Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Differentials market is valued at approximately USD ~ billion based on a recent historical assessment, driven by increasing vehicle production, expanding logistics infrastructure, and rising demand for commercial and passenger vehicles. Growth is supported by higher adoption of all-wheel-drive systems and durable drivetrain components. Government-backed infrastructure projects and steady automotive assembly activities further contribute to consistent demand for differential systems across multiple vehicle categories.

Metro Manila, Cebu, and Calabarzon regions dominate the Philippines Differentials market due to strong automotive distribution networks, industrial clusters, and high vehicle density. These regions benefit from proximity to assembly plants, logistics hubs, and import terminals, enabling efficient supply chain operations. Additionally, urban expansion and commercial fleet growth in these areas continue to support higher demand for drivetrain components, reinforcing their dominance in the market landscape.

Market Segmentation

By Product Type

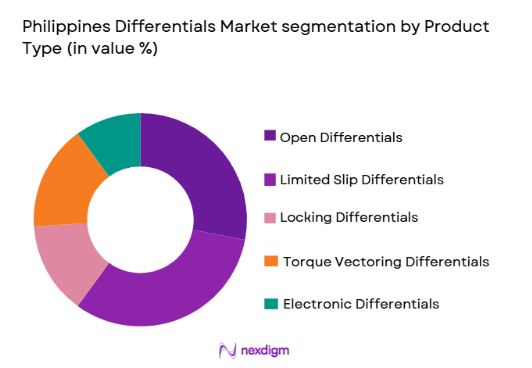

Philippines Differentials market is segmented by product type into open differentials, limited slip differentials, locking differentials, torque vectoring differentials, and electronic differentials. Recently, limited slip differentials have a dominant market share due to their superior traction control, adaptability in varying road conditions, and growing use in both passenger and commercial vehicles. Their increasing integration in modern vehicles, combined with improved performance efficiency and reduced wheel slippage, has made them highly preferred among OEMs and fleet operators. Additionally, infrastructure expansion and off-road vehicle demand further contribute to their higher adoption across the country.

By Vehicle Type

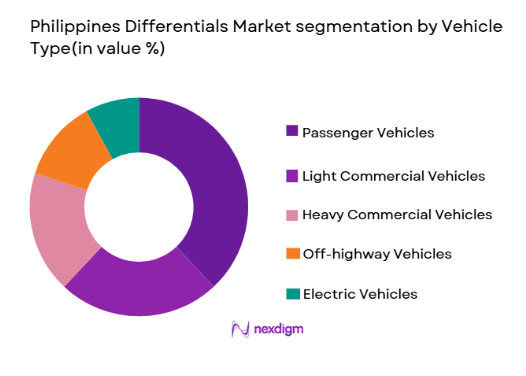

Philippines Differentials market is segmented by vehicle type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, off-road vehicles, and electric vehicles. Recently, passenger vehicles have a dominant market share due to increasing urbanization, rising disposable income, and higher private vehicle ownership. The growing middle-class population and preference for personal mobility solutions drive consistent demand in this segment. Furthermore, the expansion of financing options and dealership networks enhances accessibility, making passenger vehicles the largest contributor to differential system demand across the country.

Competitive Landscape

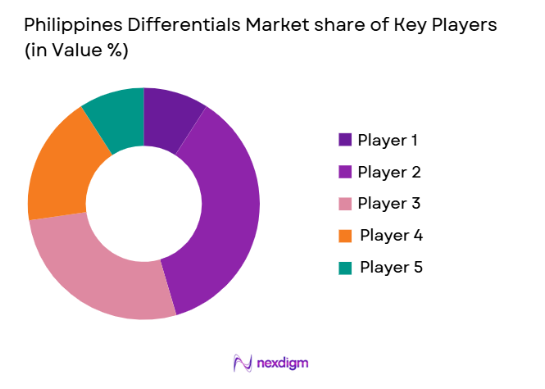

The Philippines Differentials market is moderately consolidated, with a mix of global automotive component manufacturers and regional distributors shaping the competitive environment. Large multinational companies dominate due to advanced technology capabilities, established supply chains, and strong OEM partnerships. Local players contribute through aftermarket services and distribution networks, creating competitive pressure in pricing and accessibility.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Distribution Strength |

| Dana Incorporated | 1904 | USA | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Aisin Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| BorgWarner Inc. | 1928 | USA | ~ | ~ | ~ | ~ | ~ |

| GKN Automotive | 1759 | UK | ~ | ~ | ~ | ~ | ~ |

Philippines Differentials Market Analysis

Growth Drivers

Expansion of Commercial Vehicle and Logistics Infrastructure:

The rapid development of logistics networks and e-commerce activities in the Philippines is significantly driving demand for durable and efficient drivetrain components, including differentials. Increased investments in transportation infrastructure such as highways, ports, and urban delivery systems are contributing to higher commercial vehicle usage. Fleet operators are expanding their vehicle base to meet rising demand for goods movement, which directly increases the need for reliable differential systems. Additionally, growing last-mile delivery services are creating sustained demand for light commercial vehicles. This trend encourages OEMs to integrate advanced differential systems that improve fuel efficiency and load handling. Government infrastructure programs further stimulate vehicle usage across construction and transport sectors. The need for enhanced traction and durability in heavy-duty vehicles supports increased adoption of advanced differential technologies. As logistics operations expand geographically, demand for robust drivetrain systems continues to rise. This sustained growth reinforces the importance of differentials in ensuring operational efficiency across transport networks.

Rising Adoption of Advanced Drivetrain Technologies in Passenger Vehicles:

The increasing preference for vehicles with enhanced performance, safety, and driving comfort is boosting the adoption of advanced differential systems in passenger vehicles. Consumers are increasingly opting for vehicles equipped with improved traction control systems, especially in urban and semi-urban environments. Automakers are integrating technologies such as electronic and torque vectoring differentials to enhance vehicle stability and efficiency. This shift is supported by growing awareness of vehicle performance features among buyers. Additionally, the rising demand for sport utility vehicles and crossover vehicles further contributes to the need for advanced drivetrain solutions. OEMs are focusing on innovation to meet consumer expectations for smoother and safer driving experiences. The availability of financing options and improved dealership networks supports higher vehicle sales. Urban congestion and varied road conditions also increase the importance of efficient differential systems. These factors collectively drive the integration of advanced differentials in modern passenger vehicles.

Market Challenges

High Cost and Complexity of Advanced Differential Systems:

The increasing sophistication of differential technologies, particularly electronic and torque vectoring systems, leads to higher production and maintenance costs. These advanced systems require precision engineering and specialized components, making them expensive compared to traditional differentials. This cost burden is often passed on to consumers, limiting adoption in price-sensitive markets. Additionally, maintenance and repair require skilled technicians, which are not widely available in all regions. Limited technical expertise can result in longer downtime and higher servicing costs. Supply chain disruptions for critical components further add to cost volatility. Small and medium automotive players may struggle to integrate these systems due to financial constraints. Import dependency also contributes to pricing challenges. These factors collectively hinder widespread adoption of advanced differential technologies across all vehicle segments.

Dependence on Imported Components and Supply Chain Vulnerabilities:

The Philippines automotive component industry heavily relies on imported differential systems and related components, exposing the market to supply chain risks. Fluctuations in global trade conditions and currency exchange rates can significantly impact procurement costs. Delays in shipments or disruptions in international supply chains can lead to production slowdowns. Local manufacturing capabilities for advanced drivetrain components remain limited, increasing reliance on foreign suppliers. This dependency reduces flexibility for OEMs and distributors in managing inventory. External geopolitical factors can further influence supply stability. Additionally, increased logistics costs add pressure on overall pricing structures. Limited domestic production infrastructure restricts technological advancement within the country. These challenges create uncertainty in supply consistency and cost management for market participants.

Opportunities

Growth of Electric Vehicle Drivetrain Integration:

The gradual shift toward electric mobility in the Philippines presents a significant opportunity for differential system manufacturers to innovate and adapt their products. Electric vehicles require specialized drivetrain systems that differ from traditional internal combustion engine vehicles. This creates demand for lightweight, efficient, and electronically controlled differential solutions. As government policies begin to support electric mobility adoption, manufacturers are encouraged to invest in new technologies. The integration of advanced differentials in electric vehicles enhances performance and energy efficiency. OEMs are exploring partnerships to develop compatible drivetrain components. The emergence of hybrid vehicle segments also contributes to increased demand. Technological advancements enable better torque distribution and vehicle stability. This evolving landscape opens new avenues for product differentiation and market expansion.

Expansion of Aftermarket Services and Replacement Demand:

The growing vehicle parc in the Philippines leads to increased demand for replacement parts, including differential systems. As vehicles age, the need for maintenance and component replacement becomes more frequent. Aftermarket players are expanding their distribution networks to cater to this demand. Independent service providers and workshops play a critical role in supporting vehicle maintenance. The availability of affordable replacement parts encourages consumers to extend vehicle lifespan. Additionally, rising awareness of preventive maintenance supports aftermarket growth. Digital platforms are also enhancing accessibility to automotive components. The expansion of service centers improves availability across urban and semi-urban areas. This creates sustained demand for differential systems beyond original equipment sales. The aftermarket segment thus represents a significant growth opportunity for market participants.

Future Outlook

The Philippines Differentials market is expected to witness steady growth driven by rising vehicle demand, infrastructure expansion, and technological advancements in drivetrain systems. Increasing adoption of electric and hybrid vehicles will reshape product innovation strategies. Government initiatives supporting automotive and logistics sectors will further enhance demand. Advancements in lightweight materials and electronic systems will improve efficiency. Overall, the market is poised for gradual transformation with strong emphasis on performance and sustainability.

Major Players

- GKN Automotive

- Dana Incorporated

- American Axle & Manufacturing

- ZF Friedrichshafen AG

- BorgWarner Inc.

- Eaton Corporation

- Schaeffler Group

- JTEKT Corporation

- Hyundai Wia Corporation

- Aisin Corporation

- Magna International Inc.

- Linamar Corporation

- Meritor Inc.

- NTN Corporation

- Mitsubishi Heavy Industries Automotive Components

Key Target Audience

- Automotive OEMs

- Fleet Operators

- Automotive Component Distributors

- Aftermarket Service Providers

- Construction and Mining Companies

- Agricultural Equipment Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research begins with identifying critical variables influencing the Philippines Differentials market such as vehicle production, drivetrain technology trends, and import dependency. These variables form the basis for analysis and forecasting.

Step 2: Market Analysis and Construction

Comprehensive data collection is conducted using industry databases, company reports, and government publications. The market structure is analyzed to determine segmentation, supply chain dynamics, and competitive positioning.

Step 3: Hypothesis Validation and Expert Consultation

Initial findings are validated through consultations with industry experts, manufacturers, and distributors. Feedback is incorporated to refine assumptions and ensure data accuracy.

Step 4: Research Synthesis and Final Output

All insights are synthesized into a structured format, ensuring consistency and reliability. Final outputs are developed with validated data and aligned with industry standards.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing vehicle production and ownership in urban and semi-urban regions

Expansion of logistics and transportation sectors driving commercial vehicle demand

Growing adoption of all wheel drive and off-road vehicles

Rising infrastructure development boosting construction vehicle usage

Technological advancements in drivetrain systems enhancing efficiency - Market Challenges

High cost of advanced differential systems limiting adoption

Supply chain disruptions affecting component availability

Limited local manufacturing capabilities increasing import dependency

Maintenance complexity in electronic differential systems

Fluctuations in raw material prices impacting production costs - Market Opportunities

Growth in electric vehicle drivetrain integration creating new demand avenues

Expansion of aftermarket services and replacement parts demand

Adoption of smart and electronically controlled differentials in premium vehicles - Trends

Shift toward lightweight materials improving fuel efficiency

Integration of electronic control units in differential systems

Rising popularity of torque vectoring technology in performance vehicles

Increasing demand for durable systems in commercial applications

Growth of hybrid drivetrain compatibility with advanced differentials - Government Regulations & Defense Policy

Vehicle safety and emission compliance standards influencing drivetrain systems

Import regulations impacting differential component sourcing

Infrastructure and transportation policies supporting commercial vehicle growth - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Open Differentials

Limited Slip Differentials

Locking Differentials

Torque Vectoring Differentials

Electronic Differentials - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Off-Road Vehicles

Electric Vehicles - By Fitment Type (In Value%)

Front Axle Fitment

Rear Axle Fitment

All Wheel Drive Fitment

Original Equipment Fitment

Aftermarket Fitment - By EndUser Segment (In Value%)

Automotive OEMs

Fleet Operators

Construction and Mining Companies

Agricultural Equipment Users

Aftermarket Service Providers - By Procurement Channel (In Value%)

Direct OEM Contracts

Authorized Dealers

Independent Distributors

Online Automotive Platforms

Government Procurement Programs - By Material / Technology (in Value %)

Cast Iron Differentials

Aluminum Alloy Differentials

Electronic Control Systems

High Performance Gear Systems

Advanced Lubrication Technologies

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Breadth, Pricing Strategy, Technology Integration, Manufacturing Capacity, Distribution Network Strength, Aftermarket Presence, Regional Reach, R&D Investment, OEM Partnerships, Supply Chain Efficiency)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

GKN Automotive

Dana Incorporated

American Axle & Manufacturing

ZF Friedrichshafen AG

BorgWarner Inc.

Eaton Corporation

Schaeffler Group

JTEKT Corporation

Hyundai Wia Corporation

Aisin Corporation

Magna International Inc.

Linamar Corporation

Meritor Inc.

Mitsubishi Heavy Industries Automotive Components

NTN Corporation

- Automotive OEMs focusing on integrating advanced drivetrain technologies

- Fleet operators prioritizing durability and cost efficient maintenance solutions

- Construction sector demanding heavy duty differential systems for rugged use

- Aftermarket players expanding distribution networks for replacement components

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now