Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Collision Avoidance Systems market is valued at approximately USD ~ billion based on a recent historical assessment, driven by rising vehicle safety regulations, increasing automotive production, and growing adoption of advanced driver assistance systems. Demand is supported by urban congestion, higher accident rates, and consumer awareness of safety technologies. Technological advancements in radar, LiDAR, and AI-based sensing systems further contribute to adoption, particularly in passenger and commercial vehicles across expanding urban centers.

Metro Manila, Cebu, and Davao dominate the Philippines Collision Avoidance Systems market due to higher vehicle density, developed road infrastructure, and stronger enforcement of automotive safety regulations. These regions benefit from greater availability of technologically advanced vehicles and higher consumer purchasing power. Additionally, logistics hubs and commercial fleets concentrated in these cities drive demand for collision avoidance systems to reduce operational risks and improve fleet efficiency under increasing urban traffic complexities.

Market Segmentation

By System Type

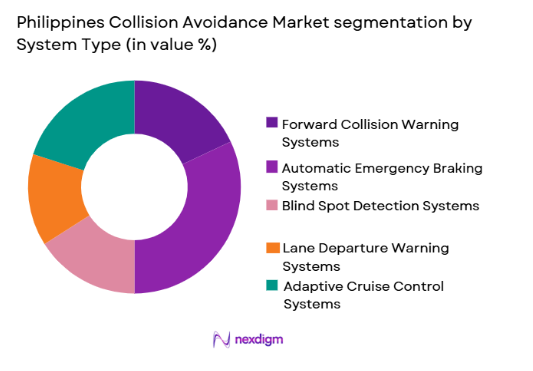

Philippines Collision Avoidance Systems market is segmented by system type into Forward Collision Warning Systems, Automatic Emergency Braking Systems, Blind Spot Detection Systems, Lane Departure Warning Systems, and Adaptive Cruise Control Systems. Recently, Automatic Emergency Braking Systems has a dominant market share due to strong regulatory push, integration in mid-range vehicles, and proven effectiveness in reducing accident severity. OEMs increasingly bundle AEB with standard safety packages, while fleet operators adopt it to reduce insurance costs and operational risks in congested urban environments.

By Product Type

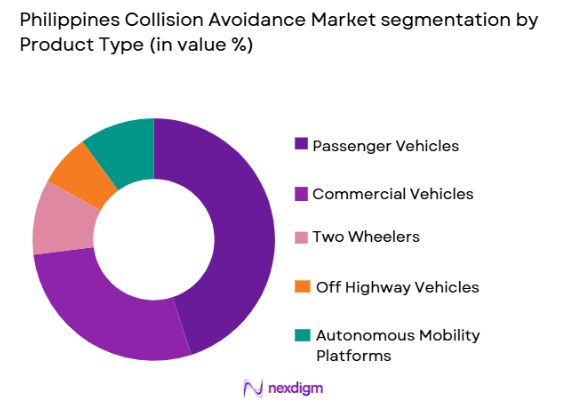

Philippines Collision Avoidance Systems market is segmented by product type into Passenger Vehicles, Commercial Vehicles, Two Wheelers, Off Highway Vehicles, and Autonomous Mobility Platforms. Recently, Passenger Vehicles has a dominant market share due to increasing private vehicle ownership, growing middle-class income, and rising demand for safety features. Automotive manufacturers are prioritizing ADAS integration in passenger cars, supported by urban consumer awareness and dealership-led promotion of advanced safety technologies.

Competitive Landscape

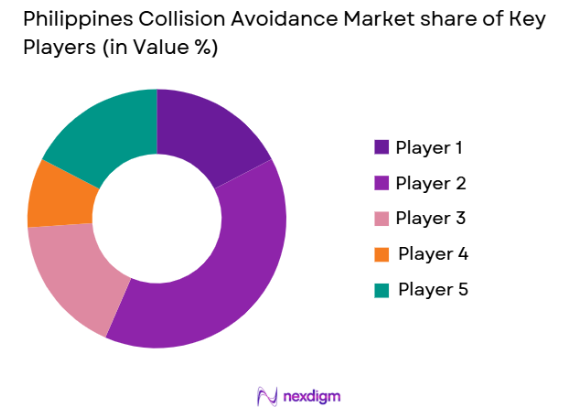

The Philippines Collision Avoidance Systems market is moderately consolidated, with global automotive technology providers dominating through OEM partnerships and strong technological capabilities. Major players leverage advanced sensor technologies, AI integration, and economies of scale to maintain competitive positioning. Regional distribution networks and aftermarket expansion strategies further strengthen their market presence, while local players focus on integration and cost-effective solutions to capture emerging demand.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Integration Capability |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Robert Bosch GmbH | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| Valeo SA | 1923 | France | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

Philippines Collision Avoidance Systems Market Analysis

Growth Drivers

Increasing Government Safety Regulations and Mandates

The Philippines automotive sector is witnessing a steady rise in regulatory interventions aimed at improving road safety, which directly accelerates the adoption of collision avoidance systems. Government initiatives focusing on reducing road fatalities are encouraging automakers to integrate advanced driver assistance systems into vehicles. Regulatory frameworks are increasingly aligning with global safety standards, pushing OEMs to include features such as automatic emergency braking and lane departure warning systems. These policies create a strong compliance-driven demand for safety technologies across both passenger and commercial vehicle segments. Additionally, stricter vehicle inspection norms and safety certifications further reinforce system integration. Public awareness campaigns around accident prevention also influence consumer behavior, increasing preference for vehicles equipped with advanced safety features. Insurance companies are offering incentives for vehicles with such technologies, creating additional motivation for adoption. The combined impact of regulatory enforcement, consumer awareness, and industry compliance is significantly driving the growth of collision avoidance systems across urban and semi-urban regions.

Rapid Urbanization and Rising Traffic Congestion

Urbanization in key Philippine cities is intensifying traffic density, which increases the likelihood of road accidents and creates a strong need for advanced safety technologies. As vehicle ownership rises in metropolitan areas, congestion becomes a major challenge, leading to frequent low-speed collisions and traffic incidents. Collision avoidance systems provide real-time monitoring and automated intervention, making them essential in densely populated urban environments. Fleet operators, including logistics and ride-hailing services, are adopting these systems to improve safety and operational efficiency. Increased commuting times and complex road conditions further highlight the importance of driver assistance technologies. Consumers are becoming more inclined toward vehicles that offer enhanced safety features to navigate crowded roads. Infrastructure development, including smart traffic systems, is also supporting the integration of advanced vehicle technologies. The interaction between urban expansion, mobility demands, and safety requirements is significantly boosting the adoption of collision avoidance systems across multiple vehicle categories.

Market Challenges

High Cost of Advanced Safety Technologies

One of the major barriers to the widespread adoption of collision avoidance systems in the Philippines is the high cost associated with advanced safety technologies. These systems rely on sophisticated components such as radar sensors, LiDAR, cameras, and AI-driven processing units, which significantly increase vehicle production costs. As a result, these features are often limited to mid-range and premium vehicles, restricting accessibility for price-sensitive consumers. The cost challenge is further amplified by import dependencies for key components, leading to higher retail prices. Local manufacturing capabilities for advanced automotive electronics remain limited, increasing reliance on international suppliers. This creates pricing volatility and affects affordability in the domestic market. Additionally, aftermarket installation costs for these systems can be prohibitive, limiting adoption among existing vehicle owners. Consumers in emerging markets often prioritize price over advanced features, slowing penetration rates. The balance between cost efficiency and technological advancement remains a critical challenge for market expansion.

Limited Infrastructure and Technological Integration Barriers

The effectiveness of collision avoidance systems depends heavily on supporting infrastructure and seamless integration with vehicle platforms, which remains a challenge in the Philippines. Road conditions, inconsistent lane markings, and lack of standardized traffic management systems can limit the performance of advanced driver assistance technologies. These systems require accurate environmental sensing, which can be affected by poor infrastructure quality. Additionally, integration with older vehicle models poses technical difficulties, reducing the potential for widespread adoption. Limited availability of skilled technicians for installation and maintenance further complicates deployment. Connectivity challenges, including inconsistent network coverage, impact the performance of connected vehicle systems. Regulatory gaps in standardizing technology implementation also create uncertainties for manufacturers. The absence of robust testing and validation ecosystems for advanced automotive technologies slows innovation. These infrastructure and integration barriers collectively hinder the scalability of collision avoidance systems in the domestic market.

Opportunities

Expansion of Electric and Smart Vehicle Ecosystems

The growing adoption of electric vehicles and smart mobility solutions in the Philippines presents a significant opportunity for collision avoidance systems. Electric vehicles are typically equipped with advanced electronic architectures, making them ideal platforms for integrating safety technologies. Government incentives for EV adoption and sustainable transportation are accelerating market growth. Manufacturers are increasingly incorporating ADAS features as standard offerings in electric vehicles to enhance safety and competitiveness. Smart city initiatives are also promoting the development of intelligent transport systems, which complement collision avoidance technologies. The integration of connected vehicle ecosystems allows real-time data exchange, improving system efficiency and responsiveness. Consumers are showing increased interest in technologically advanced vehicles, further supporting adoption. Fleet electrification trends in logistics and public transportation sectors also create demand for advanced safety systems. The convergence of electrification, connectivity, and automation is expected to significantly expand market opportunities.

Growth of Aftermarket Installation and Retrofit Solutions

The large base of existing vehicles in the Philippines provides a substantial opportunity for aftermarket collision avoidance system installations. Many vehicles on the road lack advanced safety features, creating demand for retrofit solutions that enhance driver safety. Aftermarket providers are developing cost-effective and modular systems that can be integrated into older vehicles. This segment is gaining traction among fleet operators seeking to upgrade safety without replacing vehicles. Technological advancements are enabling easier installation and compatibility with a wider range of vehicle models. Increasing awareness about road safety and insurance benefits is driving consumer interest in retrofit solutions. E-commerce platforms are facilitating access to aftermarket products, expanding market reach. Service providers are also offering bundled solutions, including installation and maintenance, to attract customers. The aftermarket segment represents a scalable and high-growth opportunity within the collision avoidance systems market.

Future Outlook

The Philippines Collision Avoidance Systems market is expected to witness steady expansion driven by regulatory support, increasing urban mobility demands, and technological advancements in automotive safety systems. Integration of AI, sensor fusion, and connected vehicle technologies will enhance system capabilities. Growing adoption of electric vehicles and smart transportation infrastructure will further support demand. Additionally, rising consumer awareness and fleet modernization initiatives will contribute to sustained market growth over the next five years.

Major Players

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Valeo SA

- ZF Friedrichshafen AG

- Autoliv Inc

- Aptiv PLC

- Magna International Inc

- Mobileye Global Inc

- Hyundai Mobis

- Hitachi Astemo Ltd

- Veoneer Inc

- Texas Instruments Automotive

- NXP Semiconductors Automotive

- Infineon Technologies Automotive

Key Target Audience

- Automotive OEMs

- Fleet Operators

- Logistics Companies

- Ride Hailing Platforms

- Government and Regulatory Bodies

- Insurance Companies

- Automotive Component Manufacturers

- Investment and Venture Capitalist Firms

Research Methodology

Step 1: Identification of Key Variables

Market variables including vehicle production, safety regulations, consumer adoption patterns, and technology penetration were identified. These variables were validated through industry reports, government publications, and automotive data sources to ensure relevance and accuracy.

Step 2: Market Analysis and Construction

A structured analytical framework was used to map market dynamics, segmentation, and competitive landscape. Historical data and current industry trends were combined to construct a comprehensive view of the market structure.

Step 3: Hypothesis Validation and Expert Consultation

Initial findings were validated through expert consultations with industry stakeholders, including automotive manufacturers and technology providers. Feedback was incorporated to refine assumptions and improve analytical precision.

Step 4: Research Synthesis and Final Output

All validated insights were synthesized into a structured report, ensuring consistency across sections. Final outputs were aligned with market realities and supported by credible data sources to maintain reliability.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising road safety awareness and accident reduction initiatives

Government mandates on advanced driver assistance systems

Growth in vehicle ownership and urban traffic congestion

Technological advancements in sensor and AI integration

Expansion of fleet management and logistics sectors - Market Challenges

High cost of advanced safety systems for mass adoption

Limited infrastructure for autonomous system integration

Low consumer awareness in rural and semi urban regions

Complex integration with legacy vehicle platforms

Dependence on imported components and technologies - Market Opportunities

Increasing adoption of electric and smart vehicles

Expansion of ride sharing and mobility as a service platforms

Growth in aftermarket safety system installations - Trends

Integration of AI driven predictive collision systems

Shift toward sensor fusion and multi sensor architectures

Adoption of semi autonomous driving technologies

Expansion of connected vehicle ecosystems

Growing demand for real time driver assistance analytics - Government Regulations & Defense Policy

Implementation of vehicle safety compliance standards

Incentives for advanced automotive technologies adoption

Integration of intelligent transport systems in urban planning - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Forward Collision Warning Systems

Automatic Emergency Braking Systems

Blind Spot Detection Systems

Lane Departure Warning Systems

Adaptive Cruise Control Systems - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Two Wheelers

Off Highway Vehicles

Autonomous Mobility Platforms - By Fitment Type (In Value%)

OEM Installed Systems

Aftermarket Retrofits

Integrated Vehicle Platforms

Modular Plug and Play Systems

Fleet Integrated Solutions - By End User Segment (In Value%)

Private Vehicle Owners

Commercial Fleet Operators

Public Transportation Agencies

Logistics and Delivery Companies

Government and Defense Authorities - By Procurement Channel (In Value%)

Direct OEM Procurement

Authorized Dealership Networks

Online Automotive Platforms

Fleet Procurement Contracts

Third Party Distributors - By Material / Technology (in Value %)

Radar Based Systems

Camera Based Systems

LiDAR Based Systems

Ultrasonic Sensor Systems

Sensor Fusion Technologies

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Technology Capability, Product Portfolio, Pricing Strategy, Regional Presence, OEM Partnerships, Innovation Index, Aftermarket Presence, System Integration Capability, Regulatory Compliance, Customer Support Strength)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Continental AG

Robert Bosch GmbH

Denso Corporation

Valeo SA

ZF Friedrichshafen AG

Autoliv Inc

Aptiv PLC

Magna International Inc

Mobileye Global Inc

Hyundai Mobis

Hitachi Astemo Ltd

Veoneer Inc

Texas Instruments Automotive

NXP Semiconductors Automotive

Infineon Technologies Automotive

- Increasing preference for safety features among private vehicle buyers

- Fleet operators focusing on accident reduction and cost savings

- Public transportation agencies adopting safety technologies for compliance

- Government agencies promoting smart mobility and road safety programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now