approximately USD ~ billion in logistics service revenue according to datasets referenced from the Philippine Statistics Authority food distribution statistics and World Bank supply chain infrastructure studies. Market expansion is driven by increasing consumption of frozen food products, expanding supermarket distribution networks, and rising pharmaceutical imports requiring reliable temperature controlled transportation and storage infrastructure.

Cold chain logistics infrastructure is concentrated primarily around Metro Manila, Cebu, and Davao where port connectivity, consumer demand centers, and food processing clusters support high volume refrigerated logistics activity. Manila hosts the country’s largest refrigerated warehouse clusters and pharmaceutical distribution facilities supported by major international airports and container terminals. Cebu functions as a central cold storage and maritime logistics hub connecting the Visayas food distribution network, while Davao supports agricultural exports and seafood logistics operations across Mindanao supported by expanding port infrastructure and regional food processing industries.

Market Segmentation

By Service Type

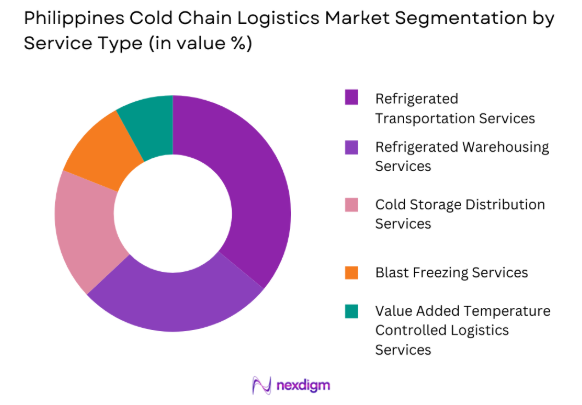

Philippines Cold Chain Logistics market is segmented by product type into refrigerated transportation services, refrigerated warehousing services, blast freezing services, cold storage distribution services, and value added temperature controlled logistics services. Recently, refrigerated transportation services has a dominant market share due to factors such as extensive nationwide food distribution requirements, increasing seafood exports, and the need for reliable temperature controlled delivery networks connecting production facilities with retail markets. Food processors, seafood exporters, and pharmaceutical distributors rely heavily on refrigerated trucking fleets capable of maintaining strict temperature conditions during intercity transportation. The country’s archipelagic geography also requires temperature controlled maritime and trucking coordination to transport frozen food and medical products between islands.

By End User Industry

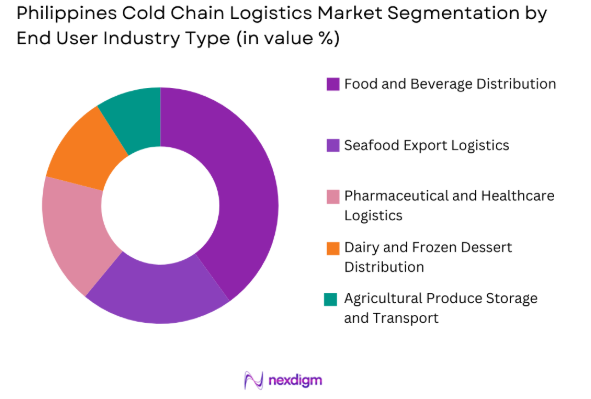

Philippines Cold Chain Logistics market is segmented by product type into food and beverage distribution, pharmaceutical and healthcare logistics, seafood export logistics, dairy and frozen dessert distribution, and agricultural produce storage and transport. Recently, food and beverage distribution has a dominant market share due to factors such as large national consumption of frozen meat, processed foods, and ready to cook products supplied through supermarket and convenience store networks. Food manufacturers and importers depend heavily on cold chain logistics providers that operate refrigerated warehouses and temperature controlled delivery fleets capable of maintaining product quality throughout the supply chain. Rapid expansion of supermarket retail chains and modern grocery distribution infrastructure also strengthens demand for large scale refrigerated logistics networks.

Competitive Landscape

The Philippines cold chain logistics market consists of both international logistics providers and domestic cold storage operators that maintain refrigerated warehouses, transportation fleets, and integrated temperature controlled distribution networks. Global logistics companies bring advanced monitoring technologies and international food and pharmaceutical supply chain expertise while local operators maintain strong domestic distribution infrastructure and regional cold storage capacity. Market competition is intensifying as companies invest in automated cold storage facilities, real time temperature monitoring platforms, and refrigerated trucking fleets to support expanding food distribution and pharmaceutical logistics demand.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Refrigerated Warehouse Capacity |

| Lineage Logistics | 2012 | United States | |||||

| Americold Logistics | 1903 | United States | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Germany | ~ | ~ | ~ | ~ | ~ |

| Royal Cargo Cold Chain | 1978 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Glacier Integrated Logistics | 2012 | Philippines | ~ | ~ | ~ | ~ | ~ |

Philippines Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Frozen Food Consumption and Supermarket Distribution Networks

Rapid expansion of modern grocery retail chains and food distribution networks across the Philippines significantly strengthens demand for cold chain logistics infrastructure capable of maintaining frozen food quality during storage and transportation. Large supermarket chains distribute extremely high volumes of frozen meat seafood dairy products and processed food items requiring reliable temperature controlled logistics systems connecting import terminals food processing plants and retail outlets. Food manufacturers increasingly depend on specialized cold chain logistics providers that operate refrigerated warehouses and distribution fleets capable of maintaining consistent temperature conditions across supply chains. Expanding urban populations and changing consumer lifestyles encourage higher consumption of packaged frozen foods which further increases logistics demand. Cold storage facilities located near major ports and food manufacturing zones therefore play a critical role in national food distribution infrastructure. Logistics providers invest heavily in refrigerated warehouse capacity and automated temperature monitoring systems designed to protect product freshness. Retail companies increasingly outsource cold storage operations to specialized logistics firms capable of managing inventory rotation and temperature compliance. Continuous growth in supermarket retail expansion and frozen food consumption therefore remains one of the most significant drivers strengthening the Philippines cold chain logistics industry.

Rising Pharmaceutical Imports and Temperature Sensitive Medical Supply Chains

The Philippines healthcare sector increasingly depends on temperature controlled logistics infrastructure to transport and store pharmaceutical products including vaccines biologic medicines insulin products and specialty therapeutics requiring strict storage conditions. Pharmaceutical distributors and healthcare providers rely heavily on validated cold chain systems capable of maintaining product stability throughout transportation and warehousing operations. Expanding national healthcare programs and pharmaceutical imports therefore increase demand for specialized temperature controlled transportation services connecting international cargo terminals with hospitals pharmacies and healthcare distributors. Logistics companies deploy refrigerated vehicles digital temperature monitoring sensors and automated alert systems that ensure pharmaceutical shipments remain within regulatory temperature thresholds during transit. Pharmaceutical manufacturers also require secure cold storage facilities capable of maintaining validated storage environments compliant with pharmaceutical distribution regulations. Increasing adoption of biologic medicines that require strict temperature management further strengthens cold chain logistics demand across healthcare supply chains. Healthcare distributors increasingly outsource cold storage operations to professional logistics providers capable of maintaining regulatory compliance. Continuous growth in pharmaceutical consumption therefore represents a major structural driver expanding the Philippines cold chain logistics market.

Market Challenges

Limited Cold Storage Infrastructure Outside Major Urban Logistics Hubs

Cold chain logistics development in the Philippines faces infrastructure limitations particularly outside major metropolitan regions where refrigerated warehouse capacity remains relatively limited. Many regional agricultural production zones and secondary cities lack sufficient temperature controlled storage facilities required to maintain product freshness during long distance distribution. Food producers and seafood exporters therefore encounter logistical constraints when transporting temperature sensitive products to major export terminals or urban retail markets. Insufficient cold storage infrastructure also increases the risk of food spoilage and supply chain inefficiencies during transportation across the archipelago. Logistics providers must coordinate complex distribution routes involving refrigerated trucks maritime shipping and regional warehouses to maintain product quality. Infrastructure investment in provincial cold storage facilities remains necessary to support agricultural supply chains and regional food distribution networks. Government agencies and logistics developers continue exploring opportunities to expand temperature controlled infrastructure near agricultural zones and regional ports. However infrastructure gaps outside major logistics hubs continue affecting the efficiency of national cold chain logistics operations.

High Capital Investment Requirements for Temperature Controlled Logistics Infrastructure

Establishing large scale cold chain logistics infrastructure requires significant capital investment due to the high cost of refrigerated warehouse construction specialized transportation equipment and advanced temperature monitoring technologies. Cold storage facilities must operate energy intensive refrigeration systems capable of maintaining precise temperature ranges necessary for food and pharmaceutical products. Logistics companies must also invest heavily in refrigerated truck fleets insulated containers and automated monitoring systems that ensure temperature stability throughout transportation operations. These capital intensive infrastructure requirements create high entry barriers for new logistics providers entering the cold chain industry. Energy consumption costs associated with refrigeration equipment also increase operational expenses for logistics operators maintaining large cold storage facilities. Companies therefore invest in energy efficient refrigeration systems and advanced monitoring technologies designed to improve operational efficiency and reduce electricity consumption. Despite these innovations the high cost of building and maintaining temperature controlled infrastructure remains a significant operational challenge across the Philippines cold chain logistics industry.

Opportunities

Expansion of Seafood Export Logistics and International Food Trade Networks

The Philippines seafood industry plays an important role in global food trade which creates significant opportunities for cold chain logistics providers supporting export oriented seafood supply chains. Large volumes of tuna shrimp and other marine products are exported from coastal production regions to international markets requiring strict temperature controlled transportation and storage infrastructure. Seafood exporters rely heavily on refrigerated warehouses blast freezing facilities and temperature controlled shipping containers that maintain product freshness during international transportation. Logistics providers therefore invest in cold storage facilities located near fishing ports and export processing zones that support seafood consolidation and packaging operations. International demand for high quality seafood products continues increasing particularly across Asian and North American markets which strengthens export logistics volumes. Cold chain operators also integrate digital temperature monitoring platforms capable of ensuring product compliance with international food safety standards. Expansion of seafood export logistics networks therefore creates long term opportunities for cold chain logistics investment across coastal regions and export corridors in the Philippines.

Development of Pharmaceutical Cold Chain Distribution for Healthcare Infrastructure Expansion

Rapid expansion of healthcare infrastructure across the Philippines significantly increases demand for specialized pharmaceutical cold chain distribution services capable of supporting hospitals clinics pharmacies and medical distributors nationwide. Pharmaceutical products including vaccines insulin biologic medicines and specialty therapeutics require validated temperature controlled supply chains throughout storage transportation and distribution processes. Healthcare providers increasingly depend on specialized logistics companies capable of maintaining strict temperature conditions and regulatory compliance across pharmaceutical supply chains. Logistics companies therefore invest in pharmaceutical grade cold storage warehouses refrigerated vehicles and digital monitoring technologies capable of tracking temperature conditions in real time. Government vaccination programs and pharmaceutical import volumes further increase demand for temperature controlled distribution networks connecting international airports with healthcare distribution centers. Pharmaceutical manufacturers and healthcare distributors increasingly outsource logistics operations to specialized cold chain providers. Expansion of pharmaceutical distribution infrastructure therefore presents major opportunities for investment and innovation within the Philippines cold chain logistics market.

Future Outlook

The Philippines cold chain logistics market is expected to expand steadily over the coming years as food distribution networks and healthcare supply chains continue strengthening across the country. Investments in automated cold storage warehouses, digital temperature monitoring systems, and energy efficient refrigeration technologies are expected to increase. Government infrastructure development supporting ports, highways, and airport logistics will improve national distribution efficiency. Growing demand for pharmaceutical cold chain distribution and frozen food logistics will further accelerate market expansion.

Major Players

- Lineage Logistics

- Americold Logistics

- DB Schenker

- DHL Supply Chain

- Kuehne + Nagel

- Royal Cargo Cold Chain

- Glacier Integrated Logistics

- Maersk Logistics

- Nippon Express

- DSV Global Transport and Logistics

- Yusen Logistics

- CEVA Logistics

- CJ Logistics

- Kerry Logistics

- Aboitiz InfraCapital Logistics

Key Target Audience

- Cold chainlogisticsoperators

- Food manufacturing and processing companies

- Seafood export companies

- Pharmaceutical distribution companies

- Retail supermarket chains

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying variables influencing cold chain logistics demand including frozen food consumption patterns pharmaceutical distribution volumes seafood exports and refrigerated warehouse capacity across the Philippines logistics infrastructure.

Step 2: Market Analysis and Construction

Quantitative and qualitative datasets are analyzed including logistics infrastructure statistics food supply chain records pharmaceutical distribution data and company financial disclosures to construct a comprehensive market framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry analysts supply chain managers cold storage operators and pharmaceutical logistics specialists are consulted to validate analytical assumptions regarding infrastructure capacity distribution networks and future industry demand.

Step 4: Research Synthesis and Final Output

All validated insights are consolidated into a structured analytical framework combining statistical datasets logistics infrastructure analysis and supply chain evaluations to produce the final comprehensive market research report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of pharmaceutical distribution requiring strict temperature controlled logistics infrastructure

Growing demand for frozen and processed food products across urban populations

Rising seafood exports requiring reliable refrigerated transportation and storage systems - Market Challenges

Limited cold storage infrastructure across secondary cities and rural production regions

High operational costs for refrigerated transport equipment and energy consumption

Logistics complexity due to the archipelagic geography requiring multimodal refrigerated transport - Market Opportunities

Development of modern cold storage facilities supporting food processing and pharmaceutical supply chains

Expansion of export oriented seafood and agricultural supply chains requiring cold chain logistics

Adoption of digital temperature monitoring and smart logistics management technologies - Trends

Integration of real time temperature monitoring and IoT enabled cold chain tracking systems

Investment in automated cold storage warehouses near major ports and urban distribution centers - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Temperature Controlled Warehousing

Refrigerated Transportation Services

Cold Storage Distribution Services

Pharmaceutical Cold Chain Logistics

Integrated Cold Chain Logistics Solutions - By Platform Type (In Value%)

Domestic Cold Chain Distribution Networks

International Cold Chain Logistics Networks

Pharmaceutical Logistics Platforms

Food Supply Chain Logistics Platforms - By Fitment Type (In Value%)

Dedicated Cold Chain Logistics Services

Shared Cold Storage and Transport Services

Contract Cold Chain Logistics Services

On Demand Refrigerated Transport Services - By End User Segment (In Value%)

Food and Beverage Producers and Distributors

Pharmaceutical and Healthcare Companies

Agriculture and Seafood Exporters

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Temperature Monitoring Technology, Geographic Distribution Network, Pharmaceutical Compliance Capability, Pricing Strategy, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Royal Cargo Logistics

2GO Group Inc.

DHL Supply Chain Philippines

Kuehne + Nagel Philippines

DB Schenker Philippines

Yusen Logistics Philippines

Nippon Express Philippines

Maersk Logistics Philippines

Fast Logistics Group

Glacier Integrated Logistics

Mets Logistics Inc.

Cold Storage Philippines

Airspeed International Corporation

CEVA Logistics Philippines

FedEx Philippines

- Food producers and retailers rely on cold chain providers to maintain product freshness and reduce spoilage during distribution

- Pharmaceutical companies require validated temperature controlled logistics for vaccines biologics and specialty medicines

- Seafood exporters depend on refrigerated logistics infrastructure to maintain product quality during international shipments

- Food service companies use cold chain logistics to support nationwide distribution of frozen and chilled products

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now