Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines CVT transmissions market is valued at approximately USD ~ billion based on a recent historical assessment, driven by increasing demand for automatic transmission vehicles in urban areas. Rising fuel efficiency standards, growing adoption of compact passenger vehicles, and expanding ride-hailing services contribute significantly to market growth. Automotive manufacturers are integrating CVT systems to enhance driving comfort and efficiency, while technological advancements in belt-driven and electronic CVT systems further support sustained demand across various vehicle categories.

Metro Manila, Cebu, and Davao emerge as dominant regions in the Philippines CVT transmissions market due to high vehicle density, urban congestion, and rising disposable incomes. These cities demonstrate strong demand for automatic vehicles as consumers prioritize convenience and fuel efficiency. Additionally, proximity to automotive dealerships, service infrastructure, and import hubs supports faster adoption of CVT-equipped vehicles. The presence of multinational automotive brands and established distribution networks further strengthens market penetration in these urban centers.

Market Segmentation

By System Type

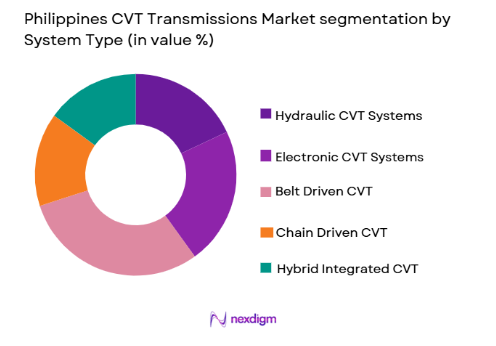

Philippines CVT Transmissions market is segmented by system type into hydraulic CVT systems, electronic CVT systems, belt driven CVT, chain driven CVT, and hybrid integrated CVT. Recently, belt driven CVT has a dominant market share due to its cost efficiency, widespread adoption in passenger vehicles, and compatibility with compact engines. Its lower manufacturing complexity and better fuel efficiency make it preferred among OEMs and consumers, particularly in urban markets where smooth driving performance and affordability are key considerations.

By Platform Type

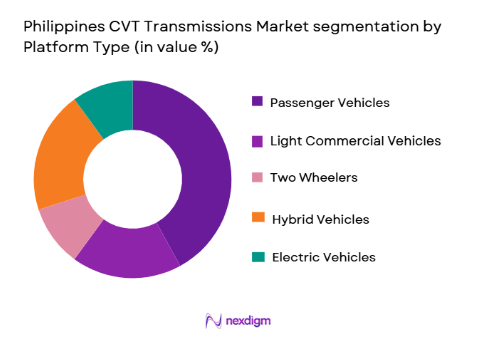

Philippines CVT Transmissions market is segmented by platform type into passenger vehicles, light commercial vehicles, two wheelers, hybrid vehicles, and electric vehicles. Recently, passenger vehicles have a dominant market share due to rising urbanization, increased consumer preference for automatic cars, and growing affordability of compact vehicles. Passenger vehicles benefit from strong dealership networks and financing options, making them the primary segment for CVT adoption in the country’s evolving automotive landscape.

Competitive Landscape

The Philippines CVT transmissions market exhibits moderate consolidation with a mix of global automotive OEMs and transmission technology providers influencing market dynamics. Established players dominate through strong distribution networks, technological expertise, and long-term OEM partnerships, while regional suppliers compete through cost optimization and aftermarket services. Continuous investments in transmission efficiency, hybrid integration, and localized production strategies further intensify competition and drive innovation across the value chain.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Transmission Integration Capability |

| Toyota Motor Philippines Corporation | 1988 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Motors Philippines | 1963 | Japan | ~ | ~ | ~ | ~ | ~ |

| Honda Cars Philippines | 1990 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Nissan Philippines | 1958 | Japan | ~ | ~ | ~ | ~ | ~ |

| Aisin Corporation | 1965 | Japan | ~ | ~ | ~ | ~ | ~ |

Philippines CVT Transmissions Market Analysis

Growth Drivers

Rising Urban Demand for Automatic Vehicles:

Increasing urban congestion and changing consumer preferences toward convenience are significantly driving the adoption of CVT transmissions in the Philippines automotive market. Consumers in metropolitan areas prefer smoother driving experiences, especially in stop-and-go traffic conditions, which enhances the appeal of CVT-equipped vehicles. The rising number of first-time car buyers is also contributing to demand, as automatic vehicles are easier to operate and require less driving skill. Automotive manufacturers are responding by expanding their CVT-equipped model portfolios across entry-level and mid-range vehicles. Additionally, improved financing options and competitive pricing strategies are making CVT vehicles more accessible to a wider consumer base. Ride-hailing services and shared mobility platforms are also accelerating demand, as operators prefer fuel-efficient and low-maintenance transmission systems. The increasing availability of service centers capable of handling CVT systems further supports adoption. Technological advancements in CVT durability and performance are reducing earlier concerns about reliability. As urbanization continues to expand, the demand for automatic transmissions is expected to remain strong.

Integration with Hybrid Vehicle Platforms:

The growing adoption of hybrid vehicles in the Philippines is creating significant demand for CVT transmissions due to their compatibility with hybrid powertrains. CVT systems offer seamless power delivery and improved fuel efficiency, which aligns well with the operational requirements of hybrid vehicles. Automotive OEMs are increasingly integrating CVT systems into hybrid models to optimize performance and emissions compliance. Government initiatives promoting fuel-efficient and low-emission vehicles are further supporting this trend. Consumers are also becoming more environmentally conscious, driving demand for hybrid vehicles equipped with advanced transmission technologies. CVT systems enable better energy utilization, making them a preferred choice for hybrid applications. Additionally, advancements in electronic control systems are enhancing the efficiency of CVT integration with electric motors. The expansion of hybrid vehicle offerings by major automotive brands is strengthening the market for CVT transmissions. Increasing investments in sustainable mobility solutions are expected to further accelerate this trend. As hybrid vehicle adoption grows, CVT systems will continue to play a critical role in the market.

Market Challenges

High Maintenance and Repair Costs:

The Philippines CVT transmissions market faces challenges related to higher maintenance and repair costs compared to traditional manual and automatic transmissions. CVT systems require specialized components such as belts, pulleys, and electronic control units, which can be expensive to repair or replace. Limited availability of skilled technicians capable of handling CVT systems further increases servicing costs. Consumers often perceive CVT vehicles as costly to maintain, which can impact purchasing decisions. Additionally, the need for regular transmission fluid replacement adds to long-term ownership expenses. Independent repair shops may lack the necessary equipment and expertise, forcing consumers to rely on authorized service centers. This dependency can lead to higher service charges and longer repair times. Concerns regarding durability under heavy load conditions also contribute to hesitancy among certain consumer segments. The absence of widespread awareness about proper CVT maintenance practices further exacerbates the issue. Addressing these challenges is critical for improving consumer confidence and expanding market adoption.

Dependence on Imported Transmission Components:

The Philippines CVT transmissions market is highly dependent on imported components, which exposes the industry to supply chain disruptions and cost fluctuations. Most advanced CVT systems and components are manufactured in countries such as Japan and Thailand, making local production limited. Currency fluctuations and import duties can increase the overall cost of CVT-equipped vehicles. Delays in component supply can also impact production timelines for automotive manufacturers operating in the region. The lack of domestic manufacturing capabilities restricts the development of a localized supply chain. This dependence reduces the flexibility of OEMs in managing production costs and inventory. Additionally, geopolitical factors and trade policies can influence the availability of critical components. Limited local research and development activities further constrain innovation within the domestic market. Efforts to establish local manufacturing facilities are still in early stages and require significant investment. Reducing reliance on imports remains a key challenge for long-term market sustainability.

Opportunities

Expansion of Localized Manufacturing Capabilities:

The development of localized manufacturing facilities for CVT components presents a significant opportunity for the Philippines market. Establishing domestic production can reduce dependence on imports and improve supply chain resilience. Local manufacturing enables cost optimization through reduced transportation and import duties. It also creates opportunities for technology transfer and skill development within the local workforce. Automotive OEMs are increasingly exploring partnerships with local suppliers to establish production bases. Government incentives supporting industrial development and manufacturing investments further enhance this opportunity. Local production can also lead to faster turnaround times and improved inventory management. Additionally, it allows companies to customize products based on regional demand patterns. The growth of the domestic automotive sector provides a strong foundation for manufacturing expansion. As investments in infrastructure and industrial capabilities increase, localized production is expected to gain momentum. This shift can significantly enhance the competitiveness of the Philippines CVT transmissions market.

Growth in Aftermarket Replacement Demand:

The increasing number of CVT-equipped vehicles on the road is creating strong demand for aftermarket replacement parts and services. As vehicles age, the need for maintenance and component replacement rises, driving growth in the aftermarket segment. Independent service providers are expanding their capabilities to cater to CVT systems, creating new business opportunities. Consumers are seeking cost-effective alternatives to authorized service centers, which supports the growth of aftermarket suppliers. The availability of compatible and high-quality replacement components is improving market accessibility. Additionally, e-commerce platforms are facilitating the distribution of aftermarket CVT parts across the country. The expansion of logistics and delivery networks further enhances market reach. Training programs for technicians are also increasing, improving service quality in the aftermarket segment. The growing awareness of preventive maintenance is encouraging consumers to invest in timely servicing. This trend is expected to sustain long-term growth in the aftermarket ecosystem.

Future Outlook

The Philippines CVT transmissions market is expected to witness steady growth over the next five years driven by increasing adoption of automatic and hybrid vehicles. Technological advancements in transmission efficiency and durability will enhance product appeal. Regulatory support for fuel efficiency and low-emission vehicles will further accelerate demand. Expansion of urban mobility solutions and aftermarket services will also contribute to sustained market development.

Major Players

- Toyota Motor Philippines Corporation

- Mitsubishi Motors Philippines Corporation

- Honda Cars Philippines Inc

- Nissan Philippines Inc

- Suzuki Philippines Inc

- Hyundai Motor Philippines Inc

- Ford Motor Company Philippines

- Aisin Corporation

- Jatco Ltd

- Bosch Philippines

- ZF Friedrichshafen AG

- Schaeffler Group

- Magna International Inc

- Continental AG

- BorgWarner Inc

Key Target Audience

- Automotive OEM manufacturers

- Transmission system suppliers

- Aftermarket service providers

- Automotive component distributors

- Fleet management companies

- Ride hailing service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Primary and secondary research sources were used to identify critical variables influencing the Philippines CVT transmissions market, including demand drivers, supply chain dynamics, and technology trends. Data points were validated across multiple industry databases.

Step 2: Market Analysis and Construction

Market models were constructed using historical data, industry benchmarks, and macroeconomic indicators to estimate market size and segmentation. Analytical frameworks ensured consistency and accuracy in market projections.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through expert interviews with industry professionals, OEM representatives, and supply chain stakeholders. Feedback was incorporated to refine assumptions and ensure reliability of insights.

Step 4: Research Synthesis and Final Output

All validated data and insights were synthesized into a structured report, ensuring clarity, accuracy, and actionable intelligence for stakeholders operating in the Philippines CVT transmissions market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for fuel efficient automatic transmissions in urban mobility

Increasing adoption of compact and mid size passenger vehicles

Expansion of ride hailing and shared mobility services

Technological advancements in CVT efficiency and durability

Growth in hybrid vehicle integration requiring CVT systems - Market Challenges

Higher maintenance costs compared to manual transmissions

Limited consumer awareness regarding CVT reliability

Dependence on imported components and technologies

Technical limitations in high torque applications

Availability of skilled technicians for CVT servicing - Market Opportunities

Expansion of hybrid and electric vehicle compatible CVT systems

Localization of CVT component manufacturing in Southeast Asia

Growth in aftermarket replacement demand for aging vehicle fleets - Trends

Shift toward electronically controlled CVT systems

Integration of lightweight materials to improve efficiency

Rising preference for smooth driving experience in urban areas

Increasing partnerships between OEMs and transmission suppliers

Development of CVT systems for electric and hybrid platforms - Government Regulations & Defense Policy

Implementation of fuel efficiency standards encouraging CVT adoption

Import regulations impacting automotive component supply chains

Policies promoting hybrid and low emission vehicle technologies - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Hydraulic CVT Systems

Electronic CVT Systems

Chain Driven CVT

Belt Driven CVT

Hybrid Integrated CVT - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Two Wheelers

Hybrid Vehicles

Electric Vehicles - By Fitment Type (In Value%)

OEM Installed Systems

Aftermarket Replacement Units

Retrofit Installations

Performance Upgrade Systems

Fleet Integrated Systems - By EndUser Segment (In Value%)

Individual Vehicle Owners

Commercial Fleet Operators

Ride Hailing Service Providers

Logistics and Delivery Companies

Automotive Dealers and Service Centers - By Procurement Channel (In Value%)

Direct OEM Procurement

Authorized Dealership Networks

Independent Aftermarket Suppliers

Online Automotive Platforms

Third Party Distributors - By Material / Technology (in Value %)

Steel Belt Technology

Composite Belt Systems

Advanced Hydraulic Systems

Electronic Control Units Integration

Lightweight Alloy Components

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Diversity, Pricing Strategy, Technological Innovation, Distribution Network Strength, Aftermarket Presence, OEM Partnerships, Production Capacity, Regional Footprint, R&D Investment, Service Capabilities)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Toyota Motor Philippines Corporation

Mitsubishi Motors Philippines Corporation

Honda Cars Philippines Inc

Nissan Philippines Inc

Suzuki Philippines Inc

Hyundai Motor Philippines Inc

Ford Motor Company Philippines

Aisin Corporation

Jatco Ltd

Bosch Philippines

ZF Friedrichshafen AG

Schaeffler Group

Magna International Inc

Continental AG

BorgWarner Inc

- Growing preference for automatic transmissions among urban consumers

- Fleet operators prioritizing fuel efficiency and lower operating costs

- Ride hailing companies demanding smoother transmission technologies

- Service centers expanding capabilities for CVT maintenance and repair

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now