Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Diagnostic Labs market is witnessing rapid growth, driven by increasing healthcare investments, a rise in chronic diseases, and advancements in diagnostic technologies. The market size has expanded significantly due to an increase in government healthcare spending and the adoption of automated diagnostic solutions. Recent data reveals that the market is valued at USD ~ billion in 2024, a reflection of both domestic and international demand for advanced diagnostic services. This demand is also supported by the adoption of more efficient testing technologies across the healthcare sector.

Dominant regions within the Philippines, such as Metro Manila, Cebu, and Davao, play a crucial role in driving the demand for diagnostic services. Metro Manila is the epicenter due to its advanced healthcare infrastructure and population density, which contributes to a higher number of diagnostic procedures. Cebu and Davao, known for their regional healthcare centers, have also seen increasing investments to cater to the growing demand for diagnostic labs, thus fostering their dominance in the market.

Market Segmentation

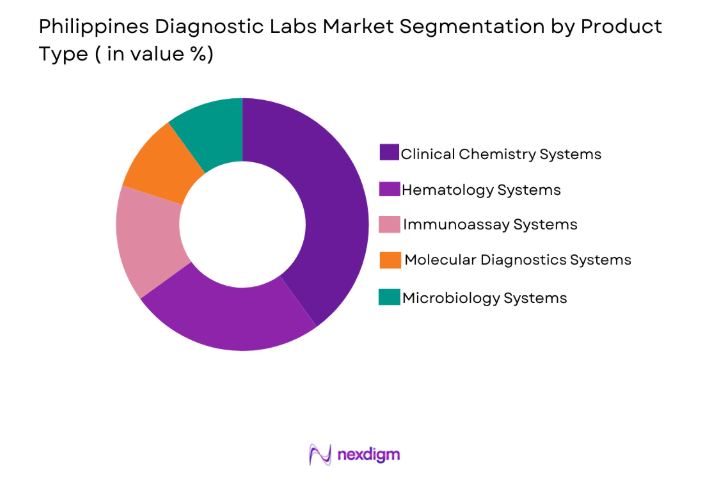

By Product Type

The Philippines Diagnostic Labs market is segmented by product type into clinical chemistry systems, hematology systems, immunoassay systems, molecular diagnostics systems, and microbiology systems. Recently, clinical chemistry systems have dominated the market share due to their widespread use in various medical conditions and their central role in routine diagnostics. The strong demand for automated testing systems in hospitals and diagnostic centers has contributed to the market leadership of clinical chemistry systems. This segment continues to experience growth driven by technological advancements, such as real-time data processing and increased accuracy, which make clinical chemistry systems an essential part of modern diagnostic labs.

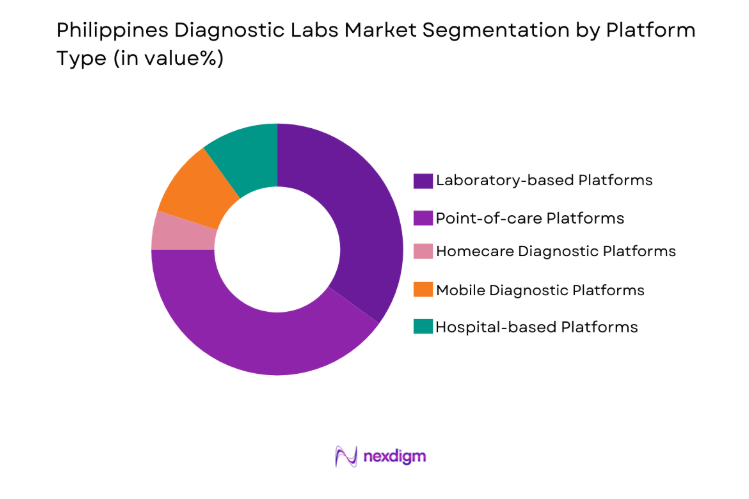

By Platform Type

The market is segmented by platform type into laboratory-based platforms, point-of-care platforms, homecare diagnostic platforms, mobile diagnostic platforms, and hospital-based platforms. Point-of-care platforms currently hold the largest market share due to their convenience and increasing usage in urgent care situations and home testing environments. The trend toward decentralization of healthcare, especially in rural areas, has boosted the demand for point-of-care solutions, which enable immediate results without the need for specialized lab facilities. This market shift towards rapid diagnostics is driven by growing healthcare needs in both urban and rural settings.

Competitive Landscape

The competitive landscape of the Philippines Diagnostic Labs market is shaped by the presence of both local and international players who contribute significantly to market consolidation. Leading companies in the market focus on expanding their service offerings, enhancing diagnostic accuracy, and ensuring faster results to meet the increasing healthcare demands. The market is also witnessing partnerships and collaborations to improve the infrastructure for diagnostic services, particularly in underserved areas.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | R&D Investment |

| Philippine Diagnostic Laboratories | 1985 | Manila | ~ | ~ | ~ | ~ | ~ |

| MedTech Diagnostics | 2000 | Quezon City | ~ | ~ | ~ | ~ | ~ |

| BioMed Laboratories | 1995 | Makati | ~ | ~ | ~ | ~ | ~~ |

| Health Metrics | 2005 | Manila | ~ | ~ | ~ | ~ | ~ |

| Quest Diagnostics | 1967 | USA | ~ | ~ | ~ | ~ | ~ |

Philippines Diagnostic Labs Market Analysis

Growth Drivers

Increased Healthcare Investment

Increased healthcare investment in the Philippines is a major driver for the growth of the diagnostic labs market. This trend reflects the government’s push for better healthcare infrastructure, including modern diagnostic facilities. The country’s healthcare budget has expanded significantly, enabling the establishment of more advanced diagnostic centers, especially in urban areas. As healthcare financing becomes more robust, the accessibility of diagnostic services across various regions improves, especially with the deployment of advanced technologies. Furthermore, increased investments in laboratory equipment and digital platforms lead to better diagnostic capabilities, ensuring faster and more accurate results, further driving market growth. The integration of artificial intelligence and automation in diagnostic labs is another key factor contributing to this development. With these improvements, diagnostics are now more reliable, and turnaround times for test results have been reduced.

Technological Advancements in Diagnostics

Technological advancements are a key growth driver in the diagnostic labs market in the Philippines. The adoption of automated and digital diagnostic tools, such as artificial intelligence and machine learning, has significantly enhanced the accuracy and speed of diagnostic testing. This technological shift allows diagnostic labs to handle larger volumes of tests while reducing human error and improving overall efficiency. The growth of molecular diagnostics, in particular, is evident, as these tools provide more accurate results for complex medical conditions. As healthcare providers continue to adopt these innovations, the demand for high-tech diagnostic tools increases. Moreover, government initiatives supporting digital health are encouraging the widespread use of these technologies, which is expected to drive further growth in the market.

Market Challenges

High Operational Costs

One of the significant challenges facing the Philippines diagnostic labs market is the high operational costs associated with maintaining state-of-the-art facilities. Diagnostic labs require substantial investments in equipment, software, and skilled personnel to operate effectively. Despite increasing demand for diagnostic services, many labs struggle to maintain profitability due to high capital expenditure on diagnostic machines, laboratory infrastructure, and recurring maintenance costs. The upfront cost of advanced diagnostic machines like molecular analyzers and automated testing equipment is particularly high, placing a financial burden on smaller diagnostic labs that cannot afford the latest technologies. These financial challenges have resulted in slower adoption rates for newer, more expensive diagnostic platforms, limiting overall market expansion in certain regions.

Regulatory and Compliance Challenges

Regulatory challenges are another significant obstacle in the Philippines diagnostic labs market. While the government has introduced various initiatives to support healthcare, including diagnostic services, navigating the regulatory landscape can be complex. Diagnostic labs must comply with strict standards set by the Department of Health and other regulatory bodies to ensure the safety and quality of their services. Additionally, the approval process for new diagnostic technologies can be slow and cumbersome, further hindering innovation and delaying the introduction of new solutions. Non-compliance with regulatory standards can lead to penalties and closures, affecting market stability.

Opportunities

Expansion of Diagnostic Services in Rural Areas

One of the key opportunities in the Philippines diagnostic labs market lies in expanding diagnostic services to underserved rural areas. The government’s healthcare initiatives have already begun to address this gap, with significant investments being made to improve healthcare accessibility in remote regions. As the demand for diagnostic services continues to rise, expanding access to these services through mobile and decentralized diagnostic solutions presents a significant market opportunity. Rural areas, which previously lacked access to diagnostic testing, are now seeing the introduction of mobile diagnostic units, telemedicine platforms, and local diagnostic labs. This expansion helps cater to the growing demand for medical testing while providing improved healthcare outcomes for rural populations.

Telemedicine Integration with Diagnostic Labs

Another opportunity lies in the integration of telemedicine platforms with diagnostic labs, which enhances accessibility and convenience for patients. With the rise of telemedicine, patients can now consult with healthcare professionals remotely, reducing wait times and improving access to services. By linking telemedicine platforms with diagnostic labs, patients can receive consultations and immediately have tests ordered, all within the comfort of their own homes. This integration provides a streamlined patient experience and opens new revenue streams for diagnostic labs. As the Philippines healthcare system becomes more digitalized, the telemedicine market continues to expand, presenting an exciting opportunity for diagnostic labs to capitalize on this trend.

Future Outlook

The Philippines Diagnostic Labs market is poised for continued growth over the next five years, driven by an expanding healthcare infrastructure and advancements in diagnostic technology. Technological innovations such as artificial intelligence and automation will further enhance diagnostic accuracy and turnaround times. Government support for healthcare services, combined with the growing demand for preventive healthcare, will drive the expansion of diagnostic labs in both urban and rural areas. As the market evolves, increased digitalization and telemedicine integration will redefine patient care and diagnostic service delivery.

Major Players

- Philippine Diagnostic Laboratories

- MedTech Diagnostics

- BioMed Laboratories

- Health Metrics

- Quest Diagnostics

- Labworks Philippines

- MediScan Laboratories

- LifeLabs Philippines

- Carewell Diagnostics

- MediPlus Healthcare

- Unilab Diagnostics

- EastMed Diagnostics

- MedTox Diagnostics

- Pathway Labs

- Philippine HealthTech

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers and professionals

- Hospital networks

- Diagnostic service providers

- Medical technology developers

- Private health insurers

Research Methodology

Step 1: Identification of Key Variables

Key variables affecting the diagnostic labs market are identified through a detailed review of market dynamics, trends, and emerging technologies.

Step 2: Market Analysis and Construction

Data from primary and secondary research is used to construct a comprehensive market model based on historical and current trends.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations are conducted to validate the research hypotheses and ensure the reliability of the market model.

Step 4: Research Synthesis and Final Output

The final market analysis report is synthesized and structured, ensuring clarity and actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising Healthcare Infrastructure Investments

Increasing Prevalence of Chronic Diseases

Advancements in Diagnostic Technologies - Market Challenges

High Operational Costs of Diagnostic Labs

Limited Access to Rural Areas

Regulatory Barriers in Diagnostic Equipment Approval - Market Opportunities

Expanding Health Insurance Coverage

Growth in Preventive Healthcare Diagnostics

Telemedicine Integration with Diagnostic Services - Trends

Shift Toward Automation in Diagnostic Labs

Growing Adoption of AI for Diagnostics - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Systems

Hematology Systems

Immunoassay Systems

Molecular Diagnostics Systems

Microbiology Systems - By Platform Type (In Value%)

Laboratory-based Platforms

Point-of-care Platforms

Homecare Diagnostic Platforms

Mobile Diagnostic Platforms

Hospital-based Platforms - By Fitment Type (In Value%)

Standalone Systems

Integrated Systems

Modular Systems

Portable Systems - By End User Segment (In Value%)

Hospitals

Diagnostic Labs

Clinics

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Technology Adoption, Cost of Operation, Geographical Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

- Philippine Diagnostic Laboratory

Health Metrics, Inc.

Clinical Laboratories, Philippines

Med Tech Diagnostics

MediScan Laboratories

LifeLabs Philippines

MedTox Diagnostics

Labworks Philippines

Philippine Laboratory Services

Quest Diagnostics

Carewell Diagnostics

EastMed Diagnostics

MediPlus Healthcare

Unilab Diagnostics

BioMed Diagnostics

- Increased Demand for Diagnostic Services in Urban Areas

- Emerging Middle Class Driving Demand for Healthcare

- Rural Healthcare Development Projects

- Health Insurance Expansion Boosting Diagnostic Demand

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now